Got an IRS Letter?

Don't Panic — Here's What to Do Next

Most IRS letters are not audits. Here's exactly how to read any notice, identify what type it is, and take the right action before the deadline passes.

You opened the mail and there it was — a letter from the IRS. Your stomach dropped. Before you do anything else, take a breath: the vast majority of IRS letters are routine notices, not audits. The IRS sends over 200 million notices every year. Most of them are math corrections, income verification requests, or balance reminders — fully resolvable with the right response and the right documentation.

The problem isn't the letter. The problem is what happens next: people panic, ignore it, or respond incorrectly — and a manageable issue becomes a complicated one. This guide walks you through exactly what to do, step by step, regardless of which notice you received.

Table of Contents

Most IRS Letters Are Not What You Think

Here is the reality of what the IRS actually sends: the overwhelming majority of notices are automated — generated by computer systems that compare data on your return to data reported by employers, banks, and 1099 payers. When numbers don't match, a notice goes out. That's it. No agent reviewed your file. No audit was triggered. A computer flagged a discrepancy.

200M+

IRS notices sent annually

The vast majority are automated and routine

~75%

Are math or income notices

CP2000, CP11, CP12 — usually resolvable

30 days

Typical response window

Missing it escalates the issue significantly

IRS notices fall into a handful of categories. Understanding which category your notice belongs to tells you almost everything about how urgent it is and what you need to do:

The IRS corrected an arithmetic error on your return. You may owe a small additional amount or receive a larger refund.

Income reported to the IRS by a third party doesn't match what's on your return. A response with documentation usually resolves it.

You owe taxes and payment hasn't been received. Urgency escalates with each subsequent notice.

The IRS is preparing to take collection action. These require immediate attention — same-day if possible.

The IRS wants to verify specific items on your return. Most are correspondence audits — handled by mail.

The single most important thing:Every IRS notice has a response deadline. Missing it doesn't make the notice go away — it makes your options narrower and your costs higher. Read the letter, find the deadline, and act before it passes.

The First 60 Seconds: What to Do Before Anything Else

Before you call anyone, search anything online, or start pulling records — do these four things in order. They take about 60 seconds and tell you almost everything you need to know about what you're dealing with.

Find the notice number

Look in the upper right corner of the letter for a code beginning with CP or LT (e.g., CP2000, LT11). This is the most important piece of information on the page — it tells you exactly what type of notice this is.

Find the tax year

IRS notices always reference a specific tax year. This tells you which return the IRS is looking at and which records you'll need to gather.

Find the response deadline

Look for a phrase like "Please respond by" or "You must respond within 30 days." Write this date down immediately. It's the most time-sensitive piece of information in the letter.

Find the amount at issue (if any)

Some notices propose a specific dollar amount you allegedly owe. Others are informational only. Knowing whether money is in dispute shapes how you respond.

Do not call the IRS first.The IRS phone lines are notoriously difficult to reach, and calling without understanding your notice type often wastes hours. Read the letter, identify the notice number, and understand what you're dealing with before picking up the phone. In many cases you'll resolve it entirely by mail without ever needing to call.

The STOP Framework: Four Steps for Any IRS Notice

Regardless of which notice you received, the same four steps apply. We call it the STOP Framework — not because you stop and do nothing, but because it's built around replacing the panic response with a deliberate, methodical one.

Stop and Read

Read the entire notice carefully before doing anything else. Find the CP or LT number in the upper right corner, the tax year referenced, and the specific issue the IRS is raising. Most people skim and miss critical details — including the deadline.

Track the Deadline

Every IRS notice has a response window — typically 30, 60, or 90 days. Write the deadline on your calendar the moment you find it. Missing a response deadline doesn't make the notice disappear; it eliminates your right to dispute the IRS's position and triggers escalation.

Organize Your Records

Pull the tax return for the year in question along with any documents the IRS is referencing — W-2s, 1099s, receipts, bank statements. In many cases the issue is a simple documentation mismatch that a single supporting document resolves.

Pick Your Path

You have three options with any IRS notice: agree and pay, dispute with documentation, or request more time. The right path depends on the notice type, whether the IRS is correct, and whether you have the documentation to support your position. When in doubt, engage a tax professional before responding.

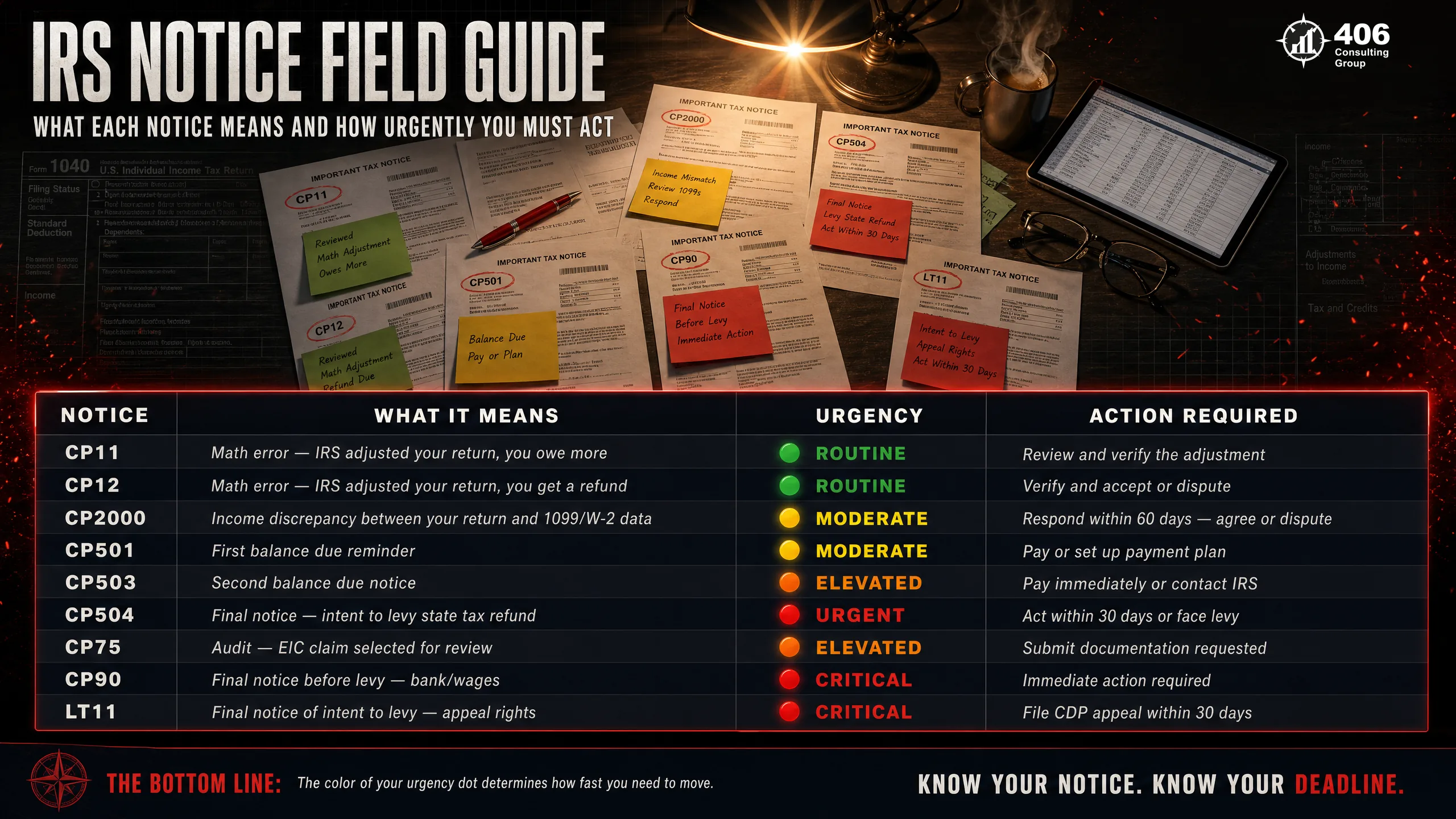

A Field Guide to Common IRS Notices

Use the notice number in the upper right corner of your letter to identify exactly what you're dealing with. Here are the most common notices Montana small business owners receive:

| Notice | What It Means | Urgency | Typical Action |

|---|---|---|---|

| CP11 / CP12 | Math error on your return — IRS made a change | Low | Review the change; respond if you disagree |

| CP2000 | Income on return doesn't match third-party reports | Medium | Agree, dispute, or partial agreement with docs |

| CP501 | First balance due reminder | Low–Medium | Pay balance or set up a payment plan |

| CP503 | Second balance due notice | Medium | Pay or contact IRS immediately |

| CP504 | Final notice — IRS may levy state refund | High | Pay in full or call IRS same day |

| CP75 / CP75A | Document request during return processing | Medium | Send requested documents by the deadline |

| CP90 / LT11 | Final notice before levy action | Critical | Call a tax professional immediately |

| CP523 | Installment agreement default notice | High | Respond immediately to avoid levy |

| Letter 525 | 30-day letter — audit proposed changes | Medium | Agree or file a protest with documentation |

| Letter 1058 | Final notice of intent to levy | Critical | Call a tax professional the same day |

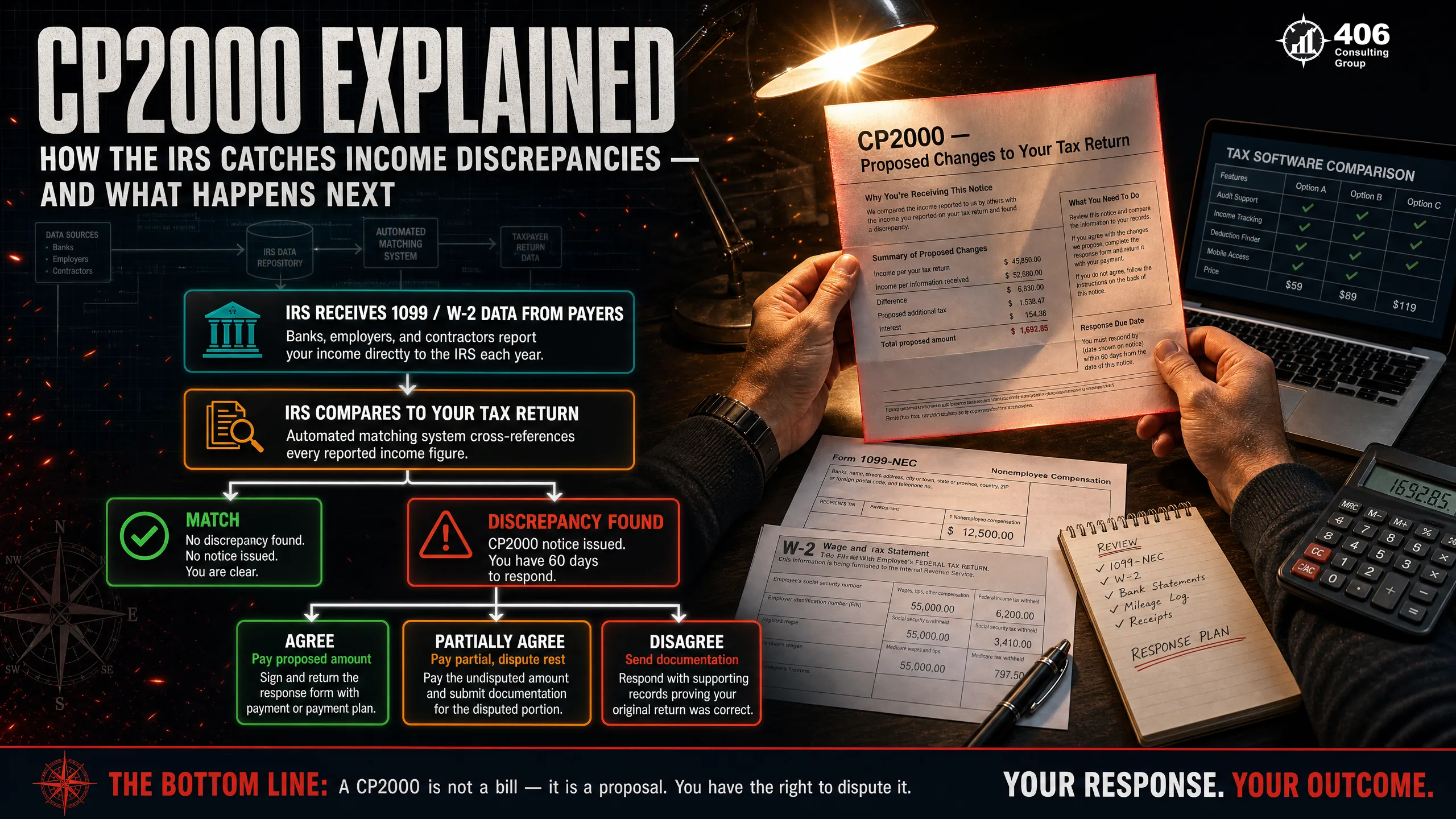

CP2000: The Most Common Notice — And Why It's Usually Fixable

The CP2000 is the IRS's most frequently issued notice. It's called an Underreporter Inquiry — it means the income reported on your return doesn't match what third parties (employers, banks, brokerages, clients) reported to the IRS. It is not an audit. It is a proposed change with a specific dollar amount the IRS believes you owe.

Common triggers for a CP2000:

You have three responses to a CP2000:

The IRS is correct. Sign the response form and pay the proposed amount (plus interest). The issue is closed.

You agree with some of the IRS's proposed changes but not all. Respond with documentation supporting the items you're disputing and pay the portion you agree with.

You have documentation proving the income was reported correctly, was not taxable, or the IRS's calculation is wrong. Respond in writing with supporting documents before the deadline.

Important:A CP2000 is a proposal, not a final determination. You have the right to dispute it — and with the right documentation, many CP2000 notices are reduced or eliminated entirely. The worst thing you can do is ignore it or agree without verifying the IRS's math.

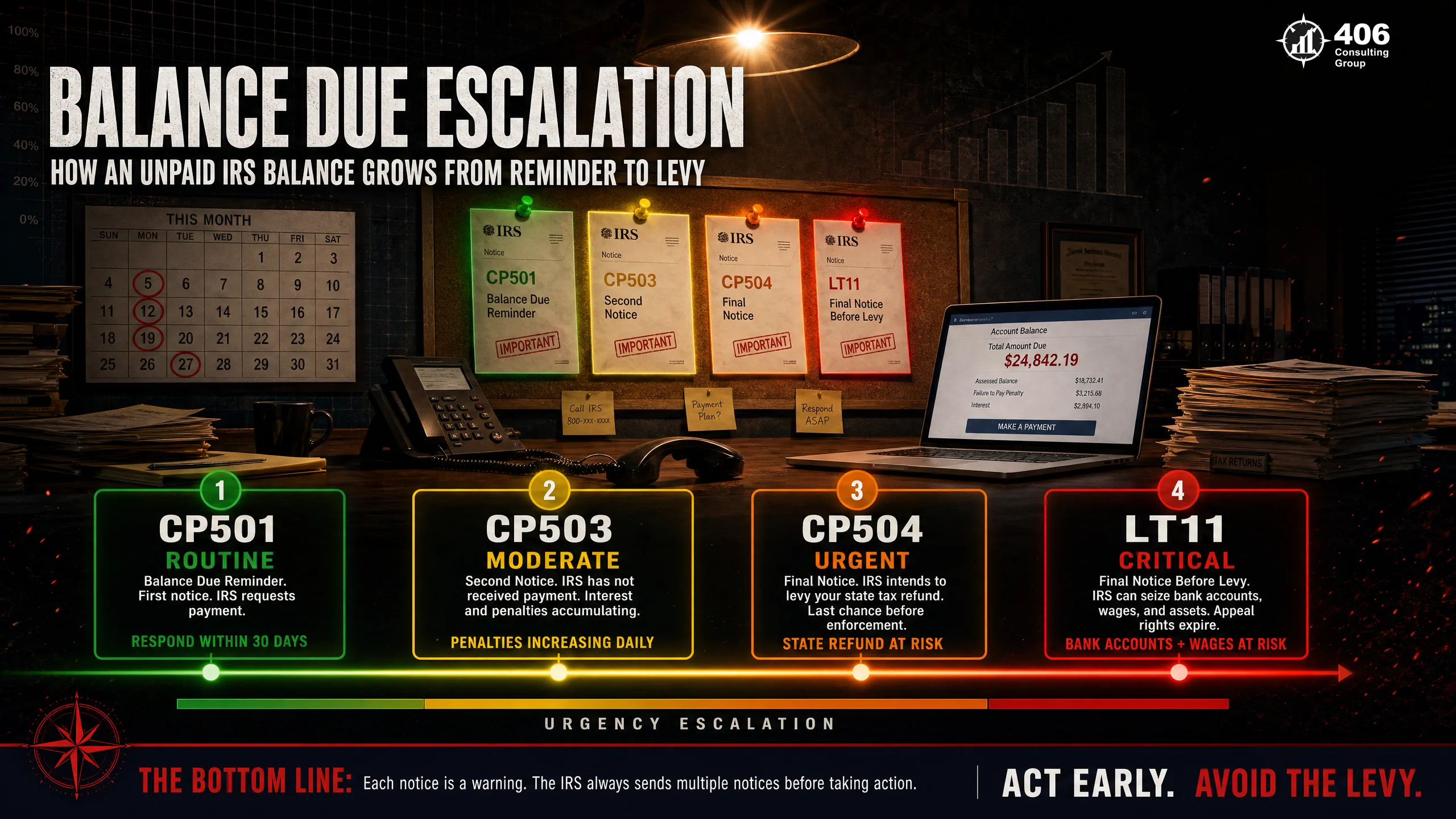

Balance Due Notices: How the Escalation Works

If you owe taxes and haven't paid, the IRS sends a series of escalating notices. Each one is more serious than the last — and at the fourth stage, the IRS has legal authority to take collection action without further notice.

CP501 — First Balance Due Reminder

The IRS is letting you know a balance is due. Penalty and interest are accruing. You can pay in full, set up a payment plan, or call to discuss options. This is the easiest and cheapest point to resolve the issue.

CP503 — Second Notice

The IRS did not receive payment or a response to CP501. The balance has grown with penalties and interest. Same options apply — but the longer you wait, the more you owe.

CP504 — Final Notice / Intent to Levy State Refund

This is a significant escalation. The IRS is notifying you it intends to levy (seize) your state tax refund. At this point, the IRS can also revoke your passport if the balance exceeds the seriously delinquent threshold (adjusted annually for inflation — verify current amount at IRS.gov). Act immediately.

LT11 / Letter 1058 — Final Notice Before Levy

This is the IRS's final warning. After this notice, the IRS can levy your bank accounts, garnish wages, and seize assets — without any additional warning. You have 30 days to respond. Call a tax professional today.

The Most Dangerous IRS Letters: When Time Really Is Running Out

Most IRS notices give you time. These do not — or give you very little. If you received any of the following, stop reading this article and call a tax professional today.

CP90 — Notice of Intent to Levy and Notice of Your Right to a Hearing

What It Means

The IRS is preparing to seize property — bank accounts, wages, real estate, vehicles. This notice simultaneously informs you of your right to request a Collection Due Process (CDP) hearing, which temporarily stops collection action.

Required Action

Request a CDP hearing immediately. You have 30 days from the date of the notice. Missing this window eliminates your appeal rights and allows the levy to proceed.

LT11 / Letter 1058 — Final Notice of Intent to Levy

What It Means

Functionally identical to CP90. The IRS has exhausted its standard notice sequence and is giving you one final opportunity to respond before taking collection action.

Required Action

Call a tax professional the same day. A CDP hearing request must be filed within 30 days. This is not a letter to sit on.

CP523 — Installment Agreement Default

What It Means

You had a payment plan with the IRS and a payment was missed. The IRS is terminating the agreement and may resume collection action immediately.

Required Action

Call the IRS or your tax professional immediately. In many cases a defaulted installment agreement can be reinstated — but only if you act quickly before collection action resumes.

Audit Notices: What They Actually Mean

The word "audit" triggers more fear than almost anything in personal finance. Here's the reality: most IRS audits are correspondence audits — handled entirely by mail, with no IRS agent ever reviewing your full return. You're asked to send specific documentation for specific line items. That's it.

Correspondence Audit

~75% of all audits

How: By mail only

Scope: Specific deductions or income items

Send requested documents by deadline. Most common audit type — the vast majority are resolved with a single documentation response.

Office Audit

~15% of audits

How: In-person at IRS office

Scope: Multiple items across the return

Bring the requested documents to an IRS office. Usually triggered by specific high-risk items. A tax professional should accompany you.

Field Audit

~10% of audits

How: IRS agent visits your location

Scope: Full return examination, often business records

The most comprehensive and rare audit type. Almost always involves a tax professional representing you. Do not handle alone.

Common Montana small business audit triggers: home office deductions, vehicle expense deductions, meals and entertainment (especially cash-heavy businesses), S-Corp reasonable compensation issues, and large deductions that are unusually high relative to industry revenue norms.

What a tax professional does in an audit that you can't: They communicate directly with the IRS on your behalf, know exactly which documents to provide (and which to withhold), understand IRS audit technique guides for your industry, and can negotiate an audit reconsideration if the initial outcome is unfavorable. Representing yourself in an office or field audit is almost never the right call.

How to Respond to an IRS Notice Correctly

Whether you agree or disagree with the IRS, how you respond matters as much as what you respond with. A poorly formatted, undocumented, or late response can turn a winning dispute into a losing one.

Respond in writing

Even if you call the IRS, follow up in writing. Written responses create a paper trail. Phone calls do not — and IRS agents can give incorrect information verbally with no accountability.

Use the response form if provided

Many notices (especially CP2000) include a response form. Use it. It tells the IRS exactly what you're agreeing or disagreeing with, and ensures your response is routed to the right department.

Include all supporting documents

Don't describe your documentation — attach it. W-2s, 1099s, receipts, bank statements, brokerage statements. Label each document and reference it in your letter.

Send by certified mail with return receipt

This creates a legal record that your response was sent and received before the deadline. Regular mail gives you nothing. If the IRS claims they didn't receive your response, certified mail is your proof.

Never send originals

Send copies only. Original documents sent to the IRS are frequently lost and nearly impossible to recover. Keep every original in your files.

Keep a complete copy of everything you send

Copy the entire response packet before mailing — your letter, every attachment, and the certified mail receipt. Store them with your tax records for at least 7 years.

Payment Options If You Actually Owe Money

If the IRS is correct and you do owe money, paying in full immediately stops interest and penalties from growing. But if you can't pay in full — or the amount is in dispute — you have more options than most people realize.

Installment Agreement (Payment Plan)

EasyEligibility

Most taxpayers who owe under $50,000 qualify automatically online

Best For

When you can pay the balance over time (up to 72 months) but not immediately

Key Note

Interest and penalties continue to accrue during the plan — the faster you pay, the less you owe total.

Currently Not Collectible (CNC) Status

ModerateEligibility

Financial hardship — income covers basic living expenses with nothing left for IRS payment

Best For

When paying anything would create genuine financial hardship

Key Note

Collection activity pauses, but the debt doesn't go away. The IRS reviews your situation annually.

Offer in Compromise (OIC)

HardEligibility

Strict — must demonstrate you cannot pay the full amount now or in the future

Best For

When the full balance is genuinely uncollectable given your income and assets

Key Note

The IRS accepts fewer than 40% of OIC applications. Most people who qualify for OIC would benefit from professional help preparing the application.

Penalty Abatement

ModerateEligibility

First-time abatement: no penalties in the prior 3 years. Reasonable cause: documented circumstance beyond your control

Best For

When penalties make up a significant portion of what you owe and you have a clean prior history

Key Note

Penalty abatement doesn't reduce the underlying tax or interest — only the penalties. But penalties can be substantial. First-time abatement is worth requesting for almost any taxpayer with a clean prior record.

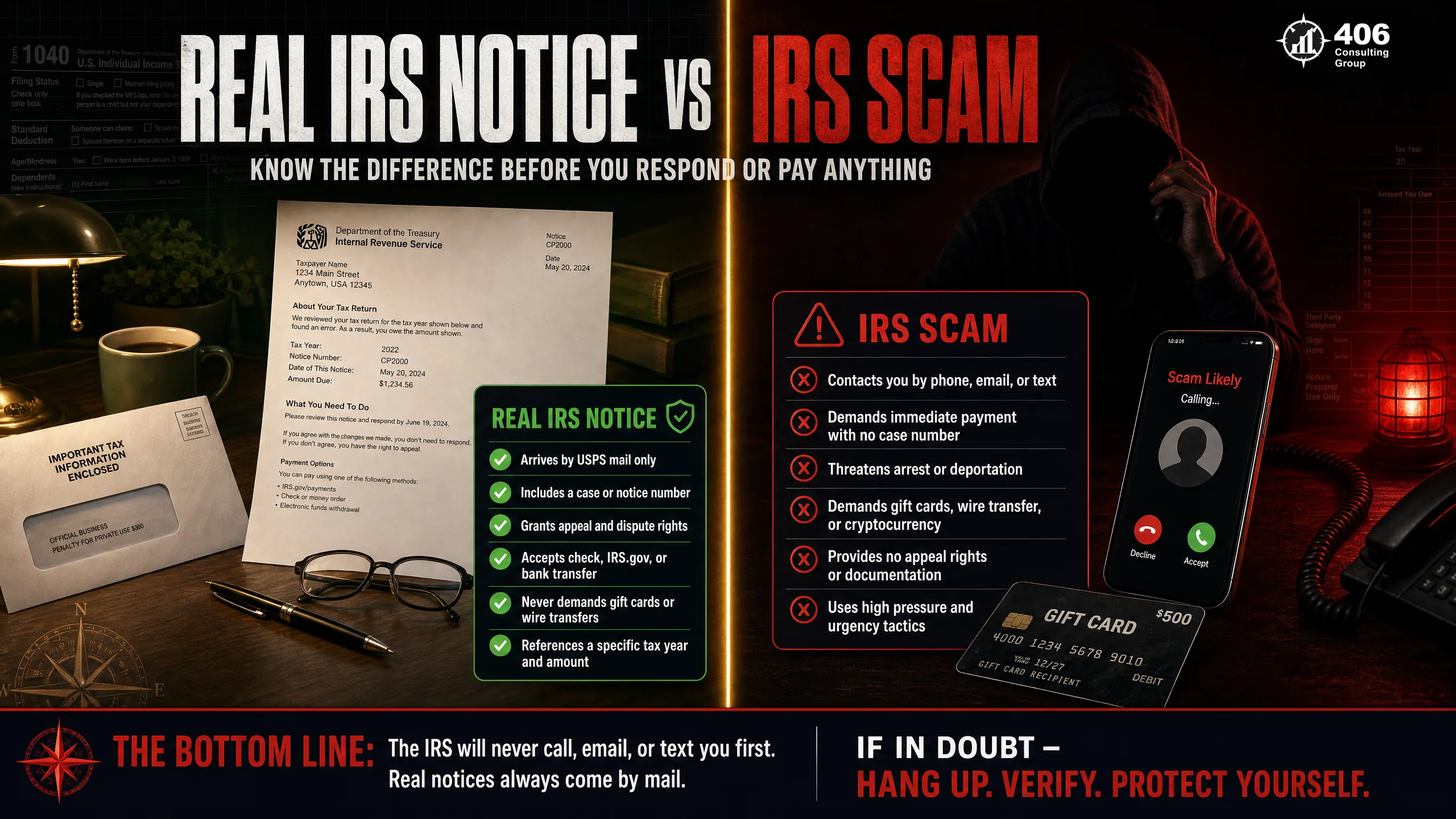

Real IRS Notice vs. IRS Scam: How to Tell the Difference

IRS impersonation scams are consistently among the most-reported consumer fraud categories tracked by the FTC. Before you respond to any contact claiming to be the IRS, verify it's real. The differences are clear once you know what to look for.

Real IRS Notice

- Always arrives by postal mail — never by email, text, or phone

- Includes a specific notice number (CP or LT) and case number

- References a specific tax year and dollar amount

- Always includes your right to appeal or dispute

- Accepts payment online at IRS.gov or by check — never gift cards or wire

- Never threatens immediate arrest or deportation

IRS Scam

- Contacts you by phone, email, or text claiming to be the IRS

- Demands immediate payment or threatens arrest within hours

- Requests payment by gift card, cryptocurrency, or wire transfer

- Refuses to provide a case number or written notice

- Threatens to send police, immigration, or law enforcement immediately

- Spoofs IRS phone numbers to appear legitimate on caller ID

Simple rule:The IRS will always contact you by mail first. If you haven't received a letter, any phone call or email claiming to be the IRS is a scam. Hang up, delete it, and report it to the Treasury Inspector General at 1-800-366-4484.

How to Prevent IRS Notices in the First Place

The best IRS notice is the one you never receive. Most notices are triggered by preventable errors — income mismatches, missed 1099s, math mistakes, and estimated payment gaps. The following habits eliminate the vast majority of notice risk.

Before You File

- • Collect every 1099 — NEC, MISC, B, INT, DIV, K — before preparing your return

- • Reconcile 1099 income to your accounting records; resolve discrepancies before filing

- • Report all income even when you didn't receive a 1099 — the IRS still knows

- • Verify your W-2 matches your last pay stub of the year

- • Check that your Social Security number and name match IRS records exactly

- • Have a tax professional prepare or review your return if you have business income

Year-Round Habits

- • Make quarterly estimated tax payments on time — underpayment triggers penalties

- • Keep business and personal finances completely separate

- • Document every deduction with a receipt and business purpose note at the time of purchase

- • Reconcile your books monthly so year-end is not a scramble

- • For S-Corp owners: pay yourself a documented reasonable salary — IRS scrutinizes this

- • Work with a tax professional who understands your industry and Montana-specific rules

For Montana contractors, construction companies, and self-employed business owners: the single highest-risk area for IRS notices is unreported 1099 income combined with large deductions. A tax professional who knows your industry reconciles your income sources before the return is filed — not after the notice arrives.

Frequently Asked Questions

How long do I have to respond to an IRS notice?

Most IRS notices give you 30, 60, or 90 days to respond — the deadline is stated on the letter. Some notices, like balance due reminders (CP501), have softer timelines but penalties and interest accrue daily. Levy notices (LT11, CP90) give you exactly 30 days before the IRS can take collection action. Write the deadline down the moment you open the letter and treat it as firm.

What happens if I ignore an IRS letter?

Ignoring an IRS notice is almost always the worst option. The IRS doesn't close cases because you didn't respond — it escalates them. An ignored CP2000 becomes a statutory notice of deficiency. An ignored balance due reminder becomes a levy notice. An ignored levy notice becomes a bank account seizure. Every stage of ignoring adds penalties, interest, and fewer options for resolution.

Can the IRS really levy my bank account?

Yes — but only after following the legal notice sequence. The IRS must issue a Final Notice of Intent to Levy (LT11 or CP90) and give you 30 days to respond before taking levy action. If you receive one of these notices and don't respond, the IRS can legally seize funds directly from your bank account, garnish wages, or place a lien on your property. This is why those specific notices require immediate attention.

How do I set up a payment plan with the IRS?

If you owe $50,000 or less in combined taxes, penalties, and interest (verify current threshold at IRS.gov), you can set up a streamlined installment agreement online without calling or visiting an IRS office. For balances over $50,000, or if you need a longer repayment term, you'll need to submit a Collection Information Statement (Form 433-F or 433-B for businesses). Interest and penalties continue accruing during the plan.

What's the difference between an audit and a CP2000?

A CP2000 is not an audit — it's an automated comparison of your return against third-party data. The IRS isn't questioning your judgment or examining your full return; it's flagging a specific income discrepancy. An audit (correspondence, office, or field) involves a broader examination of your return and requires providing documentation for specific deductions or income items. The CP2000 is more common and generally easier to resolve.

Does every IRS notice mean I owe money?

No. Some notices are purely informational — the IRS is letting you know about a change to your account that results in no additional tax. CP12 notices, for example, notify you that the IRS corrected a math error in your favor and you'll receive a larger refund. Always read the notice fully before assuming it means you owe something.

When should I hire a tax professional for an IRS notice?

For straightforward notices like CP2000 where you have the documentation and simply need to respond, many taxpayers handle it themselves. You should engage a tax professional when: the amount at issue exceeds $5,000, you disagree with the IRS and need to build a dispute case, you've received an audit notice, you received a levy or collection notice, you can't pay the full balance, or you're unsure what the notice means. The cost of a professional is almost always less than the cost of a mistake.

External Resources

Got a Notice?

We've Seen This Before — Let's Resolve It

Whether it's a CP2000, a balance due notice, or something more complex, 406 Consulting Group handles IRS correspondence for Montana small businesses. We know what the IRS is actually looking for — and how to respond in a way that resolves the issue cleanly.

The STOP Framework

4 steps for any IRS notice

Stop and Read

Find CP/LT number, tax year, deadline

Track the Deadline

Write it down — missing it costs you

Organize Records

Pull the return and supporting docs

Pick Your Path

Pay, dispute, or call a professional

Notice Urgency Quick Guide

When You Get a Notice: Checklist