Complete Guide to

Bookkeeping in Kalispell, MT

Kalispell businesses lose thousands annually to bad bookkeeping. Here's the complete guide to clean books, tax readiness, and financial clarity in the Flathead Valley.

Bookkeeping in Kalispell, MT isn't the same as bookkeeping in Phoenix or Atlanta. The Flathead Valley economy runs on construction, seasonal tourism, agriculture-adjacent businesses, and a high concentration of owner-operated companies with 1–20 employees. Most national bookkeeping advice is written for businesses that don't look anything like yours.

This guide covers what bookkeeping actually is, what it costs you when it's done wrong, how it connects to your taxes and your ability to borrow money, and exactly what good books look like every month. Whether you're doing your own books or evaluating whether to hand them off, this is the guide Kalispell business owners actually need.

Table of Contents

Why Bookkeeping in Kalispell Is Different

Flathead County is one of the fastest-growing counties in Montana — and that growth has created a business environment with very specific financial characteristics. Construction and trades are the backbone of the local economy. Tourism and hospitality create extreme seasonality. Agriculture-adjacent businesses run on cash and handshakes. And the majority of businesses are owner-operated, which means the owner is wearing five hats and bookkeeping is the one that most often gets dropped.

#1

Fastest-growing MT county

Flathead County by population, 2020–2024

68%

Owner-operated businesses

No dedicated finance staff to catch errors

$30K+

Average annual bookkeeping gap

Missed deductions + catch-up costs for Kalispell SMBs

The specific challenges that make Kalispell bookkeeping different from national norms:

Construction job costing

Revenue from a single job can span multiple months or years. Cash-basis bookkeeping makes it impossible to know whether a job was profitable until long after the work is done.

Seasonal revenue swings

Tourism and hospitality businesses may do 70% of annual revenue in four months. Books that look fine in August look alarming in January — unless your bookkeeper understands your seasonality.

High subcontractor volume

Flathead Valley construction businesses typically pay dozens of subcontractors annually. Misclassification between 1099 and W-2 is one of the IRS's top audit triggers — and it starts with how you categorize payments in the books.

No sales tax simplification

Montana has no sales tax, which removes one layer of bookkeeping complexity. But it also means out-of-state transactions, nexus questions for businesses with remote customers, and occasional Montana Department of Revenue surprises that businesses aren't prepared for.

Real example: A Kalispell contractor running $1.2M in revenue was fine on cash-basis bookkeeping until they applied for a $600K equipment line of credit. The lender required accrual-basis financials going back two years. Reconstructing two years of books in accrual format cost $14,000 and delayed the loan by four months. If their books had been done right from the start, it would have been a two-week approval.

What Bookkeeping Actually Covers (And What It Doesn't)

Most business owners use "bookkeeping," "accounting," "tax prep," and "CFO" interchangeably. They are four distinct functions — and conflating them is how businesses end up with someone doing none of them well. Here's what each actually means:

Bookkeeping

Recording every financial transaction, reconciling bank and credit card accounts, categorizing expenses correctly, and maintaining an accurate general ledger. This is the foundation everything else is built on.

Who: Bookkeeper or outsourced bookkeeping service

Frequency: Daily to monthly

Accounting

Interpreting the bookkeeping data to produce financial statements (P&L, balance sheet, cash flow), identifying trends, and producing analysis that informs business decisions.

Who: CPA or accountant

Frequency: Monthly to quarterly

Tax Preparation

Using the books and financial statements to prepare federal and Montana state tax returns. The quality of your books directly determines the quality of your tax return — and your tax bill.

Who: CPA or enrolled agent

Frequency: Annually (with quarterly estimates)

CFO / Controller

Using financial data to make strategic decisions: forecasting, budgeting, pricing, cash flow management, financing strategy, and financial modeling for growth plans.

Who: Fractional or full-time CFO

Frequency: Ongoing strategic advisory

The common trap: Asking your bookkeeper to also handle tax strategy and financial planning. Or asking your tax preparer to fix the books at year-end instead of maintaining them monthly. Each role requires different expertise — and trying to collapse them into one person or one annual event creates gaps in all four.

The Real Cost of Bad Books

Bad bookkeeping isn't free. It has a specific, measurable dollar cost — and for most Kalispell small businesses, that cost is higher than what professional bookkeeping would have cost in the first place. Here's where the money goes:

Missed deductions

$8,000 – $30,000/yearWhen expenses aren't categorized in real time, legitimate deductions get missed — vehicle mileage, home office, meals, equipment, subcontractor payments. These deductions don't exist unless they're in the books. A tax preparer working from a shoebox of receipts in March will miss deductions that a bookkeeper would have captured in April of the prior year.

Year-end catch-up bookkeeping

$2,000 – $12,000Reconstructing a year of books isn't just annoying — it's expensive. Bookkeepers typically charge $75–$150/hour for catch-up work, and a year of messy books for a business doing $500K+ in revenue can take 40–80 hours to untangle. That's on top of the higher tax prep bill that comes with disorganized records.

IRS notices and penalties

$500 – $25,000+The most common IRS notices — CP2000 underreporter inquiries — are triggered by income that appeared in third-party 1099 reports but wasn't captured in the books. Good bookkeeping reconciles every 1099 before the return is filed. Bad bookkeeping leaves gaps the IRS finds months or years later with interest accruing the entire time.

Loan denial opportunity cost

$50,000 – $500,000+Banks require 2–3 years of clean financial statements to approve commercial financing. Businesses with messy books either get denied or have to reconstruct their financials at significant cost. Meanwhile, the equipment purchase, expansion, or acquisition that would have generated returns sits on hold. This is the largest and most underappreciated cost of bad bookkeeping.

Real example:A Kalispell HVAC company doing $800K in revenue paid $22,000 more in taxes than necessary because their meals, vehicle, and home office expenses weren't tracked during the year. Their tax preparer had no documentation to support those deductions by March. A full year of outsourced bookkeeping would have cost $6,000 — and saved $22,000.

The Foundation Stack: 5 Layers Every Kalispell Business Needs

Good bookkeeping isn't a single activity — it's a stack of five interlocking layers. Each layer depends on the one below it. Skip a layer and everything above it becomes unreliable. We call this the Foundation Stack, and it's the framework we use to assess the health of any Kalispell business's financial systems.

Transaction Capture

Every dollar that moves — income, expense, transfer, payroll — is recorded in real time. Not at month-end. Not at tax time. In real time. This layer breaks when cash transactions go unrecorded, when personal and business accounts are mixed, or when expenses are paid from multiple accounts and only some of them make it into the books.

What breaks when this layer is missing

Missing revenue creates phantom profit. Missing expenses creates phantom loss. Both produce tax returns the IRS will want to discuss.

Reconciliation

Every bank account, credit card account, and line of credit is reconciled monthly — meaning every transaction in the books is matched to a corresponding bank statement entry, with zero unexplained differences. This is the layer most DIY bookkeepers skip or delay.

What breaks when this layer is missing

Unreconciled accounts drift from reality every month. Errors compound. By year-end, the difference between books and reality can be tens of thousands of dollars.

Chart of Accounts

The account structure in your bookkeeping software is designed for your business — not the QuickBooks default template. Revenue is broken into streams. Expenses are categorized specifically enough to support tax deductions, but not so granularly that the books become unmanageable. For construction businesses, this includes job-level categories.

What breaks when this layer is missing

A generic chart of accounts makes financial statements useless for decision-making. It also means deductions get lumped into categories the IRS doesn't accept.

Financial Reports

Monthly P&L, balance sheet, and cash flow statement are produced, reviewed, and understood. Accounts receivable aging is reviewed to identify slow-paying clients. These reports aren't produced once a year — they're produced every month within 10 days of month-end.

What breaks when this layer is missing

Without regular financial reports, you're flying blind. Businesses that only see their financials at tax time routinely discover problems (or opportunities) six months too late to act on them.

Tax-Ready Close

Books are formally closed each month with a reviewed trial balance. Year-end requires only a final review and adjusting entries — not a reconstruction. The tax preparer receives clean, reconciled financials by February rather than a box of receipts in March.

What breaks when this layer is missing

Without this layer, your tax preparer is doing bookkeeping at their hourly rate instead of doing tax strategy. The bill is higher and the outcome is worse.

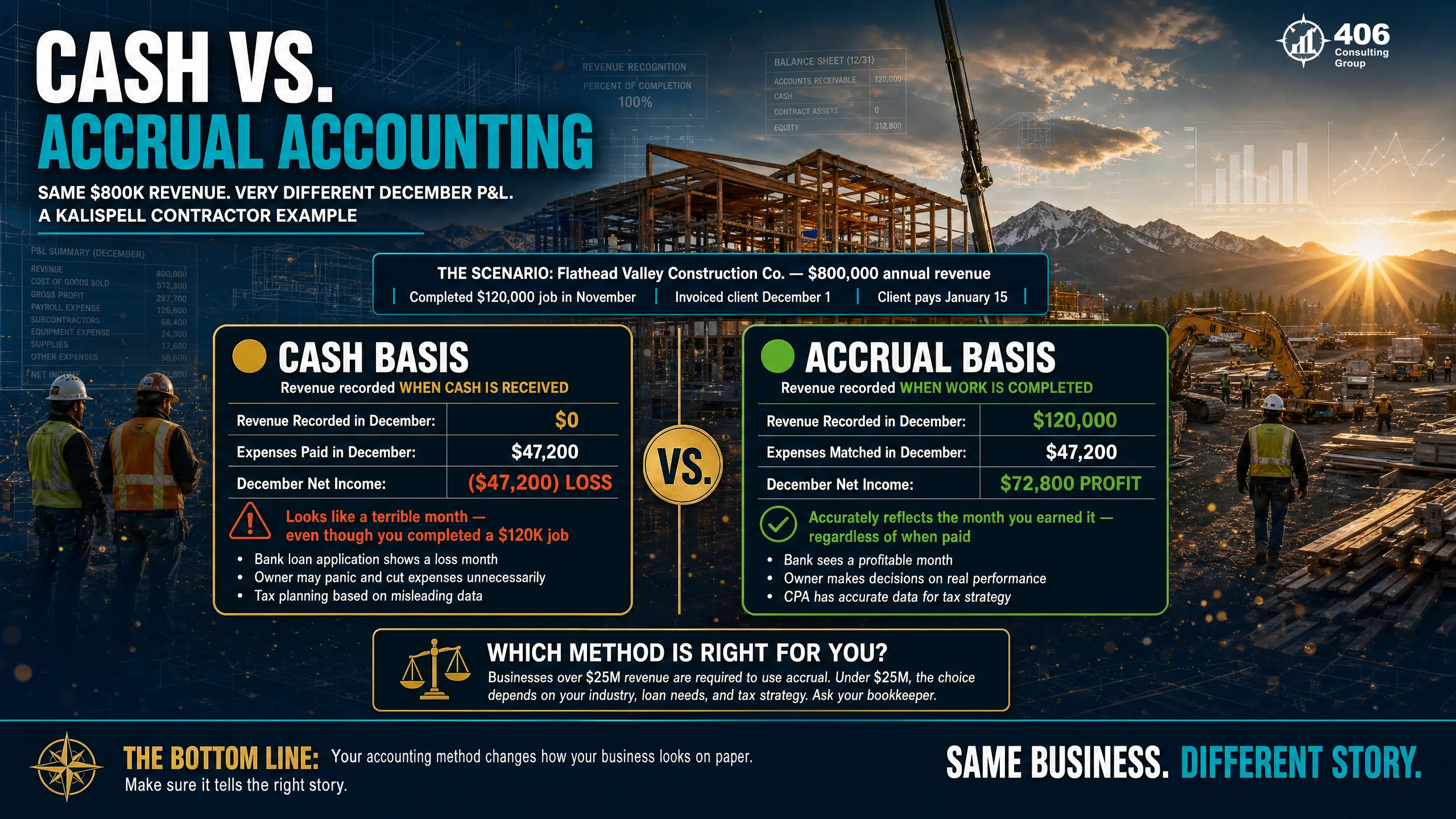

Cash vs. Accrual Accounting: Which Method for Your Montana Business

The accounting method you use determines when income and expenses are recorded — and it has a significant impact on your tax liability, your financial statements, and your ability to get financing. Here's what each method actually means in plain language:

Cash Basis

Best for: Sole proprietors, service businesses under $500K, simple retail“Record income when you receive the payment. Record expenses when you write the check or swipe the card.”

Advantages

- Simpler to maintain

- Matches cash in your bank account

- Lower tax liability in some situations (defer income to next year)

- Acceptable for most businesses under $5M in gross receipts

Limitations

- Doesn't show true profitability on long-running jobs

- Monthly P&L doesn't reflect when work was actually done

- Most lenders won't accept cash-basis financials for loans over $250K

- Required to convert to accrual if you carry inventory over a threshold

Accrual Basis

Best for: Businesses over $500K–$1M, construction, any business seeking bank financing“Record income when it's earned (invoice sent), regardless of when payment arrives. Record expenses when they're incurred, regardless of when the check clears.”

Advantages

- Shows true profitability by period

- Required by GAAP and most commercial lenders

- Accurate job-level P&L for construction

- Better for businesses with significant receivables or payables

Limitations

- More complex to maintain

- Tax liability can arise before cash is received

- Requires understanding of accounts receivable and payable

- Higher bookkeeping complexity and cost

Montana-specific note: The Montana Department of Revenue follows federal accounting method elections. If you make a change in accounting method, it generally requires filing IRS Form 3115. Switching from cash to accrual mid-stream without proper documentation creates reconciliation problems that can take months to untangle. Make the switch intentionally, with a bookkeeper and tax preparer aligned on the transition.

Industry Spotlight: Bookkeeping for Kalispell's Dominant Sectors

Kalispell's economy is concentrated in a handful of sectors, each with specific bookkeeping requirements that generic advice misses. Here's what good books look like in each:

Construction & Trades

Kalispell sector- 1Job costing — every job needs its own cost center so you know if each job was profitable

- 2WIP (Work in Progress) schedule — required for lenders, tracks revenue and costs across open jobs

- 3Retainage receivable — money withheld by GCs until project completion must be tracked separately

- 4Subcontractor 1099 tracking — every sub paid over $600 requires a 1099-NEC; books must capture this in real time

- 5Equipment depreciation — proper depreciation schedules are both a tax strategy and a balance sheet requirement

A Kalispell GC doing $2M+ needs job-costing software or QuickBooks with class tracking — standard bookkeeping templates don't cut it.

Hospitality & Tourism

Kalispell sector- 1Seasonal revenue modeling — monthly P&L comparisons should be to prior-year same-month, not prior month

- 2Tip income tracking — whether tips are pooled, distributed, or individual, they create payroll and bookkeeping complexity

- 3Occupancy tax — Montana lodging businesses collect and remit bed tax; it must be tracked as a liability, not revenue

- 4Food & beverage inventory — COGS tracking requires periodic inventory counts that feed into the books

- 5Off-season cash flow — books must show lenders that the business can survive the slow months

Many Kalispell lodging businesses understate their off-season liabilities, which creates surprises that clean books would have made visible in October.

Retail & Product-Based

Kalispell sector- 1Inventory valuation — FIFO vs. average cost method affects COGS and therefore taxable income

- 2COGS tracking — every product sold needs a corresponding cost recorded; this requires inventory bookkeeping

- 3No Montana sales tax — one significant simplification, but out-of-state sales to customers in other states may trigger economic nexus

- 4Vendor terms and accounts payable — extended payment terms must be tracked in accrual-basis books

- 5Shrinkage and write-offs — inventory losses must be documented and recorded to be deductible

Montana's lack of sales tax is a real advantage — but businesses with e-commerce or out-of-state revenue need to track nexus thresholds in other states.

Professional Services

Kalispell sector- 1Accounts receivable aging — service businesses are often slow to collect; AR over 90 days is a cash flow warning

- 2Retainer and prepaid revenue — income received before services are rendered is a liability, not revenue

- 3Mileage and home office — the two most commonly missed deductions for consultants and independent professionals

- 4S-Corp reasonable compensation — for S-Corp owners, IRS requires a documented reasonable salary; the books must reflect this correctly

- 5Quarterly estimated taxes — owners must track net income monthly to calculate accurate quarterly payments

For healthcare practices and legal offices with billing cycles, the gap between service delivery and payment receipt requires accrual accounting to see true profitability.

Bookkeeping and Tax Preparation: How Clean Books Save You Money

Your tax return is only as good as your books. This is the most direct and underappreciated connection in small business finance — and it's why the quality of your bookkeeping has a direct dollar impact on your April tax bill.

Year-End Reconstruction (What Most Businesses Do)

Tax time arrives in February. Books haven't been touched since last April. Your tax preparer receives bank statements, a shoebox of receipts, and a Venmo history.

The preparer spends 8–15 hours reconstructing the books — at their billing rate. That's $800–$2,500 in bookkeeping fees billed at accounting rates.

With limited time and incomplete documentation, they take conservative positions on deductions: the gray areas don't get claimed. Vehicle mileage with no log — not deducted. Home office without measurement — not claimed. Meals with no documented business purpose — skipped.

Result: Higher tax prep bill. Lower deductions. Higher tax liability.

Monthly Bookkeeping (The Right Approach)

Books are closed monthly. Every transaction is categorized in real time. Vehicle mileage is tracked in the app as it happens. Meals have business purpose notes attached at the time of purchase.

Tax preparer receives a clean trial balance and reconciled financials in early February. They spend 2–4 hours on tax strategy — not bookkeeping reconstruction.

With full documentation, every legitimate deduction is claimed. The preparer has time to identify tax planning opportunities: S-Corp election, depreciation elections, retirement plan contributions, timing of income and expenses.

Result: Lower tax prep bill. Maximum deductions. Optimized tax liability.

The compounding benefit: We've helped Kalispell business owners cut their tax preparation bill by 30–40% and reduce their tax liability by $8,000–$20,000 simply by switching from year-end reconstruction to monthly bookkeeping. The bookkeeping cost is offset within the first year by the reduction in tax prep fees and recovered deductions alone.

Bookkeeping and Loan Readiness: What Flathead Valley Lenders Actually Need

When a Kalispell business owner walks into Glacier Bank, Flathead Bank of Commerce, or any other local lender to apply for a commercial loan, the first thing the underwriter asks for is two to three years of financial statements. What happens next depends entirely on the quality of the books those statements came from.

Having spent years underwriting commercial loans for a local Montana bank, we know exactly what lenders are looking for — and what causes deals to stall or die. The details are covered in depth in our article on what banks actually look at for a commercial loan. The short version as it relates to bookkeeping:

Clean P&L statements for 2–3 years

Lenders need to calculate your debt service coverage ratio (DSCR) — your net operating income divided by your debt payments. If your P&L has personal expenses mixed in, intercompany transfers unexplained, or income that doesn't match your tax returns, the underwriter will flag every line item and your loan timeline extends by weeks.

Balance sheets that tie to your tax returns

One of the most common problems we see: the company balance sheet shows assets and liabilities that don't match what was reported on the business tax return. Lenders reconcile these documents — discrepancies kill deals or require expensive explanations.

Accounts receivable aging

For businesses with significant receivables (contractors, service businesses), lenders want to see an AR aging report. Receivables over 90 days are typically excluded from collateral calculations. If you've never run an AR aging report, you don't know how much of your "revenue" is actually collectible.

No personal/business account commingling

The single fastest way to kill a commercial loan application is for the underwriter to find personal expenses in the business account — or business deposits in the personal account. Clean separation of personal and business finances isn't just good bookkeeping practice; it's a loan requirement.

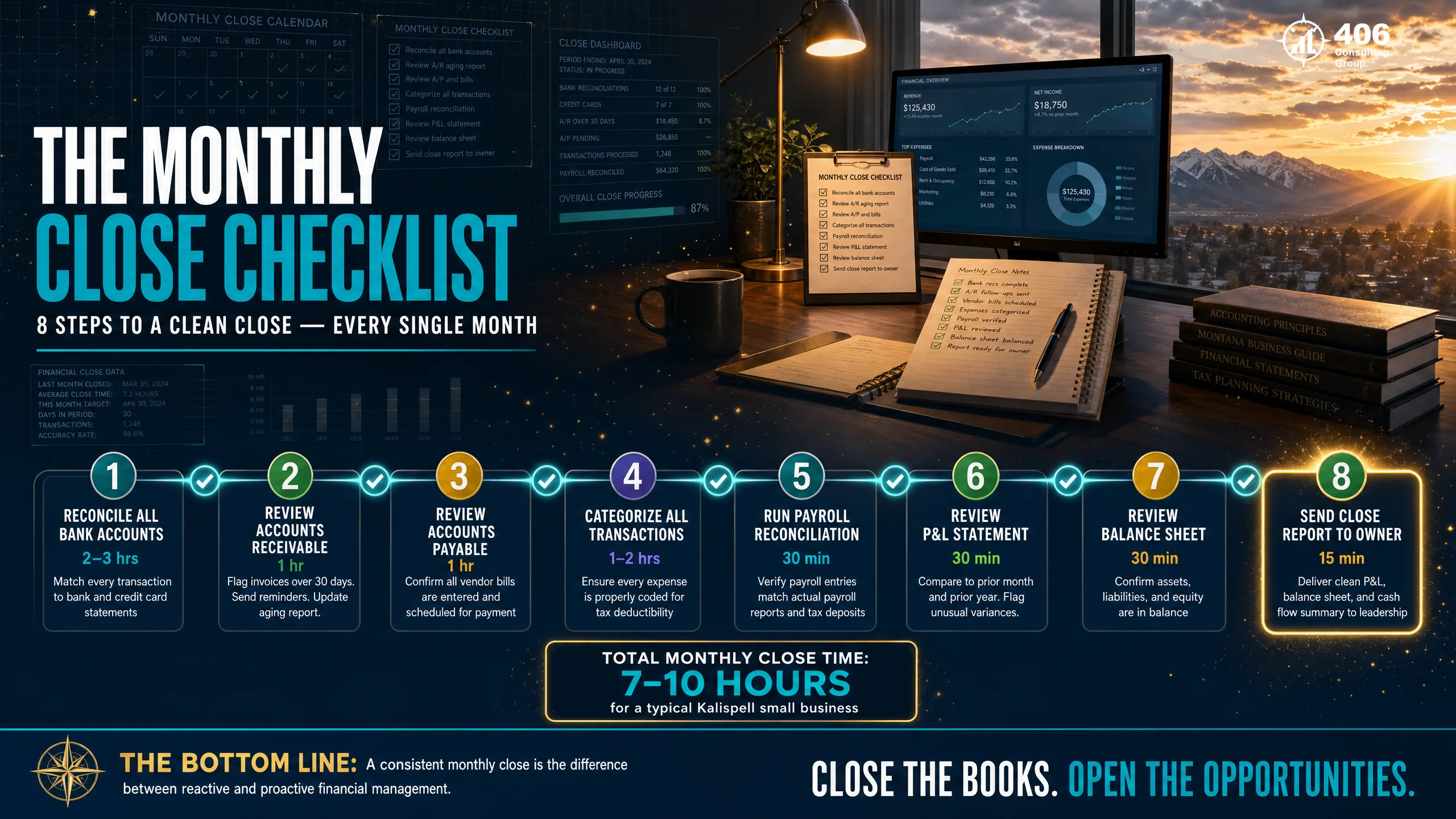

The Monthly Close Process: What Good Books Look Like Every 30 Days

"Closing the books" monthly sounds like accounting jargon. In practice it means: by the 10th of every month, your books reflect exactly where your business stood on the last day of the prior month. No missing transactions. No unreconciled accounts. No guesswork. Here's the eight-step process:

1–3 hrs

Download and categorize all transactions

Pull transactions from all bank accounts, credit cards, PayPal, Stripe, and any other payment sources. Categorize every line to the correct account. Flag any transactions that need owner clarification.

30–60 min

Reconcile all bank accounts

Match every transaction in the books to the corresponding bank statement line item. The ending balance in the books must match the bank statement. Zero unexplained variances.

30–60 min

Reconcile all credit card accounts

Same process for every credit card. Balances in the books must match statements. Expenses categorized correctly. Business vs. personal charges identified and handled.

15–30 min

Review accounts receivable aging

Run an AR aging report. Anything 60+ days should be reviewed — is it being pursued? Is it collectible? Stale receivables that won't be collected should be written off before they inflate your apparent assets.

15 min

Review accounts payable

Check what's past due on the payables side. Vendors with outstanding invoices, subcontractor bills not yet recorded, any accruals needed for services received but not yet invoiced.

15–30 min

Run P&L and compare to prior periods

Review revenue and expenses vs. prior month and same month last year. Identify any significant variances — unusual expenses, revenue timing differences, categories that look wrong. This is where you catch errors before they compound.

15 min

Review balance sheet for anomalies

Check that assets, liabilities, and equity make sense. Look for negative balances in unexpected places, liability accounts that seem too high or too low, equity that doesn't reflect retained earnings correctly.

15 min

Prepare the owner's financial summary

A one-page snapshot: revenue vs. last month and last year, top expense categories, net income, cash balance, AR and AP totals, and any items that need the owner's attention. This is what the business owner actually reads.

Time reality check:For a Kalispell small business with clean books and one to two bank accounts, this process takes 4–8 hours per month. When books are behind or accounts aren't reconciled, it takes 20–40 hours — and that time is usually spent in a panic in March. Monthly maintenance is dramatically less expensive than periodic reconstruction.

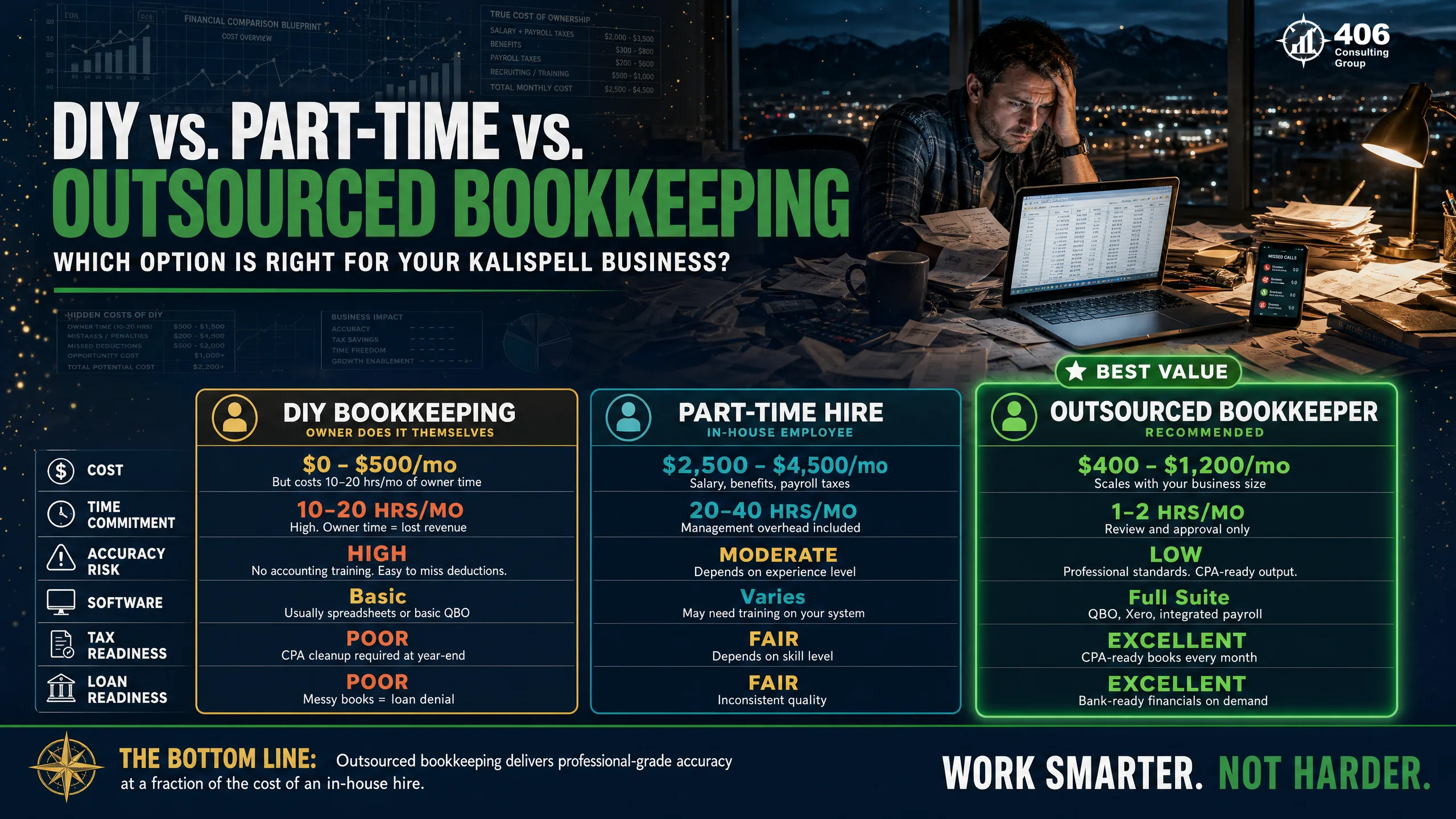

DIY vs. Outsourced Bookkeeping: When to Make the Switch

DIY bookkeeping works — until it doesn't. The question isn't whether you're capable of doing your own books. It's whether the time you're spending on bookkeeping is your best use of that time, and whether the quality of the output is what your business actually needs.

DIY bookkeeping works when:

You've hit the DIY ceiling when:

The Owner Time Math

If you bill $100–$150/hour for your work and spend 10 hours per month on bookkeeping:

$1,000–$1,500

Your time cost/month

At $100–$150/hr × 10 hrs

$300–$800/mo

Outsourced bookkeeping

For most Kalispell SMBs

$200–$1,200

Net benefit/month

Plus better accuracy and tax savings

Outsourced bookkeeping in Montana ranges from $300–$500/month for simple sole proprietors to $1,200–$2,500/month for larger businesses with employees, inventory, and multiple revenue streams. For most Kalispell businesses in the $300K–$2M revenue range, the breakeven with owner time is well under six months. See our bookkeeping services page for specific pricing.

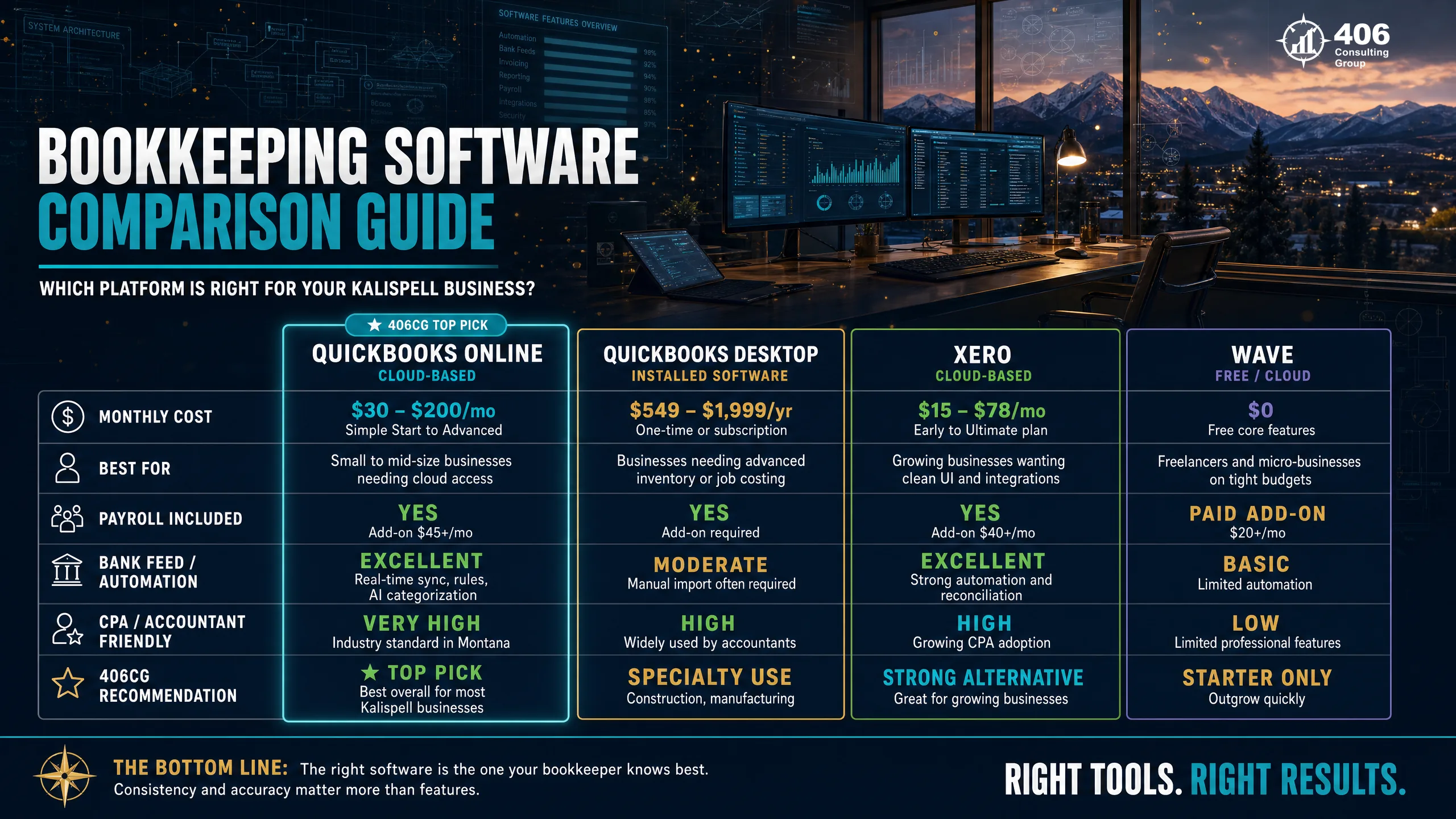

Bookkeeping Software: What Actually Works for Montana Businesses

Software is not the bottleneck. The most common bookkeeping failure we see is not using the wrong software — it's not using any software consistently. That said, the right software makes the process significantly faster and the output significantly more useful.

| Software | Best For | Monthly Cost | Strengths | Limitations |

|---|---|---|---|---|

| QuickBooks Online | Most businesses working with an outside bookkeeper | $30–$200 | Cloud-based, universal accountant familiarity, strong reporting, integrates with everything | Can be expensive; some features require higher tiers |

| QuickBooks Desktop | Construction with complex job costing needs | $550–$1,500/yr | Best job costing in the industry; WIP scheduling; robust inventory | Being phased out by Intuit; no real-time cloud sync; steep learning curve |

| Xero | Simple service businesses; international payments | $15–$78 | Clean interface, lower cost, good bank feeds, strong accounts payable | Less common among Montana bookkeepers; limited payroll integration |

| Wave | Sole proprietors under $200K with very simple books | Free | Genuinely free for core features; easy to use; fine for invoicing | Limited reporting; no inventory; payroll is paid add-on; not suitable for businesses needing bank financing |

Our recommendation for most Kalispell businesses:QuickBooks Online. It's what the majority of Montana bookkeepers and CPAs use, which means if you ever switch providers or need your accountant to access your books, there's no software translation required. For construction businesses with complex job costing needs, QuickBooks Desktop remains the superior option despite Intuit's push toward the cloud version.

Common Bookkeeping Mistakes Kalispell Businesses Make

These are the eight mistakes we see most often when a new Kalispell client hands us their books for the first time. Each has a specific, avoidable dollar consequence.

Mixing personal and business accounts

The most common mistake by far. Personal expenses run through the business account, business deposits into personal accounts. Every mixed transaction must be manually reviewed and reclassified. Over a year, this alone can take 20+ hours to untangle.

Not reconciling accounts monthly

Errors in unreconciled books compound monthly. A $200 duplicate payment undetected for six months becomes a $1,200 discrepancy that takes hours to trace. Reconciliation is the only way to catch errors before they cascade.

Using cash basis past the appropriate threshold

Businesses over $500K–$1M that continue cash-basis bookkeeping when they need financing face a forced, expensive conversion. Accrual-basis reconstruction for two to three years is a major cost that proactive accounting would have avoided.

Misclassifying contractors vs. employees

Paying a worker as a 1099 contractor when the IRS considers them an employee triggers payroll tax liability, penalties, and interest going back to the original misclassification. Montana has its own classification rules that differ from federal standards in some cases.

Ignoring accounts receivable aging

Businesses that don't run AR aging reports monthly discover at year-end that significant receivables are uncollectable. A 90-day-old invoice is significantly harder to collect than a 30-day-old one. Systematic AR review catches problems while there's still time to act.

Not tracking vehicle mileage in real time

The IRS requires a contemporaneous mileage log — reconstructed mileage from memory in March is not deductible. For a Kalispell contractor driving 20,000+ business miles per year, the missed deduction at the IRS standard rate ($0.67/mile in 2024) is $13,400. All of it deductible with proper tracking.

Lumping all revenue into one income line

A single 'Revenue' line in your books tells you nothing about which services, clients, or job types are actually profitable. Breaking revenue into meaningful streams (by service type, job category, or client segment) is what makes financial statements useful for decisions — not just compliance.

Waiting until tax season to look at the books

Tax planning only works prospectively. Strategies like retirement plan contributions, equipment depreciation elections, S-Corp salary adjustments, and income timing only work if you're looking at your numbers before December 31 — not after. By March, the opportunities from the prior year are gone.

Frequently Asked Questions

How much does bookkeeping cost in Kalispell, MT?

Outsourced bookkeeping in the Flathead Valley typically ranges from $300–$500/month for simple sole proprietors with low transaction volume, to $800–$1,500/month for businesses with employees, inventory, and multiple accounts. Construction businesses with job costing needs are typically at the higher end. Most businesses in the $300K–$1M revenue range pay $400–$900/month. Compare that to the cost of your time doing it yourself or the cost of year-end catch-up — the math usually favors outsourcing.

Can I do my own bookkeeping as a small business owner in Kalispell?

Yes — but only if you're genuinely consistent about it. The issue isn't capability; it's consistency. Most business owners who do their own bookkeeping fall behind by February and never fully catch up. If you're under $300K with simple finances and you actually do it every month, DIY works fine. If your books are perpetually behind, the cost of that — in missed deductions, tax surprises, and loan unreadiness — exceeds what outsourcing would have cost.

What's the difference between a bookkeeper and an accountant?

A bookkeeper records and categorizes financial transactions, reconciles accounts, and produces the underlying data. An accountant interprets that data, prepares financial statements and tax returns, and provides strategic financial guidance. You generally need both — a bookkeeper maintaining clean records monthly and an accountant reviewing those records for tax and advisory purposes. Trying to make your tax preparer do bookkeeping at year-end, or asking your bookkeeper to provide tax strategy, leaves gaps in both roles.

How often should my books be reconciled?

Monthly — without exception. Bank reconciliation is the primary error-detection mechanism in bookkeeping. An unreconciled account for two months means two months of undetected errors. For a business doing $50K+ per month in transactions, a single month of unreconciled books can contain thousands of dollars in misposted transactions that take hours to find later. The rule is simple: accounts are reconciled within 10 days of month-end.

Do I need QuickBooks for my Montana small business?

You need bookkeeping software — QuickBooks Online is the most common choice and what most Montana bookkeepers and CPAs work with, which makes outsourcing or collaboration significantly easier. For construction businesses, QuickBooks Desktop's job costing is hard to match. Wave is adequate for very simple sole proprietors. The key is using whatever software you choose consistently and correctly — a misused QuickBooks account is worse than a well-maintained spreadsheet.

When should I switch from cash to accrual accounting?

Switch when: (1) your revenue crosses $500K–$1M and your P&L doesn't reflect when work was actually performed, (2) you're applying for bank financing and the lender requires GAAP-basis financial statements, (3) you carry significant accounts receivable or payable that materially affect your real financial picture, or (4) your tax preparer recommends it for tax optimization. The switch requires filing Form 3115 with the IRS and coordinating between your bookkeeper and tax preparer — it's not a DIY project.

What should I bring to a first bookkeeping consultation with 406 Consulting Group?

The most useful things to bring: your most recent tax return (business and personal if applicable), access to your bookkeeping software or a recent trial balance export, your last three months of bank and credit card statements, and a sense of what's working and what isn't. If your books are a mess, don't worry — we've seen worse, and the consultation is about understanding where things are, not judging how they got there.

External Resources

Kalispell, MT

Let's Get Your Books Right

406 Consulting Group provides bookkeeping, tax preparation, and financial advisory services to Flathead Valley businesses. If your books are behind, your deductions are uncertain, or you can't tell lenders what your business is worth — let's fix that.

The Foundation Stack

5 layers every business needs

Transaction Capture

Every dollar recorded in real time

Reconciliation

Monthly, zero unexplained variances

Chart of Accounts

Structured for your business, not templates

Financial Reports

P&L, balance sheet, AR aging monthly

Tax-Ready Close

Books closed, no year-end reconstruction

Signs You've Hit the DIY Ceiling

Kalispell Bookkeeping Cost Guide