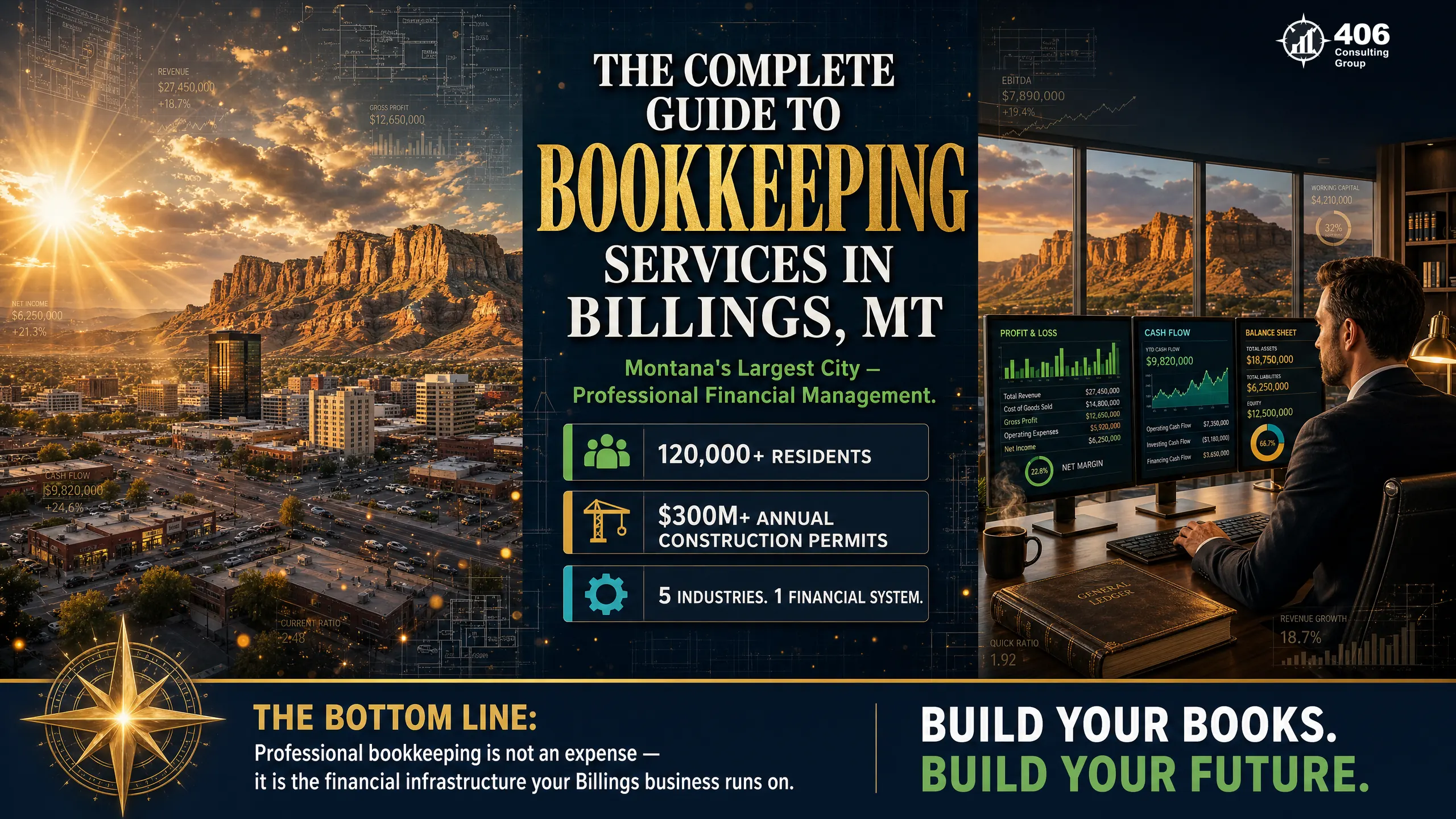

The Complete Guide to Bookkeeping Services

in Billings, MT

Billings businesses lose thousands annually to bad bookkeeping. The complete guide to professional bookkeeping in Montana's largest city — clean books, tax savings, and growth-ready financials.

Professional bookkeeping services in Billings, MT are the financial foundation every business in Montana's largest city needs to grow, borrow, and make confident decisions. Billings is a different market than the rest of Montana — larger, more economically diverse, more competitive — and its bookkeeping demands reflect that complexity.

This guide covers what professional bookkeeping actually delivers, what bad bookkeeping costs Billings businesses in real dollar terms, and how to evaluate whether your current financial system is serving your business or quietly working against it. Whether you're running a healthcare practice, an energy services company, a retail operation, or a construction firm, the system is the same: clean books produce better taxes, better loans, and better decisions.

Table of Contents

The Billings Business Landscape: Why Bookkeeping Is More Complex Here

Bookkeeping services in Billings, MT serve Montana's most economically diverse city. With 120,000+ residents, a healthcare sector anchored by Billings Clinic and St. Vincent Healthcare, a construction market producing $300M+ in annual permits, energy and oil field services tied to the Bakken, significant agribusiness, and a growing professional services sector — Billings businesses operate in a financial environment that generic bookkeeping advice consistently misses.

120K+

Billings city population

Montana's largest city and primary commercial hub

$300M+

Annual construction permits

One of Montana's highest-volume construction markets

6

Distinct business sectors

Each with different bookkeeping complexity and compliance requirements

What makes bookkeeping in Billings specifically demanding:

Economic diversity

A city with active healthcare, energy, agriculture, construction, and retail sectors cannot be served by one-size-fits-all bookkeeping. Each sector has different revenue recognition requirements, different cost structures, different compliance obligations, and different lender expectations.

Banking sophistication

First Interstate Bank (headquartered in Billings), Stockman Bank, and Glacier Bank all operate commercial lending departments that evaluate contractor, healthcare, and business loans with detailed financial underwriting. Billings businesses that want capital need financials that meet lender standards — not just tax preparer standards.

Scale and competition

Billings businesses operate in a more competitive environment than smaller Montana cities. A Billings retailer or service provider competing for the same customer base as regional and national competitors cannot afford the margin leakage that bad bookkeeping produces.

Multi-sector complexity

Many Billings business owners have income from multiple sources — a medical practice plus rental properties, a construction business plus an equipment rental operation, an ag operation plus commodity trading. Multi-source income requires a chart of accounts that captures each source correctly.

What Professional Bookkeeping Delivers That DIY and Amateur Setups Don't

Professional bookkeeping is defined by its output — five specific deliverables produced monthly, without exception. If your current bookkeeper, software, or DIY setup cannot produce all five, you have a gap that is costing you money.

Reconciled accounts

Every bank account, credit card, and line of credit matched to bank statements with zero unexplained variances. Completed by the 10th of each month for the prior month. This is the only error-detection mechanism in bookkeeping — without it, errors compound monthly and become expensive to unwind.

Accurate categorization

Every transaction assigned to the correct account in a chart of accounts built for your specific business — not a generic QuickBooks template. Categorization reviewed against your tax return structure so deductions are captured correctly all year, not reconstructed in March.

Monthly financial reports

Profit & Loss, balance sheet, and cash flow statement delivered within 10 days of month-end. Reviewed for anomalies — not just generated. Trends noted. Unusual items flagged. These reports are your business dashboard; they only work if they're produced consistently and reviewed.

Accounts receivable aging

A report showing every outstanding invoice by age — 0–30, 31–60, 61–90, 90+ days. Updated monthly. For Billings businesses with significant receivables (healthcare practices, contractors, professional services), AR aging is a cash flow management tool, not optional reporting.

Tax-ready year-end close

Books formally closed monthly so year-end requires a final review and adjusting entries — not a reconstruction project. Your tax preparer receives clean, reconciled financials in February, not in late March after a scramble. The savings in tax preparer time typically exceed the monthly bookkeeping cost.

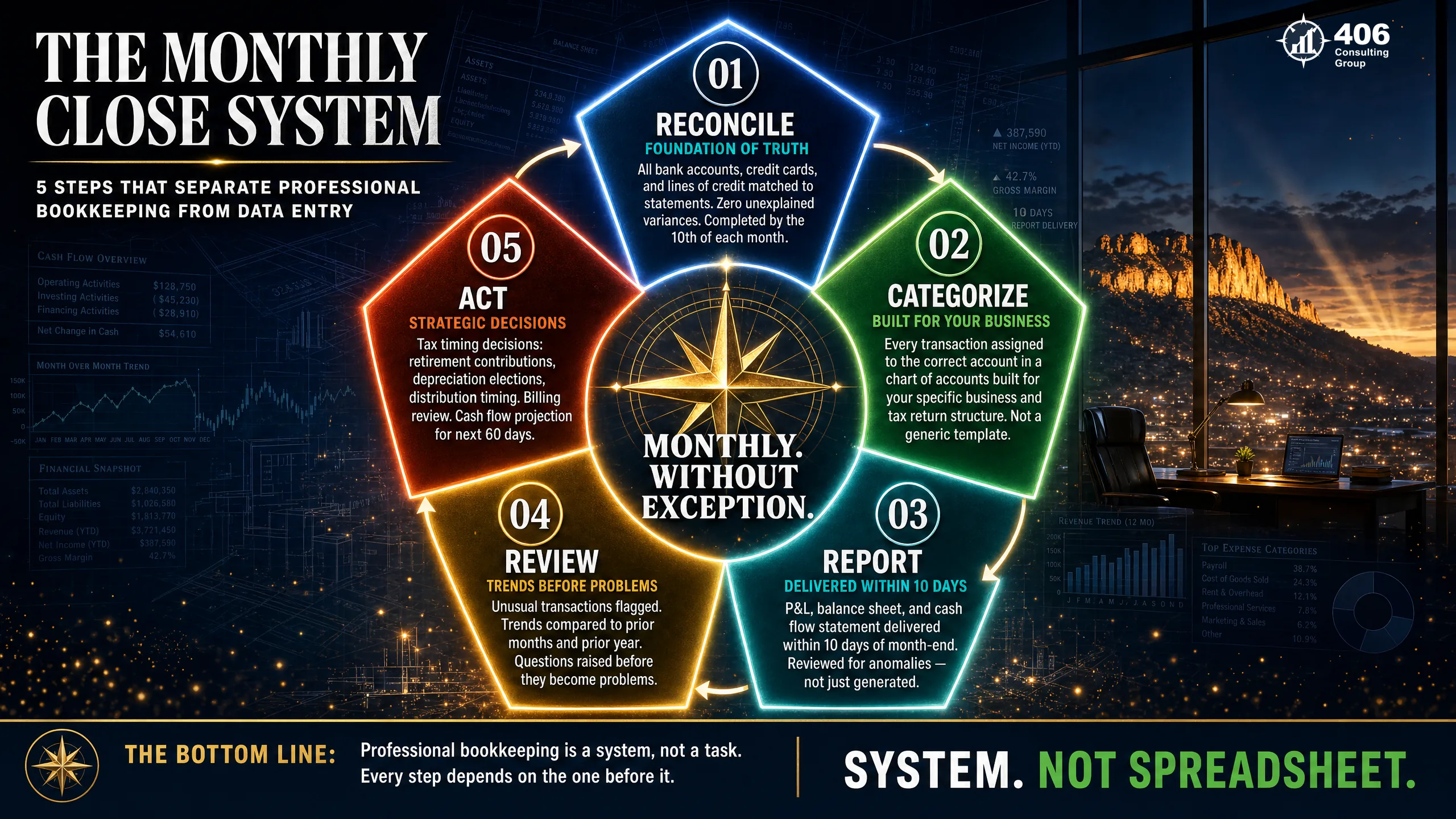

The Monthly Close System: 5 Steps to Financial Clarity

The Monthly Close System is the framework that separates professional bookkeeping from data entry. Most small business bookkeeping stops at Step 2 — transactions are entered and categorized, but the data is never transformed into actionable financial intelligence. The full five-step cycle is what makes bookkeeping worth its cost.

Reconcile

By the 10th of each monthEvery bank account, credit card, line of credit, and loan account matched to the corresponding financial institution statement. Every transaction in the books has a matching transaction on the statement. Every transaction on the statement has a matching entry in the books. Zero unexplained variances.

Why it matters: Reconciliation is the only mechanism that catches errors — duplicate payments, missing transactions, bank errors, and unauthorized charges. A business that doesn't reconcile monthly is operating on financial data it cannot trust.

Categorize

Concurrent with reconciliationEvery transaction assigned to the correct account in a chart of accounts designed specifically for your business type. The chart of accounts is built to align with your tax return schedules — so income flows to the right lines, expenses flow to the right deduction categories, and nothing is lost in translation at year-end.

Why it matters: A generic QuickBooks chart of accounts misses the nuance of your specific business. A medical practice, an oil field services company, and a retail shop all need different account structures. Correct categorization is the foundation of every financial report produced downstream.

Report

Within 10 days of month-endProfit & Loss statement, balance sheet, and cash flow statement produced and delivered. Not generated and emailed — reviewed. Anomalies identified. Current month compared to prior month and prior year. Revenue trend noted. Expense variances explained.

Why it matters: A financial report that is generated but not reviewed is noise. The value of the report is in the reading — which requires someone with enough financial knowledge to know what normal looks like and recognize when something isn't.

Review

Simultaneous with report deliveryUnusual transactions flagged and questioned. A $14,000 payment to a vendor you've never seen before — is it legitimate? A revenue line that's 40% below prior month — is that seasonal or a problem? An expense category running 25% over budget — is it a classification error or a real cost overrun?

Why it matters: This is where professional bookkeeping earns its fee. A data-entry bookkeeper records what they see. A professional bookkeeper asks questions about what they see. The review step is where problems are caught early — before they become expensive.

Act

Following review — monthlyTax timing decisions: Is it time to make a retirement contribution? Does a depreciation election need to be made before year-end? Should the owner take a distribution now or defer? Billing review: Which invoices are aging past 60 days? Cash flow planning: What does the next 60 days look like based on current backlog and receivables?

Why it matters: Bookkeeping without action is recordkeeping. The Monthly Close System is designed to produce decisions, not just reports. Step 5 is the payoff — where the financial data turns into real-world business improvements.

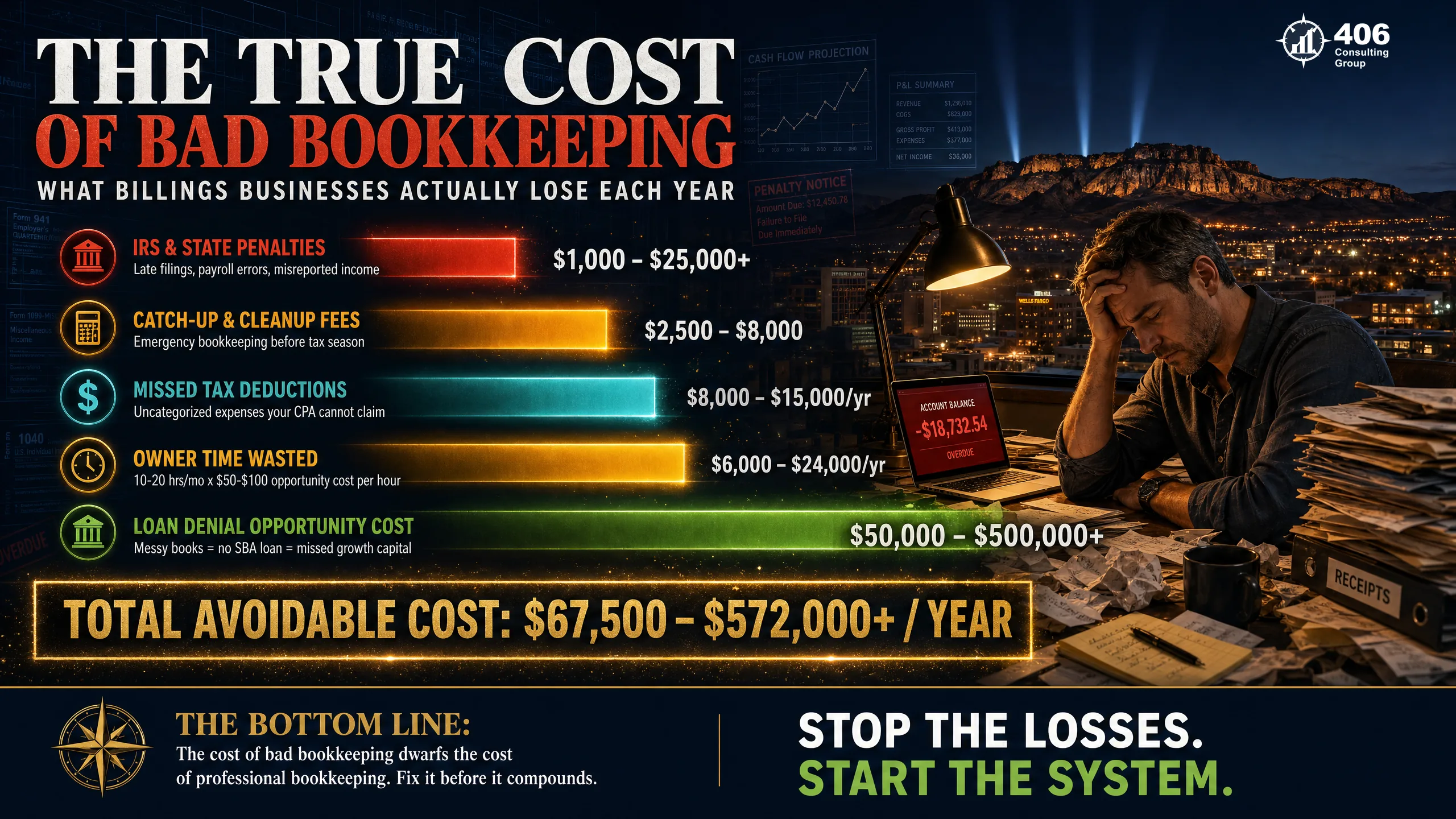

The True Cost of Bad Bookkeeping in Billings

The cost of bad bookkeeping is almost always invisible — until it isn't. Here's what Billings businesses lose across five categories when their books aren't maintained professionally. The total is rarely less than the cost of professional bookkeeping. It's usually three to five times more.

Missed Deductions

$8,000–$25,000/year- Vehicle mileage: at $0.67/mile, a Billings sales rep driving 20,000 business miles and not logging it misses $13,400 in deductions annually

- Home office: most Billings remote workers qualify for $1,500–$2,500/year — almost none claim it without monthly tracking

- Section 179 elections: a $60,000 equipment purchase expensed immediately vs. depreciated over 7 years — only visible at time of purchase with current books

- Retirement contributions: the optimal SEP-IRA or Solo 401(k) contribution requires accurate YTD net income — impossible to calculate from messy books

Compliance Penalties

$500–$50,000+- IRS CP2000 notices: 1099 income on bank statements that didn't make it into the books — with interest from the original due date

- Montana DOR underpayment: quarterly estimated taxes calculated from incorrect book income = penalties each quarter

- 1099-NEC failures: $60–$630 per missing or late form for contractors paid $600+ — multiplied by every subcontractor not tracked

- Montana UI late filing: DOR audits compare quarterly wage reports to payroll records — discrepancies trigger penalty assessments

Decision Blindness

$10,000–$100,000+- Pricing decisions made without knowing actual cost per service — a Billings HVAC company with no job-level margin data prices by instinct and loses money on its most common service call type

- Hiring at the wrong time — adding a $55,000/year employee without a 12-month cash flow projection that shows whether the business can sustain it

- Seasonal cash flow crises that were visible in the books six months before they hit — but invisible to an owner without monthly reports

- Losing bids to better-prepared competitors who can quickly produce a profit-and-loss by service line

Financing Barriers

$50,000–$500,000+- Commercial loan denied at First Interstate or Stockman Bank because financial statements are inconsistent with tax returns — a common outcome when books are reconstructed at year-end rather than maintained monthly

- SBA loan delayed by months while books are reconstructed — during which the opportunity has passed

- Equipment financing at worse rates because debt service coverage ratio (DSCR) can't be clearly demonstrated from the books

- Business sale valuation suppressed — buyers discount or walk away when financials are unreliable; clean books are worth 10–20% more at exit

Owner Time Drain

$12,000–$30,000/year- 10–15 hours per month doing bookkeeping at $100–$200/hour opportunity cost = $1,000–$3,000 per month in diverted productive time

- 20–40 hours in March reconstructing the prior year for tax prep — during the period many Billings businesses are entering their busiest spring season

- Mental load of financial uncertainty: operating without knowing cash position, actual profitability, or tax liability creates decision paralysis and stress

- Errors from doing books while tired or distracted — errors that cost more to fix than the time saved by doing it yourself

Industry-Specific Bookkeeping: Billings' Key Sectors

Billings' economic mix means that industry-specific bookkeeping knowledge matters more here than in a single-industry Montana town. Here's what each major sector requires that standard bookkeeping setups consistently miss.

Healthcare & Medical Practices

Billings sector- 1Insurance reimbursement timing: billed charges vs. collected amounts are dramatically different — accrual basis required for meaningful P&L

- 2Contractual allowances: the gap between billed and allowed must be tracked as a revenue adjustment, not an expense

- 3Multi-entity structures: Billings Clinic-affiliated practices often operate through a professional corporation plus a management services entity plus real estate — each requires its own books

- 4Provider compensation: physician partners receiving K-1 distributions plus W-2 salary creates complex payroll and equity tracking requirements

Energy & Oil Field Services

Billings sector- 1Multi-state project tracking: Bakken-adjacent contractors with projects in Montana and North Dakota have income sourced in multiple states — books must capture revenue by project location

- 2Joint interest billing: operators billing working interest owners require revenue and cost allocation by well or project

- 3Equipment-intensive cost structure: heavy equipment depreciation, fuel, and maintenance must be allocated by job for accurate margin visibility

- 4Boom/bust cash flow: energy service businesses need rolling 90-day cash flow projections based on active contracts — only possible with current books

Agribusiness

Billings sector- 1Commodity income timing: wheat, cattle, and sugar beet income arrives in lump payments that must be matched to the correct tax year

- 2FSA and USDA program payments: government payments are taxable income that must be captured as received and correctly categorized

- 3Farm equipment depreciation: Section 179 and bonus depreciation elections on combines, tractors, and irrigation systems are among the largest tax decisions ag operators make annually

- 4Schedule F vs. Schedule C: farm income and non-farm income must be tracked separately if the operator has both — a chart of accounts failure here creates a tax filing problem

Construction

Billings sector- 1Job costing: every material, labor, and subcontractor cost allocated to the specific project that incurred it — required for knowing job-level margin

- 2WIP accounting: revenue recognized by percentage complete, not by invoice date — requires a monthly WIP schedule

- 3Retainage: 5–10% withheld by GC until project completion must appear as a separate receivable on the balance sheet

- 4See our complete guide: Mastering WIP and Job Costing for Billings, MT Contractors covers the full contractor financial system

Retail

Billings sector- 1COGS tracking: beginning inventory + purchases − ending inventory = cost of goods sold. Requires periodic inventory counts and a consistent valuation method (FIFO or average cost)

- 2Merchant account reconciliation: credit card processing deposits net of fees must reconcile to both the merchant statement and the bank account — a common source of unexplained variances

- 3Seasonal buying: large inventory purchases in advance of peak season must be financed and tracked — cash flow planning requires current books

- 4Shrinkage and returns: inventory losses and customer returns must be tracked separately from COGS for accurate margin reporting

Professional Services

Billings sector- 1Retainer billing: monthly retainer income must be recognized as earned — prepaid retainers are liabilities until the service is delivered

- 21099 income complexity: consultants and professional service providers often receive income from multiple clients on 1099s — each must be captured and matched against business expenses

- 3Owner compensation optimization: S-Corp professional service businesses must balance reasonable W-2 salary against distributions — books that track this monthly enable real-time tax optimization

- 4Time-based billing reconciliation: for firms billing by the hour, monthly reconciliation of billed vs. collected vs. WIP gives visibility into revenue leakage

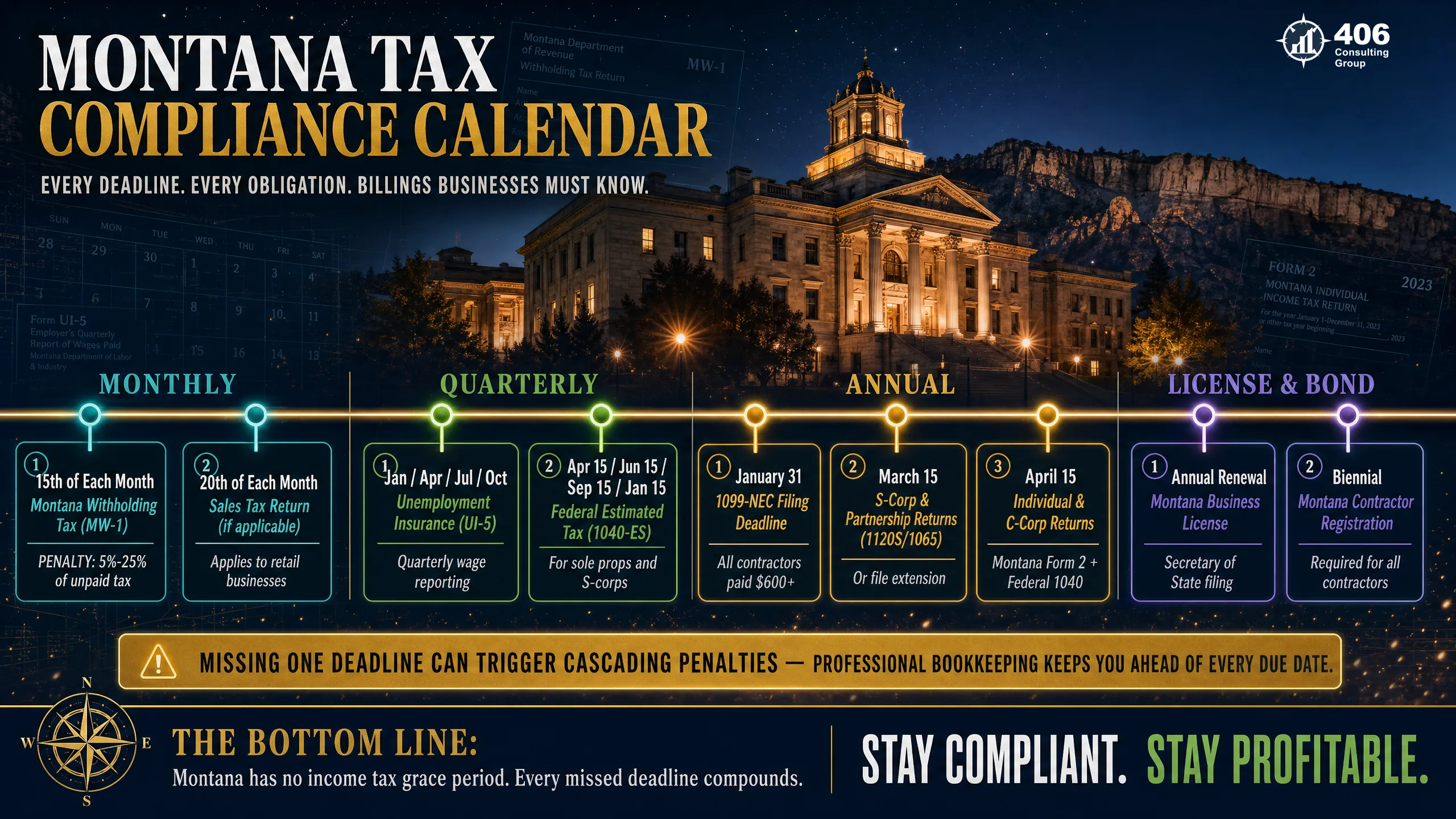

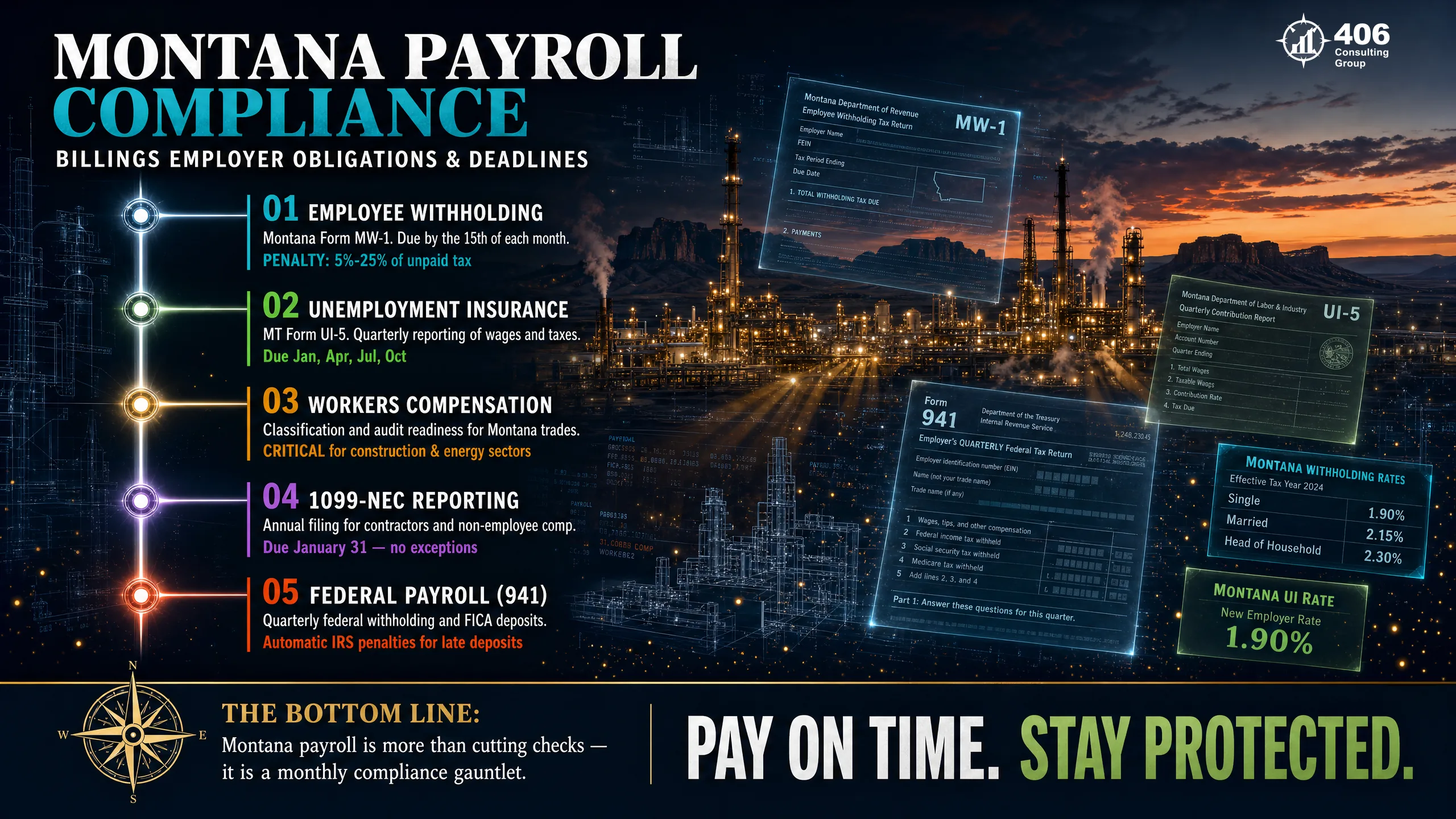

Montana Tax Obligations Every Billings Business Must Track

Montana's tax environment is meaningfully different from neighboring states and from what most national bookkeeping advice assumes. No sales tax removes one compliance layer. But state income tax, UI filings, workers compensation, and entity-level reporting create a compliance calendar that falls apart without monthly bookkeeping.

Montana Individual & Corporate Income Tax

Montana taxes business income — whether flowing through an S-Corp, partnership, or sole proprietorship — at rates up to 6.75%. Quarterly estimated payments are due April 15, June 15, September 15, and January 15. Accurate estimates require accurate current-year book income — which requires monthly books.

Montana Income Tax Withholding

Employers withhold Montana income tax from all W-2 employees at graduated rates. Remitted monthly (if withholding exceeds $500/month) or quarterly. Must reconcile to W-2s at year-end. Discrepancies trigger DOR correspondence.

Montana Unemployment Insurance (UI)

Quarterly wage reports and contribution payments due four times per year. Your books must capture gross wages by employee to produce accurate quarterly reports. Late filing triggers penalties and interest. DOR audits compare quarterly submissions to payroll records.

Montana State Fund (Workers Compensation)

Most Montana employers carry workers compensation through Montana State Fund or a private carrier. Premiums calculated on actual payroll by worker classification. Annual audit compares actual to estimated payroll — underpayment creates a retroactive bill.

1099-NEC Filing

All subcontractors, independent contractors, and non-employees paid $600+ must receive a 1099-NEC by January 31. Your books must capture EIN, legal name, and cumulative payments throughout the year — not reconstructed in January from a pile of invoices.

Montana Business Annual Report

LLCs, corporations, and registered entities must file an annual report with the Montana Secretary of State confirming registered agent and officer information. Missing it can trigger administrative dissolution — with significant implications for liability protection and banking relationships.

Bookkeeping and Tax Savings: What Clean Books Make Possible

Your tax preparer can only work with what your books provide. When books are incomplete or reconstructed at year-end, conservative positions are taken on deductions — not because the deductions aren't legitimate, but because they can't be substantiated. Monthly bookkeeping is tax strategy infrastructure.

Vehicle mileage

$0.67/mile (2024)Must be logged at time of trip — destination, business purpose, odometer. A Billings sales rep driving 25,000 business miles/year and not logging it misses $16,750 in deductions. At 24% combined tax rate: $4,020 in real cash left on the table annually.

Home office

$5/sq ft simplifiedDedicated space used regularly and exclusively for business. 320 sq ft = $1,600/year deduction. Most Billings remote workers and home-based professionals qualify. Without monthly tracking, it's rarely claimed.

Business meals

50% deductibleBusiness purpose documented at the time of the meal. A $250 client dinner documented same day = $125 deduction. Reconstructed from a credit card statement 90 days later without notes = unsubstantiated = denied by IRS.

Section 179 / Bonus depreciation

100% bonus (OBBBA permanent)$80,000 equipment purchase: $80,000 expensed in year 1 at 100% bonus depreciation — permanently restored under OBBBA (July 2025). But this is a strategy decision that must be made at purchase — not retroactively. Only visible in real time with current books.

Retirement contributions

SEP-IRA: up to 25% of net income$150,000 net income = up to $37,500 deductible contribution. The optimal amount can only be calculated from accurate YTD net income. Year-end reconstruction produces a number — monthly books produce an optimized number.

Professional development

100% deductibleIndustry conferences, trade publications, software subscriptions, CE courses. Billings professionals in healthcare, engineering, and legal regularly spend $3,000–$8,000/year on development — frequently underclaimed when lumped into miscellaneous.

What we see consistently: Billings businesses switching from year-end reconstruction to monthly professional bookkeeping recover $8,000–$22,000 in missed deductions in the first tax cycle and reduce their tax preparation fee by 30–40% (preparer time shifts from reconstruction to strategy). The bookkeeping investment is typically recovered within the first tax cycle.

Bookkeeping and Commercial Lending in Billings

First Interstate Bank (headquartered in Billings), Stockman Bank, and Glacier Bank all have commercial lending departments that regularly finance Billings businesses. When a business owner walks in with a loan application, the underwriter's first request is two to three years of financial statements. What happens next is entirely determined by the quality of the books those statements came from.

Monthly professional bookkeeping

Smooth approval process

- P&L statements clean, consistent, and reconciled to tax returns

- Balance sheet accurately reflects assets, liabilities, and equity

- Personal and business accounts completely separated

- AR aging available — demonstrates collectible receivable base

- DSCR calculated by underwriter in minutes, not weeks

- Loan closes on timeline — opportunity captured

Year-end reconstruction or DIY books

Denied, delayed, or worse terms

- Financials inconsistent with tax returns — every discrepancy flagged

- Personal expenses mixed with business — DSCR uncalculable

- Reconstruction required: $5,000–$15,000 and 2–4 months

- AR aging unavailable — receivables excluded from collateral

- Timeline missed — equipment lease, expansion, or acquisition lost

- Approved at higher rate or with additional collateral requirements

Key metrics Billings lenders calculate from your books:

DSCR

(Net Income + Depreciation + Interest) ÷ Annual Debt Service

Target: 1.25x+

Working Capital Ratio

Current Assets ÷ Current Liabilities

Target: 1.2x+

Debt-to-Equity

Total Liabilities ÷ Total Equity

Target: below 3.0x for most lenders

Payroll Compliance for Billings Employers

Payroll is where bookkeeping errors most quickly become legal liability. Montana has specific payroll obligations that create compliance risk for Billings employers who don't track them monthly in the books.

Montana income tax withholding

Withheld from all W-2 employees at graduated rates (1%–6.75%). Remitted monthly or quarterly to MT DOR. Withholding account must reconcile to W-2s at year-end. Discrepancies trigger DOR correspondence and can result in penalty assessments.

Federal payroll taxes (FICA)

Social Security (6.2% employee + 6.2% employer) and Medicare (1.45% employee + 1.45% employer) withheld from employee wages and matched by the employer. Deposited semi-weekly or monthly based on lookback period. The IRS holds officers personally liable for unpaid 941 trust fund taxes.

Montana Unemployment Insurance (UI)

Quarterly wage reports and contributions due last day of April, July, October, and January. Calculated on first $43,000 of wages per employee (2024). New employer rate: 1.0%; experience-rated employers vary. Books must capture gross wages by employee for accurate quarterly reporting.

Montana State Fund (Workers Compensation)

Premiums calculated on payroll by worker classification. Annual audits compare actual payroll to estimated payroll — underpayment creates a retroactive premium bill. Misclassified workers (e.g., a field tech coded as an office worker) create both audit exposure and premium liability.

1099 vs. W-2 classification

Montana applies the same behavioral and financial control tests as the IRS. Misclassifying an employee as a contractor avoids payroll taxes in the short term — and creates liability for all unremitted taxes plus penalties and interest retroactive to the year of misclassification. IRS enforcement is active and ongoing.

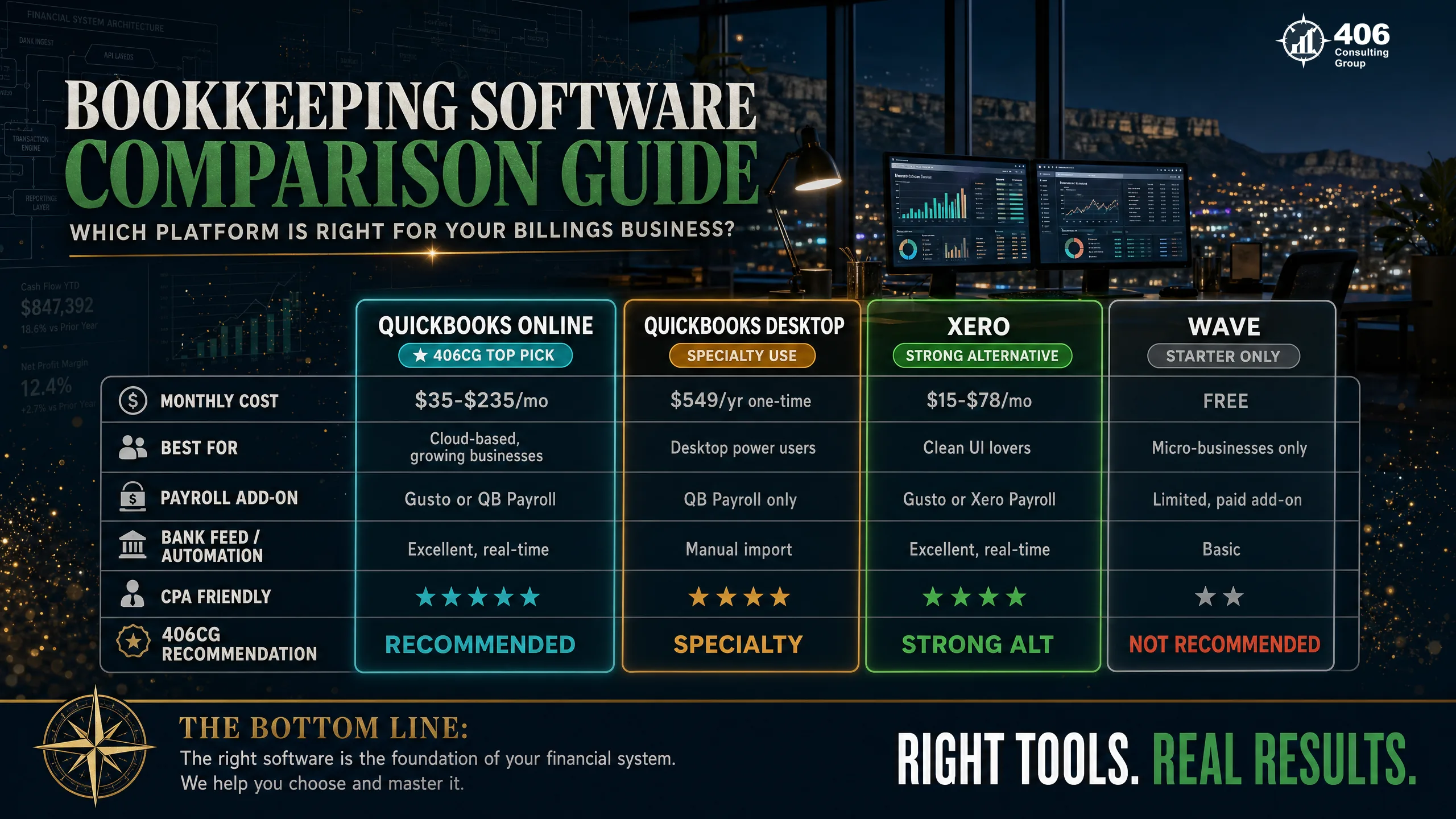

Choosing the Right Bookkeeping Software for Your Billings Business

Software is the tool — not the bookkeeper. The right platform for your Billings business depends on your industry, transaction volume, whether you have employees, and whether you need job costing. Here's how the four main options compare.

QuickBooks Online

Most common — non-contractors$30–$200/month depending on plan

Best for: Service businesses, retail, professional services, healthcare under $5M revenue

Strengths

- Cloud-based — accessible from anywhere

- Strong bank feed integration

- Payroll add-on available

- Accountant access easy to grant

- Good invoicing and AR tracking

Limitations

- Job costing limited vs. Desktop

- Inventory tracking inferior to Desktop

- Monthly cost adds up vs. Desktop annual license

QuickBooks Desktop

Best for construction/contractors$599/year (Pro), higher for Premier/Enterprise

Best for: Contractors, construction, businesses requiring job costing or complex inventory

Strengths

- Superior job costing by project

- Better inventory management

- More robust reporting

- Works offline

Limitations

- Sunset risk — Intuit pushing toward QBO

- Single-machine installation (though remote access available)

- Less intuitive for non-accountants

Xero

Service businesses$15–$78/month depending on plan

Best for: Service businesses with international clients, strong reporting needs, multiple users

Strengths

- Strong multi-currency support

- Unlimited users at most plan levels

- Clean interface, easy to learn

- Good third-party integrations

Limitations

- Less common among Montana bookkeepers — accountant familiarity limited

- Payroll requires Gusto integration (additional cost)

- Inventory management weaker than QB

Wave

Early-stage / low volumeFree (payroll add-on $20/month + $6/employee)

Best for: Sole proprietors and early-stage businesses under $250K revenue

Strengths

- Free — no monthly cost

- Simple interface for basic needs

- Invoicing and receipt scanning included

Limitations

- Limited reporting — not sufficient for lender or bonding packages

- No inventory tracking

- Payroll is a separate add-on

- Will need to migrate as the business grows

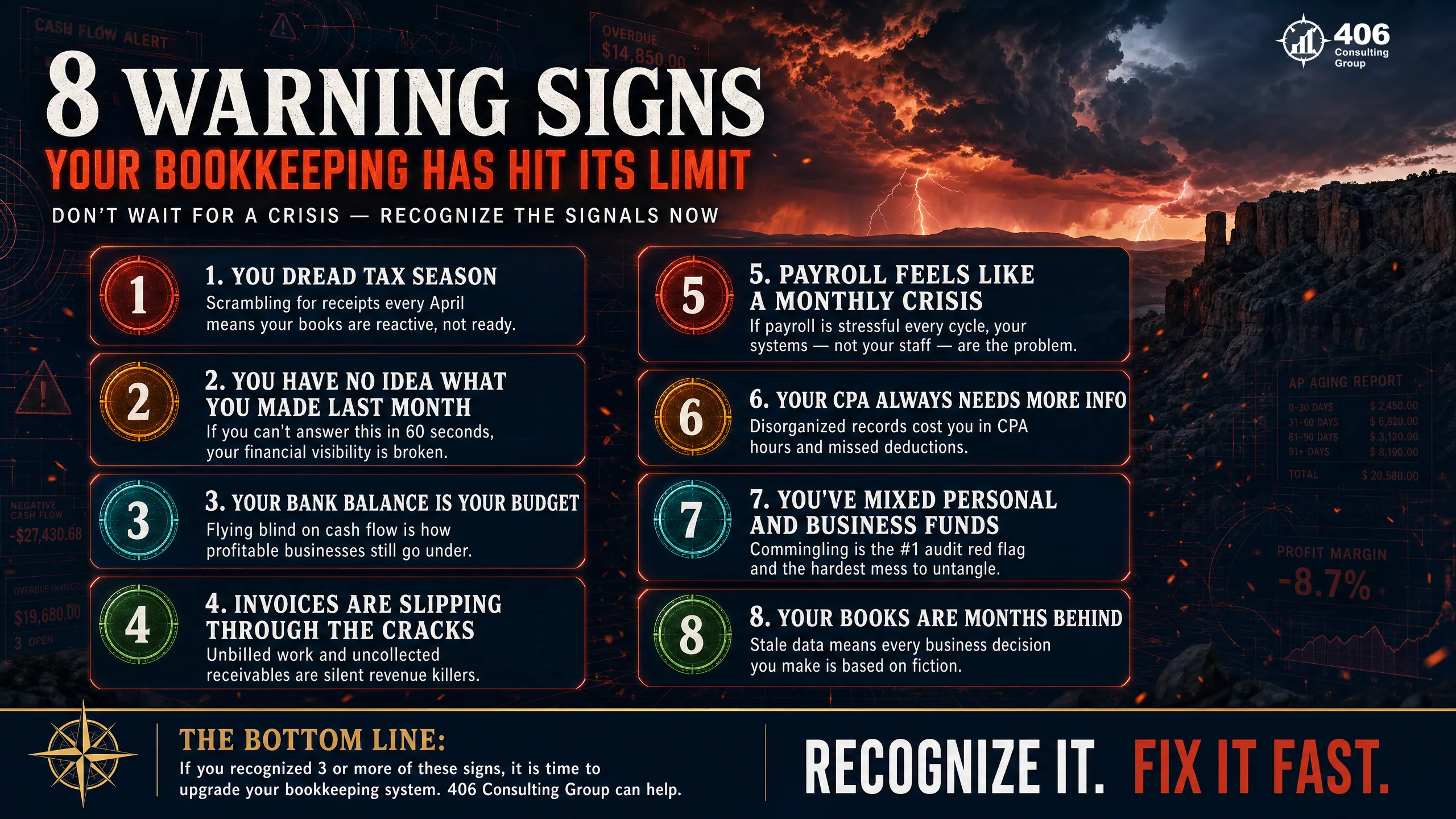

Warning Signs Your Billings Business Bookkeeping Is Failing

These eight warning signs indicate your current bookkeeping setup has hit its ceiling — regardless of who's doing it or what software you're using.

Books are 1–3 months behind

Every business decision since the last close is based on outdated financial data. You are operating blind.

Your tax preparer makes significant adjustments every year

You're paying accounting rates for bookkeeping work — and losing a full year of strategic tax opportunities while it happens.

An unexpected IRS or Montana DOR notice arrived

Unexpected notices almost always trace to bookkeeping: misclassified income, underpaid estimated taxes, missing 1099s.

A lender asked for financial statements you couldn't produce quickly

Clean books produce financial statements from software in minutes. If yours require weeks to compile, they aren't being maintained.

Your bank balance and P&L tell completely different stories

Cash and accrual divergence without explanation is a sign of misclassified transactions, unreconciled accounts, or both.

The owner is doing bookkeeping on weekends

At $100–$200/hour opportunity cost, 10 hours per month = $1,000–$2,000/month in diverted productive time — plus the errors that come from doing books while fatigued.

Your bookkeeper has never flagged an unusual transaction or raised a concern

A professional bookkeeper surfaces problems. If yours only enters data, you have a data-entry person — not a financial resource.

You can't answer 'are we profitable right now?' with confidence

Profitability should be a monthly known — not a quarterly or annual discovery. If you can't answer it, your books aren't working.

What to Expect from a Professional Bookkeeper: The Baseline Standard

These are not exceptional deliverables — they are the minimum standard a professional bookkeeping engagement should meet for any Billings business.

| Deliverable | Frequency | Standard |

|---|---|---|

| Bank reconciliation — all accounts | Monthly | Completed by the 10th. Zero unexplained variances. |

| Credit card reconciliation | Monthly | Every card reconciled to statement. Business vs. personal flagged. |

| Profit & Loss statement | Monthly | Delivered within 10 days of month-end. Reviewed, not just generated. |

| Balance sheet | Monthly | Asset values, liability balances, and equity reconcile to prior month. |

| Accounts receivable aging | Monthly | Outstanding invoices by age. 90+ day items reviewed with owner. |

| Cash flow statement | Monthly | Actual cash flow compared to prior month and prior year. |

| Tax-ready year-end close | Annual | Books closed by January 31. Tax preparer receives clean financials in February. |

| 1099-NEC preparation | Annual | All contractor payments tracked throughout year. Forms issued by Jan 31. |

| Responsive communication | Ongoing | Questions answered within one business day. Unusual items proactively flagged. |

What a mid-year transition looks like:

Switching to professional bookkeeping mid-year is almost always better than waiting until January. A mid-year transition gives your bookkeeper time to review and correct prior months before year-end — so your tax preparer receives clean full-year financials rather than discovering problems in February. Most transitions take two to four weeks. Your prior provider is legally required to provide your records upon request.

Frequently Asked Questions

How much does professional bookkeeping cost in Billings, MT?

Professional bookkeeping in Billings typically ranges from $400–$700/month for simple service businesses with low transaction volume, to $900–$1,800/month for businesses with employees, inventory, or multiple revenue streams. Construction businesses requiring job costing and WIP schedules typically run $800–$1,500/month. For most Billings businesses in the $400K–$1.5M revenue range, the monthly investment is a fraction of the annual cost of the bookkeeping gaps it prevents.

How do I switch bookkeepers mid-year?

Mid-year transitions are straightforward and usually take two to four weeks. Your prior bookkeeper is legally obligated to provide your QuickBooks file or records upon request — this is your data and your business. We handle the transition: requesting prior records, reviewing and correcting prior months, migrating your file, and getting accounts current. Starting fresh in January is rarely necessary or beneficial.

How often should my books be updated?

Monthly is the professional standard. Books updated quarterly are useful for year-end compliance but useless as a management tool — you can't make good business decisions in November based on June financials. Books updated monthly enable cash flow planning, quarterly tax estimates, and proactive financial management. Books updated annually are essentially just a tax prep input.

What's the difference between a bookkeeper and an accountant for my Billings business?

A bookkeeper records, categorizes, and reconciles transactions and produces financial reports. An accountant interprets those reports, prepares tax returns, advises on entity structure, and makes strategic recommendations. Most Billings businesses need both — a bookkeeper maintaining clean monthly books, and an accountant (or accounting firm) providing tax preparation, tax planning, and financial advisory. When an accounting firm also handles bookkeeping, the two functions coordinate directly, which produces better outcomes than siloed providers.

What do First Interstate Bank and Stockman Bank want to see in my financials?

Billings lenders underwriting commercial loans, equipment financing, or lines of credit want: P&L statements that are consistent with your tax returns, a balance sheet that clearly separates business and personal, an AR aging report demonstrating collectible receivables, two to three years of financial history showing stable or growing revenue, and a DSCR of at least 1.25x. Financial statements reconstructed at year-end often have inconsistencies that trigger lender questions. Monthly books produce consistent financials that hold up to underwriting scrutiny.

Can professional bookkeeping actually lower my tax bill?

Directly — through better deduction capture, and indirectly — through better tax strategy. Directly: vehicle mileage, home office, business meals, and professional development deductions require documentation created at the time of the expense. Monthly bookkeeping is the system that captures this documentation consistently. Indirectly: a tax preparer working from clean current books has time to advise on retirement contributions, depreciation elections, distribution timing, and entity structure decisions — rather than spending their billable time reconstructing your records.

Do I need a bookkeeper if I already have an accountant?

Yes — they serve different functions. Your accountant prepares your tax return and advises on financial strategy. They typically see your books once a year. A bookkeeper maintains your financial records monthly so your accountant has accurate, current data to work from. An accountant working from poorly maintained books is forced to spend time on record cleanup rather than strategy — at accounting rates. The combination of clean monthly bookkeeping plus annual accounting advisory almost always costs less and delivers more than annual reconstruction alone.

How do I know if I've outgrown my current bookkeeping setup?

You've likely outgrown your current setup when: you have employees (payroll complexity requires dedicated bookkeeping attention), your revenue exceeds $500K (lender and tax complexity increases meaningfully at this threshold), you apply for a commercial loan and have to reconstruct records, your tax preparer makes significant adjustments every year, or you can't tell a prospective partner or lender what your profit margin is without looking at last year's tax return. If any of these are true, the cost of upgrading is almost certainly less than the cost of staying where you are.

External Resources

Billings, MT

Professional Bookkeeping for Montana's Largest City

406 Consulting Group provides bookkeeping, tax preparation, and financial advisory to Billings businesses across every major sector. Clean books. Current financials. Tax-ready records. Ready for your lender, your accountant, and your next business decision.

The Monthly Close System

5 steps to financial clarity

Reconcile

Zero unexplained variances by the 10th

Categorize

Chart of accounts aligned to your tax return

Report

P&L + balance sheet within 10 days

Review

Anomalies flagged, trends noted

Act

Tax timing + billing + cash flow decisions

Our Services

Montana Tax Quick Reference

Related Resources