Navigating Tax Season:

A Guide for Billings, MT Businesses

For most Billings business owners, tax season is a March scramble. Here’s the year-round framework that changes how you manage it — and how much you pay.

In This Guide

- 1.Why Tax Season Feels Different in Billings

- 2.What Your Billings Business Actually Owes

- 3.The Billings Business Tax Cycle

- 4.Phase 1 — Close: October–December

- 5.Phase 2 — File: January–April 15

- 6.Phase 3 — Plan: April–June

- 7.Phase 4 — Prep: July–September

- 8.Common Tax Season Mistakes Billings Owners Make

- 9.Industry Tax Considerations in Billings

- 10.Entity Structure: Are You Taxed the Right Way?

- 11.Case Study: Billings Medical Practice

- 12.Frequently Asked Questions

For most Billings business owners, "tax season" means February through April — a stressful sprint to gather receipts, rebuild records, and hand something coherent to a CPA. The businesses that consistently pay less tax do not approach it that way. They manage taxes across all twelve months, making the decisions that matter before December 31 rather than scrambling to undo them in March.

This guide covers Montana's specific tax structure, the decisions that actually move the number, and a full-year calendar for Billings businesses — from the largest healthcare practice to the sole-proprietor electrician working Yellowstone County jobs.

Why Tax Season Feels Different in Billings

Billings is Montana's largest city — 120,000+ residents, the Yellowstone County seat, and the economic hub of Eastern Montana and the Northern Great Plains. The city's economy is more complex than most of Montana's smaller markets, and that complexity shows up at tax time.

Multi-state business activity

Billings sits near the Wyoming border, and many businesses have employees working in both states or revenue from Wyoming operations. Wyoming has no state income tax — which creates payroll apportionment questions Montana-only businesses never face. Bakken oil field activity also brings North Dakota income into the picture for energy-adjacent businesses.

Industry-specific tax complexity

Billings' dominant industries — healthcare (Billings Clinic, St. Vincent), construction, oil and gas services, and agriculture — each carry unique tax treatment that generic tax software does not handle well. Healthcare practice structure, construction job costing, royalty depletion, and farm income averaging all require specialized knowledge.

Eastern Montana seasonality

Construction, agriculture, and tourism businesses in Yellowstone County experience significant seasonal cash flow swings. Quarterly estimated payments — calculated on smoothed annual projections — frequently mismatch actual income timing, creating surprise underpayment penalties for businesses with strong Q2 and Q3 but slow Q4.

A growing professional services sector

Billings has absorbed significant business migration from higher-tax states. These businesses often arrive with complex entity structures, multi-state filing obligations, and deferred tax positions from asset sales that require careful unwinding for Montana tax purposes.

The implication:Billings businesses need a tax professional who understands both Montana's specific rules and the industry-specific issues relevant to their sector. A generalist CPA who files individual 1040s is not the same as an accountant who manages S-Corp elections, job cost deductions, and multi-state apportionment for a Billings contractor.

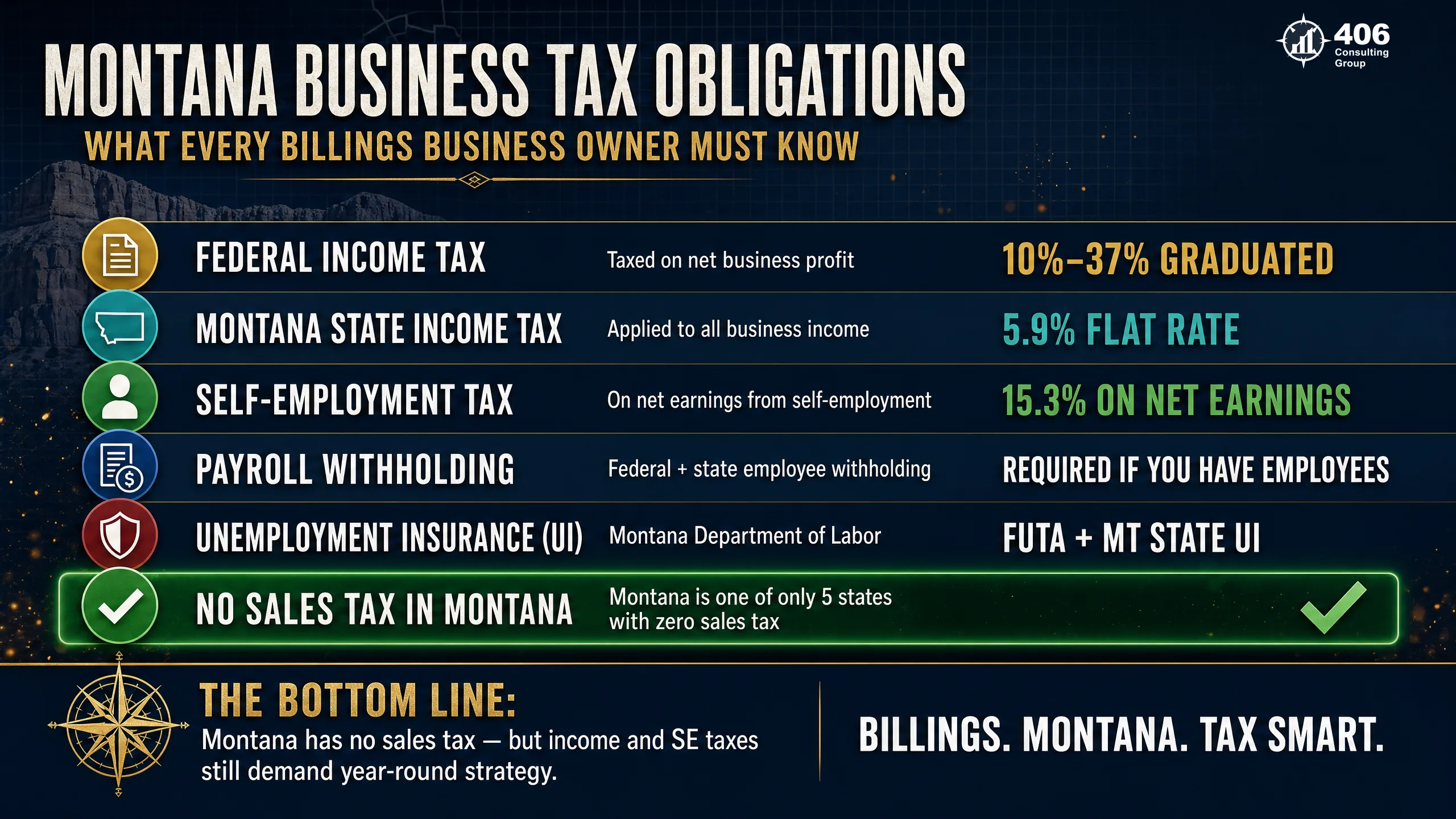

What Your Billings Business Actually Owes

Montana's tax structure is different from most states — and understanding what you actually owe (and what you do not owe) is the starting point for every Billings business tax conversation.

| Tax | Who It Applies To | Rate / Amount | Paid To |

|---|---|---|---|

| Montana income tax | All businesses / owners | 4.7%–5.9% on taxable income | MT Dept. of Revenue |

| Federal income tax | All businesses / owners | 10%–37% (individual brackets) | IRS |

| Self-employment tax | Sole props, partners, LLC members | 15.3% up to SS wage base + 2.9% above | IRS |

| Payroll withholding | Businesses with W-2 employees | Per employee W-4 | IRS + MT DOR |

| Montana unemployment insurance | Businesses with employees | Variable; new employer rate applies first 3 years | MT Dept. of Labor |

| Workers' compensation | Required for all Montana employers | Varies by industry / payroll | MT State Fund or private carrier |

| SOS annual report | All registered entities | $20/year (most entities) | MT Secretary of State |

| Sales tax | N/A | Montana has no general sales tax | N/A |

The no-sales-tax advantage:Montana's lack of a general sales tax is a genuine competitive advantage for Billings businesses. Retail and service operations here carry a lower compliance burden than counterparts in Idaho, Wyoming (for some goods), or Washington. However, Montana does impose a use tax on goods purchased out of state and used in Montana — if your business buys equipment from out-of-state vendors, use tax may apply.

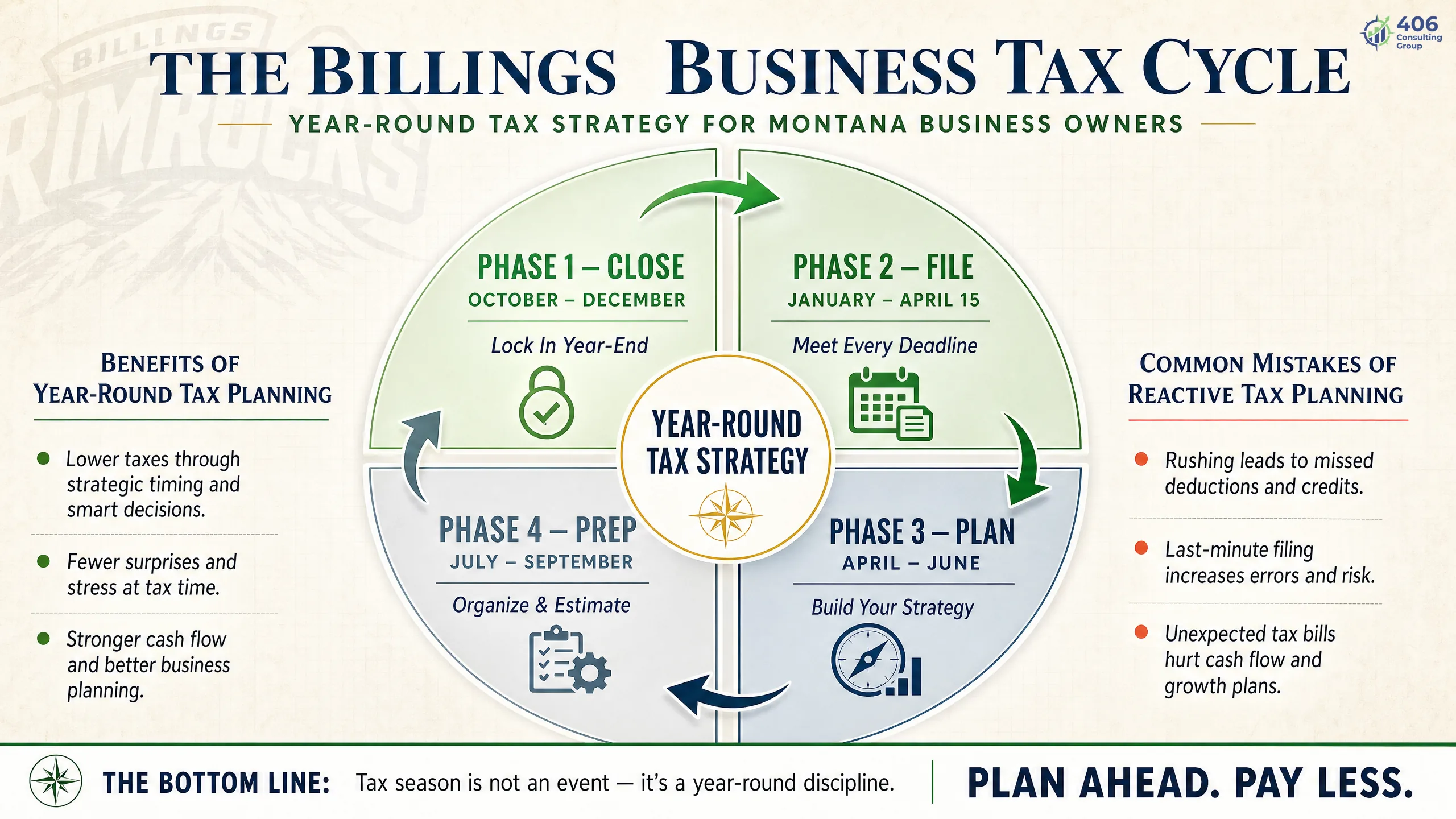

The Billings Business Tax Cycle

The Billings Business Tax Cycle reframes tax management as a year-round discipline rather than an April event. The cycle has four phases — each with specific decisions that determine your tax outcome for the year. Missing Phase 1 (Close) is what creates the scramble in Phase 2 (File).

Close

When the real decisions get made

- Max retirement contributions before Dec 31

- Section 179 and bonus depreciation elections

- Year-end payroll and bonus decisions

- Q4 estimated payment (due January 15)

- Entity structure review with your accountant

File

When the calendar forces your hand

- W-2s and 1099-NECs to recipients by January 31

- S-Corp and partnership returns by March 15

- Individual and C-Corp returns by April 15

- Q1 estimated payment due April 15

- Extension if needed — pay first, file later

Plan

When most owners stop — and shouldn't

- Post-filing debrief with your accountant

- Q2 estimated payment due June 15

- Late S-Corp election relief if March deadline missed

- Mid-year payroll and withholding review

- Year-to-date bookkeeping cleanup

Prep

When you build the foundation

- Q3 estimated payment due September 15

- Year-end projection meeting with accountant

- Depreciation scheduling for Q4 equipment purchases

- 1099 contractor list review — collect W-9s now

- Bookkeeping audit for the full year to date

The key insight: The decisions made in Phase 1 (October–December) determine roughly 70% of your tax outcome. Phase 2 is mostly execution — filing returns that reflect decisions already made. The business owners who pay less tax are not better at filing; they are more deliberate in October and November.

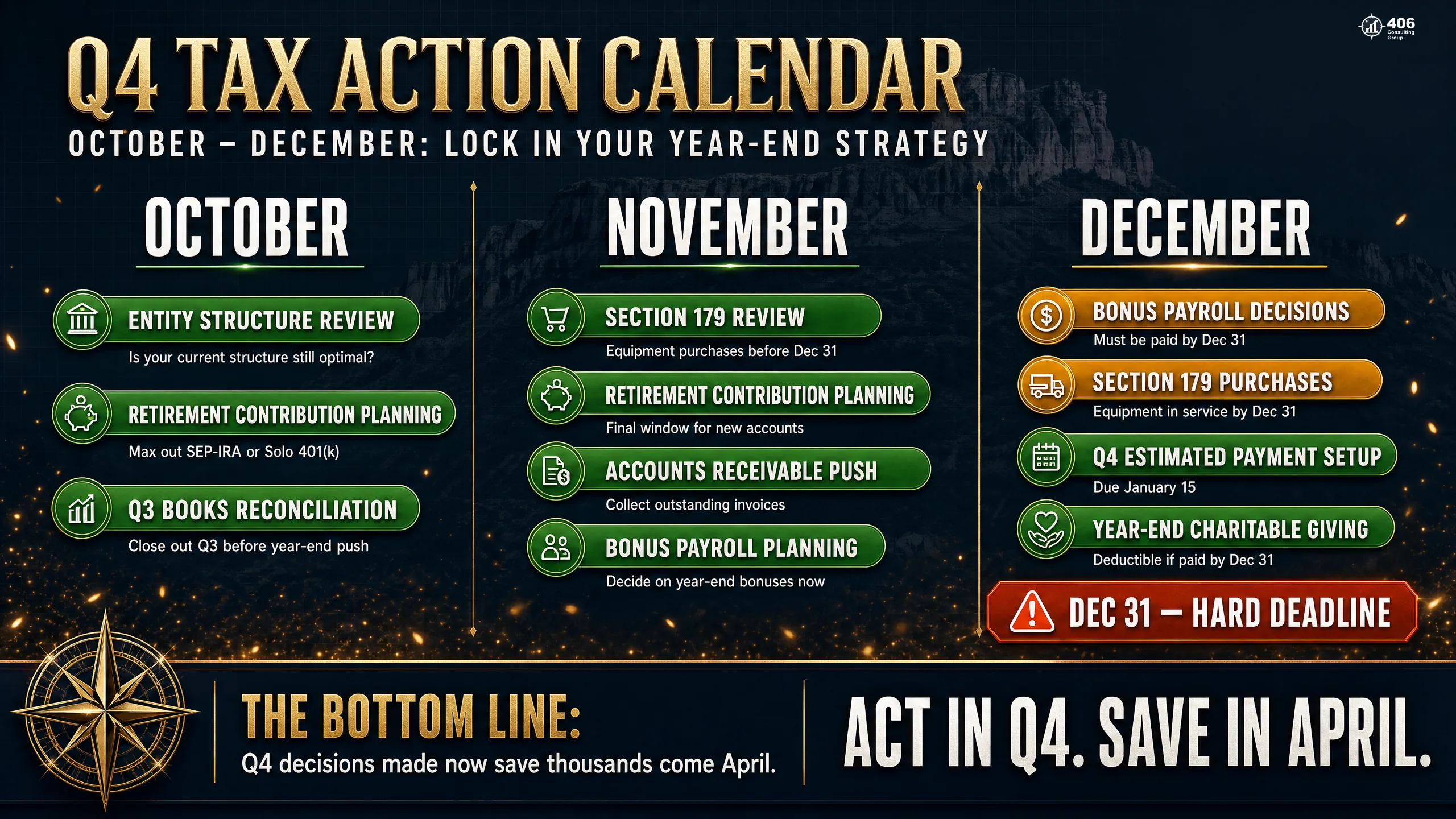

Phase 1 — Close: The October–December Moves That Matter

Most of the meaningful tax reduction strategies available to a Billings business owner have a December 31 deadline. After that date, the options narrow to what you can do on a return — which is considerably less. Here are the high-impact moves, in priority order.

Maximize retirement contributions

A Solo 401(k) must be established by December 31 of the year you want to contribute — the account must exist even if the actual contribution can be made until the tax return due date (including extensions). A SEP-IRA can be opened and funded as late as the extended return deadline (October 15). For a Billings sole proprietor at $180,000 net profit, a Solo 401(k) contribution up to the current IRS limit (verify at irs.gov/retirement-plans) reduces taxable income dollar-for-dollar — saving $4,000+ in combined federal and Montana taxes at common contribution levels. See the year-end financial checklist for the full December 31 decision list.

Section 179 and bonus depreciation elections

Section 179 allows immediate expensing of qualifying business property placed in service during the tax year — up to the annual limit (verify current limit at IRS.gov). Bonus depreciation allows additional first-year expensing on qualifying property. For Billings construction firms, medical practices, and oil field service companies with significant equipment purchases, these elections can reduce taxable income by tens of thousands of dollars in the purchase year. The asset must be placed in service by December 31 — ordered and paid for is not enough.

Year-end payroll and bonus decisions

Bonuses paid by December 31 are deductible in the current tax year for cash-basis businesses — the vast majority of Billings small businesses. Bonuses accrued but not paid are not. For S-Corp owner-employees, this is also the time to review whether your salary has been reasonable and consistent. If your Q4 looks profitable, your accountant may recommend a salary adjustment to maintain defensible consistency.

Accounts receivable timing

Cash-basis Billings businesses recognize income when payment is received, not when invoiced. If you are approaching the upper end of a tax bracket or have had an unusually profitable year, deliberately delaying invoices to January can shift income into the next tax year. This is a conversation to have with your accountant using projected numbers — not a guess.

Q4 estimated payment setup

The fourth quarterly estimated tax payment is due January 15. Calculating it in December — based on your full-year actual numbers rather than an estimate — ensures you pay enough to avoid underpayment penalties without overpaying. For Montana, both federal (1040-ES or EFTPS) and state (Montana Form EST) estimated payments are required if you expect to owe more than $500 at Montana filing.

Entity structure review

If your net profit has grown past $80,000–$100,000 and you are still filing as a default LLC, your Q4 accountant meeting should include an S-Corp election analysis. The election must be filed by March 15 of the year it takes effect (see our S-Corp election deadline guide for what to file and when). Making the decision in October or November gives you time to prepare properly — not the week before the deadline.

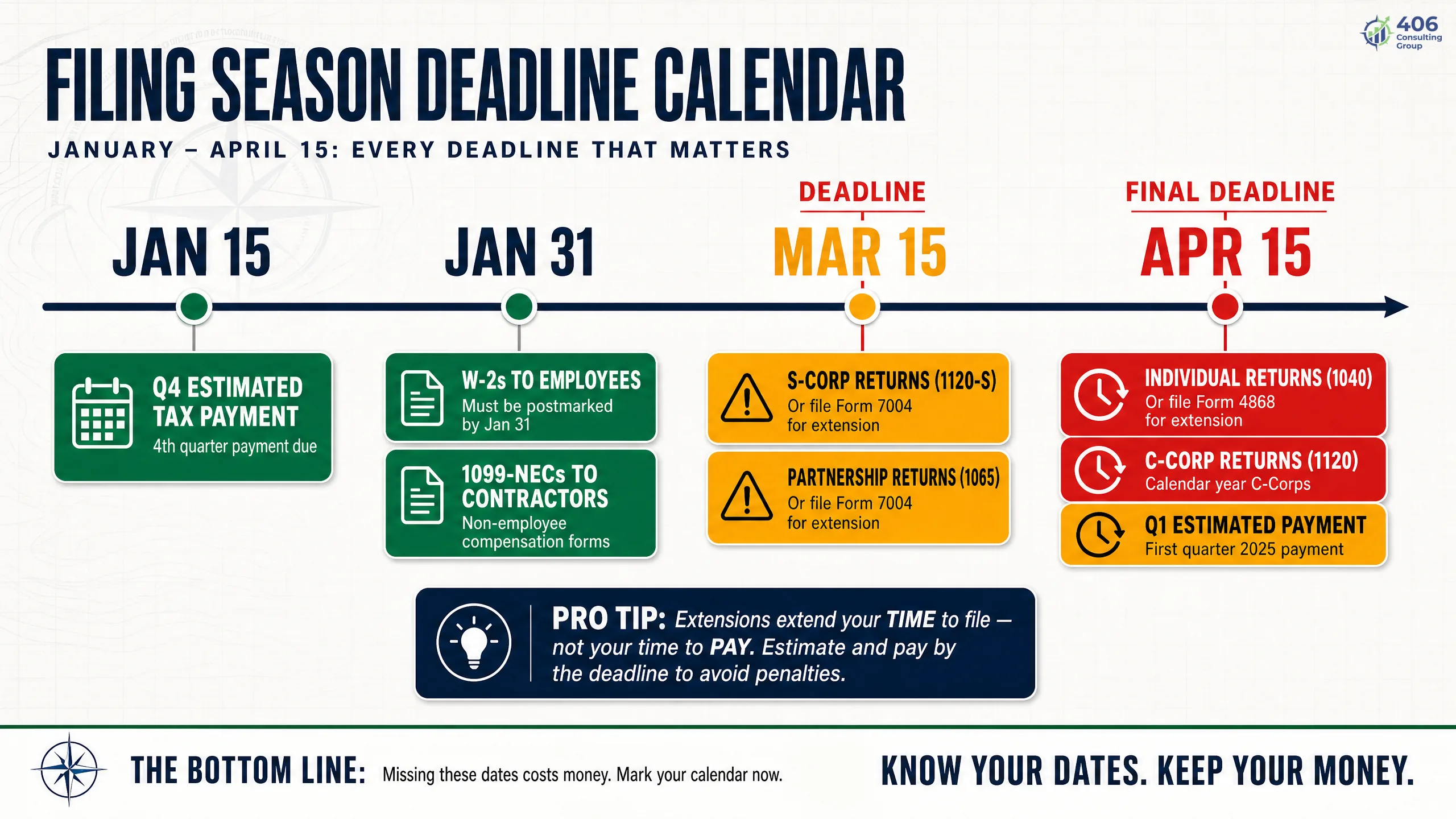

Phase 2 — File: The January–April 15 Calendar

Filing season runs from January 1 through April 15 — but the deadlines are not all on April 15. Missing the earlier ones creates penalties that compound. Here is the full calendar for Billings, Montana businesses.

January 15

- Q4 estimated tax payment due (federal 1040-ES or EFTPS; Montana Form EST)

- Alternative: file and pay full return by Feb 1 to skip the Jan 15 estimated payment

January 31

- W-2s delivered to employees

- 1099-NEC delivered to contractors paid $600+ during the year

- 1099-NEC filed with IRS (paper and electronic — no extension available for this form)

- FUTA annual return (Form 940) if not deposited quarterly

February 28 / March 31

- 1099-MISC, 1099-INT, 1099-DIV and other information returns filed with IRS (Feb 28 paper, Mar 31 electronic)

- Montana 1099 filing follows federal deadlines

March 15

- S-Corporation return (Form 1120-S) due — or 6-month extension (Form 7004)

- Partnership return (Form 1065) due — or 6-month extension (Form 7004)

- Montana pass-through entity return (Form PTE) due for S-Corps

- Last day to file S-Corp election (Form 2553) for the current tax year

April 15

- Individual income tax return (Form 1040) due — or file Form 4868 for 6-month extension

- C-Corporation return (Form 1120) due — or 6-month extension

- Montana individual income tax return (Form 2) due

- Q1 estimated payment for the new tax year (federal + Montana)

- SEP-IRA contribution deadline for non-extended returns

Extension: The Most Misunderstood Tool in Tax Filing

What an Extension Does

- Moves your filing deadline to October 15 (individuals) or September 15 (S-Corps, partnerships)

- Eliminates the failure-to-file penalty (5%/month, up to 25%)

- Gives time to collect complete information and avoid amended returns

- Automatic — no reason required, no IRS approval needed

What an Extension Does NOT Do

- Does not extend the payment deadline — taxes owed are still due April 15

- Does not stop interest from accruing on unpaid balances

- Does not delay the Q1 estimated payment due date

- Does not apply to 1099-NEC filings (those deadlines are absolute)

Montana extension note: Montana does not require a separate state extension form if a federal extension has been filed. Your federal Form 4868 or 7004 automatically extends your Montana return deadline. However, any Montana tax owed must still be paid by April 15 to avoid interest.

Phase 3 — Plan: April–June (The Phase Most Owners Skip)

Most Billings business owners mentally close the books on taxes the moment they file. That is the instinct Phase 3 is designed to override. The weeks after filing are the highest-leverage window for planning next year's tax outcome — because the prior year is still fresh and the current year has not yet developed bad habits.

Post-filing debrief with your accountant

Schedule a 30–60 minute meeting specifically to review what happened: which deductions were large, which were missed, what unexpected income categories appeared, what you would do differently. This meeting is the most valuable hour of your tax year — the return is fresh, the decisions that changed it are visible, and there's still time to course-correct for the current year.

Q2 estimated payment (due June 15)

The Q2 estimated payment covers April, May, and June income. If your business has strong spring revenue — which construction, landscaping, and outdoor recreation businesses in Yellowstone County often do — your Q2 payment may need to be significantly larger than Q1. Calculate from actual year-to-date numbers, not a simple division of last year's liability.

Late S-Corp election relief

If you missed the March 15 deadline for an S-Corp election, you may still qualify for late election relief under IRS Revenue Procedure 2013-30. The IRS generally grants relief if the business operated as if it were an S-Corp and the failure to timely file was due to reasonable cause. Applications submitted in April–June — while the reason for the missed deadline is still clear — are easier to document than applications filed years later.

Mid-year payroll and withholding review

For S-Corp owner-employees, review whether your year-to-date salary is on track to be reasonable and consistent through year-end. For businesses with employees, confirm that withholding projections will result in accurate W-2s — catching underwithholding in June is far less disruptive than correcting it in December.

Phase 4 — Prep: July–September

Phase 4 is setup work — building the foundation for a strong Phase 1. Billings businesses that spend July through September on their books and tax position arrive at October's critical window with options. Businesses that wait until November or December find that many options have already closed.

Q3 estimated payment (September 15)

The September 15 estimated payment covers July, August, and September income. For Billings businesses with strong summer revenue — hospitality, construction, outdoor services — this is often the largest quarterly payment. Missing or underpaying it triggers the annualized underpayment penalty even if you catch up in Q4.

Year-end projection meeting

Schedule a Q3 meeting with your accountant in August or September to project full-year taxable income. Armed with year-to-date actuals and projected Q4, you can calculate the retirement contribution target, the Section 179 opportunity, and whether any other year-end moves are warranted. This meeting turns Phase 4 into a planned Phase 1.

Depreciation scheduling

If you're considering equipment purchases in Q4, identify them now. Lead times on major equipment — medical devices, construction machinery, energy equipment — can be 60–90 days. An order placed in September can be delivered and placed in service by December 31. An order placed in December often cannot.

1099 contractor list review

The 1099-NEC deadline of January 31 can be missed when W-9s are not collected at the start of the contractor relationship. By September, you know which contractors you've paid $2,000+ year-to-date (threshold raised from $600 under OBBBA for 2026 payments). Request outstanding W-9s now — vendors reluctant to provide them mid-year are unlikely to respond to a rushed January request.

Bookkeeping checkpoint: By September 30, your books should be current through at least July. A business that hands a CPA nine months of unreconciled bank statements in October pays for it in reconstruction fees, rushed year-end decisions, and missed deductions. If your books are behind, engage your bookkeeper now — not in November. See our guide to professional bookkeeping in Billings for what to look for in a bookkeeping partner.

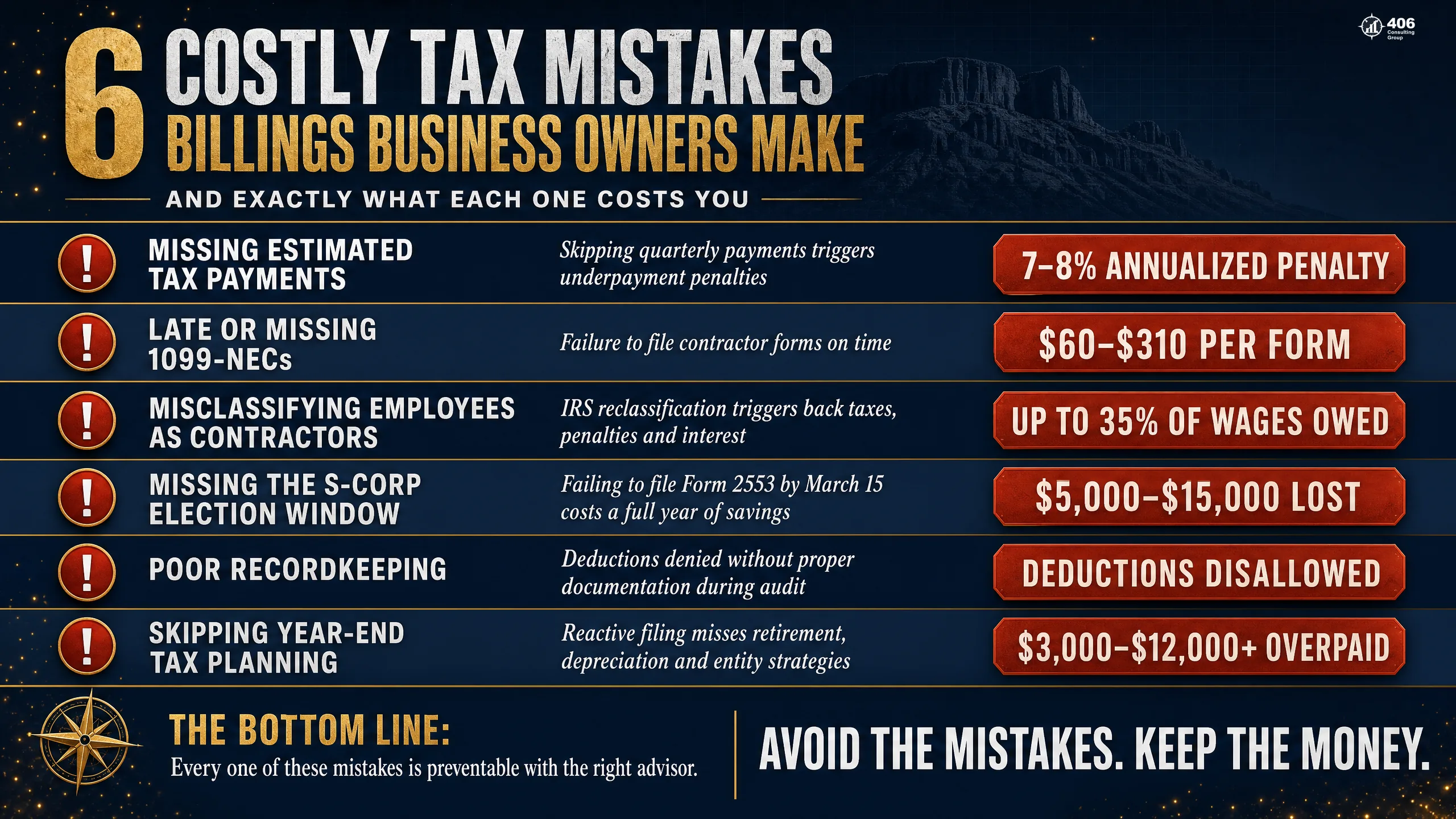

Common Tax Season Mistakes Billings Business Owners Make

These are not unusual mistakes — they are the ones that appear in the majority of Billings business tax engagements. Each is avoidable with advance planning.

Skipping or underpaying quarterly estimated payments

IRS underpayment penalty: current quarterly rate (verify at irs.gov/payments/penalties)Montana requires quarterly estimated payments if you expect to owe $500+ at filing. The IRS requires them if you expect to owe $1,000+. Missing a quarter — or basing the payment on last year's income when this year has been significantly better — creates an underpayment penalty that runs from the due date of the missed payment, not from April 15.

Missing 1099-NEC deadlines

$60–$330 per form ($660 per form if intentional disregard)The January 31 deadline for 1099-NEC is not moveable by extension. Penalties accrue per form. Billings businesses in construction, professional services, and healthcare frequently pay dozens of contractors annually. A 20-contractor list with late 1099s can generate $1,200+ in avoidable penalties.

S-Corp owner salary set too low

IRS back payroll taxes + interest + penalties if reclassifiedAn S-Corp owner who pays himself a $30,000 salary while the business generates $250,000 in net profit will draw IRS scrutiny. The IRS actively audits S-Corps for unreasonably low compensation and can reclassify distributions as wages — imposing employment tax on the reclassified amount plus interest and penalties from the original payment date.

Delivering disorganized books to the CPA in March

$1,500–$5,000+ in reconstruction fees plus missed deductionsAccountants who receive unreconciled bank statements and misclassified transactions in March either charge significantly more to reconstruct the records or file based on incomplete information. The businesses that pay less for tax preparation are the ones whose books arrive clean — already reconciled and categorized.

Not reviewing entity structure annually

$5,000–$20,000/year in excess SE tax for businesses past the thresholdA Billings business that grows from $60,000 to $120,000 in net profit may still be filing as a default LLC sole proprietorship — paying SE tax on the full $120,000. The S-Corp election analysis takes one meeting. At $120,000 in net profit, net annual savings are typically $5,000–$10,000. Three years without reviewing means $15,000–$30,000 in avoidable tax.

Missing the Section 179 election window

Loss of immediate deduction; multi-year depreciation insteadSection 179 allows immediate expensing of qualifying property — but the election must be made on a timely filed (or extended) return. Equipment placed in service in December that the owner forgot to discuss with the accountant before year-end often results in a missed election that adds complexity and cost to amend.

Billings Industry Tax Considerations

Billings' diverse economy means that tax strategy looks different depending on which sector your business operates in. Here is how Montana's four dominant Billings industries interact with the federal and state tax code. Billings contractors should also review our dedicated guide on WIP and job costing for Billings contractors for the full construction accounting picture.

Construction & Trades

Job costing and deductions

Materials, subcontractors, equipment, and direct labor on each job are deductible — but only if job costing captures them. A Billings general contractor who cannot allocate costs to jobs cannot maximize deductions or demonstrate legitimate business expenses if audited.

Section 179 and bonus depreciation

Heavy equipment purchases — excavators, cranes, trucks — are among the largest deductions available to Billings contractors. Proper depreciation scheduling determines whether those deductions land in the right year.

Subcontractor 1099-NEC compliance

Most Billings construction businesses pay dozens of subcontractors annually. Every one paid $600+ requires a 1099-NEC by January 31. Missing this deadline creates per-form penalties and potential loss of the deduction.

Prevailing wage on public contracts

Montana state and federal public contracts require certified payroll at prevailing wage rates. The payroll complexity — different rates for different job classifications, certified payroll reporting — requires a system that can track it accurately.

Healthcare & Medical Practices

Practice entity structure

A Billings physician or dentist at $250,000+ in net income is paying $29,000+ in self-employment tax if still operating as a default LLC. The S-Corp election — with a defensible salary for a physician — can reduce that by $10,000–$15,000 annually.

Retirement plan optimization

High-income medical professionals have access to retirement plan options unavailable to most businesses: defined benefit plans, solo 401(k)s with high contribution limits, and cash balance plans. A Billings physician at $500,000 net profit can legally shelter substantial income through aggressive but compliant retirement planning.

Medical equipment depreciation

Imaging equipment, exam chairs, specialized technology, and practice management software qualify for Section 179 and bonus depreciation. Coordinating purchase timing with the depreciation calendar can significantly reduce tax liability in equipment-heavy years.

Multi-location and HIPAA compliance

Patient financial records must be retained per HIPAA requirements — which exceed the standard IRS 3-year audit window. Medical practice bookkeeping must maintain records in a format satisfying both tax compliance and healthcare regulatory requirements.

Energy & Oil Field Services

Royalty income and depletion allowance

Billings businesses receiving oil and gas royalties are entitled to a depletion allowance — typically 15% of gross royalty income under the percentage depletion method. This is one of the most underutilized deductions in the energy sector, reported on Schedule E and reducing taxable royalty income directly.

Intangible drilling costs

For businesses with a working interest in an oil or gas well, intangible drilling costs — labor, fuel, chemicals used to drill — may be immediately deductible rather than capitalized. This is a significant first-year deduction that requires careful characterization.

Multi-state filing

Bakken revenue from North Dakota, Wyoming mineral interests, or Montana-Wyoming border operations create multi-state filing obligations. Montana taxes all income of Montana residents plus Montana-source income of non-residents. Apportionment calculations must be accurate.

Equipment and vehicle deductions

Oil field service companies operate large fleets of specialized vehicles and equipment. MACRS depreciation, Section 179 elections, and fuel tax credits are all available — but require organized records tying vehicle use to business purpose.

Agriculture & Ranching

Farm income averaging (Schedule J)

Agricultural income is often volatile. Farm income averaging allows you to spread a high-income year's tax across the prior three years, potentially reducing the marginal rate on the spike year's income — a significant advantage for Yellowstone County and Eastern Montana ranchers.

Section 179 on farm machinery

Combines, tractors, irrigation equipment, and grain storage systems qualify for Section 179 immediate expensing. Coordinating equipment purchases with the depreciation calendar is a core tax strategy for Montana agricultural operations.

Cash accounting method

Most farming operations qualify to use the cash accounting method — reporting income when received and expenses when paid. Delaying grain sales to January or accelerating seed and chemical purchases in December can shift substantial income between tax years when coordinated with your accountant.

Crop insurance proceeds timing

Crop insurance payments received in the year of the insured loss are generally taxable in that year. However, farmers who receive payment in the year following the loss may elect to defer recognition. Timing matters — and the election has a deadline.

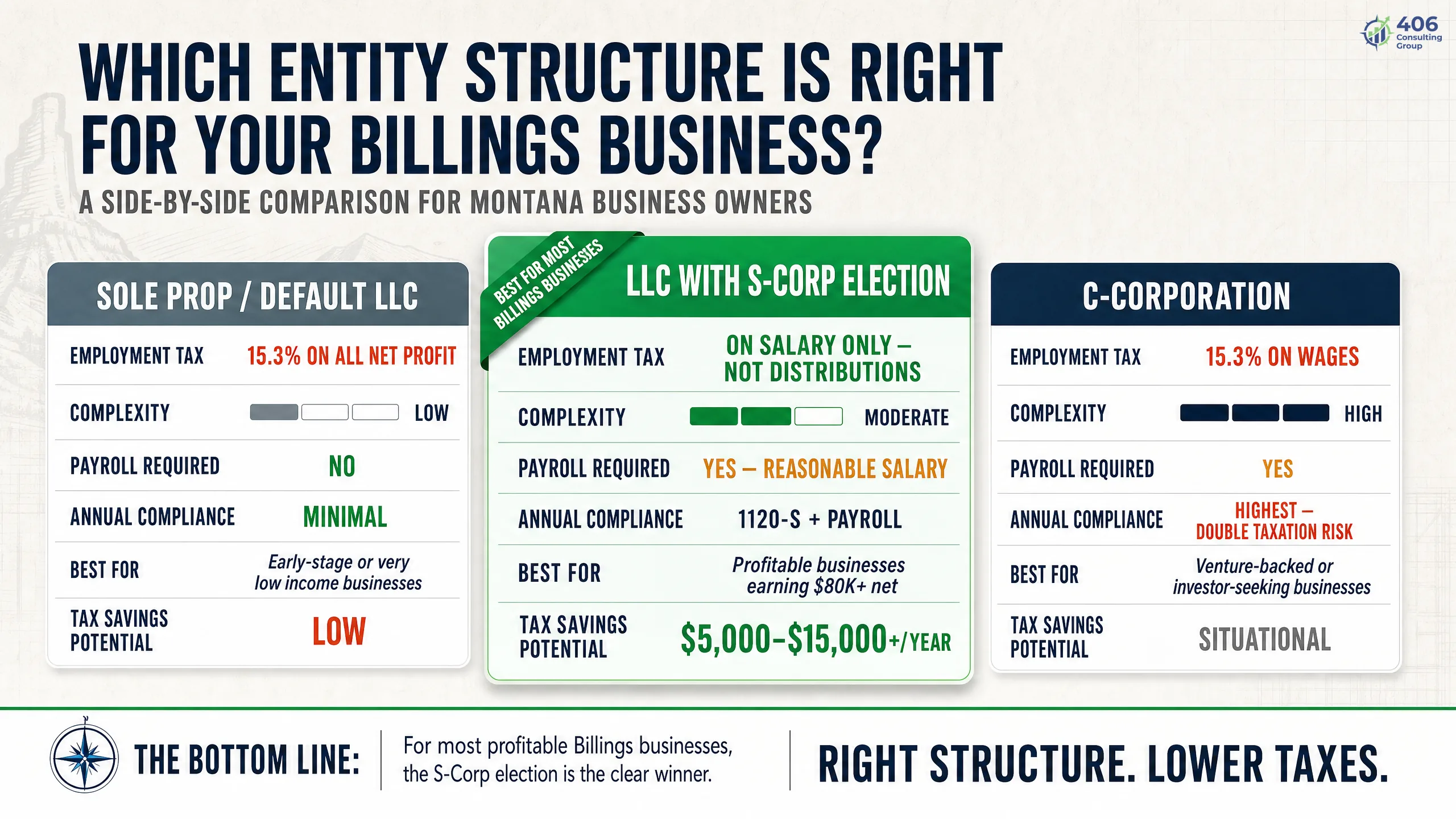

Entity Structure: Is Your Billings Business Taxed the Right Way?

Entity structure is the single largest lever most Billings business owners have not pulled. The difference between a default LLC and an S-Corp election at the same income level can be $8,000–$20,000 per year. The analysis is straightforward — but it requires doing it.

| Structure | Employment Tax | Complexity | Best For |

|---|---|---|---|

| Sole Prop / Default LLC | 15.3% SE tax on all net profit (up to SS wage base) | Low — one return, no payroll required | Starting out; net profit under $60,000 |

| LLC with S-Corp Election | 15.3% only on salary; distributions not subject to SE tax | Moderate — payroll, S-Corp return, Montana Form PTE | Service businesses, contractors, practices at $80K–$500K+ net profit |

| C-Corporation | 21% flat corporate rate; dividends taxed again at individual level | High — corporate return, double taxation risk | Outside investment; specific retention strategies — rarely optimal for most Billings small businesses |

The S-Corp break-even for Billings businesses: For most Billings businesses, the S-Corp election pays for itself when net annual profit consistently exceeds $80,000–$100,000. Below that threshold, the compliance costs typically exceed the SE tax savings. Above it, net annual savings are typically $5,000–$15,000+. Run your numbers with our S-Corp Savings Calculator or see the full analysis in our Montana S-Corp tax benefits guide.

Annual review trigger: If your net profit increased by 25%+ from the prior year, or you crossed the $80,000 threshold for the first time, your next accountant meeting should include an entity structure review. This is an annual question, not a one-time decision.

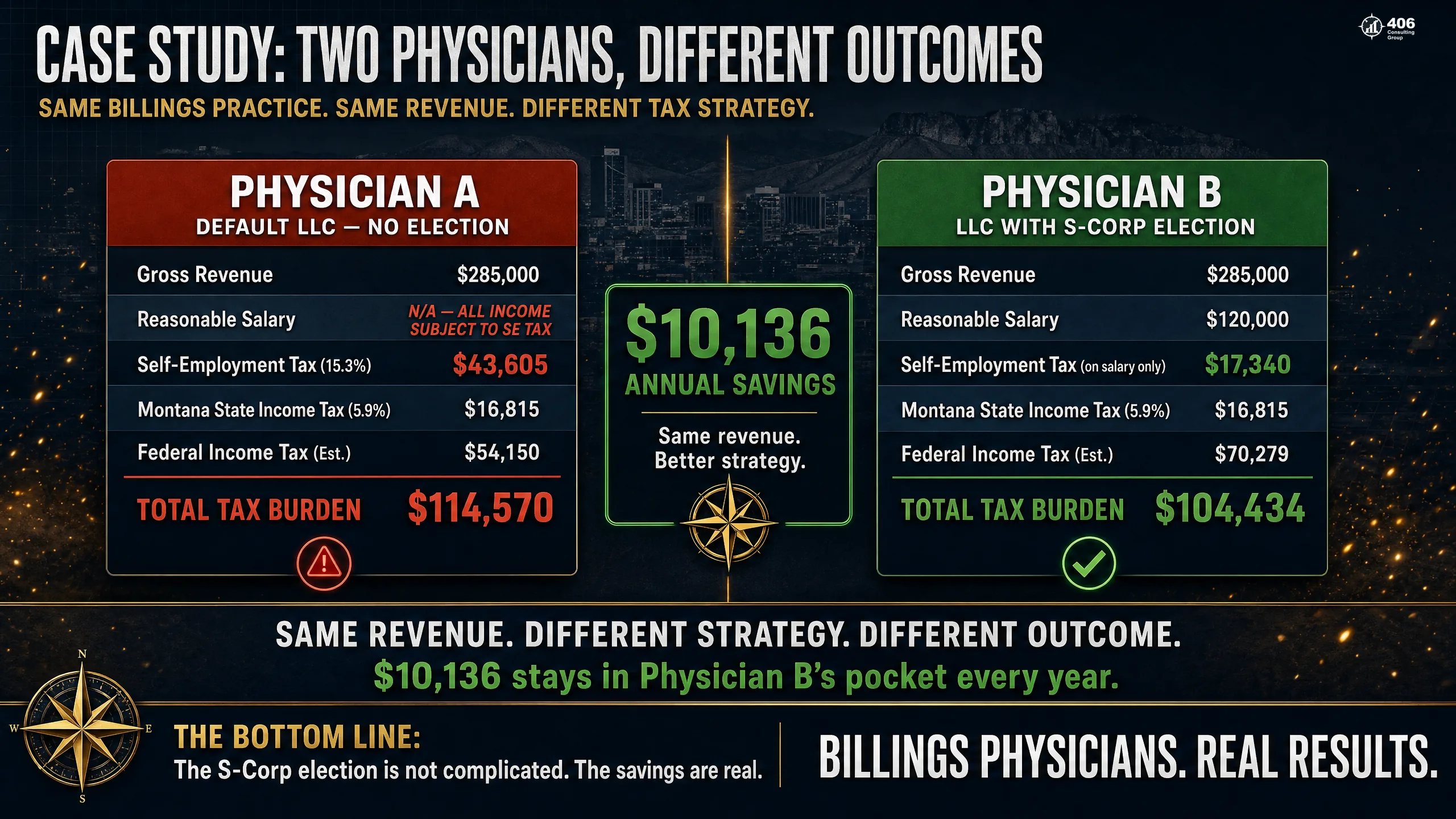

Case Study: Billings Medical Practice — Two Tax Season Outcomes

Anonymized — Billings, MT

Two Primary Care Physicians — Same Revenue, Different Outcomes

Annual net profit (both)

$280,000

Specialty

Primary care, solo practice

Years in practice

6 years

Physician A — Default LLC, Reactive Approach

Physician B — S-Corp Elected, Proactive Planning

$29,956

Physician A SE tax on full profit

$21,420

Physician B FICA on salary only

$10,136

Annual savings from S-Corp election alone

Total annual difference: $48,156 − $38,020 = $10,136 saved

Over five years, Physician B's proactive approach accumulates $50,680 in tax savings. The compliance cost differential ($2,800 reconstruction fee vs. $3,500 for Physician B's full S-Corp package) is only $700 — the proactive approach costs slightly more at the accountant level but saves over $10,000 net annually.

Frequently Asked Questions: Tax Season for Billings, MT Businesses

What taxes does a Billings, MT small business need to file?

Most Billings small businesses file: a federal income tax return (Form 1040 Schedule C for sole props, Form 1120-S for S-Corps, or Form 1065 for partnerships); a Montana income tax return (Form 2 for individuals, Form PTE for S-Corps); quarterly federal and Montana estimated tax payments if they expect to owe $1,000+ federal or $500+ Montana; payroll tax deposits if they have employees; quarterly unemployment insurance contributions to the Montana Department of Labor; and an annual Montana Secretary of State report. The exact forms depend on entity structure, employee count, and business activity.

What is the Montana income tax rate for Billings businesses?

Montana taxes pass-through business income at the individual level, with rates of 4.7% and 5.9% based on income level (verify current rates at MTrevenue.gov). C-Corporations file a separate Montana corporate income tax return at the applicable corporate rate. Montana has no general sales tax — a meaningful advantage for Billings businesses compared to neighboring states.

How do I calculate quarterly estimated tax payments for my Billings business?

You can pay 100% of last year's tax liability in four equal installments (110% if last year's AGI exceeded $150,000) — this avoids underpayment penalties regardless of current-year income. Alternatively, calculate actual current-year liability from year-to-date books and project through year-end. Montana requires quarterly estimated payments if you expect to owe $500+ at filing. Due dates: January 15, April 15, June 15, September 15.

What are the key tax filing deadlines for Montana businesses in Billings?

Key deadlines: January 15 (Q4 estimated payment); January 31 (W-2s and 1099-NECs to recipients); March 15 (S-Corp 1120-S, partnership 1065, Montana Form PTE, and the S-Corp election Form 2553 deadline for the current year); April 15 (individual 1040, C-Corp 1120, Montana Form 2, Q1 estimated payment). Montana automatically accepts the federal extension — no separate state form required — but tax owed must still be paid by April 15.

Does Billings have a local city income tax or business tax?

No. Billings and Yellowstone County do not impose a local city income tax. Montana businesses in Billings pay federal and state tax only — no additional municipal income tax layer. Montana cities may impose business license fees or specific occupational taxes for certain industries, but these are not income taxes.

When should a Billings business review its entity structure for tax purposes?

Entity structure should be reviewed annually after your tax return is filed, when you have a full picture of the prior year's net profit. The two most important triggers: net profit has crossed $80,000–$100,000 for the first time (making an S-Corp election potentially worthwhile), or net profit has changed by 25%+ in either direction. The S-Corp election deadline is March 15 — the decision should be made in Q4 or early January, not in March under deadline pressure.

Does 406 Consulting Group serve Billings, MT businesses for tax planning?

Yes. 406 Consulting Group provides tax planning, S-Corp election analysis, bookkeeping, and fractional CFO services for businesses in Billings, across Montana, and throughout the Intermountain West. Jason Anderson's background in operational finance and Carrie Anderson's experience in commercial banking and tax strategy are both relevant for Billings businesses navigating tax season decisions — from first estimated payment to year-end structure review. Contact us to discuss what a tax planning engagement looks like for your business.

External Resources

Billings, MT

Ready to Navigate Tax Season the Right Way?

406 Consulting Group provides tax planning, S-Corp election analysis, bookkeeping, and fractional CFO services for Billings and Montana businesses. We manage the full Billings Business Tax Cycle — not just April 15.

The Billings Business Tax Cycle

Four phases, year-round

Close

Oct–Dec: The decisions that move the number

File

Jan–Apr 15: Filing season execution

Plan

Apr–Jun: Post-filing strategy

Prep

Jul–Sep: Build the foundation

Montana Tax Deadline Quick Reference

Q4 estimated payment

W-2s and 1099-NECs to recipients

S-Corp / partnership returns + Form PTE

S-Corp election (Form 2553) deadline

Individual return + C-Corp + Q1 payment

Q2 estimated payment

Q3 estimated payment + extended returns

Extended individual return deadline

Related Reading

About the Author

Jason Anderson

Principal, 406 Consulting Group

Background in operational finance and business strategy. Works with Montana and Intermountain West businesses on tax planning, entity structure, and the systems that make year-round tax management possible.

Manage tax season year-round — not just in April.

We run the full Billings Business Tax Cycle for Montana businesses across all four phases.

Schedule a Consultation