Why Missoula, MT Businesses Need

Professional Bookkeeping

Missoula businesses lose thousands annually to poor bookkeeping. Here's what professional bookkeeping delivers — and what skipping it actually costs you.

Professional bookkeeping in Missoula, MT is not optional for businesses that want to grow, borrow, or simply know whether they're profitable. It is the financial foundation everything else is built on — taxes, financing, payroll, and business decisions. Yet most Missoula business owners are working with something that looks like bookkeeping but isn't: a spreadsheet, a self-taught QuickBooks user, or a well-intentioned employee who learned to enter transactions but doesn't understand what those transactions mean.

This guide explains exactly what professional bookkeeping provides that DIY and amateur approaches don't, what bad bookkeeping actually costs Missoula businesses in dollar terms, and how to evaluate whether your current financial system is serving your business — or quietly working against it.

Table of Contents

The Missoula Business Landscape: Why Professional Bookkeeping Matters Here

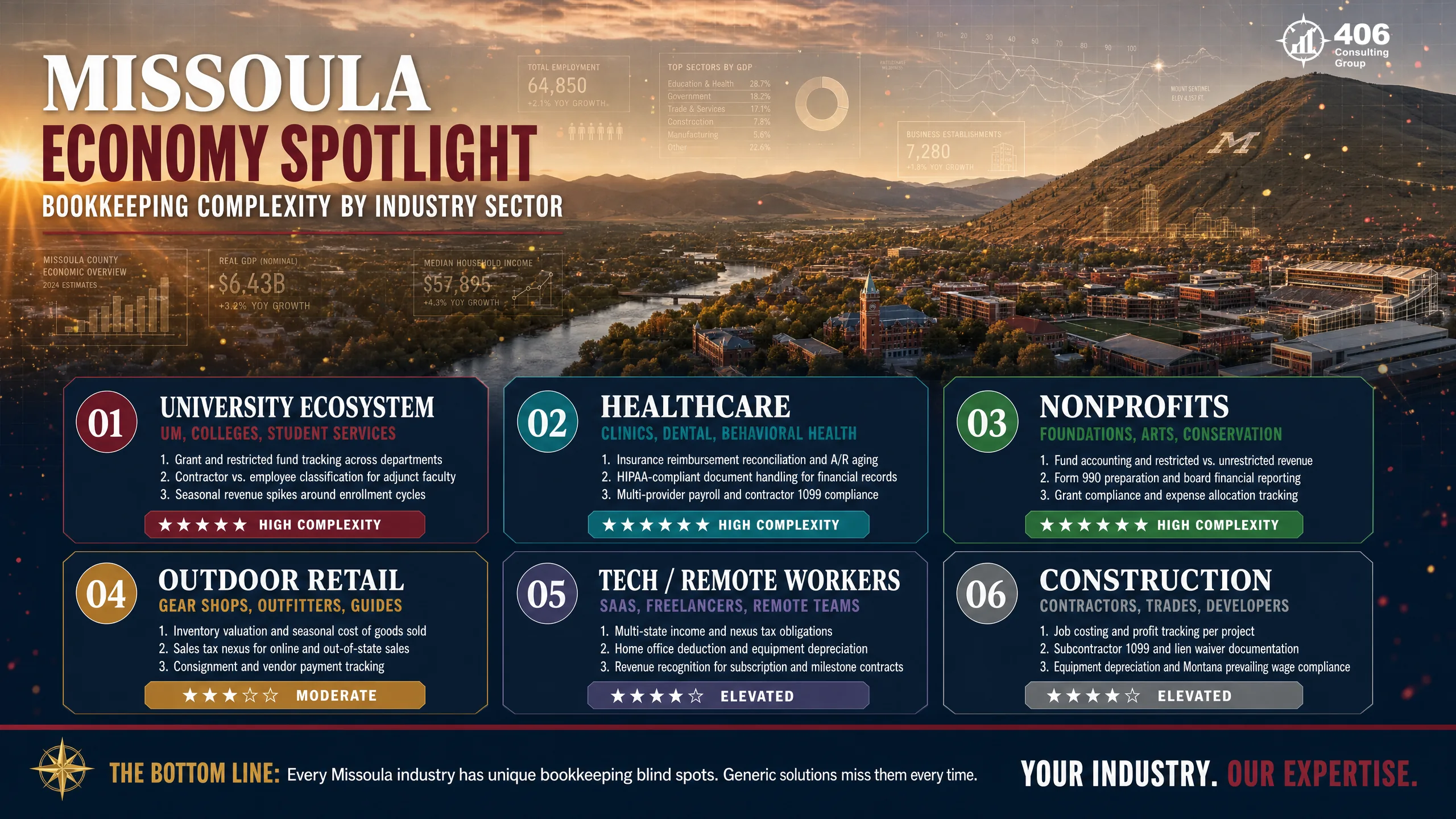

Missoula is unlike any other Montana city in its business composition. The University of Montana anchors an economy that blends academia, healthcare, arts, outdoor retail, nonprofits, and a fast-growing remote-worker community — all layered over a traditional Montana base of construction, trades, and agriculture-adjacent businesses. This diversity creates a bookkeeping environment where generic advice consistently falls short.

75K+

Missoula city population

Montana's second-largest city with a diverse economic base

~500

Active nonprofits in Missoula County

One of Montana's highest nonprofit concentrations — each with distinct bookkeeping needs

$25K+

Average annual bookkeeping gap

Missed deductions, penalties, and catch-up costs for Missoula SMBs

What makes Missoula's bookkeeping environment specifically demanding:

University-adjacent income complexity

UM faculty consulting, research spinoffs, tutoring businesses, student-facing retail, and housing operations all create income and expense patterns that standard bookkeeping templates don't handle cleanly. Misclassification of university contract income vs. self-employment income is one of the most common mistakes we untangle for Missoula clients.

Large nonprofit sector

Missoula has one of the highest concentrations of nonprofits in Montana — environmental organizations, arts groups, social services, and healthcare auxiliaries. Nonprofits require fund accounting that is fundamentally different from for-profit bookkeeping. Using a standard bookkeeping setup for a nonprofit creates Form 990 problems and grant reporting failures.

Remote worker and freelance economy

Missoula's quality of life has attracted a significant remote worker and independent contractor population. Many are high earners with multiple income streams — clients in multiple states, 1099 income, business expenses, and home office deductions — whose tax situations are more complex than their bookkeeping reflects.

Seasonal tourism and outdoor retail

Businesses adjacent to Glacier National Park, the Bob Marshall Wilderness, and Missoula's outdoor recreation culture experience seasonal revenue patterns that require cash flow planning and year-over-year comparison — tools that only work when books are maintained monthly.

The QuickBooks Trap: Why Transaction Entry Isn't Bookkeeping

Anyone can learn to enter transactions into QuickBooks. It takes a weekend, a YouTube tutorial, and a willingness to click through menus. This is not bookkeeping — it is data entry. And the distinction matters enormously, because the difference between data entry and professional bookkeeping is exactly where Missoula businesses are losing money they don't know they're losing.

We are accountants, not bookkeepers. The difference is not a credential technicality — it is the depth of understanding behind every financial decision we make in your books. When our team categorizes a transaction, we understand its tax implication. When we design your chart of accounts, we build it to feed directly into your tax return schedules. When something unusual hits your bank feed, we recognize it and ask the right question instead of guessing. That is what accounting-firm-backed bookkeeping delivers that a self-taught QuickBooks user cannot.

The 8 Costly Mistakes Self-Taught Bookkeepers Make

Wrong chart of accounts from day one

A self-taught bookkeeper uses the QuickBooks default template or copies someone else's setup. The result: income and expense categories that don't align with your tax return's schedules, your industry's norms, or the reporting your lender needs. Rebuilding a chart of accounts mid-stream is expensive and disruptive. An accountant designs it right before the first transaction is entered.

Misclassifying owner contributions as revenue

When the owner transfers money from personal savings into the business account, an untrained bookkeeper often records it as income. It isn't — it's an equity contribution. Misclassified owner contributions inflate reported revenue, distort profitability, and create a tax liability on money that was never profit. This single error can cost thousands in unnecessary taxes.

Expensing capital assets instead of depreciating them

A $15,000 equipment purchase is not an operating expense in the year it's bought — it's a capital asset that must be depreciated over its useful life (or elected for immediate expensing under Section 179 with proper documentation). A self-taught bookkeeper frequently expenses large purchases directly to the P&L, distorting profitability and creating audit exposure. An accountant makes the correct determination every time.

Never reconciling bank accounts

Many self-taught bookkeepers enter transactions from bank feeds but never formally reconcile — meaning they never verify that every transaction in the books matches a corresponding bank statement entry. Errors compound monthly. Duplicate payments, missing transactions, and bank errors go undetected for months or years. Reconciliation is the only error-detection mechanism in bookkeeping.

Mishandling loans as income

When a business takes out an SBA loan, line of credit, or owner loan, the funds appear in the bank account. An untrained bookkeeper sometimes records the deposit as income. It is not income — it is a liability. Recording loans as revenue creates phantom taxable income and misrepresents the company's financial position to any lender reviewing the balance sheet.

S-Corp reasonable compensation errors

For Missoula business owners operating as S-Corps, the IRS requires owners who work in the business to pay themselves a reasonable salary subject to payroll taxes. Self-taught bookkeepers often don't understand this requirement or don't track it correctly in the books. The IRS has aggressively audited S-Corp reasonable compensation for years — this is not a gray area.

Misclassifying contractors as employees (or vice versa)

The IRS and Montana DOR both scrutinize 1099 vs. W-2 classification. A self-taught bookkeeper records payments based on how they're labeled by the business — without understanding the legal test for classification. Misclassification is one of the IRS's highest-priority enforcement areas, and the liability flows back to the year of the misclassification with interest.

No understanding of accrual vs. cash implications

Self-taught bookkeepers generally keep books on cash basis regardless of whether that's appropriate for the business. As revenue crosses $500K–$1M, lenders begin requiring accrual-basis financials and banks become suspicious of cash-basis statements. Converting from cash to accrual requires an accounting judgment call at every transaction — not something a transaction-entry bookkeeper is equipped to handle.

Self-Taught QuickBooks Bookkeeper

- Enters transactions — does not understand their tax consequences

- Uses default chart of accounts not designed for your business

- Has no professional accountability if errors cost you money

- Cannot identify when something is wrong — only records what they see

- Has no connection to your tax preparer — books and taxes are siloed

- Year-end is a scramble — tax preparer receives incomplete records

- No professional liability insurance for errors

Accounting-Firm-Backed Bookkeeping (406 CG)

- Every transaction reviewed through the lens of tax implication

- Chart of accounts designed to align with your tax return schedules

- Professional liability — errors are caught, corrected, and covered

- Unusual transactions flagged and questioned, not blindly recorded

- Bookkeeping and tax prep coordinated by the same team year-round

- Year-end requires a review, not a reconstruction — books are already clean

- E&O insurance carried — you have recourse if something goes wrong

What "Professional" Bookkeeping Actually Means

Professional bookkeeping is not defined by software or price — it is defined by output and accountability. A professional bookkeeping engagement produces five specific deliverables every month, without exception. If your current provider cannot deliver all five, you have a gap.

Reconciled accounts

Every bank account, credit card, and line of credit matched to bank statements with zero unexplained variances. Completed by the 10th of each month. This is the non-negotiable foundation of accurate books.

Accurate categorization

Every transaction assigned to the correct account in a chart of accounts designed for your specific business — not a generic template. Categorization is reviewed against your tax return structure so nothing is lost at year-end.

Monthly financial reports

P&L, balance sheet, and cash flow statement delivered monthly, within 10 days of month-end. These are not generated — they are reviewed. Anomalies are flagged. Trends are noted. The reports tell a story, not just numbers.

Accounts receivable aging

A report showing every outstanding invoice by age — 0–30 days, 31–60, 61–90, 90+. Updated monthly. Missoula businesses with significant receivables cannot manage cash flow without this visibility.

Tax-ready year-end close

Books are formally closed monthly so year-end requires only a final review and adjusting entries — not reconstruction. Your tax preparer receives clean, reconciled financials in February, not in March after a scramble.

The True Cost Ledger: 5 Ways Bad Books Cost Missoula Businesses Money

The True Cost Ledger is our framework for quantifying what bad bookkeeping actually costs — across five categories that most business owners never see itemized together. When you add them up, the total is almost always larger than what professional bookkeeping would have cost.

Tax Leakage

$8,000 – $30,000/year- Deductions not captured in real time: vehicle mileage without a log, meals without documented business purpose, home office not measured and tracked

- Deductions missed entirely: professional development, software subscriptions, equipment under $2,500 that qualifies for immediate expensing

- Tax strategy opportunities invisible to the tax preparer because the books don't surface them: retirement plan contributions, depreciation elections, S-Corp salary optimization

- Tax preparer billing at higher rates to do bookkeeping reconstruction — time that should be spent on tax strategy spent on transaction entry instead

Compliance Exposure

$500 – $50,000+- IRS CP2000 notices from income not captured in books that appeared on third-party 1099 forms — with interest accruing from the original due date

- Montana DOR underpayment penalties from estimated taxes calculated on incorrect book income

- 1099-NEC filing failures for subcontractors not tracked in bookkeeping — $60–$630 per missed form, plus IRS penalty notices

- Montana UI (unemployment insurance) underpayment from payroll not reconciled to books — audited quarterly by the Montana Department of Labor

Decision Blindness

$10,000 – $100,000+ in missed or wrong decisions- Pricing decisions made without knowing actual cost — businesses that have never calculated their true cost per service or product are guessing on margin

- Hiring decisions made without cash flow projections — adding a $60,000/year employee without knowing if the business can sustain it for 12 months

- Seasonal cash flow crises that were visible in the books six months earlier but invisible to the owner who doesn't have monthly reports

- Revenue trends that show which services or clients are growing vs. declining — invisible without job-level or segment-level reporting

Growth Barriers

$50,000 – $500,000+ in denied or delayed financing- Commercial loan applications denied because financial statements are unauditable or inconsistent with tax returns

- SBA loan applications delayed by months while books are reconstructed — during which time the opportunity the loan was meant to fund may have passed

- Business sale valuation suppressed by poor financial records — buyers discount price or walk away entirely when books are unreliable

- Bonding capacity for construction contractors limited by inability to produce clean WIP schedules and balance sheets

Owner Time Drain

$12,000 – $30,000+/year in opportunity cost- 10–15 hours per month spent on bookkeeping by owners billing $100–$150/hour = $1,000–$2,250/month in diverted productive time

- Additional hours in March reconstructing the year for tax prep — typically 20–40 hours for businesses that didn't maintain monthly books

- Mental load of financial uncertainty: operating without knowing your actual cash position, profitability, or tax liability creates stress that affects business decisions

- Tax season scramble that consumes owner attention during a period when many Missoula businesses are entering their busiest spring season

Missoula's Economic Mix: Industry-Specific Bookkeeping Needs

Missoula's unusual economic composition means that industry-specific bookkeeping knowledge matters more here than in many Montana cities. Here's what each major sector requires:

University of Montana Ecosystem

- 1Faculty consulting income: UM faculty who consult externally often receive 1099 income that sits alongside W-2 wages — correct classification and expense tracking against consulting income is essential

- 2Research and grant-funded businesses: spinoff companies from UM research programs often have a mix of federal grant income and commercial revenue requiring separate tracking

- 3Student-facing businesses: tutoring, childcare, food service with university contracts — often have inconsistent revenue patterns and complex receivable timing

- 4Housing adjacent to campus: furnished rentals, student housing operations, and property management with high tenant turnover create significant receivables and security deposit tracking requirements

Healthcare & Medical Practices

- 1Insurance reimbursement timing: income billed to insurance differs significantly from income received — accrual basis required for meaningful financial reporting

- 2Provider compensation structures: physicians as partners vs. employees vs. independent contractors creates significant payroll and K-1 complexity

- 3Multiple entity structures: Missoula practices often operate through a professional corporation, a management services organization, and a real estate entity simultaneously

- 4Montana Medicaid and Medicare billing adjustments: contractual allowances between billed charges and reimbursed amounts must be tracked as revenue adjustments, not expenses

Outdoor Retail & Recreation

- 1Seasonal cash flow extremes: summer and fall revenue may represent 70–80% of annual income — books must reflect this pattern for accurate year-over-year comparison

- 2Inventory management: COGS tracking requires periodic inventory counts and consistent valuation method (FIFO or average cost) applied throughout the year

- 3Consignment and vendor-managed inventory: items in the store but not yet purchased create receivable and payable tracking that standard bookkeeping templates miss

- 4Equipment rental tracking: shops that rent gear alongside selling it need clear separation of rental revenue from product sales in the chart of accounts

Construction & Trades

- 1Job costing: every material, labor, and subcontractor cost allocated to the specific project that incurred it — required for knowing whether each job is profitable

- 2Retainage receivable: funds withheld by general contractors until project completion must be tracked as a separate receivable line item — often represents 5–10% of contract value

- 3Subcontractor 1099 compliance: every subcontractor paid over $600 requires a year-end 1099-NEC — books must capture name, EIN, and payment amount throughout the year

- 4Montana workers compensation: L&I equivalent through Montana State Fund — rates vary by trade classification and must be tracked against certified payroll records

Technology & Remote Workers

- 1Multi-state income: remote workers and consultants with clients in multiple states may have filing obligations in states where they earn income — books must capture client location by revenue

- 2Home office deduction: the most commonly missed deduction for Missoula remote workers — requires square footage documentation and consistent monthly tracking to survive audit

- 3Subscription and SaaS revenue recognition: recurring billing models require revenue to be recognized as services are delivered, not when payment is received

- 4Equity compensation for startups: options, warrants, and phantom equity require specific accounting treatment that standard bookkeeping templates don't handle

Hospitality & Food Service

- 1Tip income reporting: whether tips are pooled, individual, or credit card-allocated, they create payroll tax complexity that must be tracked and reported correctly

- 2Food and beverage COGS: gross profit on food service requires tracking beginning inventory, purchases, and ending inventory every accounting period

- 3Liquor license compliance: alcohol sales tracking for both COGS and compliance reporting — Montana's unique liquor license system creates additional administrative requirements

- 4Seasonal staffing fluctuations: Missoula hospitality businesses with high summer turnover face significant payroll complexity and W-2 reconciliation at year-end

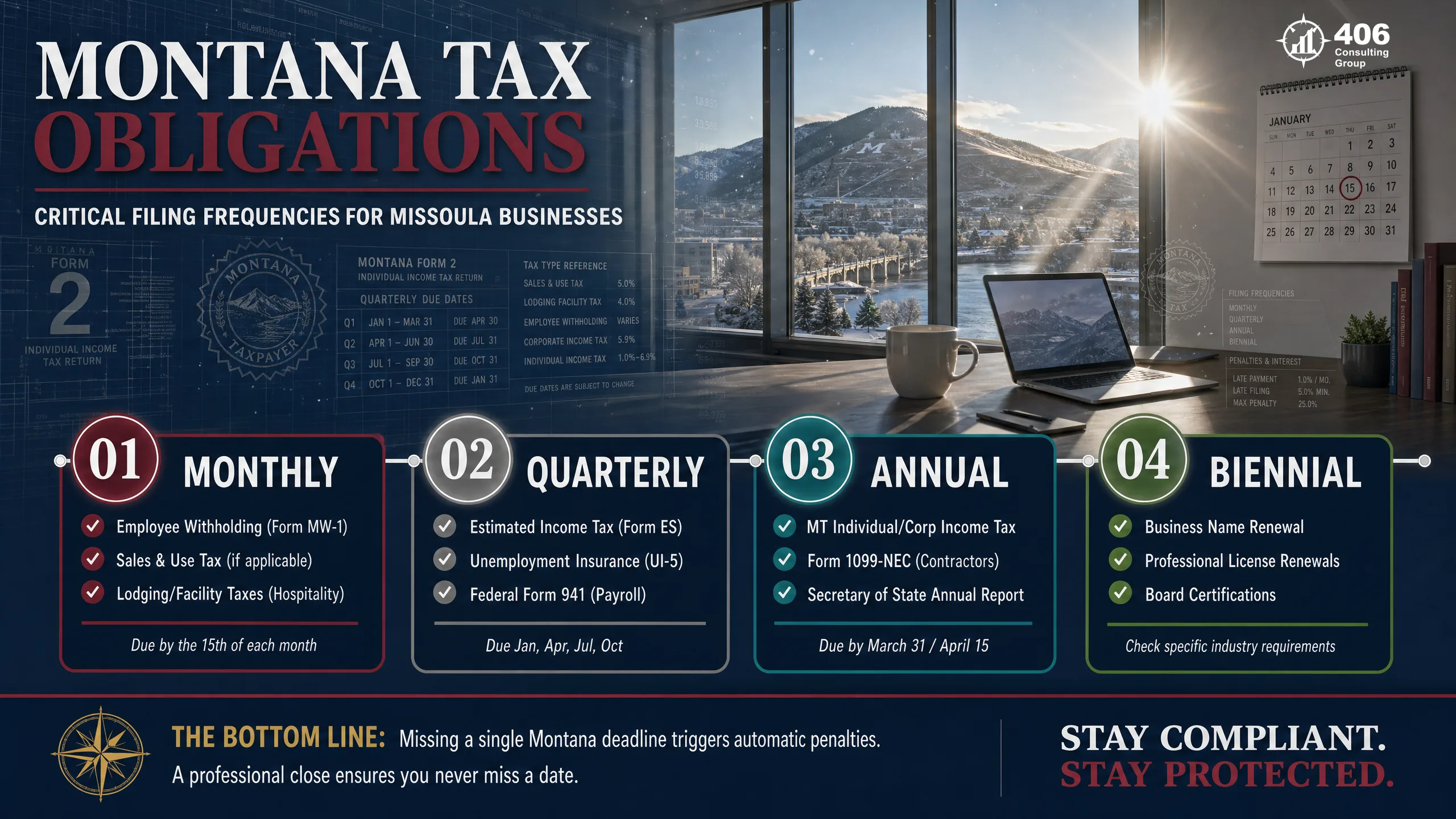

Montana Tax Obligations Every Missoula Business Must Track

Montana's tax structure is meaningfully different from neighboring states — and different from what most national bookkeeping advice assumes. No sales tax simplifies one layer. But Montana income tax, UI filings, workers compensation, and annual report requirements create a compliance calendar that falls apart when books aren't maintained monthly.

Montana Individual and Corporate Income Tax

Montana taxes business income at rates up to 6.75% for both individuals (pass-through income from S-Corps, partnerships, and sole proprietorships) and C-Corps. Quarterly estimated payments are due April 15, June 15, September 15, and January 15. Underpayment penalties apply when estimates fall below safe harbor thresholds. Books must be accurate monthly to calculate estimates correctly.

Montana Withholding Tax

Employers must withhold Montana income tax from employee wages and remit to the Montana DOR on a monthly or quarterly schedule based on total withholding volume. The withholding account must reconcile to W-2s at year-end. Discrepancies trigger DOR correspondence that is time-consuming and potentially penalized.

Montana Unemployment Insurance (UI)

Montana employers are required to register for and remit unemployment insurance contributions to the Montana Department of Labor and Industry. Quarterly wage reports are due the last day of April, July, October, and January. UI contributions are calculated on taxable wages per employee — failure to file or late filing triggers penalties and interest. Books must capture wages by employee accurately for the quarterly report.

Montana Workers Compensation (Montana State Fund)

Most Montana employers must carry workers compensation through Montana State Fund or a private carrier. Premiums are based on payroll by employee classification code. Annual audits compare actual payroll to estimated payroll — underpayment creates a retroactive premium bill. Books must classify wages by worker classification correctly throughout the year.

1099-NEC Filing (Federal + Montana)

Every subcontractor, independent contractor, or non-employee paid $600 or more must receive a 1099-NEC by January 31. Montana also requires 1099 copies for contractors with Montana withholding. Books must capture contractor names, EINs, and payment totals throughout the year — attempting to reconstruct this in January from bank statements is error-prone and often incomplete.

Montana Business Annual Report

Montana LLCs, corporations, and other registered entities must file an annual report with the Montana Secretary of State. The report confirms registered agent, officer information, and business status. While the filing itself is simple, missing it can result in administrative dissolution — which has significant implications for liability protection and banking relationships.

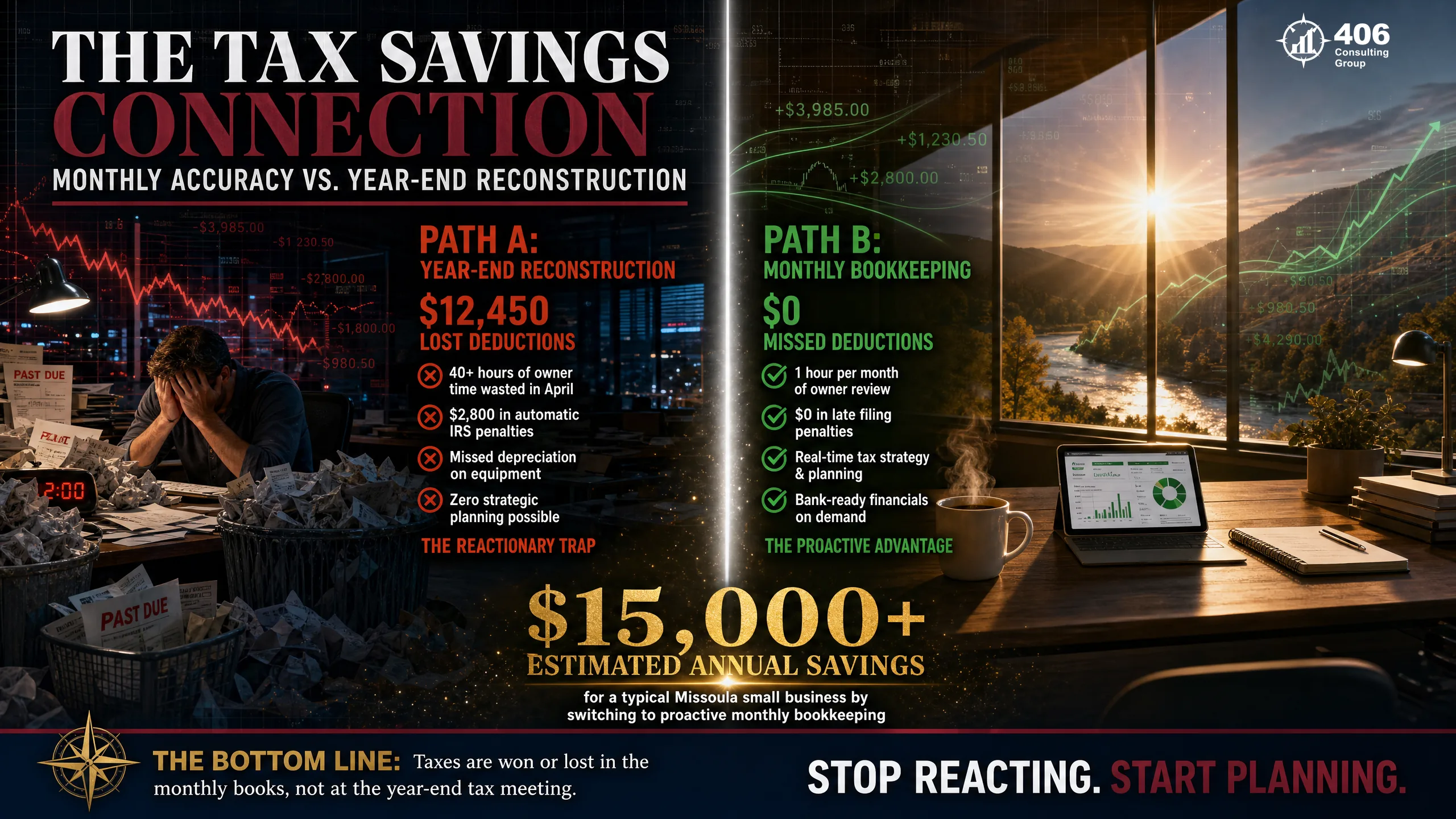

How Professional Bookkeeping Connects to Tax Savings

The connection between bookkeeping quality and tax outcome is direct, specific, and measurable. Your tax preparer can only work with what the books provide. When the books are incomplete, conservative positions are taken on deductions — not because the deductions aren't legitimate, but because they can't be substantiated without documentation.

Specific deductions commonly missed by Missoula businesses with poor bookkeeping:

Vehicle mileage

$0.67/mile (2024 rate)Must be logged contemporaneously — reconstructed logs from memory are not deductible. A Missoula contractor driving 20,000 business miles/year misses $13,400 in deductions without a real-time log.

Home office

$5/sq ft (simplified method)Requires consistent documentation of dedicated space used regularly and exclusively for business. Not claimed unless books track it monthly — and yet most Missoula remote workers qualify.

Business meals

50% deductibleRequire documented business purpose at the time of the meal. A receipt from three months ago with no notes attached is not a deductible meal — the documentation must exist contemporaneously.

Professional development

100% deductible if business-relatedCourses, conferences, books, and subscriptions related to your trade or business. Commonly missed when lumped into miscellaneous or not tracked at all.

Section 179 / Bonus depreciation

100% bonus depreciation (OBBBA permanent)Equipment, software, and certain improvements can be expensed in the year purchased rather than depreciated — permanently at 100% under OBBBA (July 2025). Requires a tax strategy decision at purchase time — invisible if books don't surface the purchase correctly.

Retirement plan contributions

SEP-IRA: up to 25% of net earningsDeductible contributions to SEP-IRA, Solo 401(k), or SIMPLE IRA reduce taxable income dollar-for-dollar. The optimal contribution amount can only be calculated from accurate year-to-date net income — which requires accurate books.

What we see consistently: Missoula business owners who switch from year-end reconstruction to monthly professional bookkeeping reduce their tax preparation bill by 30–40% (preparer spends time on strategy, not reconstruction) and reduce their tax liability by $8,000–$20,000 (previously missed deductions now documented and claimed). The bookkeeping cost is recovered within the first tax cycle in most cases.

Bookkeeping and Business Financing in Montana

Missoula's lending market includes Glacier Bancorp, First Security Bank of Bozeman (Missoula branches), Opportunity Bank of Montana, and several credit unions. When a Missoula business owner walks in to apply for a commercial loan, equipment financing, or a line of credit, the underwriter's first request is for two to three years of financial statements. What happens next is determined entirely by the quality of the books those statements came from.

Books maintained professionally

Smooth approval

- P&L statements clean, reconciled, and consistent with tax returns

- Balance sheet shows assets, liabilities, and equity accurately

- AR aging report demonstrates collectible receivables

- Personal and business accounts completely separated

- Underwriter can calculate DSCR in minutes, not weeks

- Loan closes on timeline — opportunity captured

Books in poor condition

Denied or significantly delayed

- Financial statements inconsistent with tax returns — underwriter flags every discrepancy

- Personal expenses mixed with business — DSCR calculation impossible to validate

- No AR aging report — receivables excluded from collateral analysis

- Reconstruction required — costs $5,000–$15,000 and takes months

- Timeline missed — equipment purchase, expansion, or acquisition delayed or lost

- Loan denied — or approved at worse terms with additional collateral requirements

Payroll Compliance for Missoula Employers

Payroll is where bookkeeping errors become legal liability most quickly. Montana has specific payroll obligations — beyond federal requirements — that create compliance risk for Missoula employers who don't track them correctly in the books.

Montana income tax withholding

Employers withhold state income tax from all W-2 employees. Rates range from 1%–6.75% based on withholding tables. Remitted monthly or quarterly depending on volume. Books must reconcile withholding remittances to payroll records — discrepancies surface in DOR audits.

Federal payroll taxes (FICA)

Social Security (6.2% employer + 6.2% employee) and Medicare (1.45% employer + 1.45% employee) withheld and matched by employer. Remitted to IRS semi-weekly or monthly. Payroll software handles the calculation — books must capture the full cost including the employer match, not just take-home pay.

Montana Unemployment Insurance (UI)

Quarterly wage reports and contribution payments due last day of April, July, October, and January. New employer rate is 1.0% on first $43,000 of wages per employee (2024). Experience-rated employers may pay higher or lower. Books must capture gross wages by employee for accurate quarterly reporting.

Montana State Fund (workers compensation)

Premium calculated on actual payroll by worker classification. Annual audit compares actual payroll to estimated payroll — underpayments create retroactive bills, overpayments create credits. Books must classify each worker's wages by their correct MSF classification code.

1099 vs. W-2 classification

Montana applies the same behavioral and financial control tests as the IRS for worker classification. Misclassifying an employee as a contractor avoids payroll taxes in the short term but creates liability for all unremitted taxes plus penalties — potentially going back multiple years. An accountant reviews classification decisions; a self-taught bookkeeper records whatever the business owner tells them.

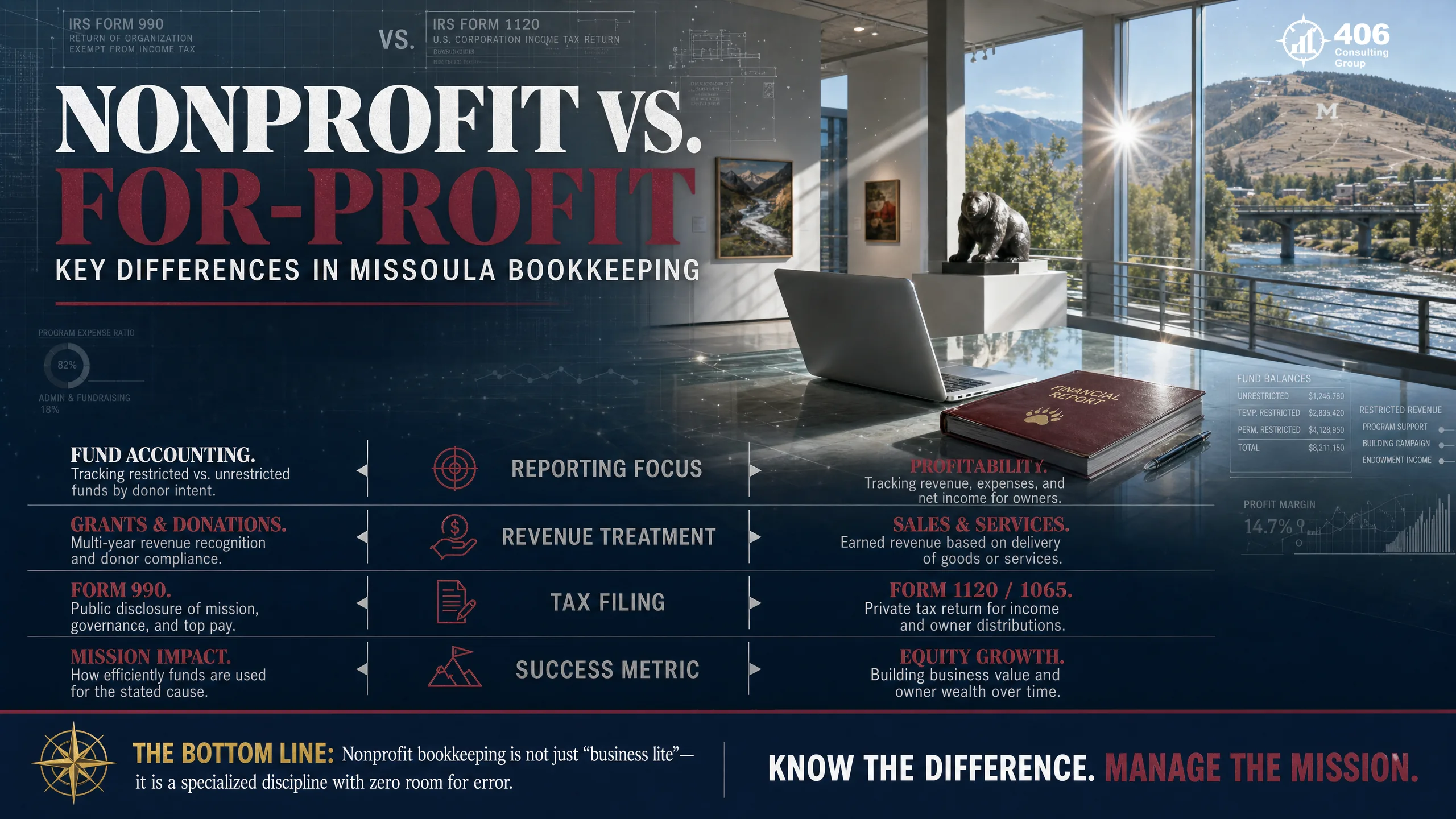

The Nonprofit Bookkeeping Question: A Missoula-Specific Consideration

Missoula has one of the highest concentrations of nonprofits in Montana — environmental organizations, arts groups, social services agencies, healthcare auxiliaries, and university-adjacent foundations. Nonprofit bookkeeping is fundamentally different from for-profit bookkeeping, and using a standard for-profit setup for a nonprofit creates specific, costly problems.

For-Profit Bookkeeping

Revenue

Recorded when earned; profit maximization is the goal

Reporting

P&L and balance sheet — focused on profitability and net worth

Tax filing

Form 1120 (C-Corp), 1120-S (S-Corp), 1065 (partnership), Schedule C (sole proprietor)

Chart of accounts

Organized around operating profit — revenue, COGS, operating expenses

Grant income

Treated as revenue when received or earned

Nonprofit Fund Accounting

Revenue

Segregated into restricted and unrestricted net assets — restricted grants can only be spent on the donor-specified purpose

Reporting

Statement of financial position, statement of activities, statement of functional expenses — organized around mission delivery

Tax filing

Form 990, 990-EZ, or 990-N depending on gross receipts — publicly disclosed; errors are visible

Chart of accounts

Organized around programs, supporting services, and fundraising — functional expense allocation required

Grant income

Restricted grants treated as conditional contributions — revenue recognized only when conditions are met, not when cash arrives

The common mistake:Missoula nonprofits using a standard for-profit QuickBooks setup — no fund tracking, no functional expense allocation, no restricted vs. unrestricted segregation. The Form 990 then requires data the books can't produce, creating either a delayed or inaccurate filing. Form 990 is public record — major donors and foundation grant committees review it before making contribution decisions.

When Your Current Bookkeeping System Has Hit Its Limit

These eight warning signs indicate that your current bookkeeping system — whether it's DIY, a self-taught bookkeeper, or a setup that worked fine at $200K but hasn't been upgraded since — has hit its ceiling.

Books are perpetually 1–3 months behind

You are operating on outdated financial data. Every business decision made since the last close is based on incomplete information.

You avoid looking at your financial reports

This is the clearest signal that the reports aren't useful or trustworthy. Owners who have confidence in their books look at them regularly because they help.

Your tax preparer makes significant adjustments every year

If your accountant or tax preparer is reclassifying large amounts, adjusting retained earnings, or rebuilding schedules at year-end, your books are not accurate. You are paying accounting rates for bookkeeping work.

You can't answer "are we profitable right now?" with confidence

If profitability is a quarterly or annual discovery rather than a monthly known, your bookkeeping isn't serving your business.

You've received an IRS or Montana DOR notice you didn't expect

Unexpected tax notices almost always trace back to bookkeeping — unreported income, misclassified payments, or estimated tax underpayment from inaccurate books.

A lender asked for financial statements and the response was "we'll need some time"

Financial statements should be producible in minutes from well-maintained books. If they require weeks to compile, your books aren't current.

You have employees and no one is reconciling payroll to the books monthly

Payroll is the highest-frequency source of bookkeeping errors for businesses with staff. Unreconciled payroll compounds into year-end W-2 problems and UI reporting discrepancies.

Your bookkeeper has never mentioned a tax implication, flagged an unusual transaction, or proactively raised a financial concern

If your bookkeeper only enters transactions and never surfaces anything, you have a data entry person — not a professional financial resource. Accounting-backed bookkeeping should generate insights, not just records.

What to Expect from a Professional Bookkeeper: The Baseline Standard

If you're evaluating whether to upgrade your bookkeeping or switch providers, here is the minimum standard any professional engagement should meet. These aren't exceptional deliverables — they are the baseline.

| Deliverable | Frequency | Standard |

|---|---|---|

| Bank reconciliation — all accounts | Monthly | Completed by the 10th of each month. Zero unexplained variances. |

| Credit card reconciliation | Monthly | Every card reconciled to statement. Business vs. personal charges flagged. |

| Accounts receivable aging | Monthly | Report showing outstanding invoices by age. 90+ day items reviewed with owner. |

| Profit & Loss statement | Monthly | Delivered within 10 days of month-end. Reviewed for anomalies, not just generated. |

| Balance sheet | Monthly | Reviewed for accuracy — asset values, liability balances, and equity tie to prior month. |

| Tax-ready year-end close | Annual | Books closed by January 31. Tax preparer receives clean financials in February. |

| Responsive communication | Ongoing | Questions answered within one business day. Proactive flags raised when something unusual appears. |

| Annual 1099 preparation | Annual | All contractor payments tracked throughout the year. 1099-NECs issued by January 31. |

Frequently Asked Questions

How much does professional bookkeeping cost in Missoula, MT?

Professional bookkeeping in Missoula ranges from $350–$600/month for simple service businesses with low transaction volume, to $800–$1,500/month for businesses with employees, inventory, or multiple revenue streams. Nonprofits requiring fund accounting typically fall in the $500–$1,200/month range depending on grant complexity. For most Missoula businesses in the $300K–$1M revenue range, the monthly investment is significantly less than the annual cost of the bookkeeping gaps described in the True Cost Ledger above.

What's the difference between a bookkeeper and an accounting firm doing bookkeeping?

A standalone bookkeeper — especially a self-taught one — enters transactions, reconciles accounts, and produces reports. They typically have no formal accounting education and no professional accountability. An accounting firm doing bookkeeping brings accountants who review every decision for tax implication, design your chart of accounts to align with your tax return, flag unusual transactions that a transaction-entry bookkeeper would record without question, and connect your books to your tax strategy year-round. The output looks similar on the surface; the quality and usefulness are not comparable.

Does my Missoula nonprofit need different bookkeeping than a for-profit business?

Yes — significantly. Nonprofits require fund accounting that segregates restricted and unrestricted net assets, tracks grant conditions and expenditure, allocates expenses by functional category (programs, management, fundraising), and produces financial statements in the formats required for Form 990. A standard for-profit QuickBooks setup cannot produce these outputs without significant modification. Nonprofits that use a for-profit bookkeeping setup typically discover the problem when Form 990 is due and the required data doesn't exist in the books.

How do I know if my current bookkeeper is making costly mistakes?

The most reliable indicators: your tax preparer makes significant adjustments or reclassifications every year (sign the books aren't accurate); you've received IRS or DOR notices you didn't expect (sign of income mismatches or underpayment); your financial statements don't match your tax returns (sign of misclassification); you can't get a current P&L quickly when needed (sign books aren't maintained monthly). If any of these are true, a professional review of your books will almost always surface the specific problems.

Can I switch to 406 Consulting Group mid-year?

Yes — and mid-year is often better than waiting until January. A mid-year switch gives us time to review and correct the prior months before year-end, ensuring your tax preparer receives clean financials rather than discovering problems in February. We handle the transition, including requesting your prior records from your current provider (they're legally required to provide them), migrating your bookkeeping file, and getting your accounts current. Most transitions take two to four weeks.

What Montana-specific taxes does a Missoula business need to track?

Montana businesses must track state income tax withholding (for W-2 employees), quarterly unemployment insurance (UI) contributions and wage reports, workers compensation premiums through Montana State Fund or a private carrier, and the Montana annual report for registered entities. Montana has no sales tax, which removes one layer of complexity. Quarterly estimated income tax payments (both federal and Montana) must be calculated from accurate current-year book income — which is only possible if books are maintained monthly.

What should I bring to a first consultation with 406 Consulting Group?

The most useful things to have available: your most recent business tax return, access to your current bookkeeping software or a trial balance export, the last three months of bank and credit card statements, and a clear sense of where your current bookkeeping is falling short. If your books are significantly behind or disorganized, don't worry — we assess the situation without judgment and give you a specific plan for getting current. The consultation is about understanding where things are, not where they should have been.

External Resources

Missoula, MT

Professional Bookkeeping Backed by Accountants

406 Consulting Group provides bookkeeping, tax preparation, and financial advisory to Missoula businesses. Our bookkeepers are backed by accountants who understand the tax implications behind every entry — so your books are accurate, compliant, and ready when you need them.

The True Cost Ledger

What bad bookkeeping actually costs

Tax Leakage

Compliance Exposure

Decision Blindness

Growth Barriers

Owner Time Drain

You've Hit the Limit When...

Montana Tax Quick Reference

Related Resources