S-Corp Tax Benefits:

Is It Worth the Switch for Your Montana Business?

Montana business owners ask about S-Corp elections every tax season. Here's the honest math — when it saves money, what it costs, and how to know if the switch is right for your situation.

In This Guide

- 1.What an S-Corp Election Is and Why Montana Owners Ask

- 2.How S-Corp Tax Savings Actually Work

- 3.The Montana S-Corp Break-Even

- 4.Montana-Specific Considerations

- 5.The Montana S-Corp Decision Matrix

- 6.What Changes After You Elect S-Corp Status

- 7.The Compliance Costs: What You're Taking On

- 8.Montana Industry Analysis

- 9.Timing: The March 15 Deadline

- 10.How to Evaluate Your Specific Situation

- 11.Case Study: Year-One S-Corp Savings

- 12.Frequently Asked Questions

Every tax season, Montana business owners ask the same question: should I switch to an S-Corp? The answer is almost never yes or no — it is a math problem. At some income levels, the S-Corp election saves $15,000 or more per year. At others, the compliance costs eat most of the savings and add complexity that is not worth it.

This guide covers exactly how the savings work, where the Montana-specific numbers change the analysis, and how to calculate whether the switch makes sense for your specific situation.

What an S-Corp Election Is and Why Montana Owners Ask About It

An S-Corp election is not a business structure — it is a tax classification. Your LLC or corporation remains exactly what it is. The IRS simply agrees to tax it differently: as an S-Corporation rather than as a sole proprietorship, partnership, or C-Corporation.

What stays the same

- Your Montana LLC operating agreement is unchanged

- Your liability protection remains intact

- Your bank accounts, contracts, and EIN remain the same

- Your Montana Secretary of State registration is unchanged

- Day-to-day business operations are unaffected

What changes

- How the IRS taxes your business profit

- You must pay yourself a W-2 salary as an owner-employee

- The business files its own federal and Montana tax return

- You must run formal payroll — quarterly deposits, W-2 at year-end

- Your bookkeeping and tax compliance complexity increases

Why Montana owners ask about it: Self-employment tax — the 15.3% tax that sole proprietors and LLC members pay on all net profit — is the single largest avoidable tax for most Montana small business owners. The S-Corp election is the primary legal mechanism for reducing it. The question is not whether it works. It is whether it works at your income level after accounting for what it costs to maintain.

How S-Corp Tax Savings Actually Work

Self-employment tax is 15.3% on net profit up to the Social Security wage base (verify current limit at IRS.gov), then 2.9% on everything above it. For a Montana LLC taxed as a sole proprietorship or partnership, every dollar of net profit is subject to this tax in addition to federal and Montana income tax.

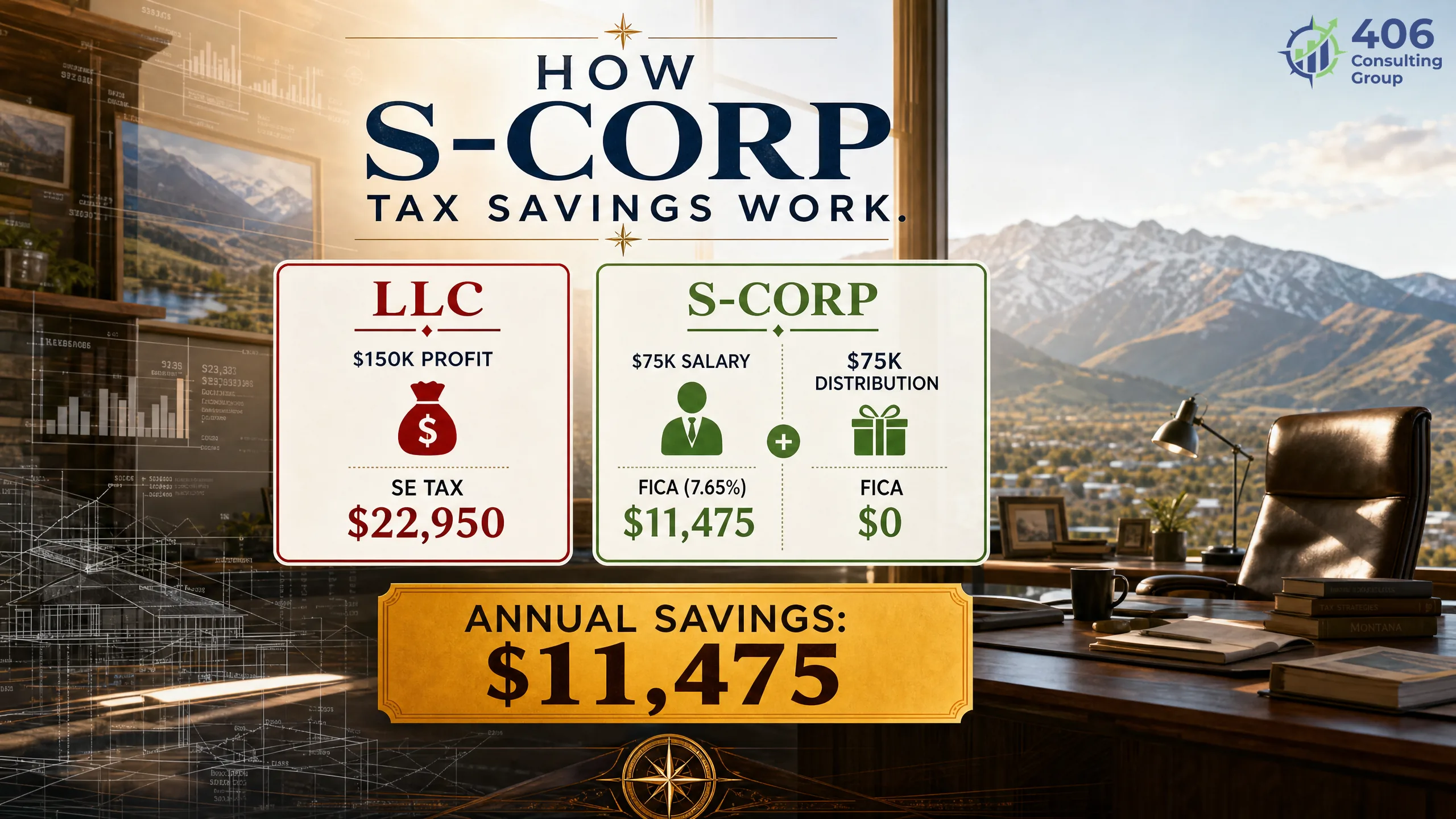

The Mechanics: $150,000 Net Profit Example

Without S-Corp Election (LLC)

With S-Corp Election

Annual SE Tax Savings: $21,194 − $11,475 = $9,719

Before subtracting S-Corp compliance costs (~$2,000–$4,000/year)

The critical variable:The owner's salary must be "reasonable compensation" — what you would pay someone else to do your job. The IRS actively audits S-Corps that set artificially low salaries to maximize distributions. A $30,000 salary for an owner running a $300,000 professional services firm is not defensible. A $75,000–$90,000 salary for the same firm probably is. The salary level determines everything — the savings math only works with a defensible number.

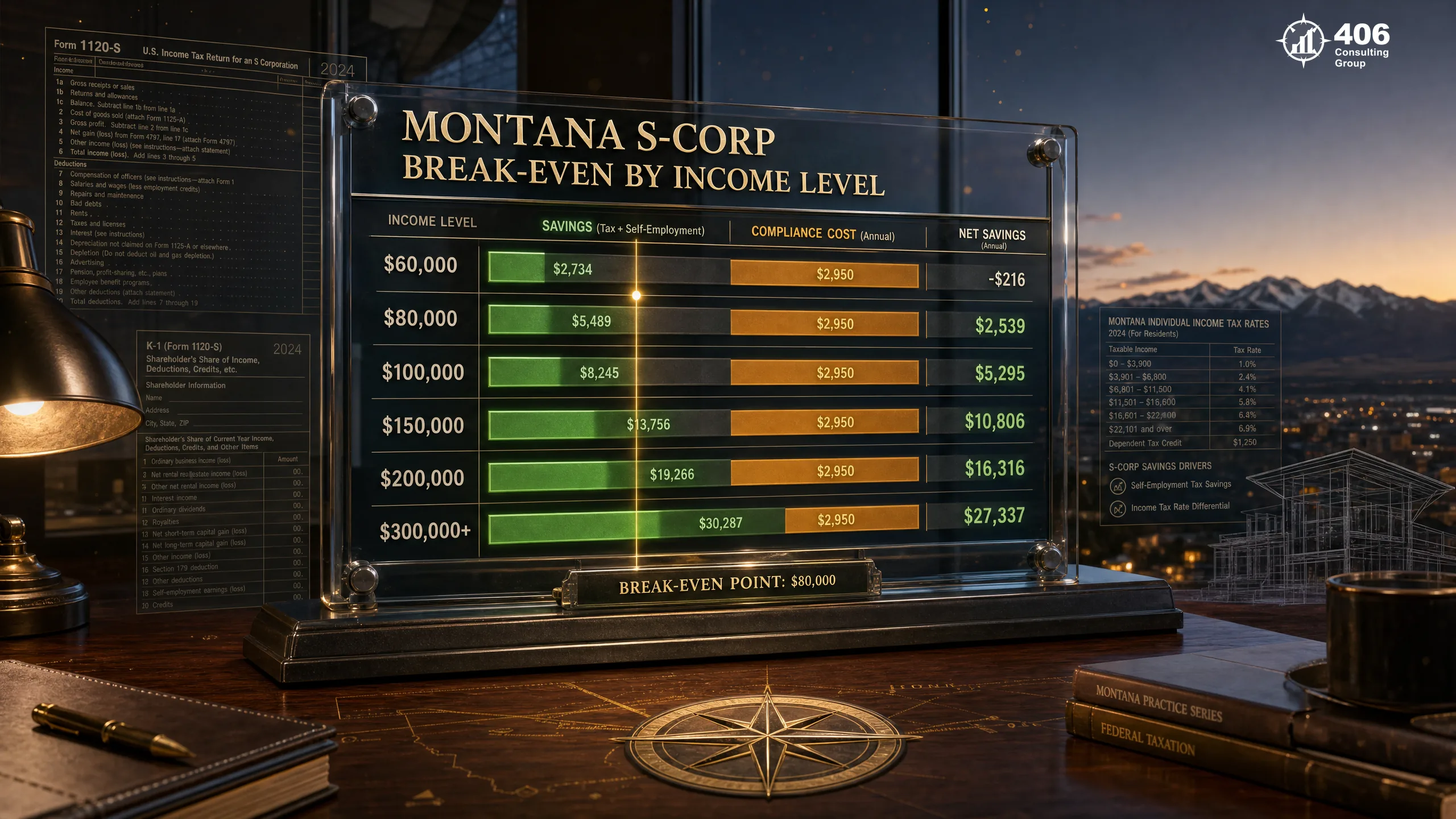

The Montana S-Corp Break-Even

The S-Corp election only makes financial sense when the SE tax savings exceed the additional compliance costs — payroll processing, S-Corp tax return preparation, and increased bookkeeping complexity. For most Montana businesses, that break-even point falls between $80,000 and $100,000 in net annual profit.

| Net Annual Profit | Estimated SE Tax Saved | Est. Compliance Cost | Net Annual Benefit | Verdict |

|---|---|---|---|---|

| $60,000 | $3,200 – $4,800 | $2,000 – $4,000 | $0 – $2,800 | Borderline |

| $80,000 | $5,500 – $7,000 | $2,000 – $4,000 | $1,500 – $5,000 | Likely Yes |

| $100,000 | $7,500 – $9,000 | $2,500 – $4,500 | $3,000 – $6,500 | Yes |

| $150,000 | $10,000 – $13,000 | $3,000 – $5,000 | $5,000 – $10,000 | Strong Yes |

| $200,000 | $13,000 – $17,000 | $3,500 – $5,500 | $7,500 – $13,500 | Strong Yes |

| $300,000+ | $16,000 – $22,000 | $4,000 – $6,000 | $10,000 – $18,000 | Strong Yes |

Important caveat:These are estimates based on typical reasonable salary levels and compliance costs. Your specific numbers depend on your industry, your defensible salary level, your current bookkeeper's fee structure, and whether your accountant charges separately for payroll and S-Corp returns. Run the analysis with your actual numbers before deciding.

Montana-Specific Considerations

The federal S-Corp savings analysis is the same regardless of which state you are in. But Montana has specific rules, tax rates, and compliance requirements that affect the total cost-benefit calculation. Here is what Montana business owners need to know that their out-of-state content did not tell them.

Montana income tax on S-Corp income

Montana taxes S-Corp income at the individual level, just like the federal government. Montana's top marginal income tax rate is 5.9%, with rates of 4.7%–5.9% based on income level (verify current rates at MTrevenue.gov). Both your salary income and your S-Corp distribution income are taxable at Montana rates on your individual return. The S-Corp election does not reduce your Montana income tax — it reduces your federal and Montana self-employment/payroll taxes only.

Montana S-Corp pass-through return (Form PTE)

A Montana S-Corp must file Form PTE (Montana Pass-Through Entity Tax Return — Form CLT-4S was discontinued after the 2018 tax year) each year in addition to the federal Form 1120-S. The Montana return is due the 15th day of the third month after the tax year ends — March 15 for calendar-year filers. Nonresident shareholders may owe composite tax. This is an additional filing your accountant must prepare, which is one component of the increased compliance cost.

No Montana franchise or privilege tax on S-Corps

Unlike some states (Texas, California, New York), Montana does not impose a franchise tax, privilege tax, or minimum annual tax on S-Corporations. California, for example, charges S-Corps a minimum $800 franchise tax annually plus 1.5% of net income. Montana has no equivalent. This makes the Montana S-Corp election more economically favorable than the same election in many other states.

Montana Secretary of State annual report

Every Montana business entity — including an LLC that has elected S-Corp status — must file an annual report with the Montana Secretary of State. The fee is $20 for most entities. Missing the annual report results in administrative dissolution of the entity. Your bookkeeper or accountant should have this on the compliance calendar.

Montana withholding for owner-employees

As an S-Corp owner-employee receiving a W-2 salary, you are subject to Montana income tax withholding on your wages — the same as any Montana employee. The S-Corp must register as an employer with the Montana Department of Revenue, withhold Montana income tax from your paycheck, and remit it quarterly. This is handled through your payroll processor if you use one.

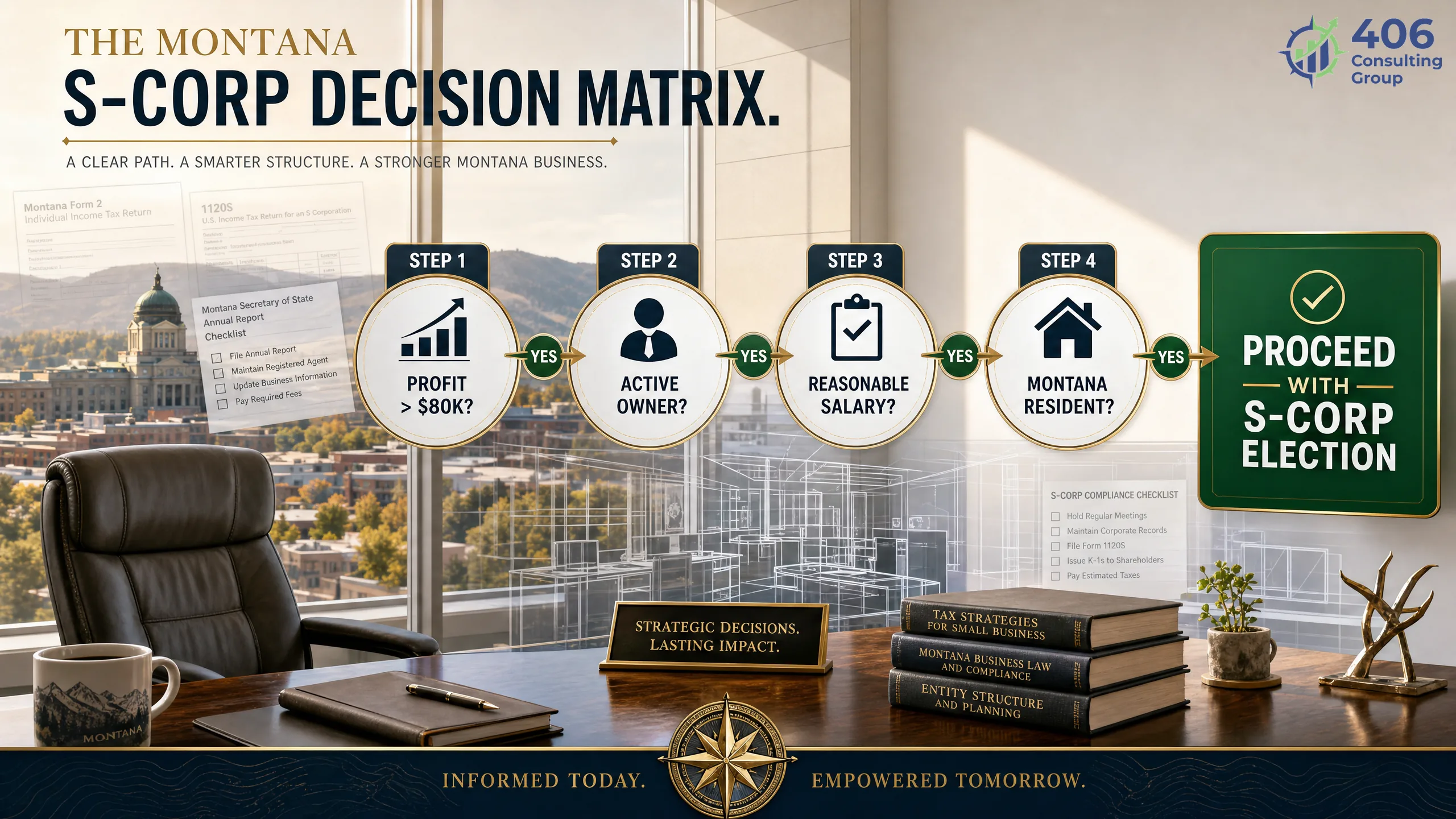

The Montana S-Corp Decision Matrix

The Montana S-Corp Decision Matrix is a four-factor evaluation framework. All four factors must score favorably for the election to make sense. If any one of them does not clear the threshold, the analysis typically comes back negative.

Net Profit Level

Pass

Net profit has been at or above $80,000 for at least two consecutive years and is expected to remain there

Fail

Net profit is below $80,000, highly variable year to year, or dependent on a single client that could leave

Consistency matters more than a single good year. An S-Corp election is a multi-year commitment — the compliance structure does not go away if you have a down year. Montana businesses with highly seasonal income or significant revenue concentration risk should model a below-average year before committing.

Reasonable Compensation

Pass

You can justify a salary of $60,000–$90,000 for your role and still have $40,000+ in distribution income after the salary

Fail

Your net profit is close enough to a market-rate salary that there is little or no distribution remaining after you pay yourself appropriately

The IRS's "reasonable compensation" standard is the most litigated issue in S-Corp audits. The salary must reflect what you would pay a non-owner employee to perform your functions. A Montana HVAC contractor running a one-person $120K-revenue operation might justify a $55,000 salary. A Missoula attorney at $200K net could not justify a $40,000 salary. When in doubt, document the comparable market data.

Compliance Cost

Pass

Additional payroll processing, S-Corp return preparation, and bookkeeping complexity cost less than $4,000/year and represent less than 30% of gross savings

Fail

Your current accountant charges significantly for payroll management, or the S-Corp return cost pushes total additional cost above 40% of gross savings

Compliance costs vary significantly by accountant and region. In Montana, a typical S-Corp package — payroll setup and processing, Form 1120-S preparation, Montana Form PTE, and additional bookkeeping — typically runs $2,500–$5,000 annually. Get a specific quote from your accountant before modeling the net savings.

Net Annual Savings

Pass

Factor 1 savings minus Factor 3 costs produce at least $3,000 in net annual benefit — enough to justify the added complexity and ongoing management attention

Fail

Net savings after compliance costs fall below $3,000, meaning the election saves less than $250/month — typically not worth the operational complexity

The $3,000 threshold is not a hard rule — it reflects the value of your time in managing the additional compliance, plus a margin for years when compliance costs run higher than expected. Some business owners set the bar at $5,000 because they want a larger cushion before adding complexity.

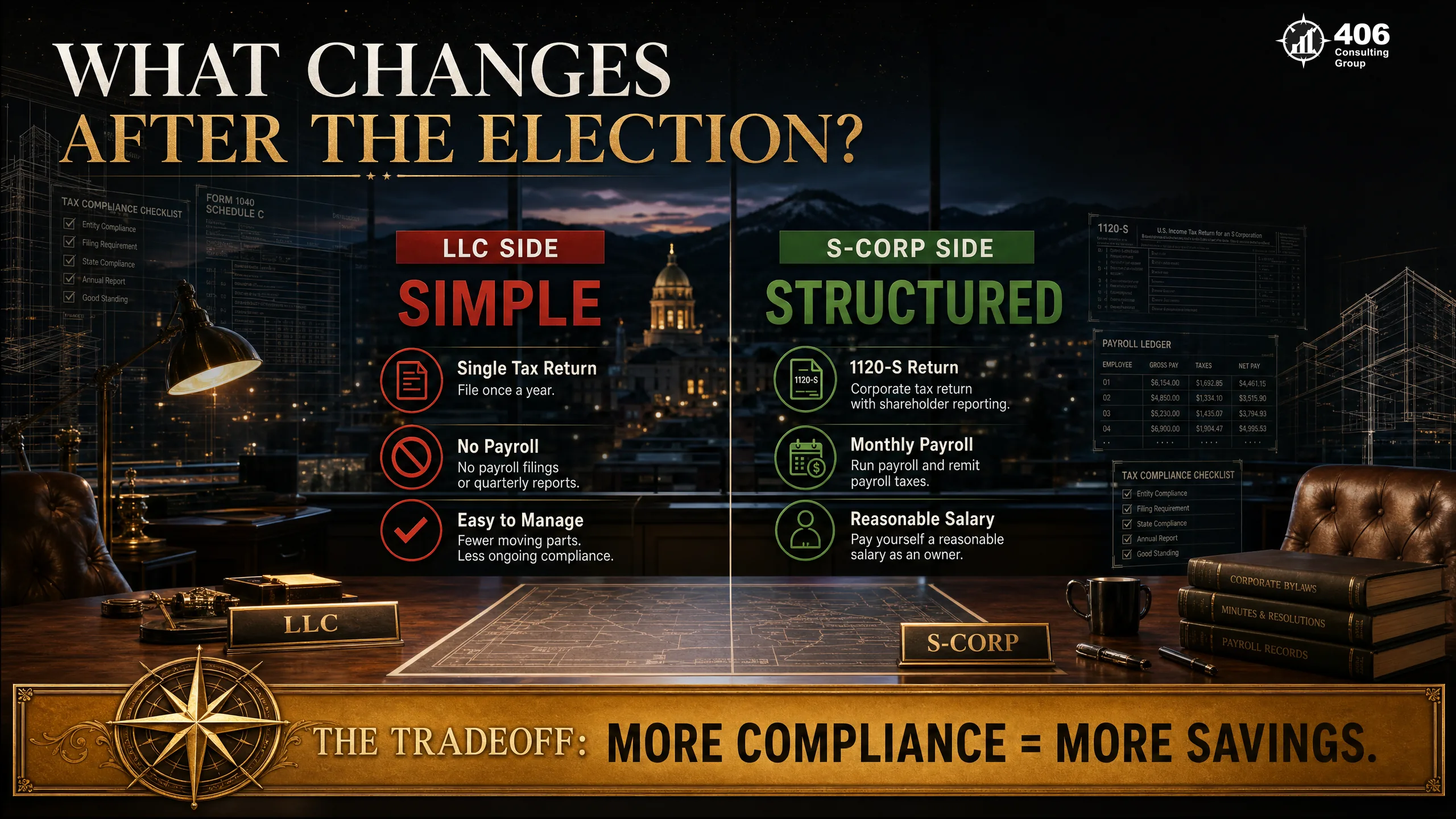

What Changes After You Elect S-Corp Status

Most S-Corp content focuses on the savings. Not enough of it covers what actually changes operationally when you make the election. Here is what shifts — and what Montana business owners are often surprised by in year one.

Before S-Corp Election (LLC)

- File Schedule C (sole prop) or Form 1065 (partnership) — no separate business return

- No payroll required — owner takes draws from the business account as needed

- No W-2 issued to yourself — no payroll tax deposits

- SE tax paid annually with your personal return (or quarterly estimated payments)

- Simpler bookkeeping — no payroll accounts, no payroll liability tracking

- One tax return: your personal Form 1040 (with business schedule)

After S-Corp Election

- File Form 1120-S (federal S-Corp return) + Montana Form PTE annually

- Must run formal payroll — at minimum, pay yourself a W-2 salary quarterly or more

- Issue yourself a W-2 at year-end; issue K-1 for distribution income

- Make federal payroll tax deposits (EFTPS) and Montana withholding remittances quarterly

- Additional bookkeeping: payroll accounts, payroll liabilities, owner equity split between salary and distribution

- Two returns: personal Form 1040 + S-Corp Form 1120-S (and Montana Form PTE)

The most common year-one mistake: S-Corp owners who continue to take irregular owner draws rather than setting up payroll. The IRS considers this a failure to pay reasonable compensation and can reclassify distributions as wages — imposing back payroll taxes, interest, and penalties that exceed the original tax savings. Payroll must be formal, timely, and consistent.

The Compliance Costs: What You're Actually Taking On

The compliance cost is the denominator in the S-Corp math. Get it wrong and your net savings calculation is wrong. Here is what Montana S-Corp compliance actually costs — broken into its components.

Payroll Processing

$600 – $1,800/yearRunning formal payroll for one owner-employee in Montana typically costs $50–$150/month through a payroll processor (Gusto, ADP, QuickBooks Payroll). This includes federal tax deposits via EFTPS, Montana withholding remittances, quarterly payroll tax returns (Form 941 federal), annual Montana withholding reconciliation (Form MW-3, due January 31), W-2 preparation, and unemployment insurance reporting. Some accountants include this in a bundled fee.

Federal S-Corp Tax Return (Form 1120-S)

$800 – $2,000/yearThe federal S-Corp return is a separate business tax return — more complex than a Schedule C and typically priced accordingly. For a simple one-owner Montana S-Corp with straightforward operations, expect $800–$1,400. Add partners, multi-state activity, or significant depreciation schedules and the fee rises to $1,500–$2,000+.

Montana S-Corp Return (Form PTE)

$200 – $600/yearSome Montana accountants include Form PTE preparation in the federal return fee; others charge separately. The Montana return is simpler than the federal 1120-S for most businesses, but it is a separate filing with its own deadline and signature requirement.

Additional Bookkeeping Complexity

$300 – $900/yearS-Corp bookkeeping requires tracking owner payroll, payroll tax liabilities, the distinction between salary income and distribution income on the equity schedule, and the S-Corp's basis — a running calculation that determines the taxability of distributions. If your bookkeeper charges by the hour or scope, expect a 10–20% increase in monthly fees.

Montana Annual Report

$20/yearA flat $20 fee to the Montana Secretary of State. Minor — but it must be on the compliance calendar.

Total Estimated Annual Compliance Cost

Low end (simple operations, bundled accounting)

High end (complex operations, separate service providers)

$1,920

$5,320

This is the hurdle your SE tax savings must clear to make the election worthwhile. Get a specific quote from your accountant before running the net savings calculation.

Montana Industry Analysis: Who Benefits Most

The S-Corp election works differently across industries because of two variables: how consistently net profit clears the break-even threshold, and how defensible a reasonable salary is in the owner's role. Here is how Montana's major industries map against those two variables.

Construction & Trades

Strong CandidateMontana GCs, electricians, plumbers, and HVAC contractors — particularly in Billings, Kalispell, and the Flathead Valley — frequently clear the $80K net profit threshold. Reasonable salary is well-documented by DOL wage data for trade occupations. The election is common and defensible in this sector.

Professional Services

Strong CandidateMontana consultants, engineers, architects, accountants, and other professionals at $100K+ net profit — including those in Great Falls, Kalispell, and Bozeman — typically benefit significantly. The salary must be set at market rate for the profession — which is well-documented and defensible.

Healthcare & Dental

Strong CandidateSolo practitioners and small practice owners with significant net income after overhead are frequent S-Corp beneficiaries. The salary range for physicians, dentists, and therapists is well-documented. The election is common in this sector.

Technology & Software

Good CandidateMontana tech consultants and remote software developers often benefit from the election. The salary must reflect the market rate for their technical role — which can be higher than local Montana wages for in-demand skills. Document with national or remote-work market data.

Hospitality & Tourism

VariableMontana's seasonal tourism economy creates highly variable annual profits. A lodge that nets $120K in a strong year and $50K in a bad year is a risky S-Corp candidate — the compliance structure must be maintained in lean years. Model the analysis on a below-average year.

Agriculture & Ranching

Case-by-CaseAgricultural operations have unique tax considerations — Section 179, bonus depreciation, Farm income averaging — that interact with the S-Corp election in complex ways. The election may make sense for some ag operations and not others. This analysis requires a tax professional who knows both agricultural and S-Corp tax law.

Timing: The March 15 Deadline, Late Elections, and Relief

The S-Corp election deadline is one of the hardest deadlines in the tax code. Miss it and your election takes effect in the following tax year — meaning you pay SE tax for an extra year unnecessarily.

The standard deadline

To have the S-Corp election apply for the current tax year, Form 2553 must be filed with the IRS by March 15 of that year (for calendar-year filers). The election can also be filed in the prior tax year — so you can elect in November 2024 for the 2025 tax year. A newly formed entity has until the 15th day of the third month after formation to file and have the election apply from the formation date.

Late election relief — Rev. Proc. 2013-30

The IRS provides relief for late S-Corp elections under Revenue Procedure 2013-30. If the business acted as if it were an S-Corp (filed as one, did not take actions inconsistent with S-Corp status) and the failure to timely file was due to reasonable cause — not willful neglect — the IRS will generally grant relief and treat the election as timely. This is not automatic. You must attach a statement explaining why the election was late and attest that the business operated as an S-Corp.

The best time to evaluate

The ideal window for evaluating an S-Corp election is Q4 of the prior year or January of the current year — before the March 15 deadline. A Q4 evaluation gives time to: project next year's net profit, get a formal quote from your accountant for S-Corp compliance costs, run the net savings calculation with actual numbers, and prepare Form 2553 thoughtfully rather than under deadline pressure. See our article on the S-Corp election deadline for the complete filing guide.

If you decide to elect: Do not file Form 2553 without your accountant reviewing it first. Common errors — wrong effective date, missing shareholder signatures, incorrect entity information — can invalidate the election. See our complete guide to the S-Corp election deadline for the full filing process.

How to Evaluate Your Specific Situation

The Montana S-Corp Decision Matrix gives you the framework. Here is how to run the actual numbers for your business in seven steps.

Pull your last two years of Schedule C (or K-1) net profit

You need at least two years to establish consistency. One strong year does not make an S-Corp election — if last year was unusually good, model on the two-year average.

Calculate the SE tax you paid on that profit

For net profit below $184,500 (2026 SS wage base — verify at IRS.gov each year): multiply by 92.35% (removes the employer deduction), then by 15.3%. For profit above that threshold: $184,500 × 15.3% + (excess × 2.9%). Your Schedule SE shows the exact amount.

Determine a defensible reasonable salary

Search the Bureau of Labor Statistics Occupational Employment and Wage Statistics for your occupation and your state. Search salary surveys for your industry (MGMA for physicians, AIA for architects, etc.). Document the data source — you will need it if the IRS asks.

Calculate the FICA on your proposed salary

Multiply the proposed salary by 15.3% (up to the SS wage base). This is what you will pay in total payroll taxes — split equally between your employer and employee tax obligations, both of which the S-Corp owes.

Calculate gross SE tax savings

Subtract Step 4 from Step 2. This is the gross employment tax savings from the election. Do not stop here — this number is the starting point, not the conclusion.

Get a compliance cost quote from your accountant

Ask specifically: What will you charge for payroll processing, Form 1120-S preparation, Montana Form PTE preparation, and any increase in monthly bookkeeping fees? Get a number, not a range.

Calculate net annual savings and decide

Subtract Step 6 from Step 5. If the result is at least $3,000 and the factors in the Decision Matrix all score favorably, the election is likely worth making. If it is below $3,000 or any matrix factor fails, wait or re-evaluate next year.

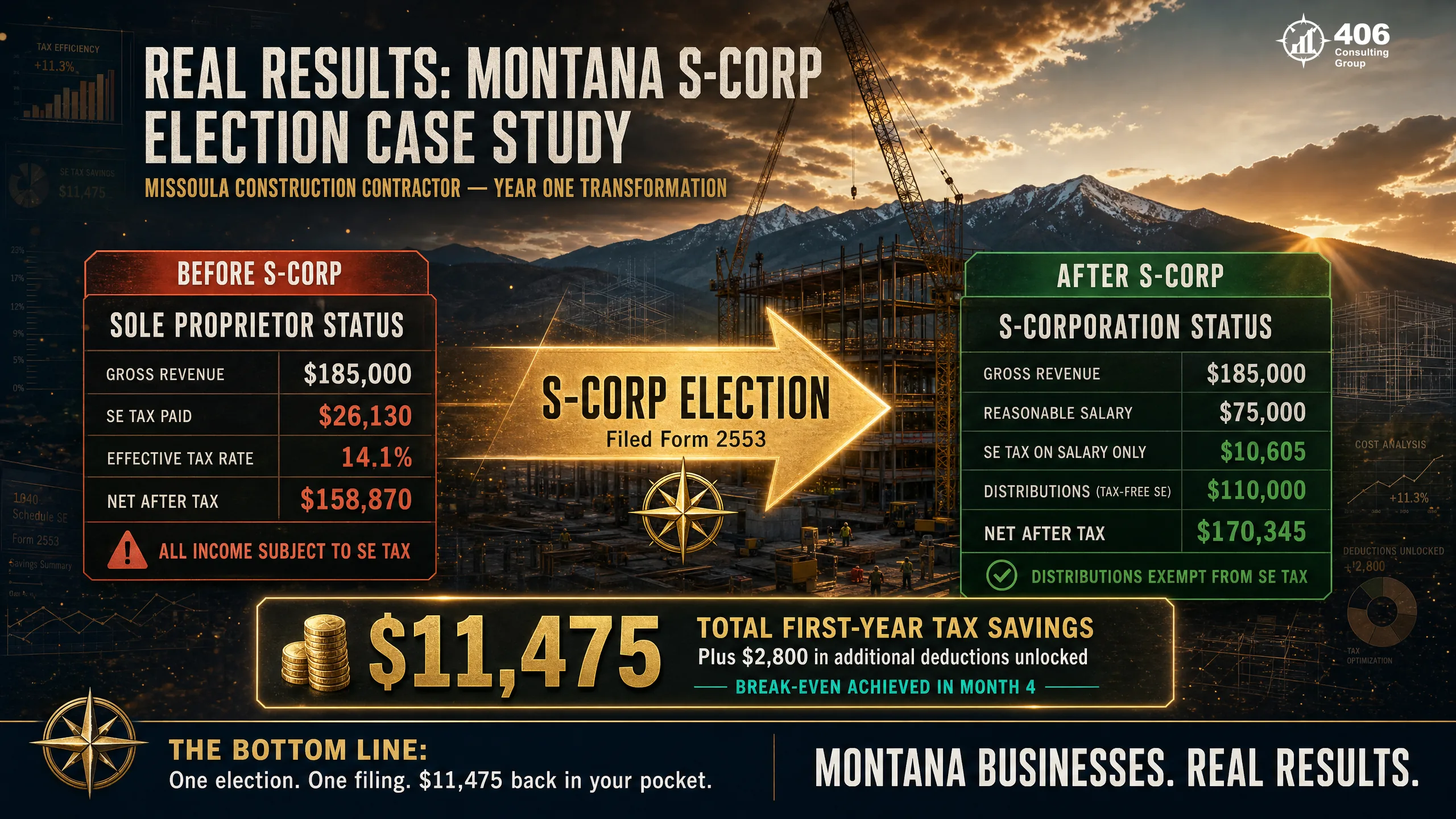

Case Study: Bozeman Contractor — Year-One S-Corp Savings

Anonymized — Bozeman, MT

General Contractor — S-Corp Election Year-One Analysis

Net annual profit (avg, 2 years)

$165,000

Owner role

Project manager + field lead

Reasonable salary established

$78,000

Before S-Corp (LLC, Schedule C)

After S-Corp Election

$11,406

Gross SE tax savings from election

$2,281

Annual compliance cost (payroll + S-Corp return)

$9,125

Net annual tax savings — year one

The 5-year picture: At $9,125 in net annual savings, this contractor is on track for $45,625 in cumulative tax savings over five years. The compliance cost of $2,281/year is 20% of the gross savings — well within the 30% threshold in the Decision Matrix. The salary of $78,000 was documented against Montana Department of Labor wage data for construction project managers (mean wage $74,540) and validated by industry salary surveys. Two years in, the election has not been challenged.

Frequently Asked Questions: S-Corp Tax Benefits in Montana

What is an S-Corp election and how does it work in Montana?

An S-Corp election is a tax classification filed with the IRS using Form 2553. It does not change your business entity — your Montana LLC remains an LLC. It changes how the IRS taxes your business income. Instead of paying self-employment tax (15.3%) on all net profit, you pay yourself a W-2 salary and pay payroll taxes only on the salary. The remaining profit is distributed as an S-Corp distribution, which is not subject to SE tax. Montana follows the federal S-Corp classification and requires a separate Montana pass-through entity return (Form PTE) in addition to the federal Form 1120-S.

At what income level does an S-Corp election make sense in Montana?

For most Montana businesses, the break-even point falls between $80,000 and $100,000 in net annual profit. Below $80,000, the SE tax savings typically do not exceed the additional compliance costs — payroll processing, S-Corp tax return preparation, and increased bookkeeping complexity — by a meaningful margin. Above $100,000, the savings generally produce a clear net benefit. The exact threshold depends on your specific compliance costs, which vary by accountant and service provider. Run the analysis with your actual numbers before deciding.

What is a 'reasonable salary' for an S-Corp owner in Montana?

Reasonable compensation is the salary you would pay a non-owner employee to perform your functions. The IRS uses this standard to prevent owners from setting artificially low salaries to maximize tax-free distributions. For Montana businesses, the Bureau of Labor Statistics Occupational Employment and Wage Statistics database provides state-level wage data by occupation. Professional associations also publish salary surveys for their industries. The reasonable salary is not arbitrary — it must be documented and defensible. A $40,000 salary for a Montana attorney at $250,000 in net profit is not defensible. A $90,000 salary for the same attorney probably is.

What are the ongoing compliance requirements for a Montana S-Corp?

A Montana S-Corp must: (1) run formal payroll for owner-employees — at minimum quarterly, with federal EFTPS deposits and Montana withholding remittances; (2) file federal Form 941 (quarterly payroll tax return); (3) issue W-2s by January 31; (4) file federal Form 1120-S by March 15; (5) file Montana Form PTE by March 15; (6) file the Montana Secretary of State annual report; and (7) maintain the bookkeeping complexity of tracking payroll accounts, payroll liabilities, and the salary/distribution split in owner equity. Most of this is manageable with a good bookkeeper and payroll processor, but it represents a meaningful step up from LLC compliance.

What is the deadline to elect S-Corp status in Montana?

The federal deadline to file Form 2553 for the current tax year is March 15 for calendar-year businesses. A newly formed business has until the 15th day of the third month after formation. If you miss the deadline, the IRS provides late election relief under Revenue Procedure 2013-30 for businesses that can demonstrate reasonable cause and that operated as if they were an S-Corp. For a complete guide to the S-Corp election filing process, see our article on the S-Corp election deadline.

Can I convert my existing Montana LLC to an S-Corp?

Yes — and you do not need to form a new entity. An existing Montana LLC simply files Form 2553 with the IRS to elect S-Corp tax treatment. The LLC structure, operating agreement, bank accounts, and Montana Secretary of State registration all remain unchanged. The only change is how the IRS taxes the entity's income. The election must be filed by March 15 to take effect for the current calendar year, or it applies to the following year.

Does 406 Consulting Group help with S-Corp elections in Montana?

Yes. 406 Consulting Group provides S-Corp election analysis, Form 2553 preparation, payroll setup, Montana Form PTE filing, and ongoing S-Corp bookkeeping and tax coordination for businesses across Montana and the Intermountain West. Carrie Anderson's background in commercial banking and tax strategy and Jason Anderson's operational finance experience are both relevant to the election analysis and year-one implementation. If you are evaluating whether an S-Corp election makes sense for your Montana business, we run the full Decision Matrix analysis as part of an initial consultation.

External Resources

Montana

Is the S-Corp Election Right for Your Montana Business?

406 Consulting Group runs the full Montana S-Corp Decision Matrix analysis and handles election filing, payroll setup, and ongoing S-Corp compliance for businesses across Montana and the Intermountain West.

Montana S-Corp Decision Matrix

All four factors must score favorably

Net Profit Level

Consistently $80,000+ per year

Reasonable Compensation

Defensible salary with meaningful distribution remaining

Compliance Cost

Less than 30% of gross SE tax savings

Net Annual Savings

Positive by at least $3,000 after costs

Quick S-Corp Savings Estimate

Your net annual profit

e.g., $120,000

Subtract reasonable salary

e.g., − $70,000

Distribution amount (no FICA)

= $50,000

Multiply distribution by 15.3%

= $7,650 saved

Subtract compliance cost

e.g., − $3,000

Net annual savings estimate

≈ $4,650/year

Related Reading

About the Author

Carrie Anderson

Tax Strategist, 406 Consulting Group

20+ years in commercial banking and tax strategy. Specializes in S-Corp election analysis, entity structure, and tax planning for Montana and Intermountain West businesses.

Is the S-Corp election right for your business?

We run the full Decision Matrix analysis and handle filing, payroll setup, and ongoing compliance.

Schedule a Consultation