What Banks Actually Look At

for a Commercial Loan

Banks don't approve loans because they believe in your vision. They approve them because the numbers tell a specific story. Here's the exact underwriting checklist commercial lenders use — straight from someone who has reviewed hundreds of Montana loan files and still underwrites for a local bank today.

I've reviewed hundreds of commercial loan files — first as a commercial underwriter at a Montana regional bank, and today as part of 406 Consulting Group, where we still actively underwrite loans for a local bank here in the Flathead Valley. I can tell you with certainty: most business owners walk into a loan meeting without understanding what the underwriter is actually looking for. That gap costs them approvals, terms, and time.

A commercial lender isn't evaluating whether you're a good person or whether the business has potential. They're answering two very specific questions: Can you repay this loan from your operating cash flow? And what happens to the bank's money if you can't?

Everything in your application — financials, credit score, collateral, business plan — is evidence the bank uses to answer those two questions. This article breaks down exactly what underwriters look at, what each element means in plain language, and how to position your Montana business for approval.

Table of Contents

What a Commercial Lender Is Actually Trying to Figure Out

Commercial lending is not personal. I used to tell borrowers this directly when I was on the underwriting side: "I want to say yes — help me build a file that lets me do that." The problem is that most business owners don't know what the underwriter is looking at, so they submit files that make the job harder, not easier.

In 2024, the Federal Reserve's Small Business Credit Survey found that 47% of small business loan applicants were denied or received less than they requested. The most common reasons: weak credit history, insufficient collateral, and inadequate cash flow documentation — all things that can be addressed before an application is submitted, if you know what to prepare.

The Primary Question

Can you repay this from operating cash flow?

Answered by DSCR, EBITDA, and liquidity

The Backup Question

What happens to our money if you can't?

Answered by collateral, guaranty, and net worth

The underwriter's job is to document risk — not to say no. A skilled underwriter builds a case for approval, with appropriate conditions, when the file supports it. A good loan package gives them what they need to make that case to the credit committee. A bad one leaves the underwriter writing exceptions — and exceptions lead to declines.

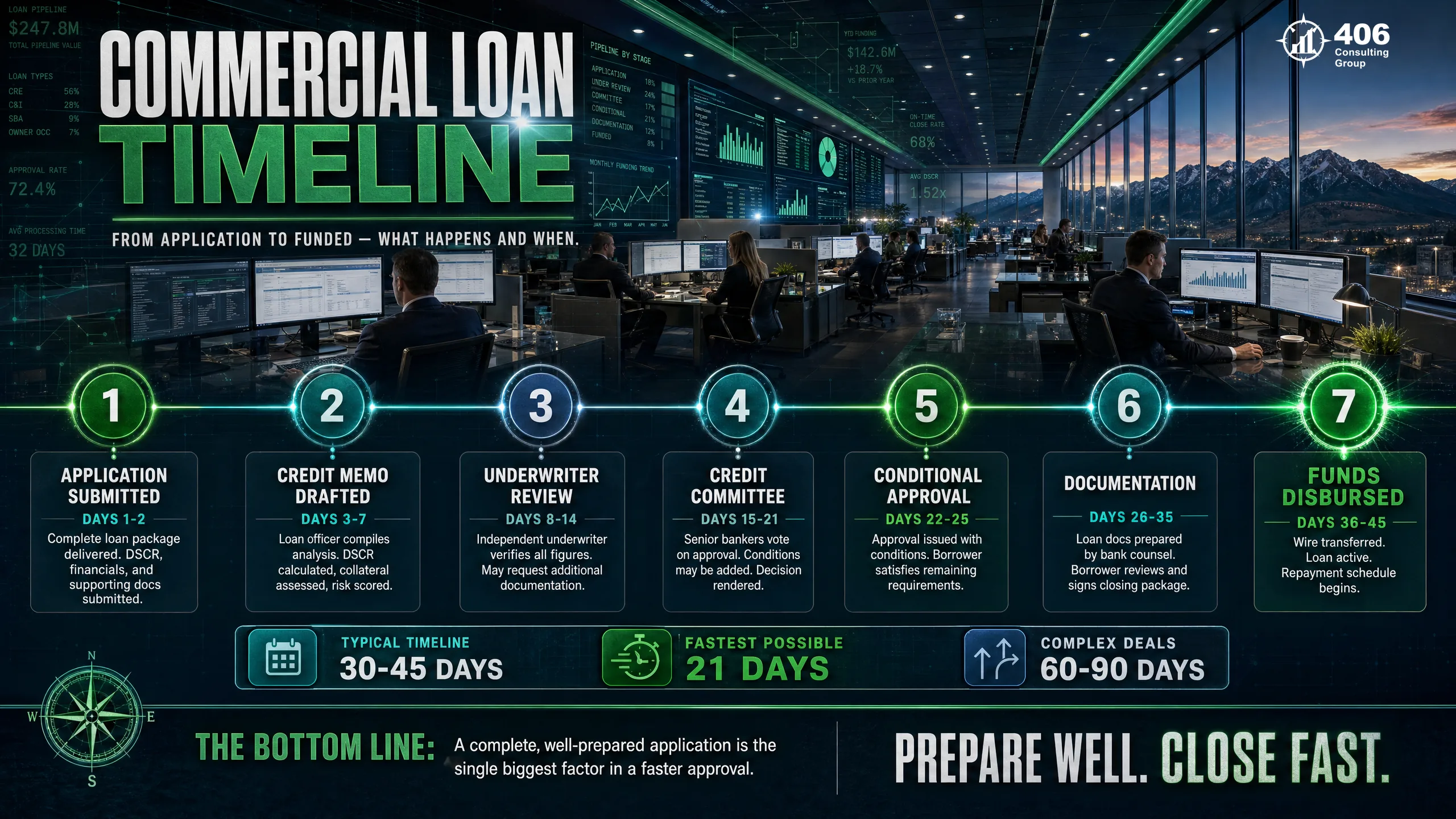

How Commercial Underwriting Actually Works

Here's what actually happens after you submit a commercial loan application at a Montana community bank — from the inside:

Application Received — Loan Officer Initial Review

A loan officer does a quick completeness check. Incomplete applications — missing financials, no debt schedule, unreconciled bank statements — get flagged and sent back. Clean, complete files move to the next step immediately. This is where 30% of applications stall.

Credit Memo Drafted

The loan officer writes a credit memo summarizing your business, the loan request, and your financial profile. This is the document the underwriter reads first. A weak memo written by a loan officer who doesn't fully understand your business can sink a strong file — which is why how you explain your business matters as much as the numbers.

Underwriter Review

A commercial underwriter — someone whose entire job is to find and document risk — reviews the file against the bank's credit policy. They calculate DSCR, stress-test liquidity, verify collateral, and flag any exceptions. This is where your actual financial story gets read in detail.

Credit Committee Review

For loans above a certain threshold (often $250K–$500K at Montana community banks), a credit committee votes to approve, decline, or counter. The loan officer presents the file. The underwriter's memo is the committee's primary reference. A well-documented file gives the loan officer something to present confidently.

Conditional Approval

Most approvals come with conditions — updated financials, specific insurance requirements, a collateral appraisal. These must be satisfied before closing. A typical conditional approval has 3–8 conditions. Each unsatisfied condition delays closing by days to weeks.

Documentation and Closing

Loan docs are prepared, signed, and recorded. Funds are disbursed at closing. From complete application to closing: 30–60 days for conventional commercial loans at Montana community banks. SBA loans: 60–90 days.

Every missing document adds a week to the process. Every exception that surfaces mid-review adds another round of back-and-forth. The business owners who close loans fastest are the ones who walk in with a complete, reconciled, well-organized package — not the ones with the highest revenue.

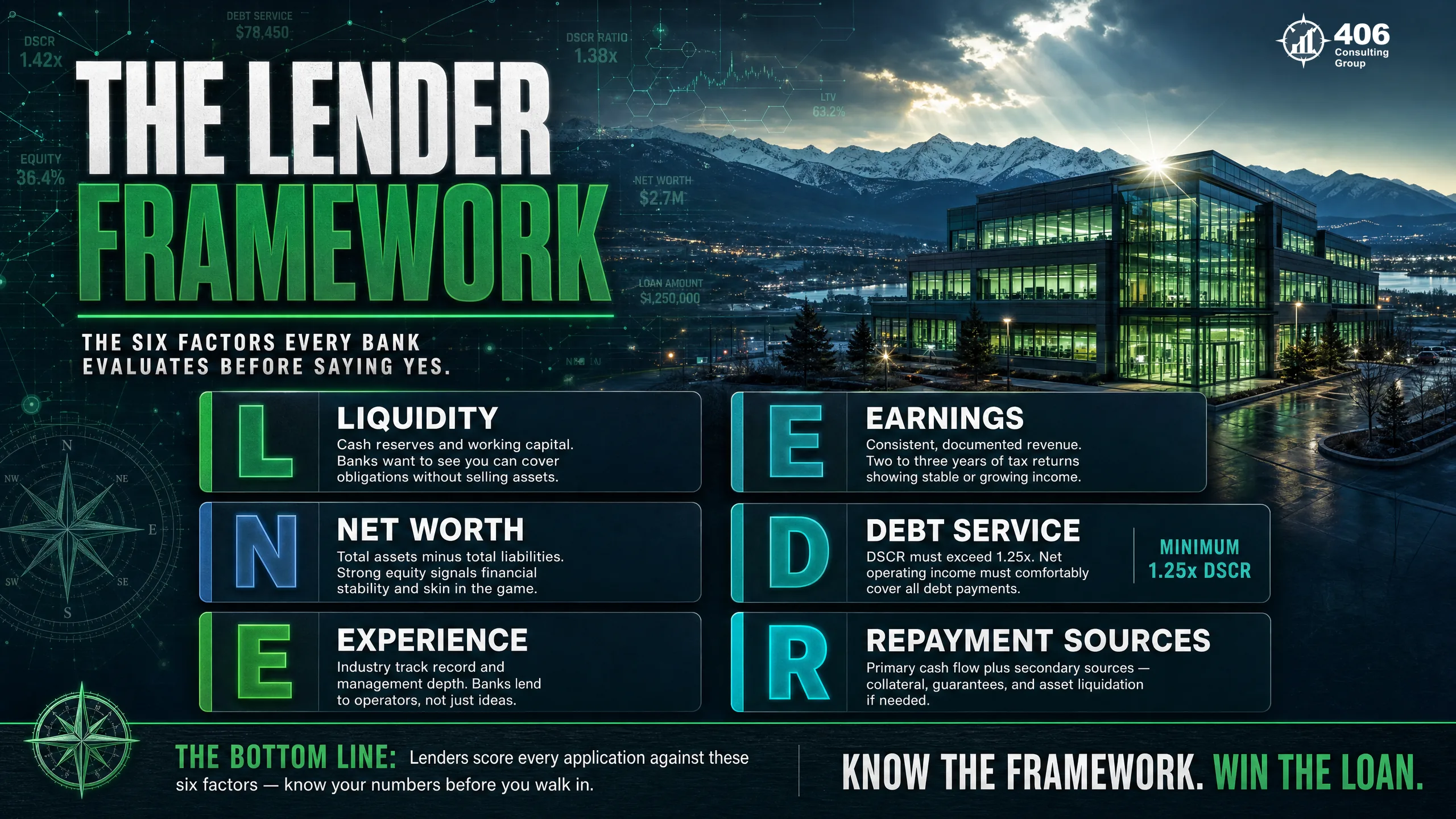

The LENDER Framework: 6 Things Every Underwriter Scores

You've probably heard of the "5 C's of Credit" — character, capacity, capital, collateral, and conditions. That framework is accurate, but it's too abstract to act on. After reviewing hundreds of loan files, I've distilled it into six dimensions that map directly to what underwriters actually measure. We call it the LENDER Framework.

| Letter | Dimension | What It Measures |

|---|---|---|

| L | Liquidity | Working capital, current ratio, cash under stress |

| E | Earnings | EBITDA trend, net income consistency |

| N | Net Worth | Owner equity, balance sheet leverage |

| D | Debt Service | DSCR — the make-or-break ratio |

| E | Experience | Owner track record, management depth, time in business |

| R | Repayment Sources | Primary (cash flow), secondary (collateral), tertiary (guaranty) |

Critical point:Banks score every dimension independently. A strong DSCR doesn't compensate for a thin balance sheet. Strong collateral doesn't save a deal with declining earnings. Each element must stand on its own — and weaknesses in any one of them need to be explained or mitigated proactively.

L — Liquidity: Your Cash Position Under Stress

Liquidity is your business's ability to meet short-term obligations — and, more importantly, its ability to survive a rough quarter while still making loan payments. In my underwriting work, I run a stress scenario on every deal: what happens to this business's cash position if two large receivables pay 30 days late simultaneously? If the answer is "the business can't make its loan payment," that's a problem before approval ever happens.

Current Ratio

Current Assets ÷ Current Liabilities

Lenders want: 1.25x or higher

Measures ability to cover short-term debts with short-term assets. Below 1.0x means liabilities exceed assets — an automatic red flag.

Working Capital

Current Assets − Current Liabilities

Lenders want: 3–6 months of operating expenses

The dollar cushion available to fund operations without borrowing. This is what keeps the business running when receivables are slow.

Real Scenario: Montana Contractor Stress Test

Monthly revenue: $67,000

Monthly operating expenses: $52,000

New loan payment (requested): $4,200/month

Cash on hand: $18,000

Stress scenario: Two major invoices ($40K total) pay 30 days late. By month 2, the business runs negative — and can't make its loan payment.

Fix: Build a $35K operating reserve before applying. The underwriter needs to see the cushion, not just the revenue.

Before applying for a commercial loan, calculate your current ratio and run a 90-day cash projection assuming your two largest receivables pay 30 days late. If the numbers don't hold, that's the first weakness to fix before you submit anything.

E — Earnings: What EBITDA Means and Why It's Not Your Net Income

Net income on your tax return is not what lenders use to evaluate repayment capacity. They use EBITDA — Earnings Before Interest, Taxes, Depreciation, and Amortization — and for owner-operated businesses, they add back excess owner compensation above a market-rate salary. This is one of the most misunderstood elements of commercial underwriting.

How Adjusted EBITDA Gets Built

Net Income (per tax return): $180,000

+ Interest expense: $22,000

+ Income taxes: $38,000

+ Depreciation & amortization: $63,000

= EBITDA: $303,000

+ Owner comp addback ($150K salary,

market rate $90K — addback $60K): $60,000

= Adjusted EBITDA: $363,000

A business that looks like it earns $180K actually has $363K in underwriter-recognized cash flow. That difference can be the margin between approval and denial.

This is one of the biggest reasons business owners with profitable companies get declined — they hand the bank their tax returns without an addback schedule. If your accountant has been aggressively minimizing taxable income (which is smart for taxes), your net income may look too low to support the loan you need. The fix is a properly prepared addback schedule, not changing your tax strategy.

Lenders also want to see a trend, not a snapshot. Three years of growing EBITDA tells a different story than one strong year following two weak ones. If your business had a pandemic dip and a strong recovery, be prepared to explain it with specific context — "we lost our primary hospitality client in 2020 and replaced that revenue with two long-term construction contracts by Q3 2021" is a story the credit memo can tell. "COVID impact" with nothing further is not.

Tax minimization works against you here.Every dollar your accountant saves in taxes reduces the earnings figure the underwriter uses to evaluate your loan. That's not a reason to pay more taxes — it's a reason to make sure you arrive at the bank with a complete addback schedule and a well-prepared financial narrative.

N — Net Worth: Why the Balance Sheet Matters as Much as the P&L

Two businesses can have identical cash flow and DSCR — but radically different balance sheets — and the lender will treat them very differently. Owner's equity is the cushion that absorbs losses before the bank does. The more equity you have, the more risk the bank is willing to share with you.

Overleveraged — Hard Approval

- Total assets: $500,000

- Total liabilities: $440,000

- Owner equity: $60,000

- Debt-to-equity ratio: 7.3x

- Underwriter concern: any loss hits the bank immediately

Lender-Ready — Standard Approval

- Total assets: $500,000

- Total liabilities: $250,000

- Owner equity: $250,000

- Debt-to-equity ratio: 1.0x

- Underwriter view: strong buffer — business can absorb a bad year

Most conventional commercial lenders want a debt-to-equity ratio under 3:1. SBA lenders are more flexible on this metric, but they have other requirements that compensate. If your balance sheet is heavily leveraged, the fix isn't fast — but it is predictable: retain earnings rather than distributing them, or inject personal capital into the business.

Common mistake I see repeatedly: Business owners who distribute all profits at year-end to minimize taxes arrive at the bank with strong earnings but a hollowed-out balance sheet. A controller or fractional CFO can model the right retained earnings target before distributions — this is one of the highest-ROI moves a business owner can make in the 12–18 months before they need capital.

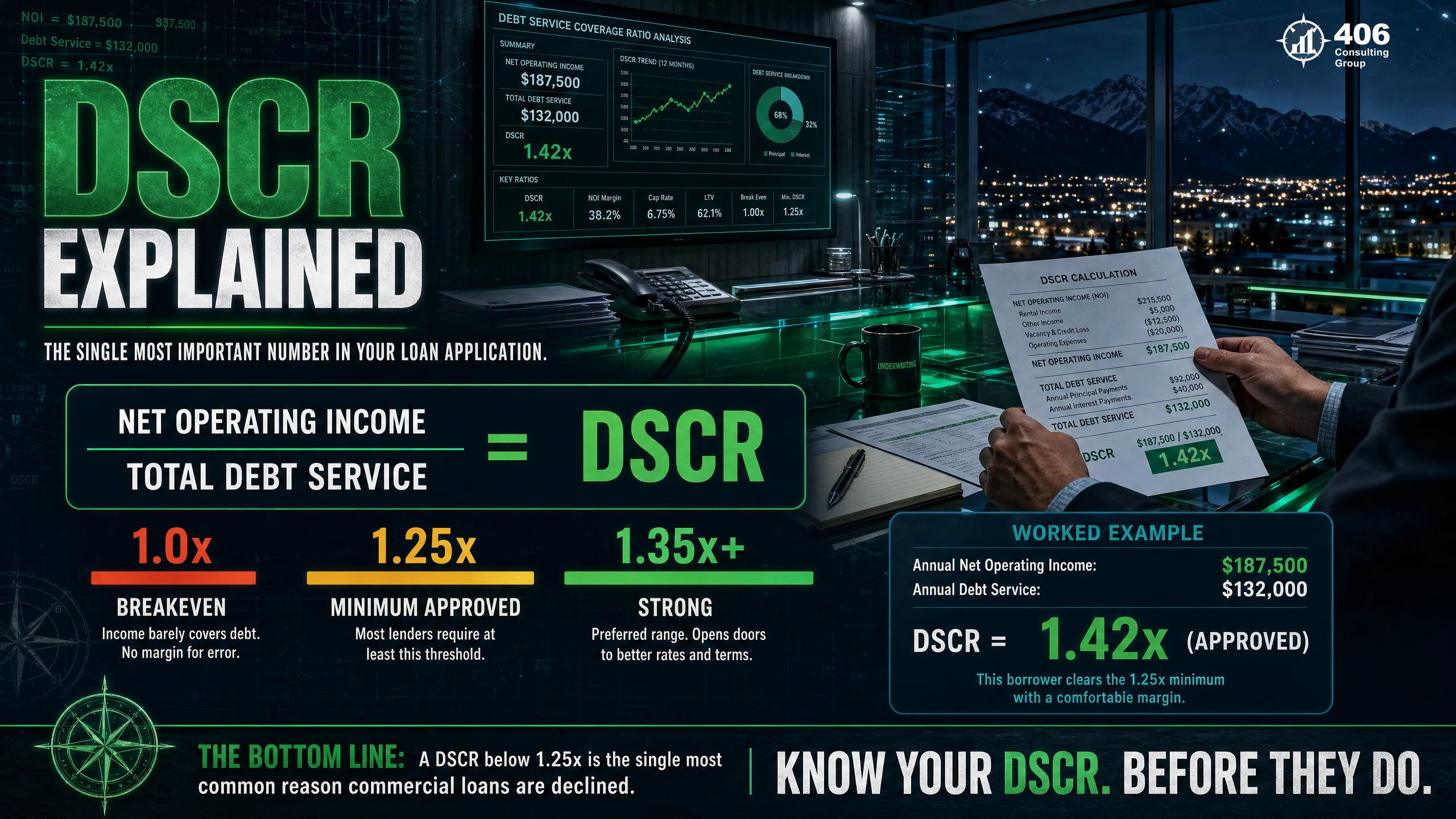

D — Debt Service Coverage Ratio: The Number That Makes or Breaks Your Loan

If you learn one number from this article, make it DSCR. The Debt Service Coverage Ratio is how lenders quantify whether your cash flow is sufficient to cover your loan payments — both what you already owe and what you're requesting. In my underwriting work, every deal starts and ends with DSCR.

DSCR Formula

DSCR = Net Operating Income ÷ Total Annual Debt Service

Net Operating Income = Adjusted EBITDA minus taxes minus non-financed capex

Total Annual Debt Service = all existing loan payments + the new loan's annual payment

| DSCR | What Lenders Think | Typical Outcome |

|---|---|---|

| Below 1.0x | Business cannot cover debt from operations | Denied — automatic |

| 1.0x – 1.15x | Borderline — zero margin for error | Denied or heavily conditioned |

| 1.15x – 1.25x | Marginal — meets minimum at some banks | Possible with strong collateral and experience |

| 1.25x – 1.35x | Acceptable — standard approval range | Approved with standard pricing |

| 1.35x+ | Strong — preferred by all lenders | Best terms, fastest process |

Worked Example: $400K Equipment Loan Request

Business Financials

Adjusted EBITDA: $363,000

Income taxes (est.): $48,000

Capital expenditures (unfinanced): $15,000

Net Operating Income: $300,000

All Debt Obligations

Existing term loan payments: $36,000/yr

New $400K loan (7%, 10-yr term): $55,680/yr

Total Annual Debt Service: $91,680

DSCR = $300,000 ÷ $91,680 = 3.27x — Strong approval candidate at any Montana bank

If your DSCR comes in below 1.25x, the fix may be simpler than you think: pay off a smaller existing loan before applying, reduce owner distributions to show more retained cash, or request a longer loan term to reduce the annual payment. Run the numbers before you submit anything.

E — Experience: Why Your Résumé Is Part of the Credit File

Commercial lenders evaluate the business — but they also evaluate the person running it. I've seen financially strong businesses get declined because the owner had no relevant industry background, and I've seen marginal files approved because the owner had a 20-year track record in the industry and had successfully managed debt before. Experience is a real underwriting factor, not a soft consideration.

Time in Business

Two years is the informal minimum for most conventional commercial loans. Businesses under two years are considered higher risk and typically need SBA backing or a strong co-borrower. First full year of operations will almost always require an SBA route.

Owner Industry Experience

Years in the industry before ownership matter. A general contractor who spent 12 years as a project superintendent before starting his own firm looks very different than someone who bought a construction business with no field background. Document this in your loan narrative explicitly.

Management Depth

Single-owner businesses with no management team are a concentration risk. Lenders ask: what happens to the business if the owner is injured, ill, or unavailable for 90 days? A key-man life insurance policy and an identified operations manager changes that risk profile significantly.

Prior Lending History

A clean record of repaid business debt — even small equipment financing or an SBA microloan — builds credibility. Prior defaults, even resolved ones, need to be addressed proactively in your narrative with specific context, not discovered by the underwriter mid-review.

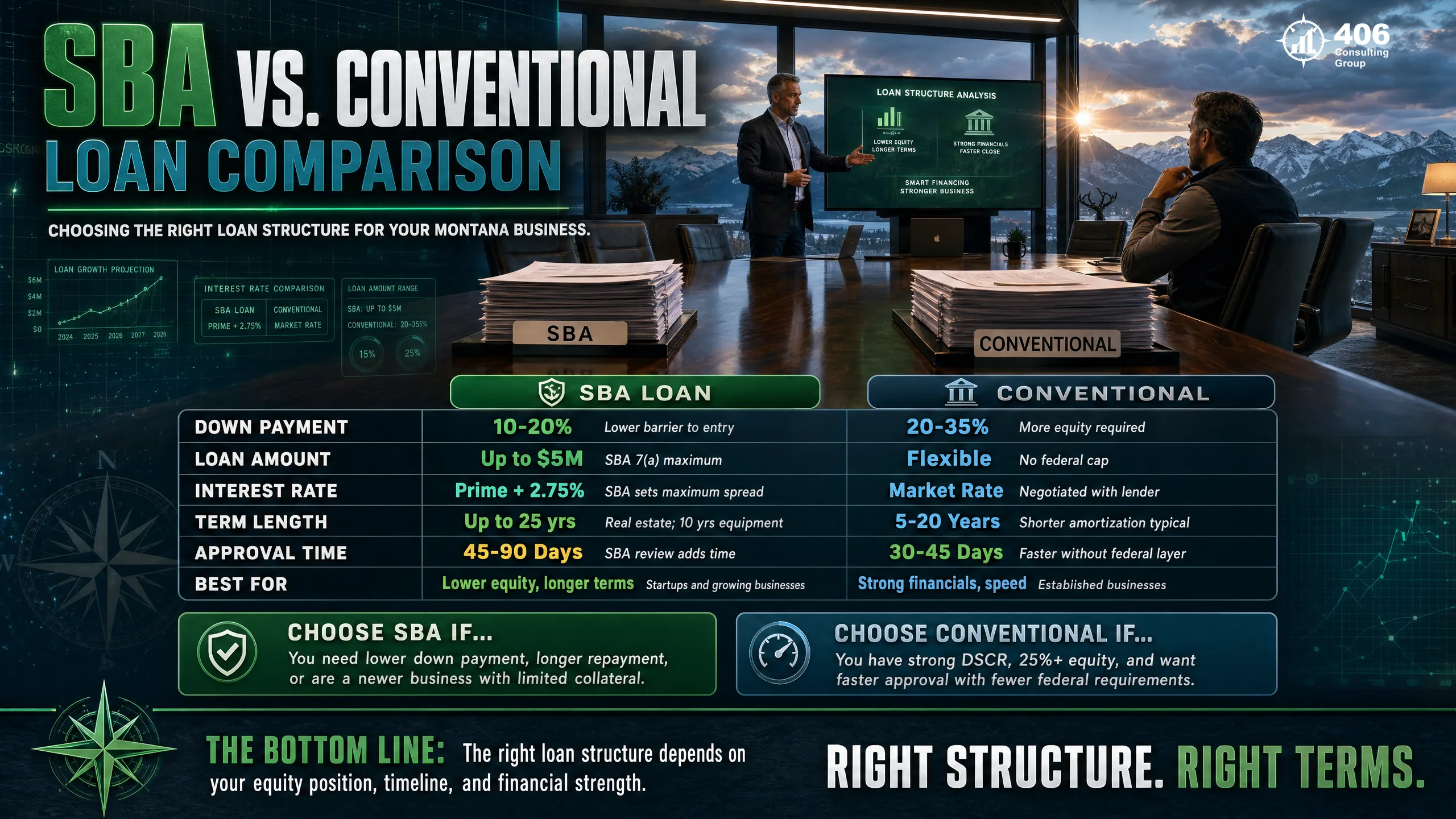

If you're a first-time business owner or under two years in operation, the SBA 7(a) program is not a consolation prize — it's the designed pathway for building commercial lending history. Use it strategically: a small SBA loan repaid cleanly positions you for conventional financing on the next round.

R — Repayment Sources: How Banks Think in Three Layers

Every commercial loan has a primary repayment source, a secondary, and often a tertiary. A bank approves a loan when it's confident in the primary — but the underwriter documents all three, because the credit committee wants to know exactly what happens in each failure scenario.

Primary Source

Operating cash flow

DSCR measures this. If business cash flow covers debt service with margin, this source is considered reliable.

Secondary Source

Collateral liquidation

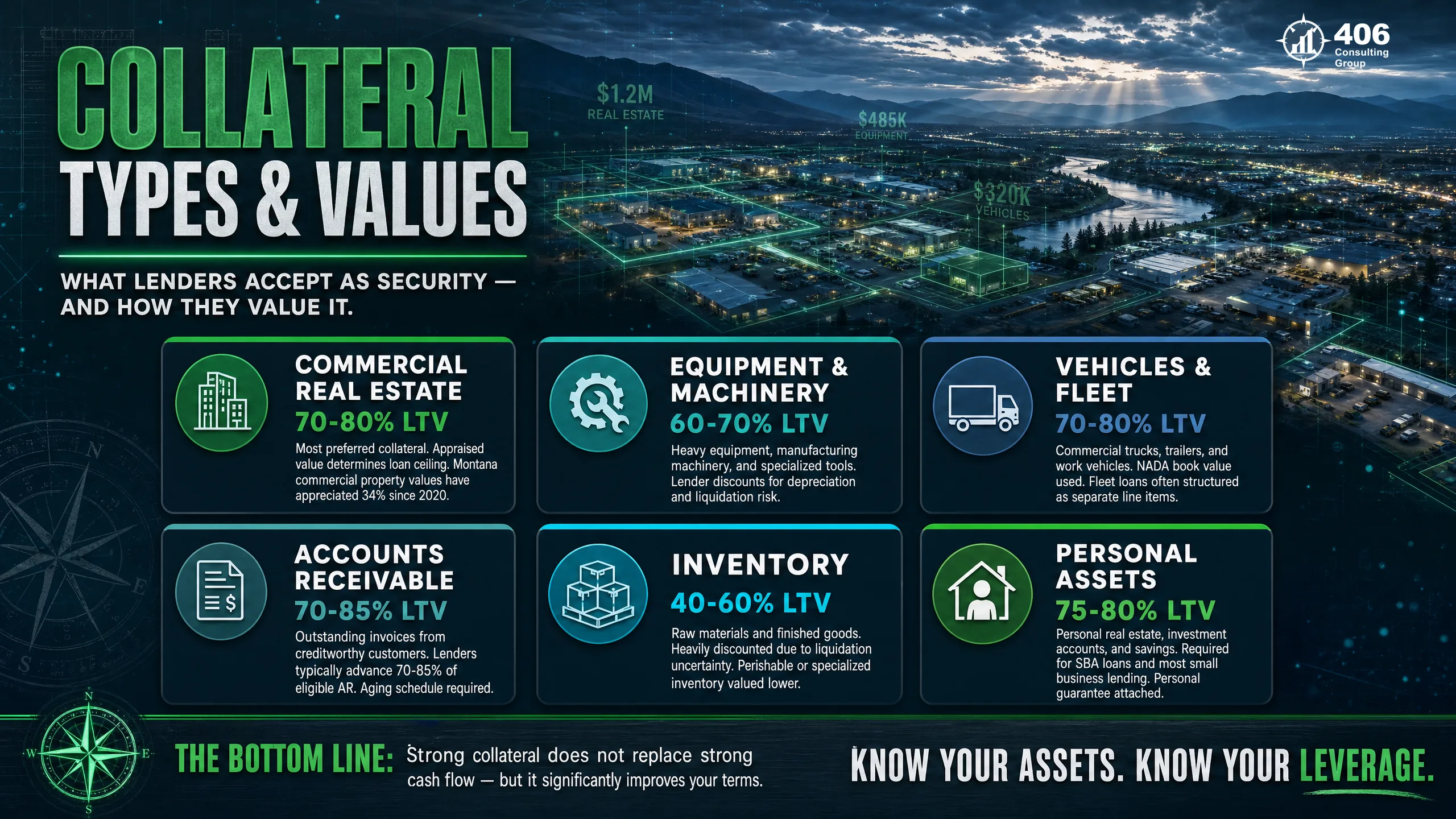

Real estate, equipment, receivables. What can the bank sell to recover its balance if the business fails?

Tertiary Source

Personal guaranty

Most commercial loans under $5M require a personal guaranty, making the owner personally liable if business and collateral both fall short.

Collateral types and typical loan-to-value (LTV) ratios at Montana banks:

| Collateral Type | Typical LTV | Notes |

|---|---|---|

| Commercial real estate | 70–80% | Strongest collateral — most lenders prefer real estate-secured deals |

| Owner-occupied real estate | 75–80% | Slightly preferred over investment real estate |

| New equipment | 70–80% | Depreciates — lenders typically require 20–30% down |

| Used equipment | 50–60% | Higher discount — liquidation value is uncertain in Montana markets |

| Accounts receivable | 70–80% | Only high-quality receivables under 90 days, creditworthy debtors |

| Inventory | 30–50% | Lowest value — hard to liquidate, value decays quickly |

Service-based businesses with few hard assets often face a collateral gap. Options: pledge personal real estate as additional collateral, use SBA programs with lower collateral requirements, or — for smaller amounts — look at unsecured SBA microloans. Don't try to conceal a collateral gap. Address it directly in your loan narrative with a proposed solution. Underwriters respect transparency; they penalize evasion.

How to Prepare a Commercial Loan Package That Gets Read

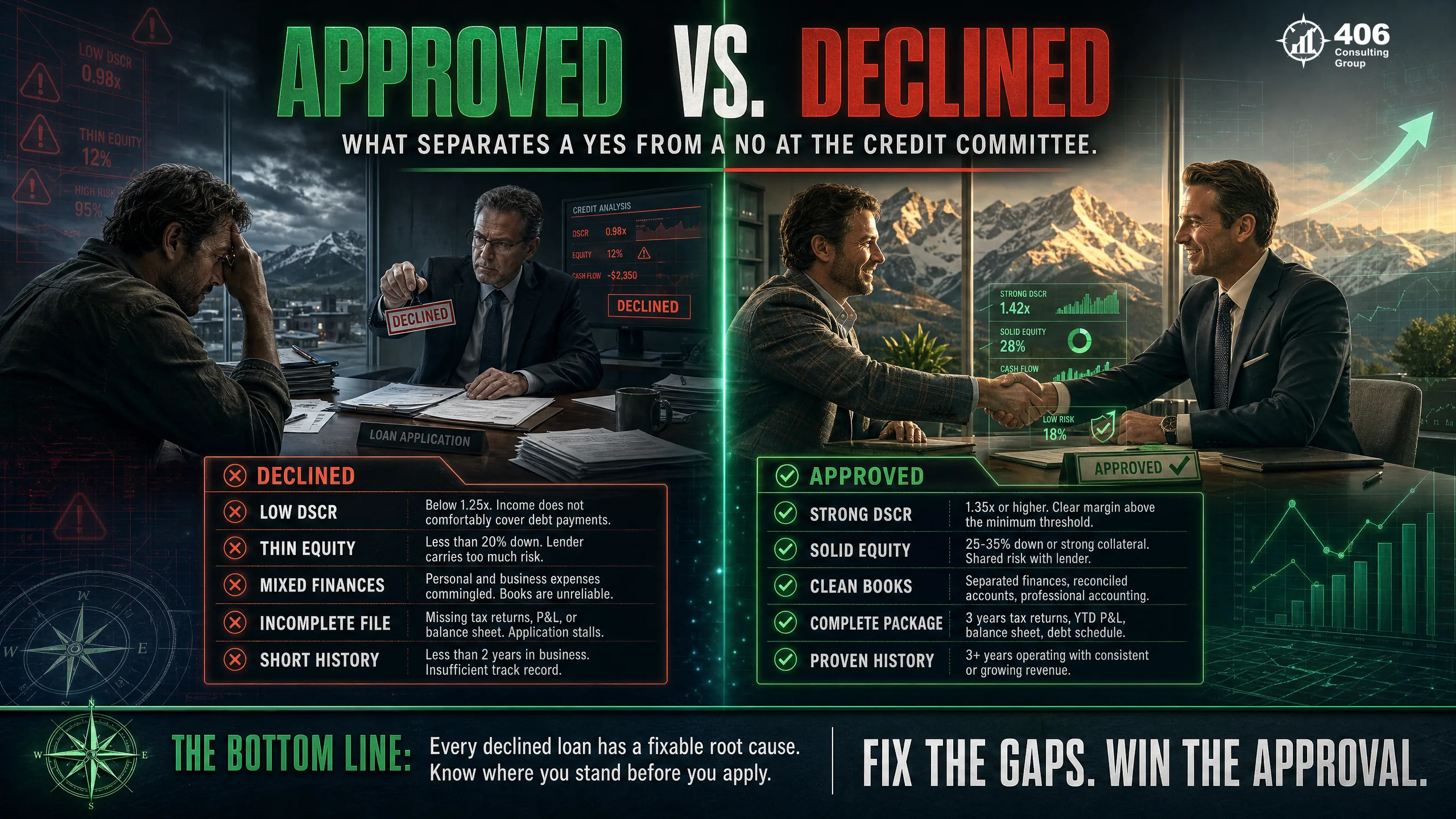

A loan application is a sales document. It's making the case — in numbers and in narrative — that your business is creditworthy and the bank's money is safe. Loan officers review dozens of files. A clean, complete, well-organized package signals a well-run business before the underwriter reads a single number.

From my time on the underwriting side, I can tell you exactly what kills applications before they reach the credit committee: mixed personal and business expenses in the bank statements, missing years of tax returns, financial statements that don't reconcile to bank deposits, no explanation for revenue spikes or dips, and a loan narrative that says "to purchase equipment" with no further context. These aren't dealbreakers if caught early — they're problems when the underwriter discovers them mid-review.

Financial Documents

- 3 years of business tax returns (signed)

- 3 years of business financial statements (P&L + balance sheet)

- YTD P&L and balance sheet (within 90 days of application)

- 12-month cash flow projection with stated assumptions

- Complete debt schedule — all existing loans with balances and payments

- Business bank statements — last 3 months

- Addback schedule (if owner compensation or non-recurring expenses are material)

Supporting Documents

- Business plan summary (2–3 pages: purpose of loan, repayment plan, use of funds)

- Personal financial statement — all guarantors

- 3 years personal tax returns — all guarantors

- Business entity docs (articles, operating agreement, ownership structure)

- Purchase contract or equipment quote (if applicable)

- Collateral list with estimated current market values

- Résumés of key management if relevant to experience scoring

406 CG tip: We recommend a "pre-loan package review" 60–90 days before you intend to apply. We build your addback schedule, reconcile your financials, calculate your projected DSCR, and identify any weakness that needs to be addressed before the bank sees the file. Our loan readiness program does exactly this — and because we still actively underwrite commercial loans for a local Montana bank, we know precisely what the underwriter on the other side of the table is looking for.

What Montana Lenders Specifically Look For

Montana's commercial lending market is dominated by community and regional banks — Glacier Bank, First Interstate Bank, Whitefish Credit Union, Opportunity Bank, and Freedom Bank Montana — alongside national SBA lenders. Each has its own credit culture, but several Montana-specific patterns are worth knowing before you submit.

Community Banks Weigh Relationships

Glacier Bank, First Interstate, and Freedom Bank Montana are relationship lenders. A long banking history at the institution — even if you've only used personal checking — carries weight in the credit memo. If you're starting from scratch, open a business checking account and build a 12-month banking relationship before applying. It matters more than most borrowers expect.

Freedom Bank Montana — Worth Knowing

Freedom Bank Montana is an excellent resource for Flathead Valley business owners. As a community bank with local decision-making authority, they move faster on deal approval than larger regional institutions and have more flexibility on deal structure for Montana businesses with local collateral. They actively work with Montana SBDC-referred borrowers and are SBA preferred lenders.

Seasonal Cash Flow Gets Scrutinized

Montana's construction, tourism, and agriculture businesses run seasonal cycles. Montana lenders understand this — but they want it documented. Provide monthly cash flow projections (not just annual totals), and specifically demonstrate how you cover payroll and overhead through the slow months without cash shortfalls. A seasonal business that can't show this answer clearly will struggle at any Montana bank.

SBA 7(a) and 504 Programs Are Well-Used Here

Montana's small business ecosystem leans heavily on SBA programs. The 7(a) covers working capital, equipment, and real estate up to $5M. The 504 program is for commercial real estate and major equipment — lower down payments, longer terms, better rates. Montana SBDC (mtsbdc.org) connects borrowers with local SBA preferred lenders and provides free pre-application counseling.

Because 406 Consulting Group actively underwrites loans for a local Montana bank, we have a real-time view of what's being approved, what's being declined, and how deal structures are shifting in the current rate environment. That's not something you get from a general financial advisor — it's inside knowledge that directly benefits every client we take through our loan readiness program.

Common Reasons Montana Businesses Get Declined — and How to Fix Them

A declined commercial loan is not necessarily a dead end. In most cases it's a gap-identification exercise — the bank is telling you exactly what needs to change before you reapply. Here are the five most common reasons I see Montana businesses denied, and the specific path to fixing each.

DSCR Too Low — Most Common

Root Cause

Existing debt obligations consume too much cash flow relative to income, leaving insufficient coverage for new debt

Fix

Pay off one or more smaller existing loans before reapplying, restructure existing debt to extend terms and lower monthly payments, or request a longer term on the new loan to reduce its annual payment

Timeline

60–180 days depending on which obligations are targeted

Thin Equity / Overleveraged Balance Sheet

Root Cause

Profits have been fully distributed rather than retained; high debt-to-equity ratio signals low buffer for the bank

Fix

Retain 6–12 months of earnings before reapplying, inject personal capital directly into the business, or bring in a co-borrower or SBA guarantee to reduce the bank's exposure

Timeline

12–18 months for meaningful equity build without capital injection

Low Personal Credit Score

Root Cause

Late payments, high credit card utilization, or unresolved derogatory marks on personal credit

Fix

Pay all obligations on time for 90+ consecutive days, bring credit card utilization below 30%, dispute any inaccurate marks on your credit report — then reapply

Timeline

90–180 days for meaningful score improvement

Insufficient Business History

Root Cause

Business is under 2 years old or lacks a documented financial track record

Fix

Apply for an SBA 7(a) or SBA microloan instead of conventional; build a 12-month banking relationship with the target institution; consider a co-borrower with established business history

Timeline

SBA-backed options can move in 60–90 days

Incomplete or Disorganized File

Root Cause

Missing documents, financial statements that don't reconcile to bank statements, no loan narrative, or unexplained revenue fluctuations

Fix

Engage a controller or fractional CFO to prepare a complete, reconciled loan package before reapplying — this is exactly what 406 CG's loan readiness program delivers

Timeline

30–60 days with professional preparation

Frequently Asked Questions

What credit score do I need to get a commercial loan in Montana?

Most Montana banks want a personal FICO score of 680 or higher for conventional commercial loans. Some SBA preferred lenders — including Freedom Bank Montana — will work with scores in the 640–679 range when other factors (DSCR, collateral, business history) are strong. Below 640 typically requires credit repair before a realistic application.

What DSCR do commercial lenders require?

The minimum DSCR most Montana lenders will accept is 1.20x–1.25x. At 1.25x, the business generates $1.25 in net operating income for every dollar of debt service owed. Most lenders prefer 1.35x or higher. Below 1.20x, approval is rare without significant compensating factors — and those factors need to be documented proactively, not discovered by the underwriter.

How much collateral do I need for a commercial loan?

As a general rule, lenders want collateral covering 100–125% of the loan amount at liquidation value — which means appraised market value needs to exceed the loan balance. Commercial real estate is the strongest collateral at 70–80% LTV. Service businesses with few hard assets often need to pledge personal real estate or use SBA programs with lower collateral requirements to fill the gap.

How long does commercial loan approval take?

Conventional commercial loans at Montana community banks typically close in 30–60 days from complete application submission. SBA 7(a) loans run 60–90 days. SBA 504 loans can take 90–120 days. These timelines assume a complete, well-organized file — every missing document or exception discovered mid-review adds days to weeks. The fastest closings I've seen were on files that arrived complete and clearly organized.

Do I need a business plan to apply?

For loans under $500K at a community bank where you have an established relationship, a formal business plan isn't always required. However, a 2–3 page loan narrative — describing the business, the specific purpose of the loan, the use of funds, and the repayment plan — materially strengthens any application. For SBA loans, a business plan is typically required and reviewed for credibility alongside the financial package.

When does the SBA program make more sense than conventional?

SBA programs are the right path when: you're under 2 years in business, your collateral doesn't fully cover the loan, your industry is considered higher risk by conventional lenders, or you need a longer repayment term than conventional lenders will extend. The SBA guarantee lowers the bank's risk — allowing approval on files that wouldn't qualify conventionally — but the process is longer and more document-intensive.

What should I do first if I want a commercial loan in the next 12 months?

Start with a pre-loan package review with your accountant or fractional CFO — 12 months out is exactly the right window to find and fix weaknesses before the lender sees the file. Calculate your current DSCR, review your balance sheet leverage, pull your personal credit report, and assess your collateral position. Most issues are solvable with enough runway. The worst time to discover a problem is in the middle of an underwriting review.

Get Loan-Ready

Know Where You Stand Before the Bank Does

Our loan readiness program builds your complete commercial loan package, calculates your DSCR, identifies every weakness in your file, and gives you a clear action plan — before you sit down with a lender. And because we still actively underwrite commercial loans for a local Montana bank, we know exactly what the underwriter on the other side of the table is looking for.

Why 406 CG?

Inside Knowledge You Can't Get Anywhere Else

Carrie Anderson has reviewed hundreds of commercial loan files as a Montana underwriter. 406 Consulting Group still actively underwrites commercial loans for a local Montana bank — giving our clients a real-time view of exactly what lenders are approving, declining, and why.

See Loan Readiness ProgramThe LENDER Framework

6 dimensions lenders score

Liquidity

Working capital & current ratio

Earnings

EBITDA trend, 3-year history

Net Worth

Equity & leverage ratio

Debt Service

DSCR — minimum 1.25x

Experience

Owner & management depth

Repayment Sources

Cash flow + collateral + guaranty

Key Numbers Lenders Use

Ready to Prepare?

Before You Apply: Quick Audit