Tax Preparation in Bozeman, MT:

What Business Owners Need to Know

Bozeman's growth has created a tax prep environment most general CPAs aren't equipped for. Here's what your business actually owes, when it's due, and how to stop leaving money on the table.

In This Guide

- 1.Why Tax Prep Is Different in Bozeman

- 2.What Tax Preparation Actually Covers

- 3.Federal Filing by Entity Type

- 4.Montana State Tax Obligations

- 5.The Bozeman Business Filing Calendar

- 6.The Bozeman Tax Prep Sequence

- 7.Common Tax Prep Mistakes Bozeman Businesses Make

- 8.Choosing a Tax Preparer in Bozeman

- 9.Industry Tax Prep Considerations

- 10.Virtual Tax Preparation for Bozeman Businesses

- 11.Case Study: Two Bozeman Businesses, Same Revenue

- 12.Frequently Asked Questions

Bozeman is one of the fastest-growing cities in the United States — and that growth has created a business tax environment that many general tax preparers are not equipped to handle. Tech startups receiving equity compensation, out-of-state remote workers with multi-state filing obligations, real estate investors navigating Montana's depreciation rules, and first-year businesses that have never filed a business return: these are the clients a Bozeman tax preparer needs to know how to serve. Many don't.

This guide covers what tax preparation actually involves for a Bozeman business, what you owe at the federal and Montana state level, and how to approach the process so you're not scrambling in March.

Why Tax Prep Is Different in Bozeman

Bozeman's economy has grown at a pace that has outrun its local tax infrastructure. The population has roughly doubled since 2010, Gallatin County is consistently among the fastest-growing counties in Montana, and the business mix looks nothing like the rest of the state. That complexity creates tax prep challenges that a general practitioner in a smaller Montana market simply does not encounter.

Tech startup and remote worker complexity

Bozeman has attracted significant tech company relocation and remote worker migration from California, Washington, and Colorado. These businesses often arrive with unvested stock options, multi-state income histories, and deferred tax positions that require careful unwinding for Montana filing purposes. A CPA who has never seen a 83(b) election or multi-state apportionment schedule will not catch what needs to be caught.

Real estate investor volume

Bozeman's real estate market has brought an unusually high concentration of investors — both Montana residents and out-of-state buyers with rental properties in Gallatin County. Rental income, depreciation schedules, cost segregation studies, 1031 exchanges, and passive activity loss rules are not standard small-business tax prep topics. They are a significant part of the Bozeman tax prep landscape.

First-year and early-stage businesses

Bozeman's growth has produced a high concentration of businesses in their first or second year. These owners frequently make the same four tax mistakes: no quarterly estimated payments in year one, wrong entity structure from day one, no contractor 1099-NEC system, and mixed business and personal accounts. Each is correctable — but only if the tax preparer identifies it before the return is filed.

Montana State University ecosystem

MSU's research and entrepreneurship ecosystem generates spin-out companies, licensing agreements, royalty income, and grant-funded operations that have unusual tax profiles. University-adjacent businesses — tutoring services, research contractors, housing operators — often receive income on 1098-T or 1099-MISC forms that are misclassified. Graduate students starting businesses while receiving stipends face unique self-employment tax scenarios.

The implication: Bozeman business owners need a tax preparer who has handled their specific scenario — not just someone who is geographically convenient. The right preparer for a Bozeman tech startup is not the same as the right preparer for a Bozeman general contractor. Both are legitimate needs; the expertise required is different.

What Tax Preparation Actually Covers

Most business owners think of tax preparation as filling out forms. A return is not prepared that way. A complete tax preparation engagement starts weeks before any form is touched — and the work that happens in that pre-filing window determines what the return says.

Records assembly and reconciliation

Before any return is prepared, the year's financial records must be complete, reconciled, and categorized. A CPA working from unreconciled bank statements is guessing at deductions and income — and guesses on tax returns create audit exposure. Clean, reconciled books are not a nice-to-have; they are the input that makes accurate preparation possible.

Entity structure confirmation

Each tax season should include a confirmation that the current entity structure is still optimal. A Bozeman business that was a sole prop at $50,000 net profit and is now at $120,000 may need an S-Corp election. A business that elected S-Corp status and has since declined in revenue may be paying compliance costs that exceed the savings. Entity review is a tax prep function, not a separate engagement.

S-Corp salary and payroll review

S-Corp owner-employees must pay themselves a reasonable salary — and that salary must be reviewed each year. IRS scrutiny of unreasonably low S-Corp salaries has increased. A tax preparer who files your 1120-S without reviewing whether your W-2 salary is defensible is leaving you exposed to reclassification and back employment taxes.

Depreciation and asset scheduling

Equipment purchases, vehicle additions, and real property improvements need to be properly scheduled and depreciated. Section 179 elections, bonus depreciation, and MACRS depreciation schedules are all annual decisions — not automatic calculations. A preparer who does not walk through the asset list may miss a significant deduction or create a recapture problem in a future year.

1099 and information return compliance

Every contractor paid $2,000 or more during 2026 (raised from $600 under OBBBA — verify prior-year threshold at IRS.gov) needs a 1099-NEC delivered by January 31. A complete tax prep engagement verifies that 1099s are filed, not just that the tax return is accurate. Missing 1099s create per-form penalties and can put the underlying deduction at risk of IRS challenge.

Montana-specific review

Montana has unique filing requirements — Form PTE for S-Corps (the pass-through entity return that replaced Form CLT-4S after 2018), Form 2 for individual returns, the Secretary of State annual report, and the extension treatment. A preparer unfamiliar with Montana's specific forms may file correctly for federal purposes while missing a state filing that creates a penalty.

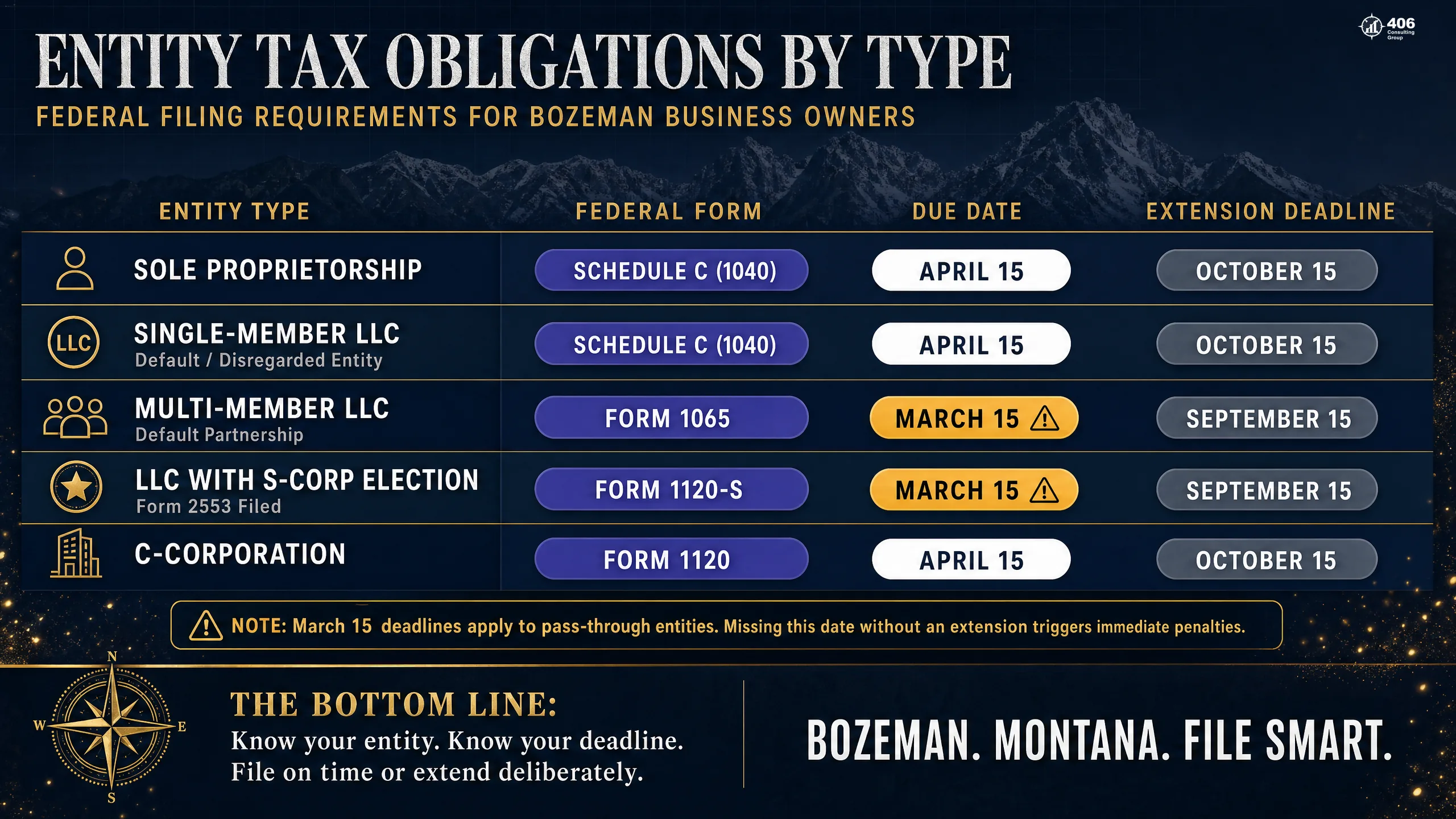

Federal Tax Filing by Entity Type

The federal return your Bozeman business files depends entirely on how it is structured. Filing the wrong form — or filing the right form on the wrong deadline — creates penalties that compound. Here is what each entity type owes and when.

| Entity Type | Federal Form | Due Date | Extension | Extended Deadline |

|---|---|---|---|---|

| Sole Proprietorship | Schedule C (with Form 1040) | April 15 | Form 4868 | October 15 |

| Single-Member LLC (default) | Schedule C (with Form 1040) | April 15 | Form 4868 | October 15 |

| Multi-Member LLC (default) | Form 1065 (partnership) | March 15 | Form 7004 | September 15 |

| LLC with S-Corp Election | Form 1120-S | March 15 | Form 7004 | September 15 |

| C-Corporation | Form 1120 | April 15 | Form 7004 | October 15 |

The March 15 trap: S-Corps and partnerships have a March 15 deadline — one month earlier than individual returns. Bozeman business owners who think "taxes are due April 15" miss this every year. The March 15 date also applies to the S-Corp election itself — Form 2553 must be filed by March 15 to take effect for the current year.

Extension reminder: Filing an extension moves your filing deadline — it does not extend the payment deadline. Any tax owed is still due on the original date. Filing an extension with a balance due and no payment creates both a failure-to-pay penalty and interest from the original due date.

Montana State Tax Obligations for Bozeman Businesses

Montana's state tax structure has meaningful advantages for Bozeman businesses — and specific filing requirements that differ from federal. Understanding both is required for a complete and compliant tax preparation.

Montana income tax

Montana taxes individual income — including pass-through business income — at two rates: 4.7% and 5.9% based on taxable income level (verify current rates at MTrevenue.gov). C-Corporations file a separate Montana corporate income tax return. Montana has no flat tax and no zero-tax bracket for business income above minimal thresholds.

S-Corp: Montana Form PTE

Montana S-Corporations file Form PTE — the Montana Pass-Through Entity Tax Return (Form CLT-4S was discontinued after the 2018 tax year). This is a Montana-specific form with no direct federal equivalent. Form PTE is due March 15, the same deadline as the federal Form 1120-S. A tax preparer unfamiliar with Montana may file the federal return correctly while missing Form PTE entirely.

No Montana sales tax

Montana has no general sales tax. Bozeman businesses do not collect or remit sales tax on goods or services. This is a meaningful compliance simplification compared to Idaho, Wyoming, or Washington. However, Montana does impose a use tax on goods purchased out of state and used in Montana — a frequently overlooked obligation for businesses buying equipment from online vendors.

Montana extension treatment

Montana does not require a separate state extension form if a federal extension has been filed. Your federal Form 4868 or 7004 automatically extends your Montana return. However, any Montana tax owed is still due by the original deadline — April 15 for individuals, March 15 for S-Corps and partnerships. Filing an extension without paying what is owed creates Montana interest charges.

Montana Secretary of State annual report

Every entity registered with the Montana Secretary of State — LLCs, corporations, partnerships — must file an annual report and pay the associated fee. This is a compliance obligation separate from tax filing and is frequently overlooked by first-year businesses. Failure to file eventually results in administrative dissolution of the entity.

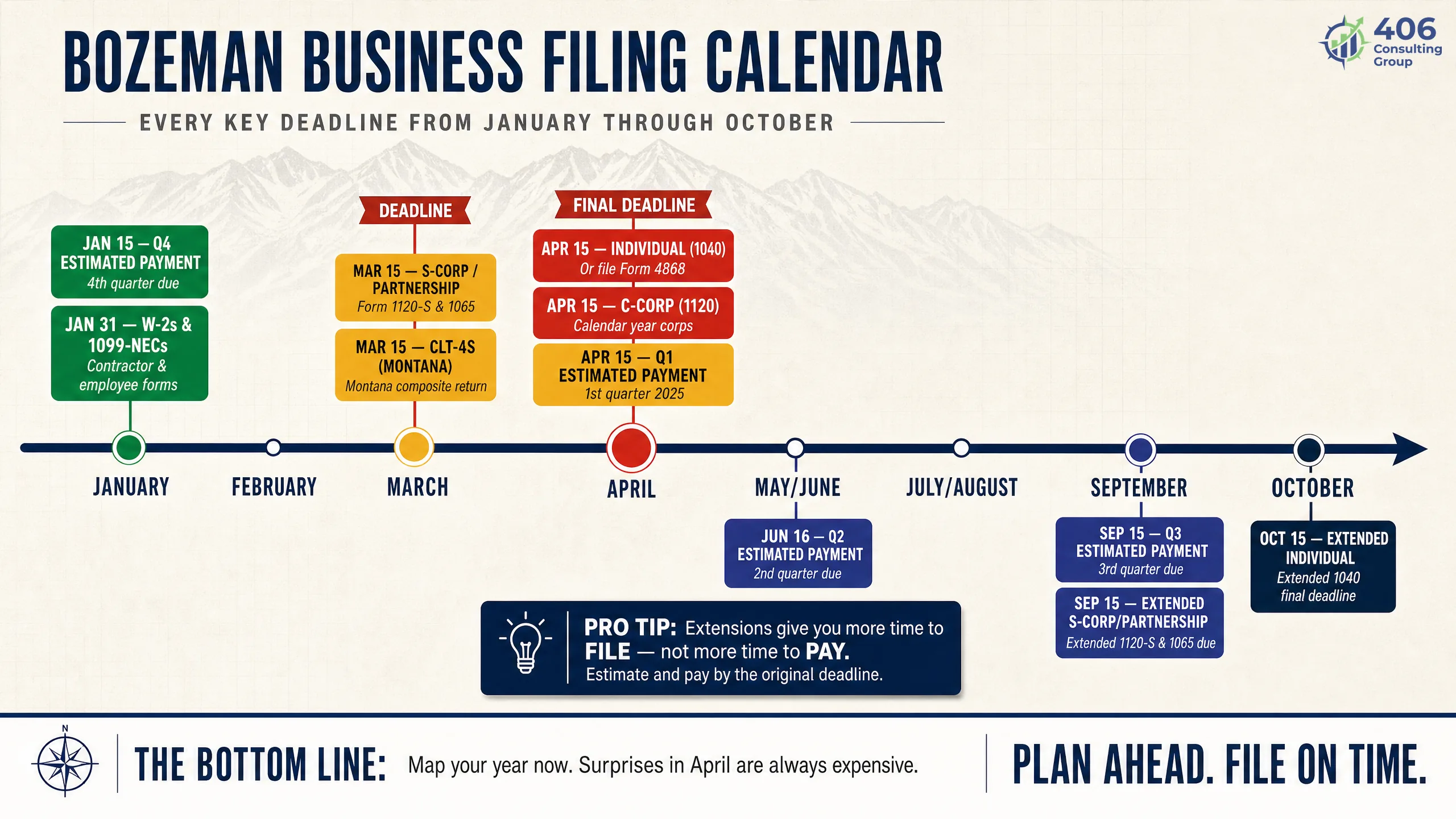

The Bozeman Business Filing Calendar

Tax preparation is not an April event — it is a year-round obligation. Here are the key deadlines a Bozeman business needs to manage from January through October.

January 15

- Q4 estimated tax payment due (federal 1040-ES or EFTPS; Montana pay via DOR TAP portal at mtrevenue.gov)

- Final chance to avoid underpayment penalty for the prior year

January 31

- W-2s delivered to employees

- 1099-NEC delivered to contractors paid $600+ during the year

- 1099-NEC filed with IRS — no extension available for this form

March 15

- S-Corp return (Form 1120-S) due — or 6-month extension (Form 7004)

- Partnership return (Form 1065) due — or 6-month extension

- Montana Form PTE due for S-Corps

- Last day to file S-Corp election (Form 2553) to take effect for the current tax year

April 15

- Individual tax return (Form 1040) due — or Form 4868 for extension

- C-Corp return (Form 1120) due — or Form 7004 for extension

- Montana Form 2 (individual) due

- Q1 estimated payment for the new tax year (federal + Montana)

- SEP-IRA contribution deadline for non-extended returns

June 15 / September 15

- Q2 estimated payment due June 15

- Q3 estimated payment due September 15

- Extended S-Corp and partnership returns due September 15

October 15

- Extended individual and C-Corp returns due

- SEP-IRA contribution deadline for extended returns

- Final opportunity to file the prior year's return without additional late-filing penalty

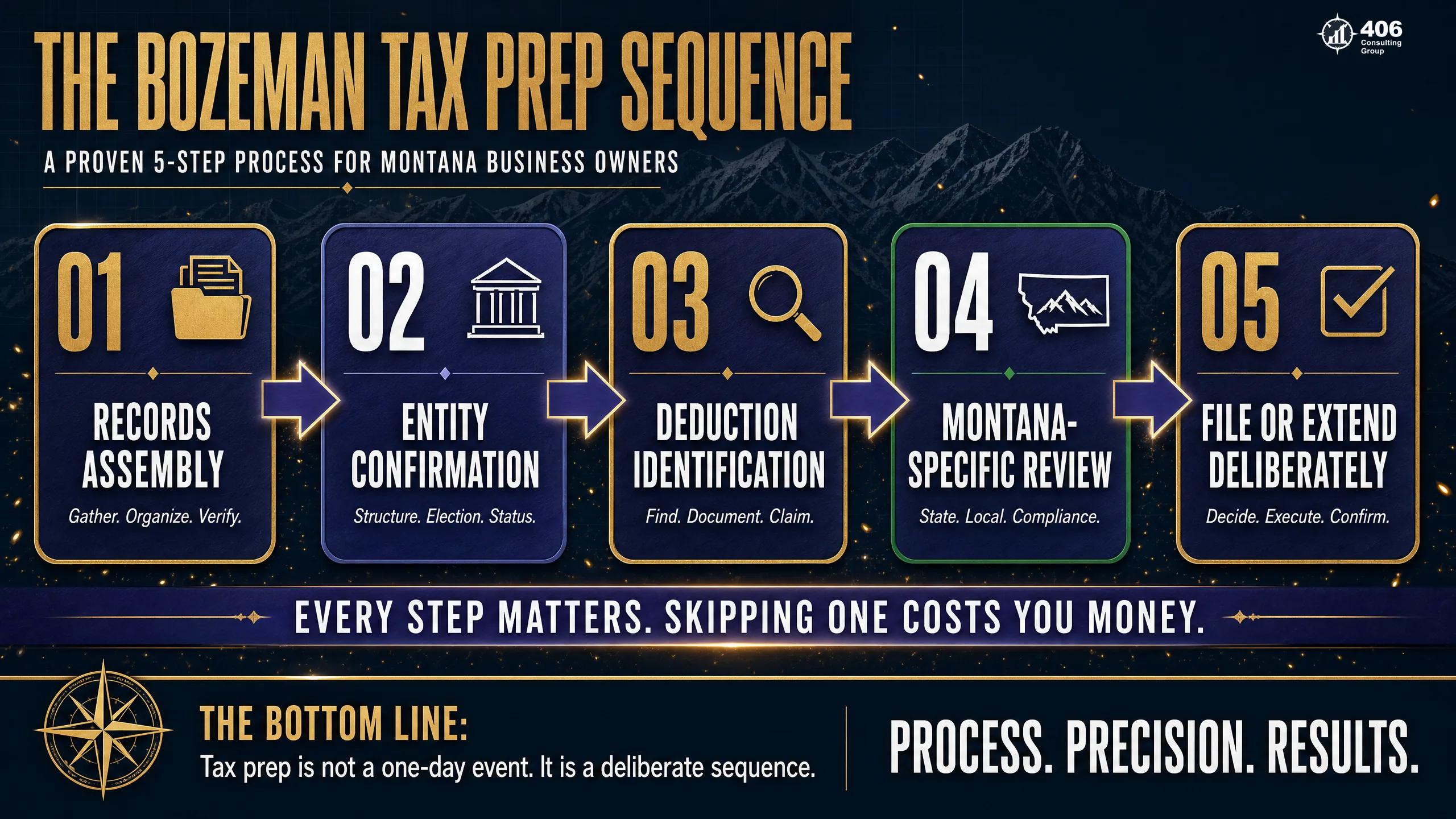

The Bozeman Tax Prep Sequence

The Bozeman Tax Prep Sequence is a five-step pre-filing workflow. Every step must be completed before the return is filed — not after. The sequence is designed to catch what tax software misses: entity structure mismatches, missing deductions, stale depreciation schedules, and Montana-specific obligations.

Records Assembly

Books closed and reconciled before preparation begins

All bank accounts and credit cards reconciled through December 31. Income and expense categories confirmed against bank statements. Payroll records matched to W-2s. All contractor payments identified and matched to W-9s on file. If books are not clean before the preparer starts, the return will be built on estimates — and estimates on tax returns create audit exposure.

Entity Confirmation

Is the current structure still optimal?

Review net profit against prior year and current-year projections. If net profit crossed $80,000–$100,000 for the first time, an S-Corp election analysis is warranted before filing this year's return — the election must be filed by March 15. If the entity is already an S-Corp, confirm that the owner salary is reasonable and that the S-Corp is still cost-justified at the current income level.

Deduction Identification

Every legitimate deduction captured before the return is filed

Walk through the deduction checklist: home office, vehicle mileage, retirement contributions, health insurance premiums, Section 179 elections, bonus depreciation, business meals, software subscriptions, professional development, and any industry-specific deductions. Deductions not identified before the return is filed require an amended return to recover — which costs more than finding them in preparation.

Montana-Specific Review

Federal-correct is not automatically Montana-correct

Confirm Form PTE is required and prepared (S-Corps — Form CLT-4S was discontinued after 2018). Verify Montana Secretary of State annual report has been filed. Confirm Montana estimated payments made during the year match actual liability to identify any underpayment exposure. Check use tax obligations for any out-of-state equipment purchases. Confirm Montana extension treatment if an extension is being filed.

File or Extend — Deliberately

Extension is a tool, not a last resort

If the return is complete and accurate, file by the deadline. If records are incomplete, the entity review surfaced a question that needs resolution, or a deduction is uncertain, file an extension — deliberately, not as a panic move. Pay any tax owed with the extension to stop penalty and interest accrual. Set a target date for filing the extended return — October 15 is too late to start organizing records.

The sequence is not optional. Skipping Steps 1–4 and going directly to Step 5 is how Bozeman businesses end up filing amended returns, missing deductions, and paying penalties they did not owe. Each step exists because something in that step is routinely missed when it is skipped.

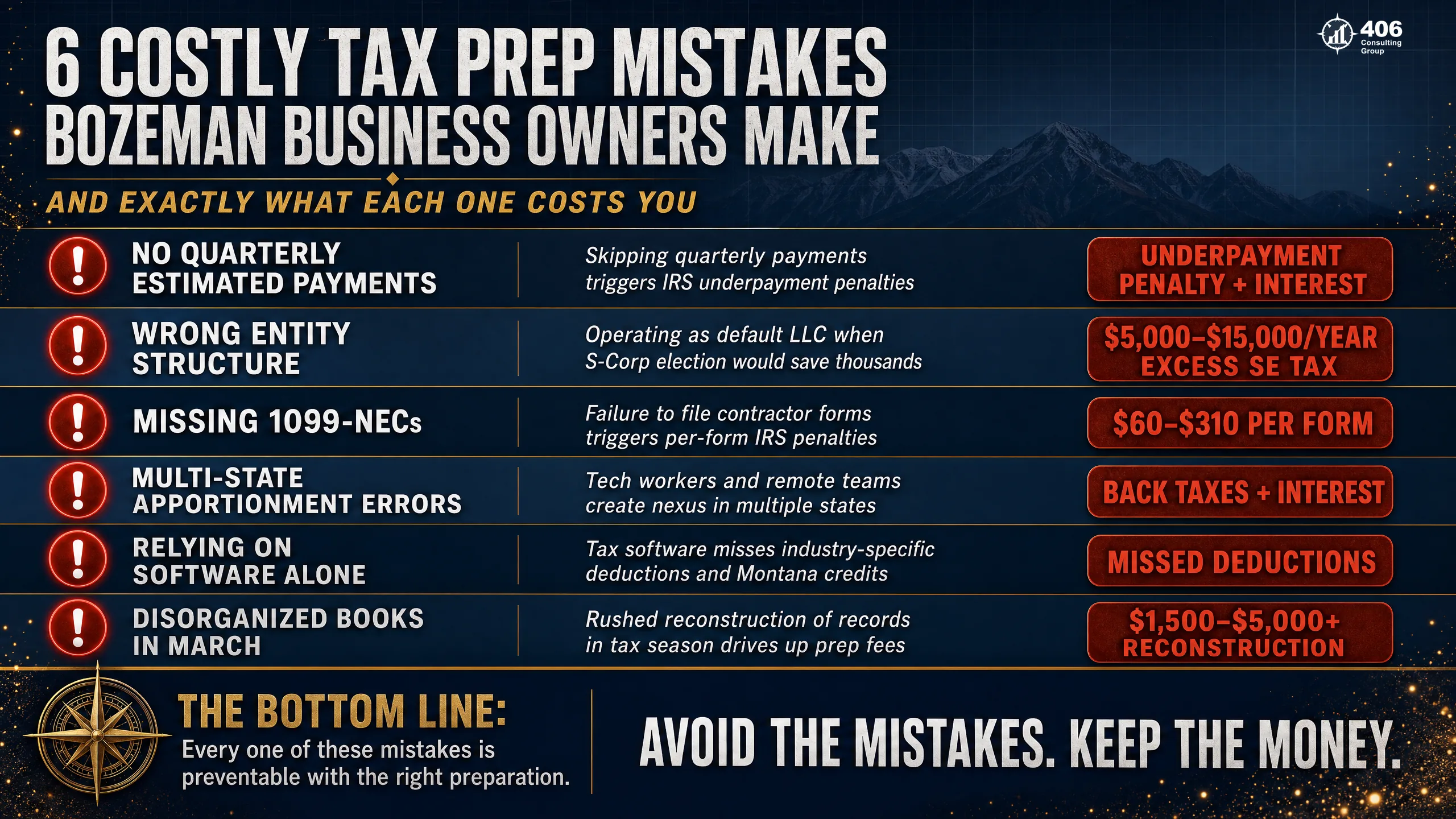

Common Tax Prep Mistakes Bozeman Businesses Make

These are the mistakes that appear in the majority of Bozeman business tax engagements — particularly among first-year businesses and businesses that have outgrown their current preparer.

No quarterly estimated payments in year one

Underpayment penalty + interest from the first missed quarterFirst-year business owners frequently do not know that estimated tax payments are required — or do not realize their new business income is substantial enough to trigger the obligation. The IRS requires quarterly estimated payments if you expect to owe $1,000+ at filing. Montana requires them at $500+. Missing all four quarters creates a penalty that runs from each missed due date, not from April 15.

Wrong entity structure from year one

$5,000–$15,000/year in excess SE tax at $100K+ net profitMany Bozeman businesses start as default single-member LLCs — which is appropriate when starting out. But a business that reaches $100,000+ in net profit and continues operating as a default LLC is paying self-employment tax on the full amount when an S-Corp election could reduce it substantially. The election must be filed by March 15 — and the analysis should happen in the prior Q4, not in March.

Missing contractor 1099-NECs

$60–$330 per form; potential loss of the underlying deductionBozeman's tech and construction sectors both rely heavily on contractors. Every contractor paid $600+ during the year requires a 1099-NEC by January 31. Missing this deadline creates per-form penalties. Beyond the penalty, an IRS examination can challenge the deductibility of contractor payments not reported on a 1099 — turning a missed filing into a disallowed deduction.

Multi-state apportionment errors

Back taxes, interest, and penalties in the state where income should have been reportedBozeman businesses with remote employees in other states, clients in Wyoming or Idaho, or operations that cross state lines face multi-state filing obligations. Montana taxes its residents on all income and non-residents on Montana-source income. Getting the apportionment wrong — or ignoring it — creates exposure in the state where income should have been reported.

Relying on software without a review

Missed deductions + incorrect entity treatment + filing errorsTurboTax and similar software are designed for simple returns. A Bozeman business with an S-Corp election, rental income, multi-state activity, or significant equipment purchases needs a preparer who can identify what the software cannot: the deduction the owner did not know to enter, the state filing that is not in the program's scope, the depreciation election that requires professional judgment.

Disorganized books delivered in March

$1,500–$5,000+ in reconstruction fees; missed deductionsCPAs who receive nine months of unreconciled bank statements in March charge for the reconstruction — or file based on incomplete information. Either outcome costs the business owner more than organized books would have. Clean books by January 31 give a preparer the input they need to file an accurate, complete return without a premium for emergency cleanup.

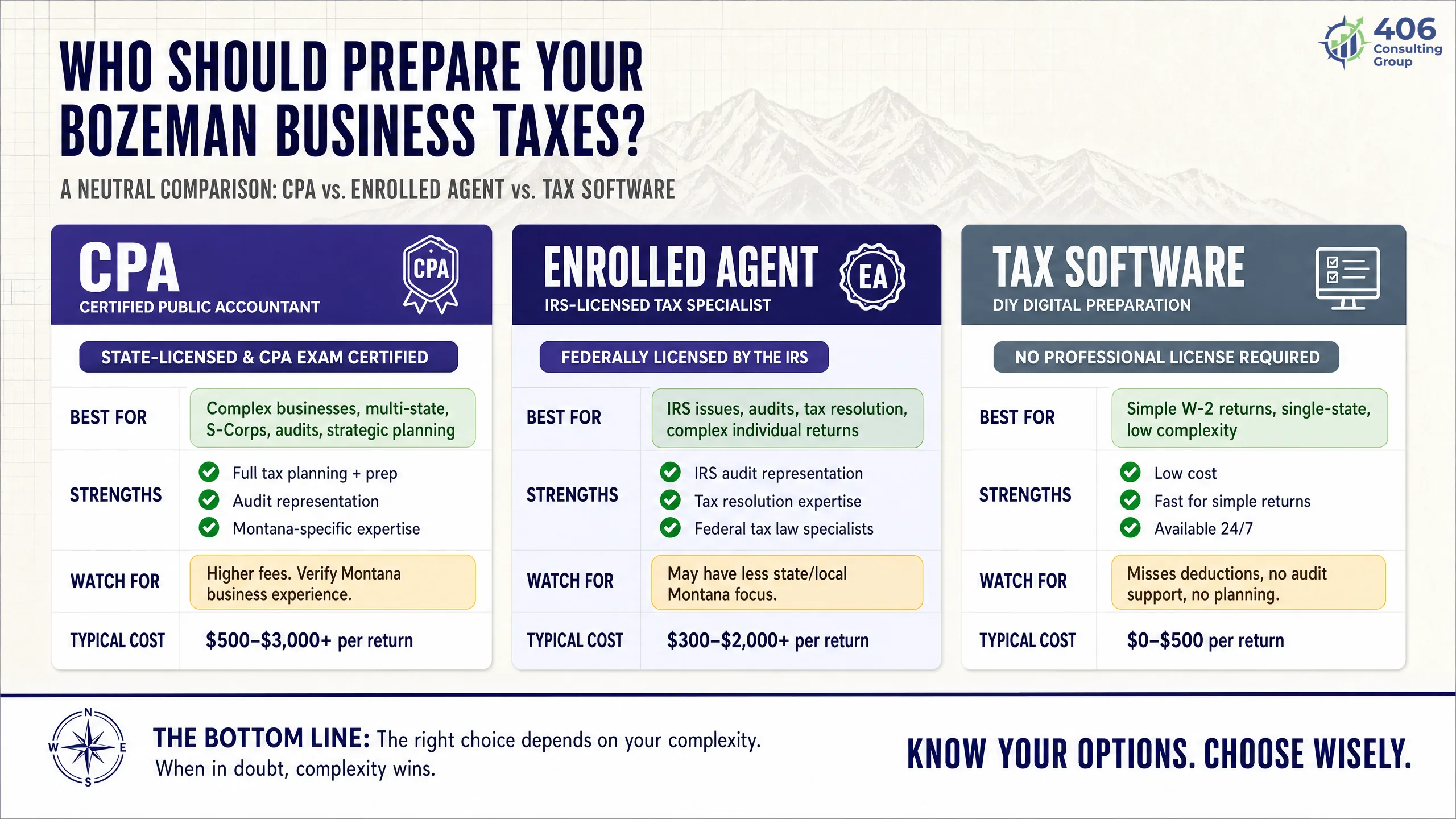

Choosing a Tax Preparer in Bozeman

Not all tax preparers are equivalent — and in a market as varied as Bozeman, the difference between the right preparer and the wrong one is measured in thousands of dollars per year. Here is how to evaluate the options.

CPA

Certified Public Accountant — licensed by state board

Best for

Complex business returns, S-Corps, multi-state, audit representation

Watch for

Not all CPAs specialize in business tax — confirm they handle your entity type and industry regularly

Enrolled Agent

IRS-credentialed — authorized to represent taxpayers before the IRS

Best for

Federal tax compliance, audit representation, IRS issue resolution

Watch for

May not have deep Montana state tax experience — confirm Montana Form PTE (S-Corp pass-through return) and other state-specific filing familiarity

Tax Software

No credential — software only, no professional review

Best for

Simple sole prop returns with straightforward income and deductions

Watch for

Not appropriate for S-Corps, multi-state filers, real estate investors, or businesses with significant assets — the software cannot exercise judgment

Questions to Ask a Prospective Tax Preparer

Do you prepare returns for S-Corporations regularly — including Montana Form PTE (the pass-through entity return)?

How many returns do you prepare for businesses in my industry each year?

Do you handle multi-state apportionment for Montana businesses with out-of-state activity?

What is your process if the IRS contacts my business after you file?

Do you review entity structure as part of preparation — or only prepare the return as presented?

What information do you need from me, and by what date, to file without an extension?

Red flags: A preparer who has never heard of Montana Form PTE (the S-Corp pass-through return that replaced Form CLT-4S after 2018). A preparer who does not ask about entity structure. A preparer who guarantees a refund before reviewing your records. A preparer who charges a percentage of your refund. These are signs that the preparer is optimized for volume, not accuracy.

Industry Tax Prep Considerations in Bozeman

Bozeman's four dominant industry sectors each carry tax prep complexity that a generalist preparer may not handle correctly. Here is what matters by industry.

Tech Startups and Remote Workers

R&D Tax Credit

Bozeman tech companies engaged in qualified research activities may be eligible for the federal R&D tax credit — a dollar-for-dollar reduction in tax liability, not just a deduction. Qualified expenses include wages for employees engaged in R&D, contractor costs for R&D, and supply costs. This credit is frequently missed by preparers unfamiliar with the tech sector.

Equity compensation

Stock options, restricted stock units, and 83(b) elections are common in Bozeman startups. Each has distinct tax treatment. Incentive stock options (ISOs) create AMT exposure. NSOs are taxed as ordinary income at exercise. An 83(b) election on restricted stock starts the capital gains clock at grant — but must be filed within 30 days of grant or the opportunity is permanently lost.

Remote worker multi-state filing

A Bozeman business with remote employees in other states may have payroll tax and income tax nexus in those states. Montana residents working remotely for out-of-state companies pay Montana income tax on that income. The intersection of Montana residency and remote work income requires careful treatment in both the employer's payroll system and the employee's individual return.

Construction and Trades

Job costing and deductions

Construction tax prep is only as accurate as the job costing underneath it. Materials, subcontractors, equipment, and direct labor must be captured per job to maximize deductions and demonstrate legitimate business expenses under audit. A Bozeman contractor who cannot produce job-level profit and loss during an IRS examination is at a disadvantage.

Section 179 and equipment depreciation

Heavy equipment — excavators, skid steers, work trucks, trailers — qualifies for Section 179 and bonus depreciation. These are annual elections that require the preparer to walk through the asset list and calculate the optimal depreciation strategy. Automatic MACRS depreciation on a large equipment purchase may leave significant first-year deductions on the table.

Prevailing wage and certified payroll

Montana and federal public projects require prevailing wage payroll at rates set by the Montana Department of Labor. The payroll complexity — different rates per classification, certified payroll reporting — is a compliance obligation separate from tax filing. A CPA who manages construction tax prep should understand how prevailing wage records interact with job costing and payroll tax deposits.

Outdoor Recreation and Hospitality

Seasonal income and estimated payments

Bozeman's outdoor recreation and hospitality businesses — ski shops, outfitters, tour operators, restaurants — experience significant seasonal revenue swings. A business that earns 70% of its annual revenue in Q2 and Q3 needs estimated payments calibrated to that timing, not smoothed quarterly projections. Underpaying in high-revenue quarters and overpaying in slow quarters is a cash flow problem that good tax planning prevents.

Tip reporting compliance

Hospitality businesses with tipped employees must report tips as wages, withhold payroll taxes on tips, and remit employer FICA on tipped wages. The FICA tip credit (Form 8846) allows employers to claim a credit for FICA paid on tips above the federal minimum wage — a significant benefit that many Bozeman restaurant operators miss.

Short-term rental treatment

Bozeman's real estate market has created a large short-term rental economy through platforms like Airbnb and VRBO. Short-term rental income is taxable and must be reported on Schedule E. If the owner provides substantial services (cleaning, concierge), the income may be treated as self-employment income on Schedule C — triggering SE tax. The treatment matters significantly for total tax liability.

Real Estate Investors

Depreciation scheduling

Residential rental property is depreciated over 27.5 years; commercial property over 39 years. Cost segregation studies can accelerate depreciation by reclassifying components of the property to shorter depreciation lives. For a Bozeman rental property acquired at current valuations, a cost segregation study can produce substantial first-year deductions that straight-line depreciation never would.

1031 exchange compliance

A 1031 exchange allows a Bozeman investor to defer capital gains tax on the sale of investment property by reinvesting proceeds into a like-kind property. The rules are strict: 45-day identification period, 180-day close requirement, qualified intermediary required. A missed deadline or non-qualifying property permanently disqualifies the exchange and triggers the deferred gain.

Passive activity loss rules

Rental activity losses are generally 'passive' and can only offset passive income — not wages or business income — unless the real estate professional exception applies. A Bozeman investor with significant rental losses and high W-2 income needs a preparer who understands passive activity loss rules and can structure activity to maximize deductibility.

Virtual Tax Preparation: Why Bozeman Businesses Use Remote CPAs

The assumption that tax preparation requires an in-person relationship is outdated — and for many Bozeman businesses, a virtual tax preparer with the right specialization outperforms a local generalist who happens to be nearby. Here is how virtual tax prep works and when it makes sense.

Specialization over geography

A Bozeman tech startup or real estate investor benefits more from a CPA who prepares 200 similar returns per year than from a local generalist who has prepared three. Virtual tax prep gives Bozeman businesses access to specialists who are not geographically constrained — the right expertise, not just the nearest office.

Secure document delivery

Virtual tax preparation uses encrypted client portals for document delivery and return review. Tax documents — W-2s, 1099s, bank statements, depreciation schedules — are uploaded once, reviewed remotely, and returned as a completed return for e-signature. The process is more secure than emailing PDFs and more efficient than an in-person appointment.

Year-round access, not just filing season

The best virtual tax relationships are not transactional — they are advisory. A good remote CPA is reachable in September when you are considering an equipment purchase, in November when you are reviewing entity structure, and in January when estimated payment planning matters. Proximity does not determine accessibility; the firm's model does.

What you need to provide

For a complete virtual tax preparation, you will typically need to provide: prior year return, current year bookkeeping (reconciled), payroll records or W-2s, 1099s received, bank and investment statements, vehicle mileage log, depreciation schedule from the prior year, and any major asset purchase receipts. Most of this is what you should have organized by January 31 regardless.

406 Consulting Group's remote model: We serve Bozeman businesses entirely virtually — from onboarding through return delivery. Our clients upload documents through a secure portal, review their draft return with us on a video call, and e-sign the final return. We manage Montana-specific filings, S-Corp elections, and year-round tax planning the same way we manage everything else: remotely, efficiently, and without requiring a trip across town.

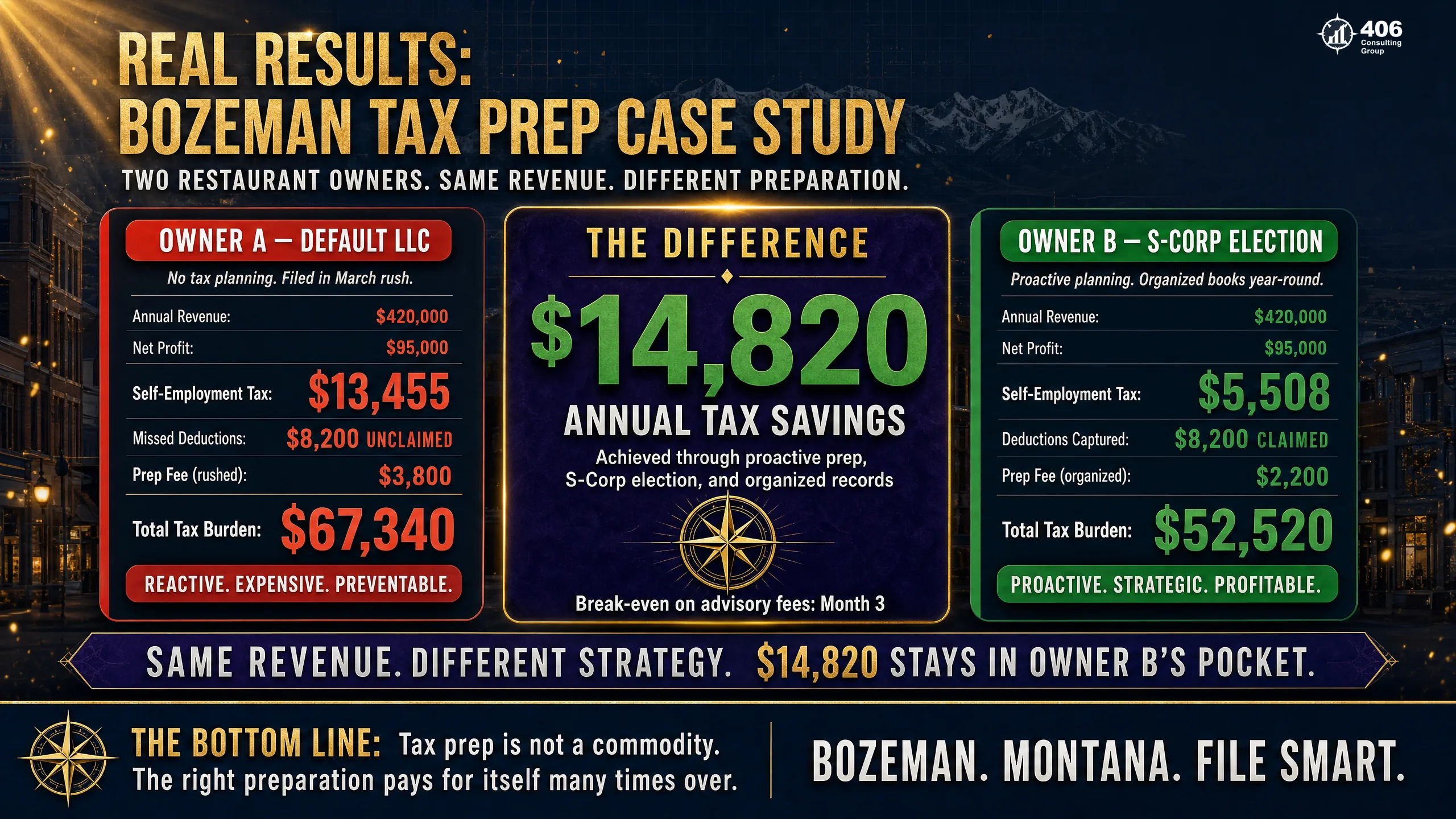

Case Study: Two Bozeman Businesses, Same Revenue — Different Outcomes

Anonymized — Bozeman, MT

Tech Consultant vs. General Contractor — Same Revenue, Different Prep

Annual gross revenue (both)

$200,000

Years in business

3 years

Entity structure

Both filed as default LLC

Business A — Tech Consultant (Reactive, Software-Only)

Business B — General Contractor (Proactive, CPA-Prepared)

$52,400

Business A total tax burden

$29,800

Business B total tax burden

$22,600

Annual difference — same revenue

The $22,600 difference came from four decisions — all made before April 15.

- S-Corp election: reduced SE tax from $23,715 to $12,240 — saving $11,475

- Solo 401(k) contribution: $23,500 deduction (2025 limit) at a combined 28% marginal rate — saving $6,580

- Section 179 on the truck: $40,000 expensed immediately instead of depreciated over 5 years

- Quarterly estimated payments: eliminated $620 Montana underpayment penalty

* SE tax is calculated on 92.35% of net profit per IRS Schedule SE. The $23,715 figure is simplified for illustration; actual SE tax at $155,000 net profit is approximately $21,901.

Frequently Asked Questions: Tax Preparation for Bozeman, MT Businesses

What taxes does a Bozeman, MT business owner need to file?

A Bozeman business owner typically files: a federal income tax return (Form 1040 with Schedule C for sole props, Form 1120-S for S-Corps, Form 1065 for partnerships, or Form 1120 for C-Corps); a Montana income tax return (Form 2 for individuals, Form PTE for S-Corps); quarterly federal and Montana estimated tax payments if net income is sufficient; payroll tax deposits if they have employees; and an annual Montana Secretary of State report. The exact filings depend on entity structure and business activity.

What is the tax filing deadline for a business in Bozeman, Montana?

Deadlines depend on entity type. S-Corporations and partnerships are due March 15 (federal Form 1120-S or Form 1065; Montana Form PTE for S-Corps). Sole proprietorships and single-member LLCs file on the individual return, due April 15. C-Corporations are also due April 15. All deadlines can be extended — S-Corps and partnerships to September 15, individuals and C-Corps to October 15 — but any tax owed is still due on the original date. Montana automatically accepts the federal extension; no separate state extension form is required.

Do Bozeman businesses need to pay quarterly estimated taxes?

Yes. The IRS requires quarterly estimated payments if you expect to owe $1,000 or more at filing. Montana requires them if you expect to owe $500 or more. Due dates: January 15, April 15, June 15, September 15. The safe harbor calculation — paying 100% of last year's tax liability (110% if AGI exceeded $150,000) in four equal installments — avoids underpayment penalties regardless of current-year income. Missing estimated payments triggers a penalty that accrues from the missed due date, not from April 15.

How do I know if my Bozeman business should be an S-Corp?

The S-Corp election typically makes financial sense when net annual profit consistently exceeds $80,000–$100,000. At that income level, the self-employment tax savings from paying yourself a salary (subject to FICA) and taking the remainder as distributions (not subject to FICA) typically exceed the additional compliance costs — payroll, the S-Corp return, Montana Form PTE. The election must be filed by March 15 to take effect for the current tax year. The analysis should happen in Q4 of the prior year, not in March. See our S-Corp tax benefits guide for the full break-even analysis.

Can I use a virtual tax preparer for my Bozeman business?

Yes — and for many Bozeman businesses, a virtual preparer with the right specialization is a better choice than a local generalist. Virtual tax preparation uses secure encrypted portals for document delivery and return review. The process eliminates the need for in-person appointments while giving you access to preparers who specialize in your entity type, industry, or specific Montana filing requirements. The only prerequisite is organized records — which you should have regardless of who prepares your return.

What should I look for in a tax preparer in Bozeman, MT?

Look for a preparer who: prepares your entity type regularly (S-Corp, partnership, etc.); is familiar with Montana-specific forms including Form PTE (the S-Corp pass-through return that replaced Form CLT-4S after 2018); has experience with your industry; reviews entity structure as part of preparation rather than just filing whatever you present; has a clear process for what information they need and when; and can represent you before the IRS if needed. Red flags include a preparer unfamiliar with Montana Form PTE, who guarantees a refund before reviewing your records, or charges a percentage of your refund.

Does 406 Consulting Group provide tax preparation services in Bozeman, MT?

Yes. 406 Consulting Group provides tax preparation, tax planning, S-Corp election analysis, bookkeeping, and fractional CFO services for businesses in Bozeman and across Montana and the Intermountain West. We work entirely virtually — clients upload documents through a secure portal, review their draft return with us on a video call, and e-sign the completed return. Carrie Anderson's background in commercial banking and tax strategy is directly relevant for Bozeman businesses navigating entity structure decisions, multi-state filings, and year-round tax planning. Contact us to discuss what a tax preparation engagement looks like for your business.

Is an S-Corp election right for your Bozeman business? Read our full S-Corp tax benefits guide — including the Montana-specific break-even analysis. Or run the numbers now with our S-Corp Savings Calculator.

External Resources

Bozeman, MT

Ready for Tax Preparation That Gets It Right?

406 Consulting Group provides virtual tax preparation, S-Corp election analysis, and year-round tax planning for Bozeman and Montana businesses. We follow the Bozeman Tax Prep Sequence — every engagement, every year.

The Bozeman Tax Prep Sequence

Five steps before you file

Records Assembly

Books closed and reconciled

Entity Confirmation

Is the structure still optimal?

Deduction Identification

Every deduction captured

Montana-Specific Review

Form PTE, SOS report, use tax

File or Extend — Deliberately

Pay what's owed; set a target date

Bozeman Filing Deadline Quick Reference

Q4 estimated payment

W-2s and 1099-NECs to recipients

S-Corp / partnership returns + Form PTE

S-Corp election (Form 2553) deadline

Individual + C-Corp returns + Q1 payment

Q2 estimated payment

Q3 payment + extended S-Corp/partnership

Extended individual + C-Corp deadline

Related Reading

About the Author

Carrie Anderson

Tax Strategist, 406 Consulting Group

20+ years in commercial banking and tax strategy. Specializes in S-Corp election analysis, entity structure, and tax planning for Montana and Intermountain West businesses.

Tax prep done right — virtually, from anywhere in Montana.

We follow the Bozeman Tax Prep Sequence for every engagement — records to return.

Schedule a Consultation