Virtual Tax Preparation Services

for Boise, ID Businesses

Most Boise businesses overpay taxes every year — wrong entity structure, missed deductions, no quarterly planning. Here's what professional virtual tax prep actually delivers.

Boise is one of the fastest-growing business markets in the country. New companies are forming, established businesses are scaling, and the tax complexity that comes with growth — entity elections, Idaho state compliance, quarterly estimated payments, sales tax nexus — is catching a lot of business owners flat-footed. Most of them are still using the same once-a-year, appointment-only tax preparer they started with when the business was a fraction of its current size.

Virtual tax preparation for businesses is not just a convenience — it is a fundamentally better model for business owners who need year-round access, faster turnaround, and a tax advisor who knows their business rather than seeing them once a year. This guide covers how virtual business tax prep works in Idaho, what Idaho-specific tax obligations Boise businesses face, common mistakes that cost Treasure Valley businesses thousands every year, and what to look for when choosing a virtual tax prep provider.

Jason Anderson co-founded 406 Consulting Group after years in small business financial management across Montana and Idaho. The perspective here is practical: not what the tax code says in the abstract, but what it means specifically for a Boise business owner trying to minimize their tax bill and stay in compliance without spending their year dealing with it.

Table of Contents

Why Boise Businesses Are Moving to Virtual Tax Prep

The traditional tax prep model — call in January, get an appointment in March, drop off a shoebox of documents, receive a return in April — was built for W-2 employees, not business owners. Business owners have quarterly deadlines, mid-year entity elections, equipment purchases that need depreciation decisions before December 31, and questions that arise in August, not just April. The once-a-year model fails them at every point where they actually need guidance.

47%

Of Boise small businesses say they overpaid taxes last year due to missed deductions or wrong entity structure

3–4×

Faster document turnaround with virtual tax prep vs. traditional in-person CPA (secure upload vs. mail/drop-off)

Year-round

Access to a tax advisor — not just during filing season — is the defining advantage of virtual tax services

Boise's growth creates new tax complexity every year

New revenue streams, new employees, multi-state sales, equipment purchases, additional locations — each of these creates tax implications that require decisions before year-end, not after. A virtual tax advisor reviews these in real time rather than discovering them the following April when nothing can be done.

The best Idaho tax expertise is not always local

Virtual tax prep allows Boise businesses to access CPAs and EAs with deep Idaho state tax expertise regardless of geography. The best tax advisor for a Boise tech company with R&D credit questions or a construction firm with complex depreciation schedules may not be the nearest office on Google Maps.

Technology has eliminated the need for physical document exchange

Secure client portals, e-signatures, cloud accounting software integrations (QuickBooks Online, Xero), and encrypted file sharing have made the in-person document exchange the least necessary part of the tax prep process. Virtual tax prep uses the same tools, without the geographic constraint.

What Virtual Tax Preparation Actually Covers

Virtual business tax preparation covers the same scope as in-person tax preparation — plus, typically, more proactive year-round advisory that in-person seasonal preparers do not provide. Here is what is included in a full-service virtual business tax engagement, and where the boundaries usually are.

What Virtual Tax Prep Includes

Federal business tax return (Form 1065, 1120-S, 1120, or Schedule C depending on entity)

Idaho state business return (Form 41, 41S, or 65)

Estimated quarterly tax payment calculations (April, June, September, January)

W-2 and 1099 preparation and filing for employees and contractors

Entity structure review and election recommendations

Year-end tax planning — deductions to capture before December 31

Coordination with bookkeeper or accountant for clean close

Response to IRS and Idaho State Tax Commission notices

Amended returns if prior-year errors are discovered

Multi-state filing if business has nexus outside Idaho

What Is Usually Separate

Bookkeeping and monthly transaction categorization — typically a separate controller or bookkeeper engagement

Payroll processing and payroll tax filings (940, 941) — separate payroll service or engagement

Sales tax collection and monthly/quarterly sales tax remittance — often a separate service

Financial statement preparation (monthly P&L, balance sheet) — controller or CFO scope

Business valuation for sale, succession, or financing — separate engagement

Legal entity formation and operating agreement drafting — attorney scope

The overlap to understand: The quality of your tax return is directly determined by the quality of your books. A virtual tax preparer working from clean, accrual-basis financial statements can optimize your return and identify deductions. A preparer working from a bank statement dump in March is doing data entry, not tax strategy. Getting your books right in Boise is the prerequisite for getting your taxes right.

Idaho Business Tax Landscape — What's Different Here

Idaho has a relatively business-friendly tax environment compared to neighboring states — no inventory tax, no gross receipts tax, no estate tax, and no local income taxes. But there are Idaho-specific rules, rates, and credits that a tax preparer who primarily works with Montana or Washington businesses will not know cold. Here is the Idaho tax landscape every Boise business owner needs to understand.

| Tax Type | Rate / Rule | Who It Affects | Key Note |

|---|---|---|---|

| Idaho Individual Income Tax | 5.8% flat rate (2023+) | Sole proprietors, S-Corp shareholders, LLC members, partners | Idaho simplified to flat rate in 2023 — prior graduated rates no longer apply |

| Idaho Corporate Income Tax | 5.8% flat rate | C-Corporations with Idaho nexus | Applied to Idaho apportioned income; Idaho uses a three-factor apportionment formula |

| Idaho Sales Tax | 6% (no local add-on) | Businesses selling taxable goods or digital products in Idaho | Idaho does not allow local sales taxes — 6% statewide. Economic nexus at $100K or 200 transactions |

| Idaho Investment Tax Credit | 3% of qualifying investment | Businesses purchasing qualifying new equipment, machinery, or property in Idaho | Often missed — applies to equipment placed in service in Idaho. Significant for manufacturers and contractors |

| Idaho Payroll Tax (withholding) | Matches individual rates (5.8% flat) | All businesses with Idaho employees | Idaho withholding registration required before first payroll |

| Idaho Unemployment Insurance | 0.207%–5.4% of first $53,500 wages (2024) | Employers with Idaho employees | New employers start at standard rate; rate adjusts based on claims history |

| Property Tax | Varies by county — Boise/Ada County avg ~0.5–0.7% | Business owners of real property in Idaho | Business personal property (equipment) is taxed in Idaho — often overlooked |

Idaho Tax Advantages

- No local income taxes anywhere in the state

- No inventory tax

- No gross receipts tax

- No estate or inheritance tax

- No franchise tax (unlike California, Texas)

- Investment Tax Credit reduces income tax owed dollar-for-dollar

Idaho Tax Traps

- Business personal property tax (equipment) — commonly missed

- Sales tax on digital goods and some SaaS — Idaho law evolving

- Economic nexus for out-of-state sellers — $100K threshold applies

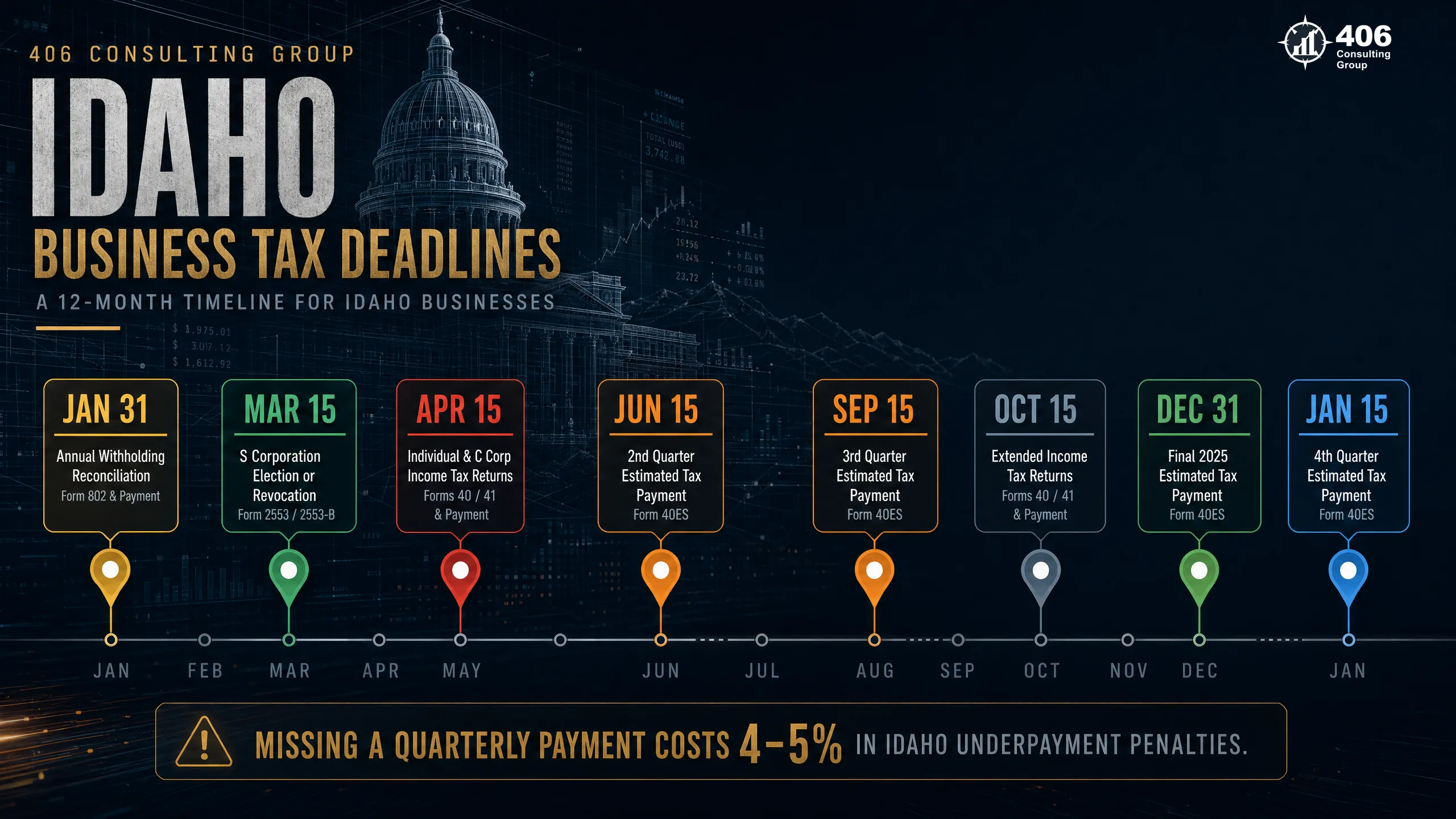

- Late estimated payment penalties — Idaho charges 4–5% underpayment penalty

- Idaho conformity gaps — not all federal elections automatically apply to Idaho return

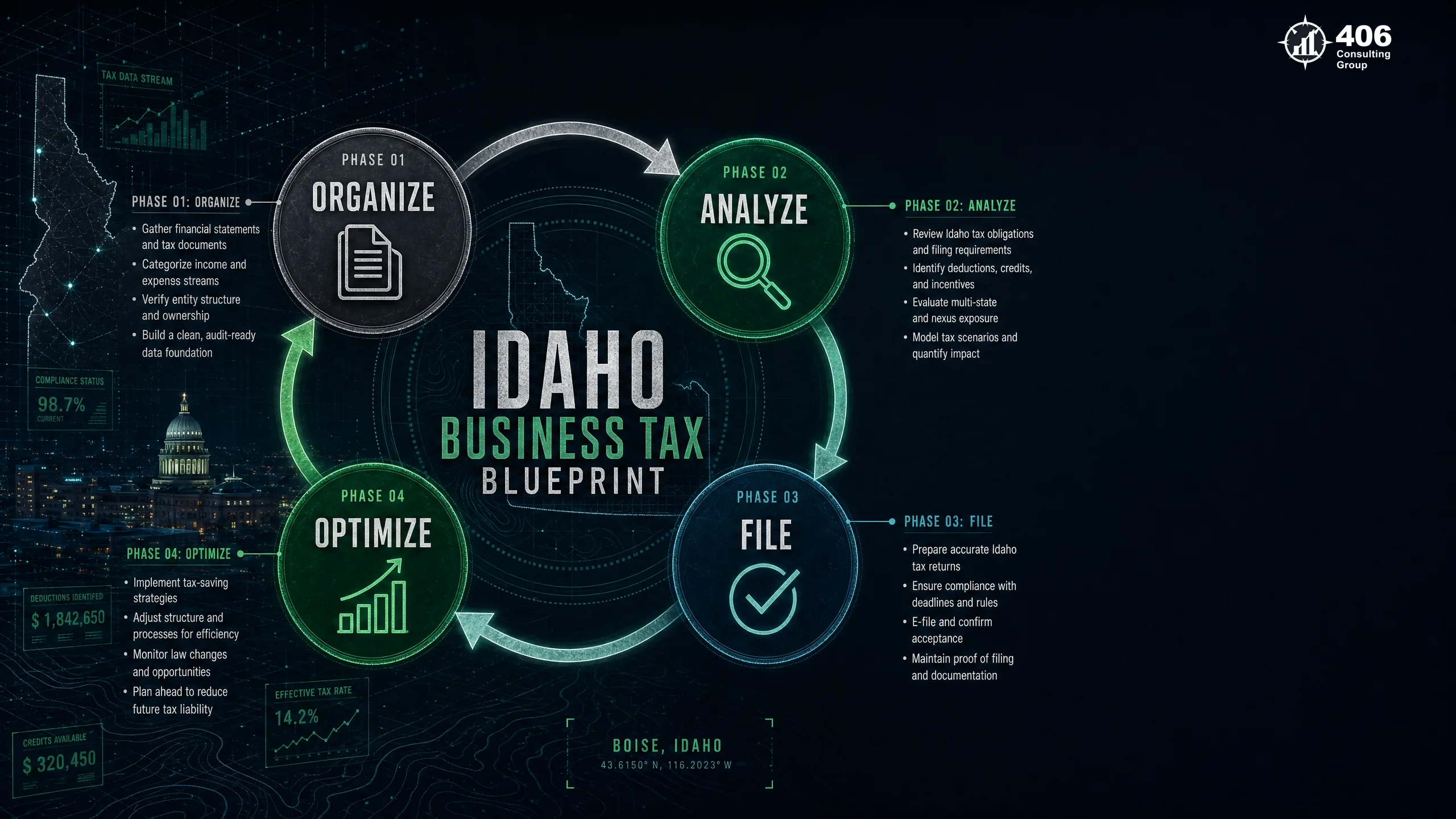

The Idaho Business Tax Blueprint: 4 Phases for Year-Round Tax Management

The Idaho Business Tax Blueprint organizes business tax management into four sequential phases that run across the full calendar year. The goal is to replace the reactive, once-a-year scramble with a proactive system where every decision is made at the right time — not discovered too late to do anything about it.

Phase 1: Organize

January – February- Gather prior year financial statements, bank statements, and receipts

- Reconcile all accounts through December 31

- Identify all 1099-eligible vendors paid $600+ during the year

- Review entity structure — did your income level change enough to reconsider your election?

- Complete tax organizer questionnaire — changes in business, major purchases, new employees, new states

Phase outcome: Clean, complete books ready for accurate return preparation. No surprises in Phase 2.

Phase 2: Analyze

February – March- Identify all available deductions: home office, vehicle, retirement contributions, equipment

- Calculate Idaho Investment Tax Credit on qualifying equipment placed in service

- Review estimated payments made — are you over or underpaid going into April?

- Model the impact of any entity election changes (S-Corp vs. LLC) for the following year

- Identify any Idaho-specific elections or adjustments not automatically tied to federal return

Phase outcome: Maximum defensible deductions identified. Return ready to file or extend with confidence.

Phase 3: File

March – April (or October if extended)- File federal return (or extension) by deadline: March 15 for S-Corps/partnerships, April 15 for C-Corps/sole props

- File Idaho state return simultaneously with federal

- Make Q1 estimated payment by April 15

- If extending, calculate safe harbor payment to avoid underpayment penalty

- File any required 1099s and W-2s (January 31 deadline — done in Phase 1)

Phase outcome: Returns filed, payments made, compliance confirmed for the prior tax year.

Phase 4: Optimize

May – December- Q2 estimated payment — June 15

- Mid-year financial review — track actual income vs. projection

- Q3 estimated payment — September 15

- Year-end planning session (October/November) — accelerate deductions, defer income, plan equipment purchases

- Q4 estimated payment — January 15 of following year

- Retirement contribution decisions — SEP-IRA, Solo 401(k), SIMPLE IRA contributions for the year

Phase outcome: Tax bill minimized through proactive decisions made throughout the year — not discovered in April.

Entity Structure & Idaho Tax Implications

The entity structure question is the highest-leverage tax decision most Boise business owners make — and most make it once at formation and never revisit it. The right structure depends on your net profit level, your personal income tax situation, your plans for the business, and Idaho-specific rules. Here is how each structure works in Idaho.

Sole Proprietorship / Single-Member LLC (Default)

Federal treatment

Schedule C — all net profit subject to self-employment tax (15.3% on first $168,600 in 2024, 2.9% above)

Idaho treatment

Idaho Form 40 — net profit flows to personal return at 5.8% flat rate

Best for: Net profit under $60,000/year. Simple structure, minimal compliance cost.

Watch: Self-employment tax is the hidden cost. At $100K net profit, SE tax alone is over $14,000 — on top of income tax. Most sole props earning above $80K should model an S-Corp election.

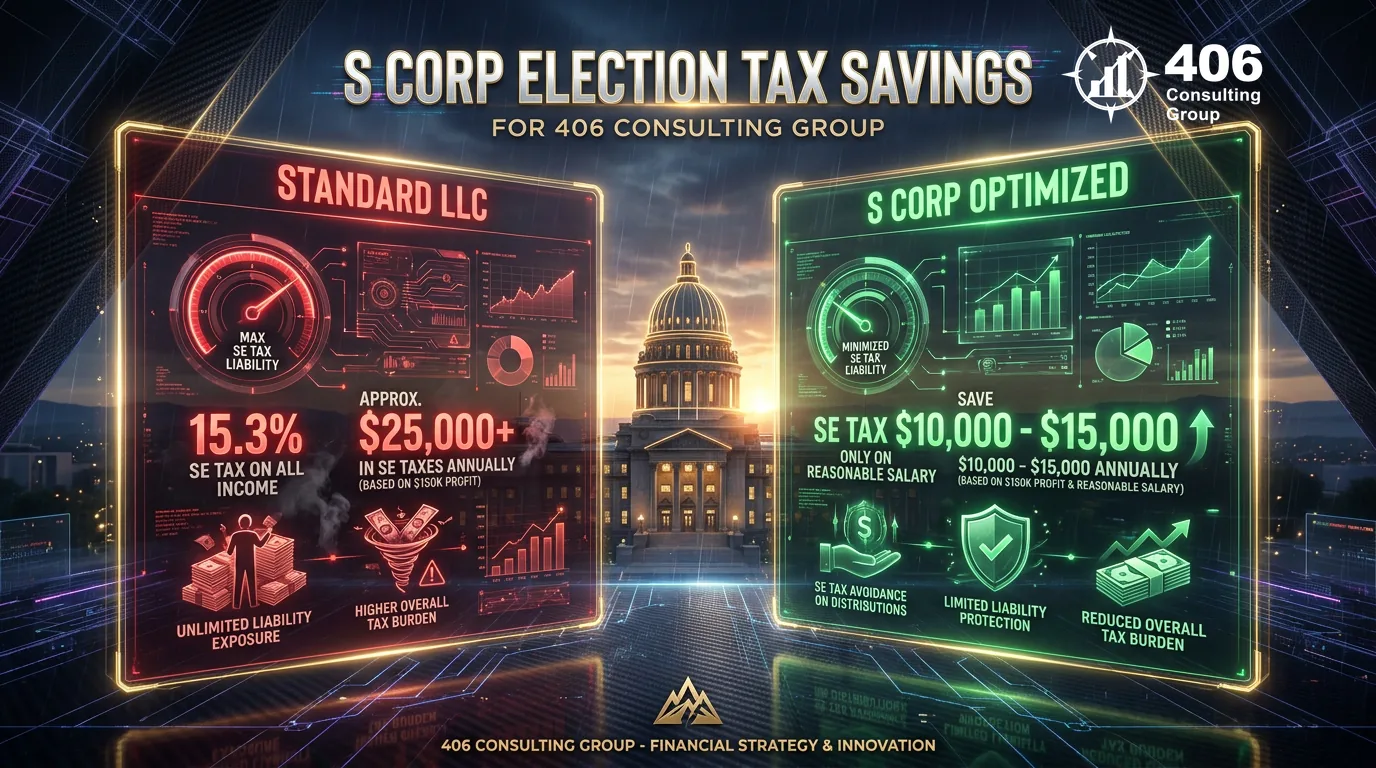

S-Corporation (Most Common Election for Boise Small Businesses)

Federal treatment

Form 1120-S — profit split between reasonable salary (subject to payroll tax) and distributions (not subject to SE tax). Filed March 15.

Idaho treatment

Idaho Form 41S — Idaho follows federal S-Corp treatment. Idaho requires S-Corp election to be made on Idaho return as well.

Best for: Net profit consistently above $80,000–$100,000/year. The SE tax savings on distributions typically exceed S-Corp compliance costs at this level.

Watch: IRS requires a 'reasonable salary' for owner-employees. Underpaying yourself to avoid payroll taxes is an audit trigger. The salary must reflect what you would pay a third party to do your job.

C-Corporation

Federal treatment

Form 1120 — corporate income taxed at 21% federal corporate rate. Dividends paid to shareholders taxed again at qualified dividend rates (15–20%). Filed April 15.

Idaho treatment

Idaho Form 41 — Idaho corporate income tax at 5.8% on Idaho apportioned income.

Best for: Businesses planning to retain earnings for growth rather than distribute them, or businesses pursuing venture capital funding (VCs typically require C-Corp structure). Also beneficial for certain Qualified Small Business Stock (Section 1202) planning.

Watch: Double taxation on distributed profits makes C-Corps generally less efficient for small businesses that plan to take money out of the company. Rarely the right choice for a Boise owner-operated business below $2M revenue.

Multi-Member LLC (Partnership)

Federal treatment

Form 1065 — pass-through to partners on Schedule K-1. General partners pay SE tax on their distributive share. Filed March 15.

Idaho treatment

Idaho Form 65 — Idaho pass-through treatment follows federal. Partners report Idaho share of income on personal return.

Best for: Businesses with multiple owners who want flexible profit allocation and do not want the formality of a corporation. Common for real estate partnerships and professional practices.

Watch: General partners in a partnership pay SE tax on their full distributive share of income — same problem as sole proprietorship at scale. Limited partners do not pay SE tax, but the rules around limited partner status are complex and audit-sensitive.

The S-Corp election timing rule: To be taxed as an S-Corp for a given tax year, the election must be filed by March 15 of that year (for existing entities) or within 75 days of formation (for new entities). Missing this window means waiting another year. A virtual tax advisor who reviews your entity structure in Q1 — not in April — gives you time to act.

Idaho Sales Tax & Nexus for Growing Boise Businesses

Idaho's sales tax is 6%, applied statewide with no local add-ons — simpler than many states. But as Boise businesses grow — adding e-commerce revenue, selling into other states, or providing services to customers outside Idaho — the nexus question becomes significantly more complex.

What Idaho Taxes (Taxable)

•Tangible personal property sold at retail

•Digital goods delivered electronically (Idaho has expanded digital goods taxability)

•Pre-written software (including SaaS in some interpretations)

•Lodging (short-term rentals are taxable)

•Admissions to events and entertainment

•Some services when sold with tangible goods

What Idaho Exempts (Not Taxable)

•Manufacturing equipment and machinery used in production

•Agricultural equipment and supplies

•Raw materials incorporated into finished products

•Most professional services (accounting, legal, medical)

•Prescription drugs and some medical devices

•Sales for resale (wholesale with valid resale certificate)

Economic Nexus: When You Owe Tax in States You've Never Set Foot In

Following the South Dakota v. Wayfair Supreme Court decision, states can require remote sellers to collect sales tax based on economic activity alone — no physical presence required. For Boise businesses selling products or taxable services to customers in other states:

Idaho (home state)

Register immediately upon starting sales; no threshold exemption for in-state sellers

Collect 6% on all taxable sales

Most US States

$100,000 in sales OR 200 transactions into the state in the current or prior calendar year

Register, collect, and remit once threshold is crossed

Washington (common for Boise)

$100,000 in Washington sales; Washington also taxes services more broadly than Idaho

Register with WA DOR; B&O tax also applies

Common Tax Mistakes Boise Businesses Make — And What They Cost

Most of the tax dollars Boise businesses unnecessarily send to the IRS and Idaho State Tax Commission are not lost to complexity — they are lost to missed deductions, wrong timing, and outdated structure decisions. Here are the most common and most costly mistakes, with the actual dollar impact at typical Boise business income levels.

Staying a sole prop or single-member LLC past $80K net profit

Typical cost: $8,000–$22,000/year in excess self-employment tax

Fix: Model the S-Corp election. At $150K net profit with a $90K salary, an S-Corp saves ~$9,000/year in SE tax after accounting for payroll processing costs.

Not making quarterly estimated payments — or underpaying them

Typical cost: $500–$3,000/year in IRS and Idaho underpayment penalties, plus a surprise April tax bill

Fix: Calculate quarterly payments based on prior-year safe harbor (110% of prior year liability) or 90% of current-year estimated liability — whichever is smaller.

Missing the Idaho Investment Tax Credit

Typical cost: 3% credit on qualifying equipment — missed by most Boise businesses that purchase equipment

Fix: Any equipment, machinery, or property purchased and placed in service in Idaho may qualify. A $50,000 equipment purchase = $1,500 direct tax credit.

Misclassifying employees as 1099 contractors

Typical cost: Back payroll taxes, penalties, and interest — potentially $10,000–$50,000+ on IRS audit

Fix: The IRS uses a multi-factor behavioral and financial control test. If you control how the work is done, not just the result, the worker is likely an employee.

Not deducting the home office

Typical cost: $1,500–$4,000/year in missed deductions for qualifying home-based business owners

Fix: The space must be used regularly and exclusively for business. Calculate using the simplified method ($5/sq ft, max 300 sq ft) or the actual expense method (pro-rated home costs).

Missing retirement contribution deductions

Typical cost: $5,000–$30,000/year in taxable income that could be sheltered in a SEP-IRA or Solo 401(k)

Fix: SEP-IRA: up to 25% of net self-employment income, max $69,000 (2024). Solo 401(k): up to $69,000 employee + employer contributions. Both reduce federal and Idaho income tax.

Not tracking vehicle mileage for business use

Typical cost: $1,000–$5,000/year in missed vehicle deductions for business owners who drive for work

Fix: Standard mileage rate (67 cents/mile in 2024) or actual expense method. A mileage tracking app makes this effortless; without records, the deduction is disallowed on audit.

Skipping year-end planning — all tax decisions made after December 31

Typical cost: Most tax-reduction strategies (retirement contributions, equipment purchases, entity elections) require action BEFORE year-end. Post-December options are nearly zero.

Fix: A year-end planning call in October or November identifies actions still available: accelerating deductible expenses, deferring invoices, purchasing needed equipment, funding retirement accounts.

The Virtual Tax Prep Process — What to Expect Step by Step

For business owners who have never worked with a virtual tax preparer, the process is straightforward — and in many ways more efficient than the in-person alternative. Here is what a full engagement looks like from first contact through filing.

Step 1 — Initial Consultation

30–60 min video callA 30–60 minute video call to review your business structure, prior tax history, and current situation. The advisor identifies immediate issues (wrong entity structure, underpayment exposure, missed credits) and scopes the engagement. This call sets the relationship and the strategy — not just the transaction.

Step 2 — Secure Document Collection

Your time: 2–4 hoursYou receive access to a secure client portal (not email attachments). Upload prior year returns, current year financial statements, bank statements, any 1099s received, and supporting documentation for deductions (mileage logs, home office measurements, equipment receipts). A structured tax organizer guides what is needed.

Step 3 — Return Preparation

Preparer works 5–15 business daysThe preparer works from your documents to prepare the federal and Idaho state returns. If the books need cleanup before the return can be prepared, that is identified here — either handled in-house or referred to a bookkeeper. This phase includes all deduction identification, credit calculations, and entity optimization.

Step 4 — Review Call

30–45 min video callA scheduled video call to walk through the completed draft return: what drove the result, any deductions that required judgment calls, any positions that carry audit risk, and what to expect going forward. This call is where questions get answered — not after filing.

Step 5 — E-Signatures and Filing

Your time: 10 minutesYou sign Form 8879 (IRS e-file authorization) and the Idaho equivalent electronically. The preparer files both returns and provides confirmation of acceptance from the IRS and Idaho State Tax Commission. You receive copies of all filed returns through the secure portal.

Step 6 — Post-Filing Debrief and Year-Ahead Setup

30 min — begins the ongoing relationshipA brief planning conversation: what is your estimated tax liability for the current year, what quarterly payments should you make, are there any entity or strategy changes to implement before next filing. This is Phase 4 of the Idaho Business Tax Blueprint — the step that makes next year better than this year.

What to Look for in a Virtual Tax Preparer for Your Boise Business

CPA or Enrolled Agent (EA) credential

Only CPAs, EAs, and attorneys are authorized to represent clients before the IRS in an audit. An unlicensed preparer cannot accompany you if the IRS questions your return. Verify the credential — both CPA and EA licenses are publicly searchable (Idaho State Board of Accountancy for CPAs; IRS for EAs).

Idaho state tax experience — not just federal

Federal tax law is the same nationwide. Idaho state tax law is not. Idaho-specific elections, the Investment Tax Credit, Idaho's conformity gaps from federal law, and Idaho's apportionment rules for multi-state businesses — these require Idaho-specific expertise. Ask directly: how many Idaho business returns do you prepare annually?

Year-round availability and communication

A preparer who is unreachable from May through December is not a tax advisor — they are a tax preparer. Year-round availability for questions about equipment purchases, estimated payments, entity elections, and financial decisions is the primary advantage of a virtual engagement over a seasonal-only CPA.

Industry experience in your specific sector

A construction company's tax return (cash vs. completed contract method, per-diem rules, equipment depreciation, bonding considerations) is materially different from a technology company's return (R&D credits, stock compensation, software capitalization). Ask whether the preparer has clients in your industry.

Flat fee pricing (not hourly)

Hourly billing for tax preparation creates an incentive to ask fewer questions, because every question costs you money. Flat fee pricing aligns the preparer's incentive with thoroughness — they get the same fee whether the return takes 8 hours or 12. Ask for a flat fee proposal at engagement start.

Secure technology — not email attachments

Financial documents sent as email attachments are not secure. A professional virtual tax practice uses an encrypted client portal for document exchange and e-signatures. If a prospective preparer asks you to email your tax documents, that is a red flag about their operational sophistication.

Year-Round Tax Strategy vs. Once-a-Year Filing

The difference between a business owner who pays the minimum required taxes and one who pays 20–30% more than necessary is not intelligence or aggressiveness — it is timing. Nearly every tax reduction strategy requires action before December 31. A preparer you only talk to in March cannot help you with decisions that had to be made in November.

| Quarter | Key Deadline | Tax Actions | Missed = Lost |

|---|---|---|---|

| Q1 Jan–Mar | March 15 (S-Corp/Partnership), April 15 (all others) | Prior-year return filed. Entity structure reviewed. S-Corp election window open until March 15. | S-Corp election for the current year — must be filed March 15 or within 75 days of formation |

| Q2 Apr–Jun | June 15 — Q2 estimated payment | Q1 actual vs. projection compared. Mid-year deduction strategy adjusted. Equipment purchase timing evaluated. | Q2 estimated payment → underpayment penalty accumulates from June 15 forward |

| Q3 Jul–Sep | September 15 — Q3 estimated payment | Year-end projection modeled. Retirement contribution strategy confirmed. Major purchases evaluated for Section 179. | Q3 estimated payment; window to restructure large Q4 purchases shrinks |

| Q4 Oct–Dec | December 31 — hard cutoff for most deductions | Accelerate deductible expenses. Defer invoices if income is too high. Fund SEP-IRA or Solo 401(k). Buy needed equipment (Section 179 requires placed in service by Dec 31). | Retirement contributions (SEP-IRA deadline is actually April 15 following year; Solo 401(k) employee contributions must be made by Dec 31); equipment Section 179; most expense timing decisions |

Industry-Specific Tax Considerations for Boise Businesses

Boise's economy spans technology, construction, healthcare, retail, and professional services — and each industry has tax rules that don't apply to others. A generalist tax preparer files what is in front of them. An industry-experienced preparer knows what questions to ask and what credits and elections exist in your specific sector.

Technology & Software

R&D Tax Credit (Section 41)

Qualifying research activities — software development, product prototyping, process improvement — generate a dollar-for-dollar federal tax credit. Often unclaimed by Boise tech firms because it is perceived as only for large companies.

Software Development Capitalization

Section 174 changes (2022) now require R&D costs to be amortized over 5 years (domestic) rather than immediately expensed. This significantly affects cash flow and tax timing for Boise software companies.

Stock-Based Compensation

ISOs and NSOs have very different tax treatment — at grant, exercise, and sale. A tech company issuing equity to employees needs a preparer who understands AMT implications and 83(b) elections.

Construction & Contractors

Accounting Method Elections

The percentage-of-completion method vs. completed contract method affects when income is recognized. For long-term contracts, the election can defer tax on income from contracts that span year-end — a material planning tool for Boise contractors.

Section 179 and Bonus Depreciation

Equipment purchases (excavators, trucks, tools, trailers) qualify for immediate expensing under Section 179 (up to $2.5M, indexed to approximately $2.56M for 2026 under OBBBA) or 100% bonus depreciation (permanently restored under the One Big Beautiful Bill Act, July 2025). Combined with the Idaho Investment Tax Credit, equipment purchases carry significant tax benefit.

Per-Diem Deductions for Travel

Contractors working away from their tax home can deduct per-diem lodging and meal expenses. The IRS per-diem rates for Boise and Idaho construction sites are published annually — using the actual rate table is significantly more accurate than estimating.

Healthcare & Medical Practices

Qualified Business Income (QBI) Deduction

Medical practices (other than specified service trades above income thresholds) may qualify for the 20% QBI deduction on pass-through income. Entity structure and income level determine eligibility — complex calculation for physician-owned practices.

HSA and HRA Deductions

Self-employed healthcare providers can establish Health Savings Accounts and deduct contributions. Employer-funded HRAs for employees are tax-deductible business expenses.

Retirement Plan Options

A defined benefit pension plan allows significantly higher pre-tax contributions than a SEP-IRA or 401(k) — potentially $150,000–$250,000/year for established physicians near retirement. The actuarial calculation is complex but the tax savings are material.

Retail & E-Commerce

Inventory Accounting Methods

FIFO (first-in, first-out) vs. LIFO (last-in, first-out) vs. weighted average cost — the method affects cost of goods sold and taxable income. In an inflationary environment, LIFO reduces taxable income by recognizing higher-cost inventory first.

Multi-State Sales Tax Compliance

E-commerce retailers selling into multiple states face economic nexus in those states once $100K or 200 transactions is reached. Managing registrations, filing calendars, and product taxability rules across states requires either a tax pro or a sales tax automation platform (TaxJar, Avalara).

Section 199A QBI for Retail Businesses

Most retail businesses (not specified service businesses) qualify for the 20% QBI deduction on pass-through income below the income thresholds. Optimizing W-2 wages paid and qualified property can maximize this deduction at higher income levels.

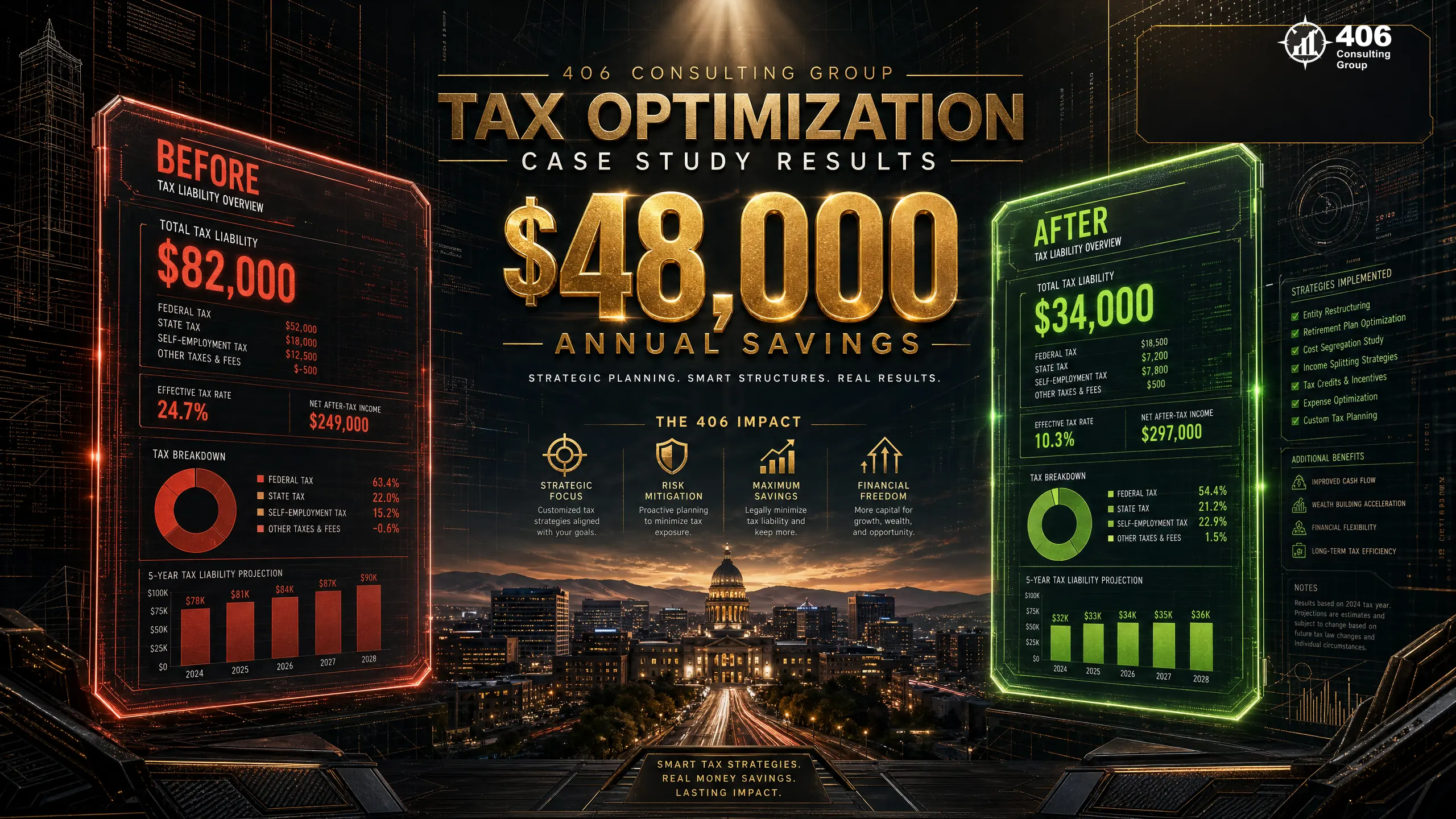

Case Study: Boise Tech Consulting Firm — $47,000 in Year-One Tax Savings

Anonymized — Boise, Idaho

Technology Consulting Firm — 3 Partners, $1.2M Revenue

Situation When We Were Engaged

- Structured as a multi-member LLC — no S-Corp election despite $1.2M revenue

- All three partners paying SE tax on full distributive share of $400K each

- Using a seasonal local CPA — no contact between April and the following January

- No quarterly estimated payments — large surprise tax bills each April

- No home office deduction claimed despite all three working from home offices

- No R&D credit claimed despite qualifying software development activities

- No retirement plan — partners taking all income as distributions, fully taxable

Changes and Results After Year One

- S-Corp election filed March 15 — each partner salary set at $130K market rate, $270K/each in distributions not subject to SE tax

- SE tax savings: ~$24,000 across three partners combined ($8,000 each)

- Home office deduction established: average $4,200 per partner → $12,600 total additional deduction

- R&D credit calculated on qualifying software development: $7,200 federal credit (dollar-for-dollar tax reduction)

- SEP-IRA established: each partner contributed $40,000 (25% of $160K W-2 compensation) → $120,000 total pre-tax savings across three partners

- Quarterly estimated payments established — no more April surprises

$47K

Total first-year tax savings across three partners

$7.2K

R&D credit — dollar-for-dollar federal tax reduction

$120K

Pre-tax retirement contributions sheltered from income tax

The insight: Three partners earning $400K each from a $1.2M revenue firm were paying SE tax on every dollar of income — roughly $56,000 per partner in SE tax alone, before federal and Idaho income tax. The S-Corp election alone, properly implemented with market-rate salaries, saved $24,000 in year one. Combined with the R&D credit and retirement contribution deductions, the total first-year tax impact was $47,000 — on a firm that had been using the same seasonal local CPA for four years with no proactive planning.

FAQ: Virtual Tax Preparation for Boise Businesses

What is virtual tax preparation for businesses?

Virtual tax preparation for businesses is a full-service tax filing engagement conducted remotely — no in-person office visits required. You upload documents through a secure portal, communicate with your tax preparer via video call and email, sign returns electronically, and receive filed returns digitally. The scope of work is identical to an in-person CPA engagement: federal business return, Idaho state return, deduction identification, estimated payment calculations, and year-round advisory. The difference is access — a virtual tax preparer is available year-round, not just during filing season, and is not constrained to your geographic area.

How does virtual tax prep work in Idaho specifically?

Idaho businesses must file both a federal business return and an Idaho state return (Form 41 for C-Corps, Form 41S for S-Corps, Form 65 for partnerships, or Schedule C on Form 40 for sole props). A virtual tax preparer files both simultaneously. Idaho-specific considerations include: the 5.8% flat income tax rate (2023+), the Idaho Investment Tax Credit (3% on qualifying equipment), Idaho's economic nexus rules for sales tax, and Idaho's partial conformity to federal tax code changes. A preparer experienced with Idaho returns handles these automatically — a generalist preparer may miss Idaho-specific elections.

What Idaho state taxes does my Boise business need to file?

The Idaho taxes most Boise businesses need to manage: Idaho income tax (5.8% flat rate on Idaho-sourced business income, filed on Form 41, 41S, or 65 depending on entity); Idaho sales tax (6% on taxable sales, filed monthly or quarterly with the Idaho State Tax Commission); Idaho payroll withholding (withheld from employees and remitted monthly or quarterly); and Idaho unemployment insurance (separate quarterly filing). Some businesses also owe Idaho business personal property tax on equipment. The specific forms and filing frequencies depend on your entity type and revenue level.

Is an S-Corp election right for my Boise business?

An S-Corp election is typically worth evaluating when your net business profit consistently exceeds $80,000–$100,000 per year. At that level, the self-employment tax savings on distributions above your reasonable salary usually exceed the additional compliance costs (payroll processing, separate business return, state filing fees). The analysis is straightforward: calculate SE tax on your current net profit (15.3% up to the SS wage base, 2.9% above), then model the same profit split between a market-rate salary and distributions with an S-Corp. The difference is your potential annual savings. A virtual tax advisor can run this analysis for your specific numbers in under an hour.

What is the Idaho Investment Tax Credit?

The Idaho Investment Tax Credit (ITC) is a 3% tax credit for businesses that purchase or lease qualified new or used property placed in service in Idaho — including manufacturing equipment, construction equipment, vehicles used in the business, and certain other depreciable assets. The credit is applied dollar-for-dollar against Idaho income tax owed, up to 50% of the tax liability in a given year (unused credit can be carried forward up to 14 years). A Boise contractor who purchases $80,000 in equipment during the year has a $2,400 credit directly reducing their Idaho tax bill. This credit is frequently missed by businesses whose tax preparers are not Idaho-specialized.

How much does virtual business tax preparation cost in Boise?

Virtual business tax preparation fees vary by entity type, business complexity, and the scope of advisory services included. General ranges: sole proprietorship or single-member LLC (Schedule C) — $500–$1,200; S-Corporation (Form 1120-S + state) — $1,200–$2,500; C-Corporation (Form 1120 + state) — $1,500–$3,000; multi-member LLC or partnership (Form 1065 + state) — $1,200–$2,500. Year-round advisory access — quarterly check-ins, questions answered outside filing season, year-end planning — is typically an additional $150–$400/month or included in a bundled annual engagement. The right comparison is not the fee in isolation but the fee relative to the tax savings identified — a $2,000 preparation fee that identifies $8,000 in missed deductions has a 4× return.

Does 406 Consulting Group offer virtual tax preparation for Boise businesses?

Yes. 406 Consulting Group provides virtual tax preparation and year-round tax advisory for businesses in Boise, the Treasure Valley, and across Idaho and the Intermountain West. We specialize in business tax returns for S-Corporations, partnerships, and LLCs — with particular expertise in Idaho state tax compliance, entity structure optimization, and year-round proactive tax planning. Our engagements include Idaho state filings, estimated payment management, and year-end planning calls — not just a return in April. Contact us to discuss what your Boise business tax situation looks like and what we can do to improve it.

External Resources

Boise, ID & Treasure Valley

Virtual Tax Preparation for Boise Businesses

406 Consulting Group provides year-round virtual tax preparation and advisory for Boise businesses — federal and Idaho state returns, estimated payment management, entity structure optimization, and proactive year-end planning. No once-a-year shoebox handoff.

Idaho Business Tax Blueprint

Which phase is your business in?

Organize

Jan–Feb: Clean books, gather documents

Analyze

Feb–Mar: Deductions, elections, credits

File

Mar–Apr: Federal + Idaho returns filed

Optimize

May–Dec: Quarterly payments, year-end planning

Idaho Tax Quick Reference

Related Reading

Ready to stop overpaying?

Virtual tax prep and year-round advisory for Boise businesses. Federal + Idaho state returns, entity optimization, no April surprises.

Schedule a Consultation