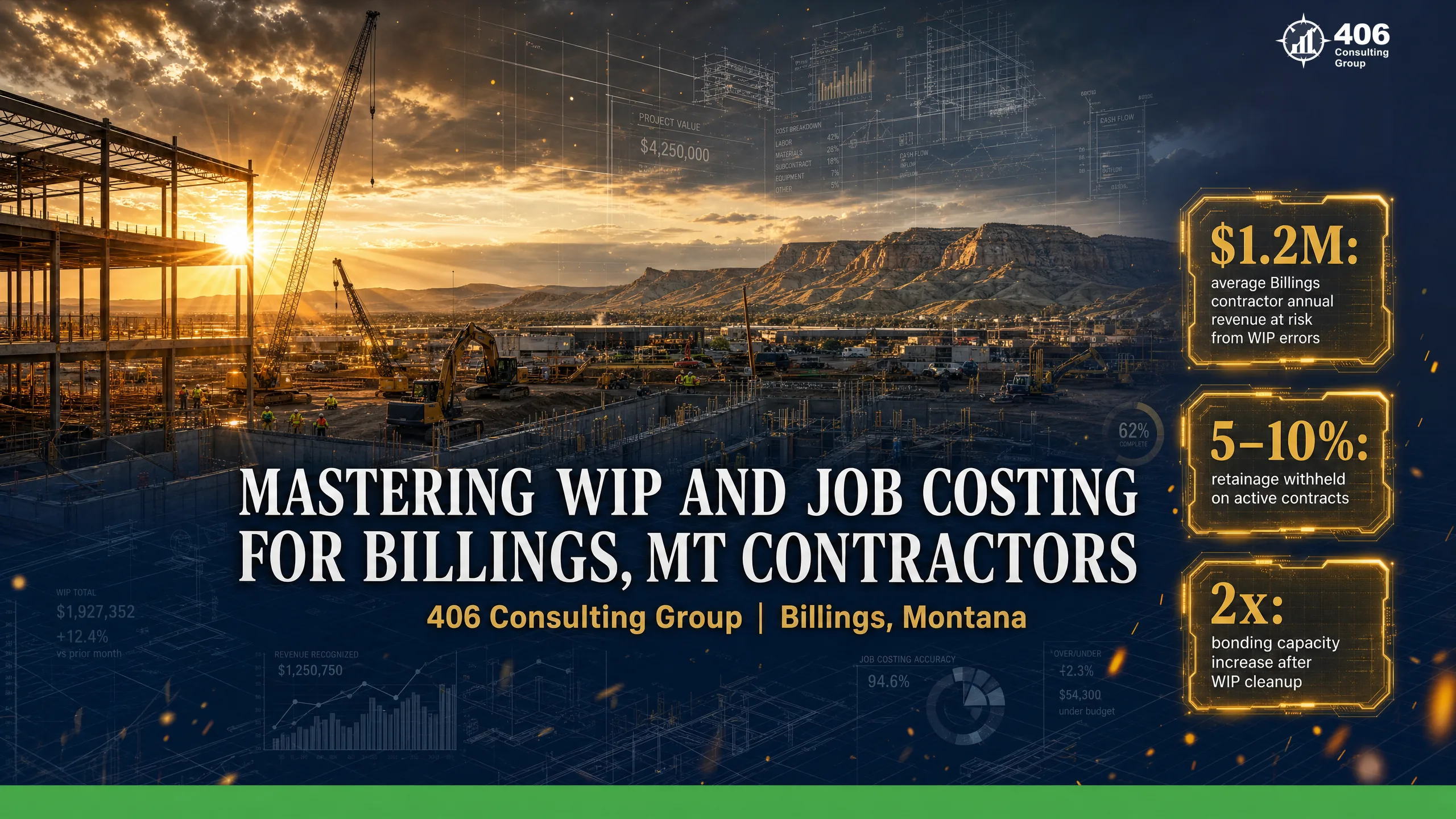

Mastering WIP and Job Costing

for Billings, MT Contractors

Billings contractors lose profit on every job without WIP and job costing. Here's the complete system — from cost capture to bonding capacity — built for Montana contractors.

Job costing and WIP accounting for Billings, MT contractors are the difference between knowing your margin and guessing at it. Most Billings contractors know roughly whether a job went well. Few know precisely — by how much, on which cost line, and early enough to do anything about it. That gap is where profit disappears.

This guide covers the complete system — from setting up job costs before the first PO is issued to reading a WIP schedule the way your bonding underwriter does. Whether you're a general contractor running multiple jobs simultaneously on the I-90 corridor or a specialty sub managing 15 open projects, the Contractor Clarity Stack applies the same way: Job Setup → Cost Capture → Monthly WIP Schedule → Capital Access.

Table of Contents

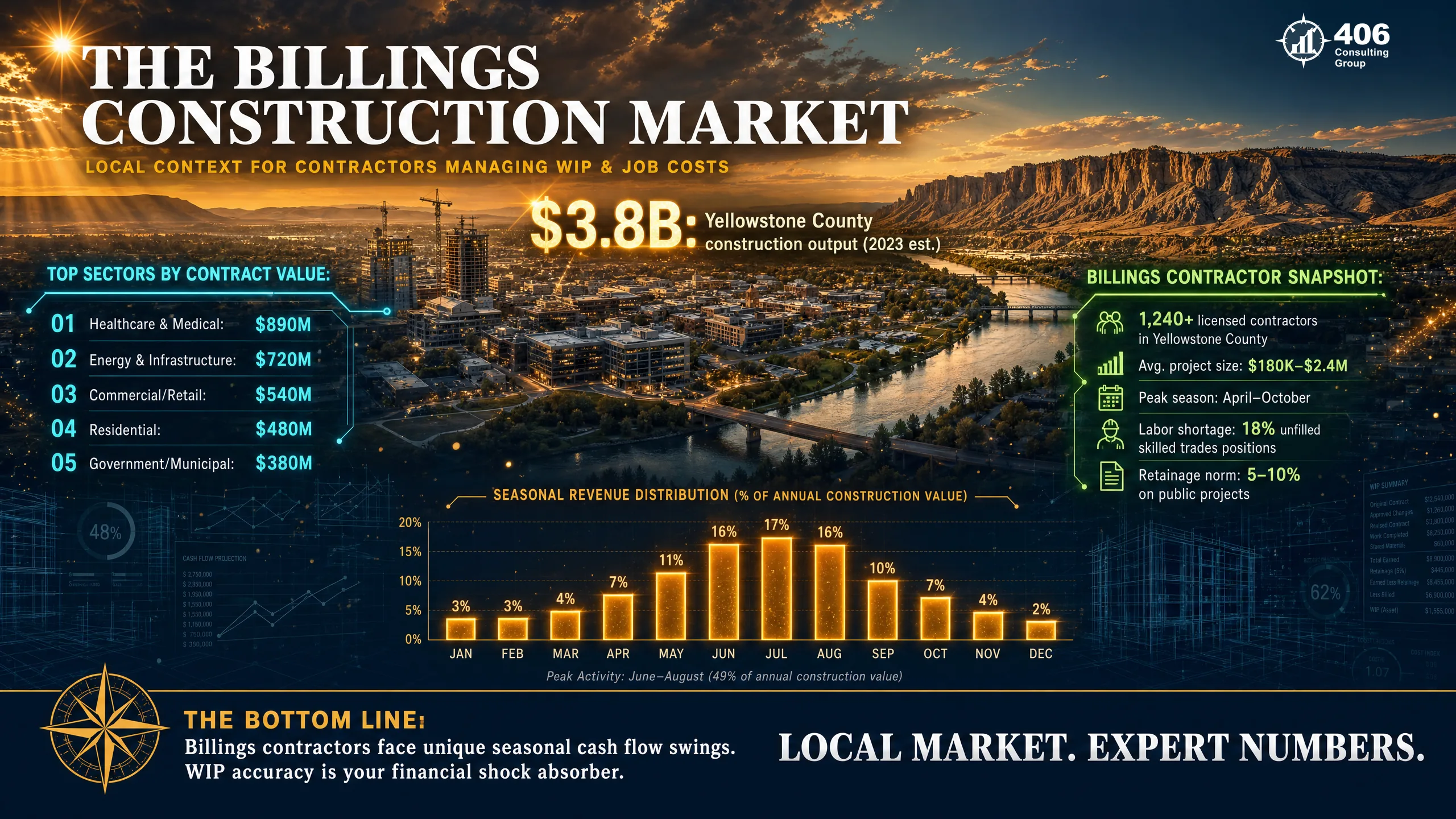

The Billings Construction Market: Why Financial Complexity Is Higher Here

Billings is Montana's largest city and its economic engine — 120,000+ residents, the state's primary commercial hub, and a construction market that runs year-round in a way smaller Montana cities cannot. That scale brings opportunity, but it also brings the kind of financial complexity that exposes contractors who are running their books like a one-job operation.

$300M+

Annual construction permits in Billings

One of the highest volumes of any Montana market

400+

Active general contractors in Yellowstone County

Competitive market where margin discipline separates winners

5–10%

Retainage withheld on active contracts

On a $3M backlog: $90K–$180K in hidden receivables

What makes Billings contractors' financial environment specifically demanding:

Multi-job pipeline management

A Billings GC managing 4–8 simultaneous projects cannot track job-level profitability without formal job costing. Each job has its own contract, its own cost budget, its own subcontractors, and its own billing schedule. Without job-level books, you're managing aggregate revenue and aggregate cost — which tells you nothing about which jobs are making money and which are bleeding.

Public contract and prevailing wage requirements

Billings contractors working on DOT projects, Yellowstone County public works, or any federally-funded contract must maintain certified payroll records and pay Montana prevailing wage rates. These requirements demand payroll systems that code by job and by trade classification — which only works if your job costing infrastructure is already in place.

Bonding and banking requirements

First Interstate Bank, Stockman Bank, and Glacier Bank all underwrite contractor loans with an expectation of clean financial statements. Surety companies set bonding limits based on working capital, equity, and WIP schedule quality. In Billings' competitive market, a contractor who can't demonstrate financial control loses bids to contractors who can.

Bakken-adjacent energy and oil field services

Contractors serving pipeline, tank, and facility work in the Bakken fringe area face additional complexity: multi-state projects, union payroll requirements, and Davis-Bacon compliance. These jobs require a job costing system sophisticated enough to separate costs by project location and labor classification.

What WIP Actually Is — And Why Most Contractors Get It Wrong

Work-in-progress (WIP) accounting is the method by which contractors recognize revenue in proportion to the work they've actually completed — not in proportion to what they've billed. This distinction is the source of most contractor financial confusion.

Cash-basis thinking — "I billed $80K this month so I made $80K this month" — is intuitive but wrong for contractors. A contractor's bank balance reflects billing timing. A WIP schedule reflects economic reality. The two can diverge by hundreds of thousands of dollars on a single project.

The Contractor Clarity Stack

Four layers every Billings contractor must build — in order

Job Setup

Chart of accounts organized by job, cost codes established, contract value and estimated cost entered before the first purchase order is issued. This layer cannot be built retroactively without significant pain.

If your job costing starts after a job is 30% complete, you've already lost the data that makes it useful. Setup happens before mobilization.

Cost Capture

Daily or weekly labor coding by employee and job, purchase orders matched to job number at point of order, subcontractor invoices coded to job on receipt.

Cost capture is a discipline problem as much as a systems problem. A bookkeeper who codes labor to 'job expenses' instead of specific jobs destroys the entire layer below.

Monthly WIP Schedule

Percentage complete calculated by cost-to-cost method, revenue earned recognized based on completion percentage, overbilling and underbilling identified by job, retainage tracked separately.

The WIP schedule is your financial compass. Produced monthly, reviewed monthly. Not a year-end document — a management tool used between jobs closing.

Capital Access

Bonding capacity calculated from clean WIP and working capital, bank lending supported by reconciled financial statements, retainage receivable recognized as collateral.

The output of a working Contractor Clarity Stack is a contractor who can borrow, bond, and bid — at better terms than competitors without this system.

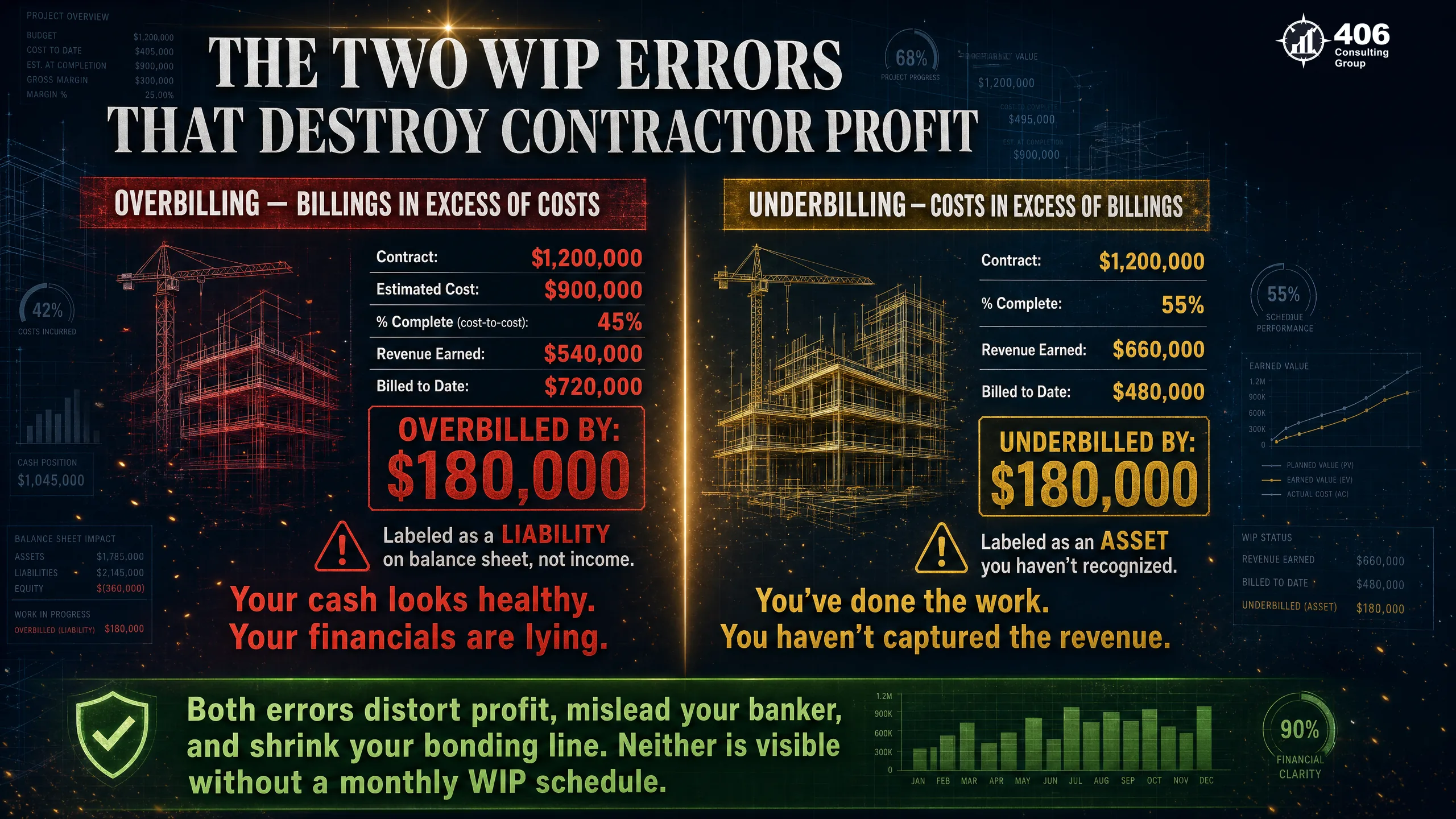

Overbilling vs. Underbilling: The Two Errors That Kill Margin

Every WIP error falls into one of two categories. Understanding the difference — and what each one means for your balance sheet, your bonding, and your banker — is the foundation of contractor financial literacy.

Overbilling — Billings in Excess of Costs

A liability on your balance sheet — not income

The $180,000 overbilled is a liability — you've collected money for work you haven't done yet. Your cash position looks strong. Your balance sheet is misrepresenting your financial position. Your banker sees this and reduces your working capital calculation.

Underbilling — Costs in Excess of Billings

An asset on your balance sheet — revenue you haven't captured

The $180,000 underbilled is an asset — you've earned revenue you haven't billed for yet. If it's not on your balance sheet, your financial statements understate your company's value, your working capital is understated, and your bonding capacity is unnecessarily limited.

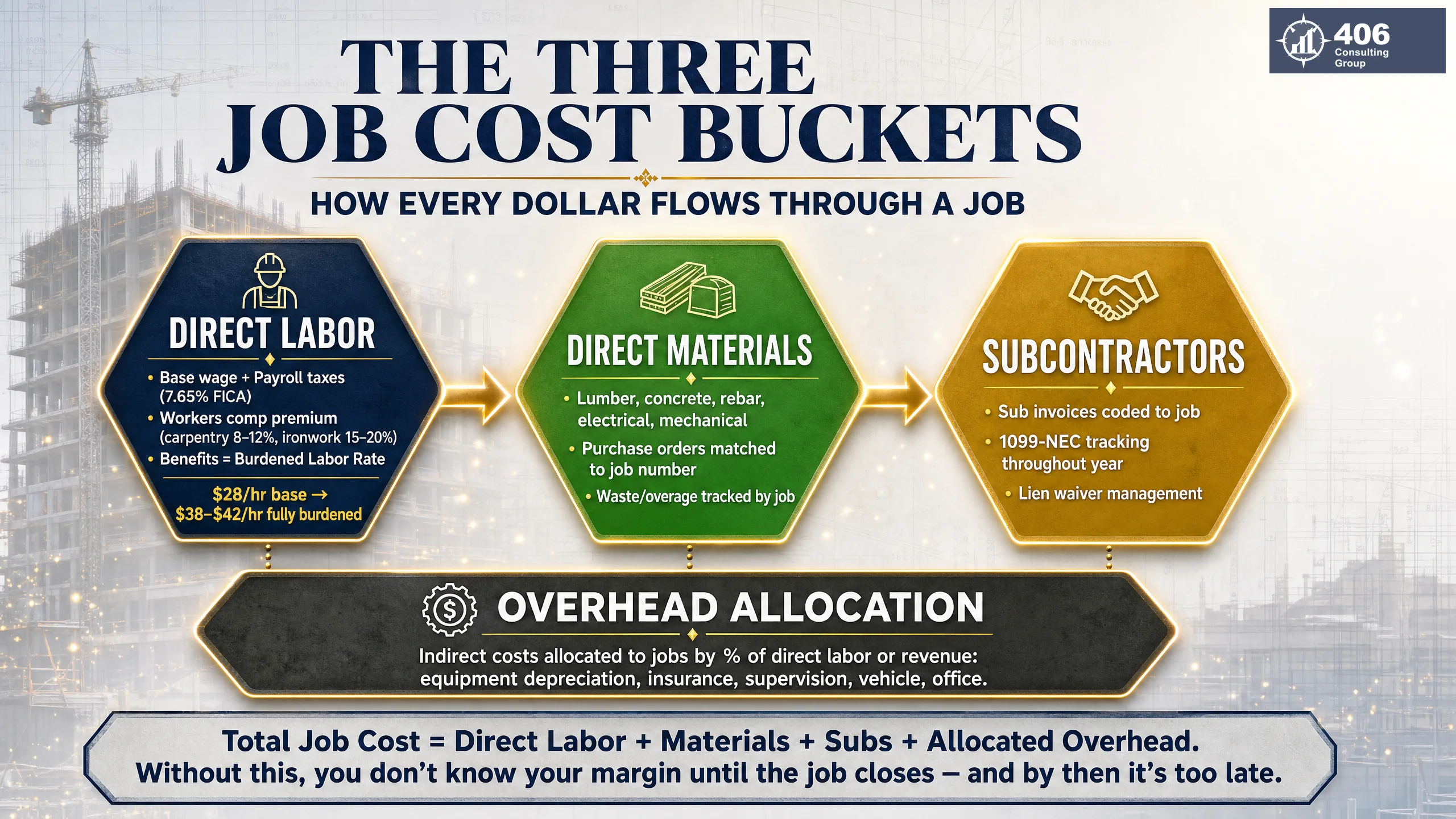

Job Costing Fundamentals: The Three Cost Buckets

Job costing is the practice of assigning every cost incurred on a project to that specific project — not to a general expense pool. The output is a job-level P&L that shows exactly what each job cost and what it returned. Without it, you know your total company margin. You don't know your margin by job — which means you're pricing by instinct, not by data.

Direct Labor

Every hour worked on a job by every employee, coded to that job at the time the work is performed — not at month-end from memory. Labor must be tracked at the burdened rate, not just base pay.

A job budgeted at $28/hour base cost is actually consuming $36–$42/hour. The difference — $8–$14/hour per employee — is the margin you lose when you don't burden your labor rates.

Direct Materials

Every material purchase, rental, and supply tied to a specific job via purchase order. The PO number should reference the job number — so the invoice, when it arrives, flows directly to the correct job cost without manual re-coding.

The most common material tracking failure: purchasing materials for multiple jobs in a single order without splitting the PO by job. The entire order lands in one job or in overhead.

Subcontractors

Every subcontractor invoice coded to the job it was performed on. Sub invoices must be reviewed against lien waivers before payment — and 1099-NEC information captured at time of payment, not in January.

Billings contractors with 10+ active subcontractors on a project cannot manage sub costs in a spreadsheet. Each sub payment must flow through job costing software.

Overhead Allocation — The Fourth Element

Indirect costs — equipment depreciation, company vehicles, office rent, insurance, supervision salary — must be allocated to jobs or your job P&Ls overstate margin. Common allocation methods:

% of direct labor

Most common for labor-heavy contractors (carpentry, electrical)

If overhead is 25% of direct labor, a job with $100K direct labor absorbs $25K overhead

% of revenue

Works for contractors with consistent labor/material mix

8% overhead rate applied to each job's contract value

Direct allocation

Best for equipment-intensive contractors

Equipment hours × hourly rate assigned directly to job

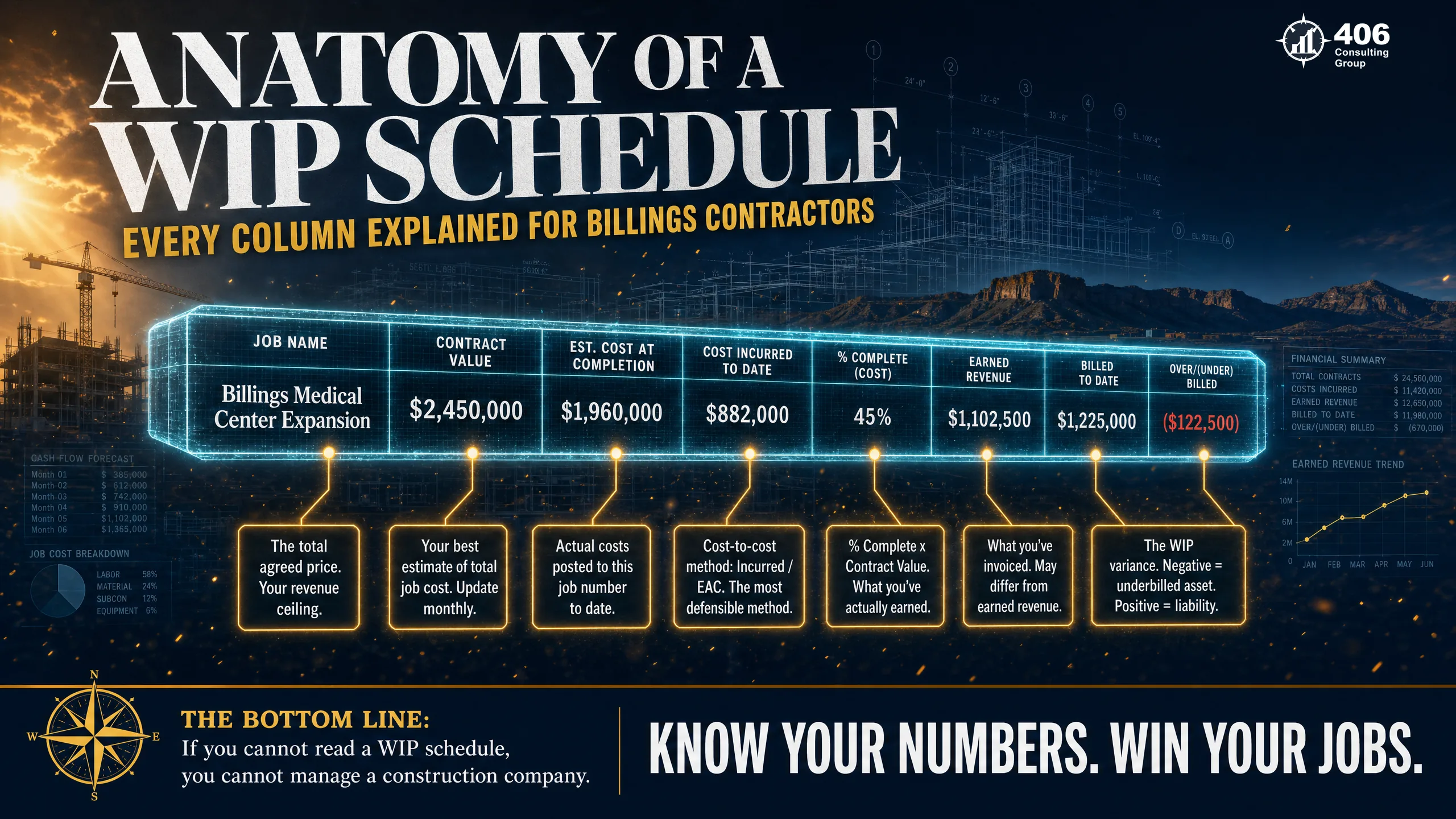

Building a WIP Schedule: Anatomy of the Document

A WIP schedule is a spreadsheet or report produced monthly that shows every active job, its financial status, and whether you've billed ahead of or behind work completed. It is the single most important financial document a contractor produces — more useful month-to-month than your P&L, and the first thing a bonding underwriter requests.

| Job Name | Contract Value | Est. Cost | % Complete | Revenue Earned | Billed to Date | Over/(Under) |

|---|---|---|---|---|---|---|

| I-90 Frontage Build | $780,000 | $610,000 | 91% | $709,800 | $702,000 | ($7,800) |

| Yellowstone Co. Warehouse | $1,240,000 | $940,000 | 38% | $471,200 | $620,000 | $148,800 |

| Billings Office Renovation | $485,000 | $362,000 | 72% | $349,200 | $310,000 | ($39,200) |

| Heights Medical Fit-Out | $920,000 | $705,000 | 15% | $138,000 | $145,000 | $7,000 |

| TOTALS | $3,425,000 | $2,617,000 | — | $1,668,200 | $1,777,000 | $108,800 over |

% Complete (cost-to-cost method)

Calculated as: costs incurred to date ÷ total estimated cost. If a job has $281,000 in costs incurred against a $705,000 estimate, it is 39.9% complete. This is the most reliable method because it ties to actual cost data — unlike units-complete methods that require physical measurement.

Revenue Earned

Contract value × % complete. This is the revenue you should have recognized, regardless of what you've billed. On the I-90 job at 91% complete: $780,000 × 0.91 = $709,800 earned. If you've only billed $702,000, you have a $7,800 underbilled balance.

Over/(Under) — the most important column

Billed to date minus revenue earned. A positive number means overbilled (Billings in Excess of Costs — a liability). A negative number means underbilled (Costs in Excess of Billings — an asset). On this schedule, the Yellowstone Warehouse job has a $148,800 overbilling that must be recognized as a liability.

The Retainage Problem Most Billings Contractors Don't Catch

Retainage is the percentage of each progress billing withheld by the owner or general contractor until project completion — typically 5% to 10% of contract value. It is not a deduction. It is a receivable you have earned but have not yet collected. And for most Billings contractors, it is invisible on their balance sheet.

The Retainage Calculation — A Billings Contractor Example

4 Active Jobs

What happens when this isn't tracked:

- Balance sheet understates accounts receivable by $128,400

- Working capital calculation is $128,400 lower than reality

- Bonding underwriter sees a weaker financial position than exists

- Bank loan capacity is reduced — $128K missing from collateral pool

- Year-end tax position may be incorrect if retainage is recognized on wrong basis

- Collections risk: retainage not tracked is retainage not chased at job close

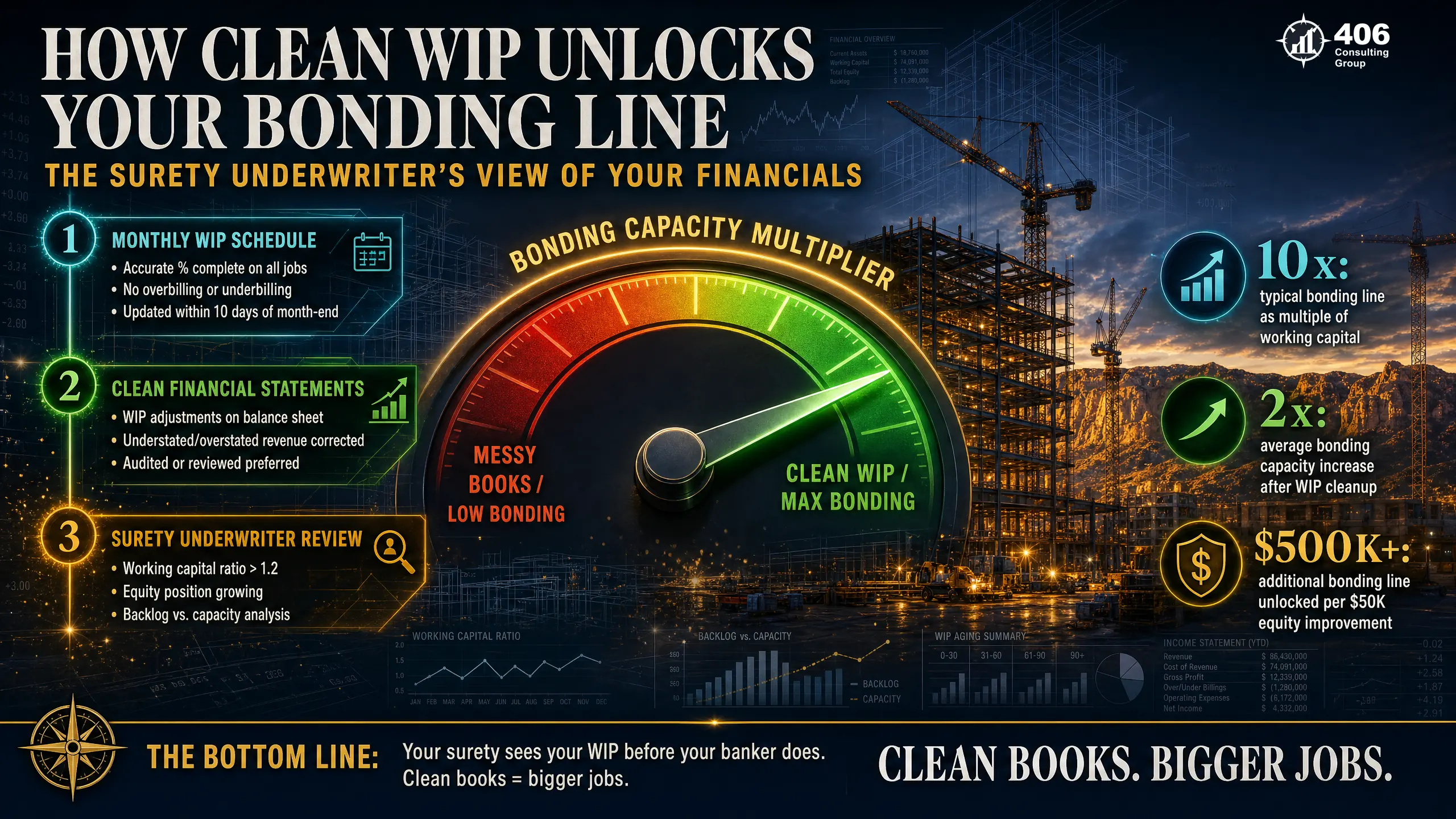

WIP and Bonding Capacity in Montana: What Surety Underwriters Actually Read

Your bonding company — whether Travelers, Merchants Bonding, Western Surety, or a regional carrier — sets your single project limit and aggregate limit based on a financial analysis of your business. The WIP schedule is not an attachment to that analysis. It is the centerpiece of it.

Working Capital

Primary factorCurrent assets minus current liabilities. For contractors, this must include retainage receivable (if properly tracked) and costs in excess of billings (underbilled jobs). A WIP schedule that accurately captures underbilled balances adds real dollars to your working capital — increasing your bonding capacity directly.

Equity / Net Worth

Trend matters as much as levelUnderwriters want to see equity growing year-over-year. A contractor with $2M equity growing 15% annually tells a different story than one with $2M equity flat for three years. Retained earnings from accurately reported jobs — not inflated by overbilling — build genuine equity.

Backlog vs. Capacity

Forward-looking indicatorTotal uncompleted work under contract compared to demonstrated throughput (what you've completed in the last 12 months). A WIP schedule provides both numbers. Underwriters want backlog at roughly 6–18 months of capacity — too little signals instability, too much signals overextension.

WIP Schedule Quality

Trust indicator — affects everything elseA WIP schedule that reconciles to your financial statements tells the underwriter your financials are reliable. A WIP schedule with unexplained variances, missing jobs, or totals that don't tie to your balance sheet tells them nothing in your package can be trusted — and they price that uncertainty into a lower limit.

WIP and Commercial Lending in Billings: What Your Banker Sees

First Interstate Bank, Stockman Bank, and Glacier Bank all have commercial lending departments that regularly underwrite contractor lines of credit, equipment financing, and term loans. Their underwriters and your surety underwriter are reading the same documents — with different questions.

Surety Underwriter

Can this contractor complete the work they're bonded for?

- 1WIP schedule — job-by-job health

- 2Working capital (including retainage + costs in excess)

- 3Backlog vs. completed revenue ratio

- 4Equity growth trend year-over-year

- 5Largest single job as % of equity

Bank Underwriter

Can this contractor service the debt we're extending?

- 1DSCR (net income + depreciation / annual debt service)

- 2Working capital ratio (must exceed 1.2x)

- 3Retainage receivable as collateral

- 4Overbilling as a liability (reduces equity in their model)

- 5Consistency of revenue and margin over 2–3 years

The DSCR calculation for contractors — simplified:

An overbilled WIP schedule inflates current-period income — which inflates DSCR temporarily — and then deflates it when the overbilling catches up. Banks that have seen this pattern get suspicious of contractor financials that show perfect DSCR for 18 months and then a sudden dip.

Montana Contractor Compliance: What Billings Contractors Must Track

Montana has specific contractor compliance requirements that sit on top of federal obligations. Most of them feed directly into your job costing system — which means a bad cost capture process creates compliance exposure, not just financial confusion.

Montana Prevailing Wage

Montana prevailing wage rates are set by the Dept. of Labor and Industry by trade and by county. Billings (Yellowstone County) rates apply on all public contracts. Rates must be posted at job sites and certified payroll submitted weekly. Violations carry per-day-per-violation penalties and can result in debarment from public contracts.

Certified Payroll (Davis-Bacon / Montana PWA)

Weekly certified payroll reports must list every worker by name, trade classification, hours worked, hourly rate paid vs. prevailing wage required, and deductions. Your job costing system must code labor by trade classification — not just by employee name — to produce certified payroll without manual reconstruction.

Montana State Fund — Workers Compensation

Montana State Fund premiums are calculated on payroll by trade classification. Carpentry: approximately $8–$12 per $100 of payroll. Ironwork/structural steel: $15–$20 per $100. Annual audits compare actual payroll to estimated payroll — misclassified workers (e.g., a roofer coded as a laborer) create retroactive premium bills. Job costing systems that capture labor by classification solve this.

Montana UI Quarterly Wage Reports

Quarterly wage reports due the last day of April, July, October, and January. Contributions calculated on first $43,000 of wages per employee (2024). New employer rate: 1.0%. Your job costing labor data must reconcile to the quarterly wage report — discrepancies trigger Department of Labor audits.

1099-NEC — All Subcontractors $600+

Every subcontractor, owner-operator, and non-employee paid $600 or more must receive a 1099-NEC by January 31. Your job costing system should capture EIN, legal name, and address at the time of the first payment — not in January from a stack of invoices. Montana requires copies of 1099s for contractors with Montana withholding.

Montana Contractor Registration

Montana requires all contractors to maintain active registration with the Dept. of Labor and Industry. Registration must be renewed annually. Lapsed registration is a compliance failure on public contracts and can void your bonding relationship with some carriers.

Software for Job Costing: What Actually Works for Montana Contractors

The software you use for job costing determines what data you can produce and how quickly. Not every platform handles contractor-specific needs equally — and the Billings market has strong preferences built on real experience.

| Feature | QB Desktop | QB Online | Sage 100 | Foundation |

|---|---|---|---|---|

| Job cost tracking | ● | ◐ | ● | ● |

| WIP schedule generation | ◐ | ✗ | ● | ● |

| Certified payroll reports | ✗ | ✗ | ● | ● |

| Retainage tracking | ◐ | ◐ | ● | ● |

| Equipment cost allocation | ◐ | ✗ | ● | ● |

| 1099-NEC tracking | ● | ● | ● | ● |

| Montana State Fund integration | ✗ | ✗ | ◐ | ◐ |

| Multi-job dashboard | ◐ | ◐ | ● | ● |

| Annual cost | $599/yr | $85–$200/mo | $200–$500/mo | $300–$800/mo |

| Best for | GCs under $5M | Simple subs | $5M–$20M GCs | Specialty + union |

QuickBooks Desktop sunset warning

Intuit has been actively discontinuing QuickBooks Desktop versions and is pushing all users toward QuickBooks Online. Most Billings contractors still rely on Desktop for its superior job costing. Plan your migration path now — QuickBooks Online's job costing limitations mean many contractors will need to move to Sage or Foundation rather than QBO.

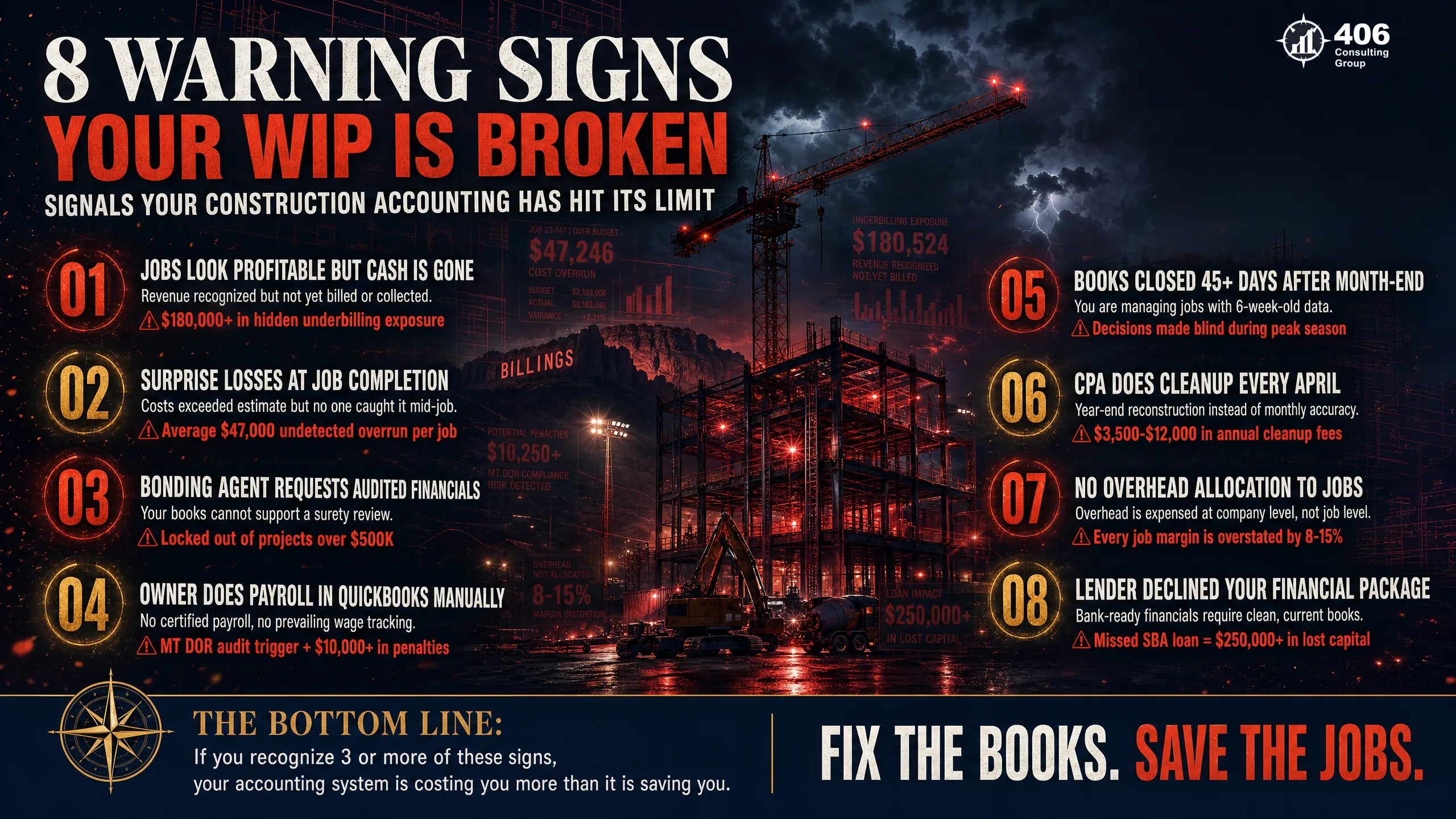

Warning Signs Your Job Costing System Has Failed

These eight warning signs indicate that your current job costing setup — regardless of what software you're using or who is managing your books — is not producing reliable data.

Jobs always look profitable mid-project, then close in losses

Classic overbilling signature. You've billed ahead of work completed throughout the job. Revenue looked strong in progress billings. When work catches up to billings in the final phase, gross profit collapses.

Your bank balance and P&L tell different stories

Cash and accrual divergence without a WIP schedule to explain it. Either you're collecting faster than you're earning (overbilling) or earning faster than you're collecting (underbilling) — and you don't know which.

No monthly WIP review meeting

A WIP schedule produced but never reviewed is a compliance document, not a management tool. The meeting — owner, project managers, bookkeeper — is where overbilled jobs get identified and billing schedules adjusted.

Retainage doesn't appear on your balance sheet

On $3M active backlog with 5–10% retainage, you have $90K–$180K in earned, uncollected receivables your banker and bonding agent can't see. This alone can reduce your bonding capacity by $900K–$1.8M.

Overhead isn't allocated to job costs

Every job P&L overstates margin. You're pricing jobs based on direct costs only, which means your bids consistently recover direct cost but don't fully recover overhead — and your company loses money at scale even when individual jobs look profitable.

Subcontractor payments aren't coded to a job

You can't calculate job-level margin without knowing what each sub was paid on each job. Sub costs in a general expense account are invisible to job costing.

Your bonding agent asked you to explain your financials

Surety underwriters don't ask when they're confident. A request for explanation is a signal that your WIP schedule didn't reconcile, your overbilling ratio is high, or your financials told a story the underwriter can't validate.

Large tax bill despite a 'good year'

Your estimated tax payments were based on inaccurate monthly books. Accurate WIP-based financials produce accurate quarterly estimates — which spread your tax liability across the year instead of delivering a single April surprise.

Common Mistakes Billings Contractors Make

Lumping all job costs into one GL account

Every job needs its own cost tracking. 'Job Expenses' as a single line item is the most common job costing failure — it produces a total spend figure with no visibility by job.

Using invoice date instead of % complete for revenue recognition

Revenue on a construction contract is earned as work is completed, not when an invoice is issued. Billing date and revenue recognition date are not the same thing.

Not tracking change orders as contract modifications

Every approved change order increases the contract value and the estimated cost. Failing to update the WIP schedule for change orders understates revenue earned and distorts % complete.

Owner's time not burdened into job cost

When the owner works on jobs, that time has a cost. An owner billing $120/hour to clients but not costing their own time to jobs makes every job look more profitable than it is.

Equipment costs not allocated by job

Company equipment used on multiple jobs must be allocated by job based on hours or days used. Equipment sitting in an overhead pool doesn't tell you which jobs are consuming it.

WIP schedule produced only at year-end

A year-end WIP schedule is a compliance document for your CPA. A monthly WIP schedule is a management tool. Only one of those prevents problems — the other documents them after it's too late.

Frequently Asked Questions

How often should I update my WIP schedule?

Monthly, without exception. A WIP schedule updated less frequently than monthly loses its value as a management tool. The whole purpose is to catch jobs trending toward a loss before they close — which requires current data. Most Billings contractors produce their WIP schedule within 10 days of month-end, after all labor timesheets and subcontractor invoices for the month have been processed.

Which percentage-complete method should I use — cost-to-cost or units complete?

Cost-to-cost is the standard for most Billings contractors and the one most lenders and bonding companies expect. It calculates % complete as (costs incurred ÷ total estimated cost) × 100. Units-complete (e.g., linear feet of pipe installed vs. total) requires physical measurement and is more accurate for repetitive-unit work like paving or utility installation. For complex GC work, cost-to-cost is more reliable and easier to verify.

How do I handle time-and-materials jobs on a WIP schedule?

T&M jobs are either excluded from the WIP schedule (if they're invoiced as costs are incurred with no contract ceiling) or included with % complete set to match billing-to-contract value if there's a not-to-exceed limit. For T&M jobs with a NTE ceiling, treat them like a fixed-price contract once you approach 80% of the ceiling — cost overrun risk materializes at that point.

When do I need a controller vs. a bookkeeper for my contracting business?

A bookkeeper handles transaction entry, reconciliation, and basic reporting. A controller builds and maintains your job costing system, produces the monthly WIP schedule, reviews job-level P&Ls for anomalies, and connects your financial data to your bonding and banking relationships. Most Billings contractors need controller-level oversight once they cross $3M in annual revenue, have 3+ simultaneous jobs, or have employees requiring certified payroll. Below that threshold, a strong bookkeeper with contractor experience and a monthly review from an accountant often covers the gap.

What do bonding underwriters actually want to see in a WIP schedule?

Specifically: (1) Every active job listed individually — no bundling of small jobs; (2) Estimated cost revised when scope changes — not locked at original bid; (3) Totals that reconcile to the balance sheet — costs in excess of billings matches the asset line, billings in excess matches the liability line; (4) Retainage shown separately from regular AR; (5) The schedule reviewed and signed off by the owner. A WIP schedule that doesn't reconcile to the financial statements tells the underwriter the numbers are unreliable.

How do I set up QuickBooks Desktop for job costing?

The key steps: (1) Enable job costing in Preferences → Jobs & Estimates; (2) Set up each job as a customer:job (e.g., 'Smith Construction: Job 2240'); (3) Create service items that map to your cost codes; (4) Assign job numbers when entering time (weekly timesheets), entering bills (vendor bills by job), and entering purchase orders. The WIP schedule itself must be built outside QuickBooks — QB Desktop generates cost-by-job reports but not a formatted WIP schedule. Most Billings contractors export to Excel for the final WIP document.

How does retainage flow through the WIP schedule?

Retainage is tracked separately from regular billings. In a correctly built WIP schedule, the 'Billed to Date' column shows gross billings including retainage billed but held — and a separate retainage column shows the cumulative amount withheld. The retainage receivable balance on your balance sheet should equal the sum of the retainage column on your WIP schedule. When they don't match, there's an error in one of the two documents.

How do I catch a job going sideways before it closes?

Three signals to watch monthly: (1) Estimated cost creeping up — if the 'revised estimated cost' is increasing each month without a corresponding change order, costs are running over budget; (2) % complete lagging behind billing schedule — you may be overbilling and the job will catch up at the end; (3) Job-level gross margin compressing — if a job that opened at 18% margin is now showing 12% at 60% complete, investigate before the final phase. The monthly WIP review meeting exists to catch these signals before close.

External Resources

Billings, MT

WIP and Job Costing Built for Montana Contractors

406 Consulting Group provides controller-level financial services to Billings contractors — including monthly WIP schedules, job costing setup, bonding package preparation, and financial reporting that satisfies both your surety and your bank.

The Contractor Clarity Stack

Build these layers in order

Job Setup

Before the first PO

Cost Capture

Daily labor + PO + sub invoices

Monthly WIP Schedule

% complete, over/under, retainage

Capital Access

Bonding + bank lending

WIP Quick Reference

Our Services

Montana Compliance Quick Reference

Related Resources