Scaling Your Columbia Falls, MT Business

with a Fractional CFO

A fractional CFO helps Columbia Falls businesses scale past the bookkeeper ceiling — with cash flow forecasting, lender-ready financials, and strategic growth planning.

A fractional CFO in Columbia Falls, MT is not a luxury item for large companies. It is the financial infrastructure that separates the businesses that scale past $1M from the ones that stall there — working harder every year without getting ahead.

Most Columbia Falls business owners hit a ceiling between $750K and $1.5M in annual revenue. Revenue is growing, the team is expanding, and the work is good — but the bank line is denied, the tax bill arrives as a surprise, and the owner is still the only person who understands the financial picture. That is not a revenue problem. It is a financial systems problem, and a fractional CFO fixes it.

This guide covers exactly how a fractional CFO helps Columbia Falls businesses scale — what they build, when to hire one, what it costs, and what the first 90 days look like in practice.

Table of Contents

What Scaling Actually Means for a Columbia Falls Business

Scaling is not the same as growing. A business that adds revenue every year is growing. A business that adds revenue without adding proportional cost, stress, or owner hours is scaling. The difference is financial infrastructure — the systems, reporting, and strategic decision-making that let a business handle more volume without breaking.

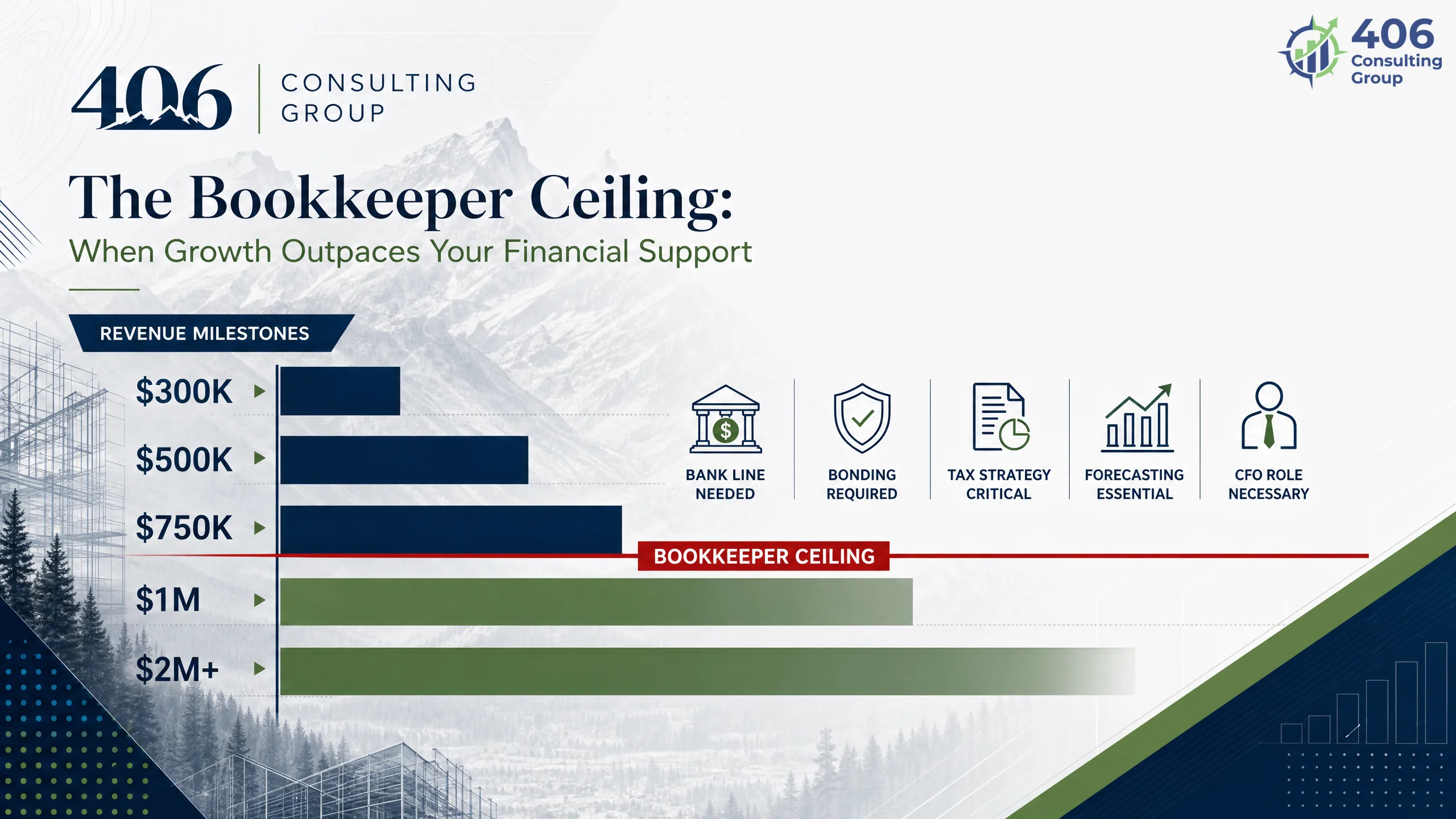

In Columbia Falls, most businesses start with a simple setup: the owner runs operations, a bookkeeper manages QuickBooks, and the CPA files taxes once a year. That system works at $300K. It works at $500K. At $800K–$1M, it starts to crack. By $1.5M, it is actively costing the business money.

Growing

Under $750K

Bookkeeper + year-end CPA

No budget, but manageable

Straining

$750K–$1.5M

Same bookkeeper, more volume

Bank line needed, no forecast, tax surprise

Stalling

$1.5M+

Still no CFO function

Margin erosion, owner overload, growth stops

The Columbia Falls context: The Flathead Valley economy — construction, tourism, trades, hospitality — creates additional scaling complexity. Seasonal cash swings, bonding requirements, and a tight local subcontractor market mean the financial systems that need to scale are more demanding than most generic business guides account for. A business hitting $1M here needs infrastructure built for that specific complexity.

The Bookkeeper Ceiling: When Your Current Setup Stops Working

The bookkeeper ceiling is the point where your existing financial setup — bookkeeper plus annual CPA — can no longer support what the business needs to do next. It appears as five specific problems, usually in this order.

The bank says no

You apply for a working capital line and the bank declines — or offers half of what you asked for. The lender cites your financials: too much debt relative to income, insufficient working capital, no verifiable cash flow projection. A bookkeeper produces historical records. A fractional CFO produces the financial package and narrative that gets the loan approved.

Hiring decisions feel like guessing

You are not sure whether you can afford to hire the next employee. Revenue is up, but you do not know the margin impact — or how much cash will be available to fund payroll six months from now. Without a budget and a 13-week cash flow forecast, every hiring decision is a guess with real consequences.

Tax bills arrive as surprises

Your Q4 estimated payment is wrong — by a lot. Or the April bill is larger than expected because nobody modeled income and deductions through the year. Tax strategy requires forward-looking planning. A bookkeeper files what happened. A fractional CFO plans what should happen so the number in April is not a shock.

You cannot answer basic financial questions

A key customer asks for your financial statements before signing a large contract. A potential partner asks about your working capital ratio. You are walking into a bank meeting without knowing your DSCR. If basic financial questions catch you off guard, your systems are not keeping pace with your business relationships.

Bonding is blocked or limited

For Columbia Falls contractors and trades businesses, bonding capacity determines which projects you can pursue. If your bonding limit is not growing with your revenue — or if you have been denied a bond on a project you wanted — the underlying financial ratios (working capital, net worth, WIP position) are the cause. A CFO builds and maintains those ratios systematically.

The short answer: If any two of these five signals are present, your business has outgrown its current financial setup. The question is not whether you need more financial infrastructure — it is which type, and when.

The Montana Business Scale Roadmap: 4 Stages of Financial Growth

The Montana Business Scale Roadmap maps where a Columbia Falls business sits on the path from bookkeeper-managed to CFO-powered. Each stage has specific financial characteristics, an infrastructure requirement, and a trigger that signals it is time to move up.

Stage 1: Survival

Under $500KInfrastructure: Bookkeeper + QuickBooks

Trigger: Business is consistent and cash flow is manageable without a forecast

At this stage, a reliable bookkeeper who keeps clean records, reconciles monthly, and prepares data for your CPA at year-end is sufficient. The owner is the financial decision-maker, and the decisions are simple enough to make from experience. The priority is clean books — not strategic finance.

Stage 2: Stability

$500K–$1.2MInfrastructure: Bookkeeper + part-time controller

Trigger: Bank lines needed, hiring decisions require analysis, tax strategy matters

The business is too complex for gut-level financial decisions. A controller function adds reporting — budget vs. actual, job-level P&Ls for contractors, monthly close, and financial statements that can go to a lender. Most Columbia Falls businesses stay at Stage 2 longer than they should because the controller function is not clearly defined or accessible in the local market.

Stage 3: Leverage

$1.2M–$3MInfrastructure: Controller + fractional CFO

Trigger: Growth is possible but not happening — the business has capacity but no financial clarity to act

This is where most ambitious Columbia Falls businesses stall. The numbers are there. The market opportunity is real. But without a CFO building forward-looking financial strategy — forecasting, scenario modeling, lender relationships, tax optimization — the business cannot confidently pull the trigger on the growth moves in front of it. The fractional CFO is the unlock at this stage.

Stage 4: Scale

$3M+Infrastructure: Full finance function or in-house CFO

Trigger: Growth is active and the business needs full-time financial leadership

At $3M+ in revenue with multiple locations, significant payroll, or complex capital needs, a fractional CFO may transition to an in-house hire or a more robust engagement. The systems built in Stage 3 are the foundation — Scale runs on them. Businesses that skip Stage 3 and try to jump straight to Scale almost always get pulled back.

Where most Columbia Falls businesses stall: The Stage 2 to Stage 3 transition. The business has outgrown bookkeeper-only, but the owner does not know what a controller or fractional CFO actually delivers — or how to find one who understands the Flathead Valley market. That ambiguity is expensive: every month at Stage 3 without a CFO is a month of decisions made without the data to make them well.

What Does a Fractional CFO Do That a Bookkeeper Cannot?

The short answer: A bookkeeper records what happened. A fractional CFO leads what happens next. The distinction is not a matter of skill level — it is a matter of role and direction. A bookkeeper processes transactions. A CFO uses financial data to make decisions, build strategy, and position the business to access capital and grow.

Cash Flow Forecasting

Bookkeeper

Records cash in and out historically

Fractional CFO

Builds rolling 13-week forecast, models seasonal gaps, arranges credit before shortfalls arrive

Budgeting & Variance Analysis

Bookkeeper

No budget; reconciles actuals only

Fractional CFO

Builds annual budget by department or job, tracks actual vs. budget monthly, identifies margin leakage early

Lender & Banking Relationships

Bookkeeper

No role in bank conversations

Fractional CFO

Prepares the financial package, coaches the borrower narrative, positions the business for loan approval

Tax Strategy

Bookkeeper

Prepares data for the CPA at year-end

Fractional CFO

Coordinates with CPA quarterly, models tax liability, times equipment purchases and entity elections to minimize exposure

KPIs & Management Dashboards

Bookkeeper

Produces P&L and balance sheet

Fractional CFO

Builds a KPI scorecard specific to the business model — margin per job, revenue per employee, DSCR, working capital ratio

Strategic Decision Support

Bookkeeper

Cannot model the impact of decisions

Fractional CFO

Runs scenarios before major moves: hire vs. contract, buy vs. lease, take the project vs. pass, open a second location vs. not

Related reading: What a fractional CFO actually costs — and what ROI to expect breaks down pricing structures and how Montana businesses should evaluate the return before engaging.

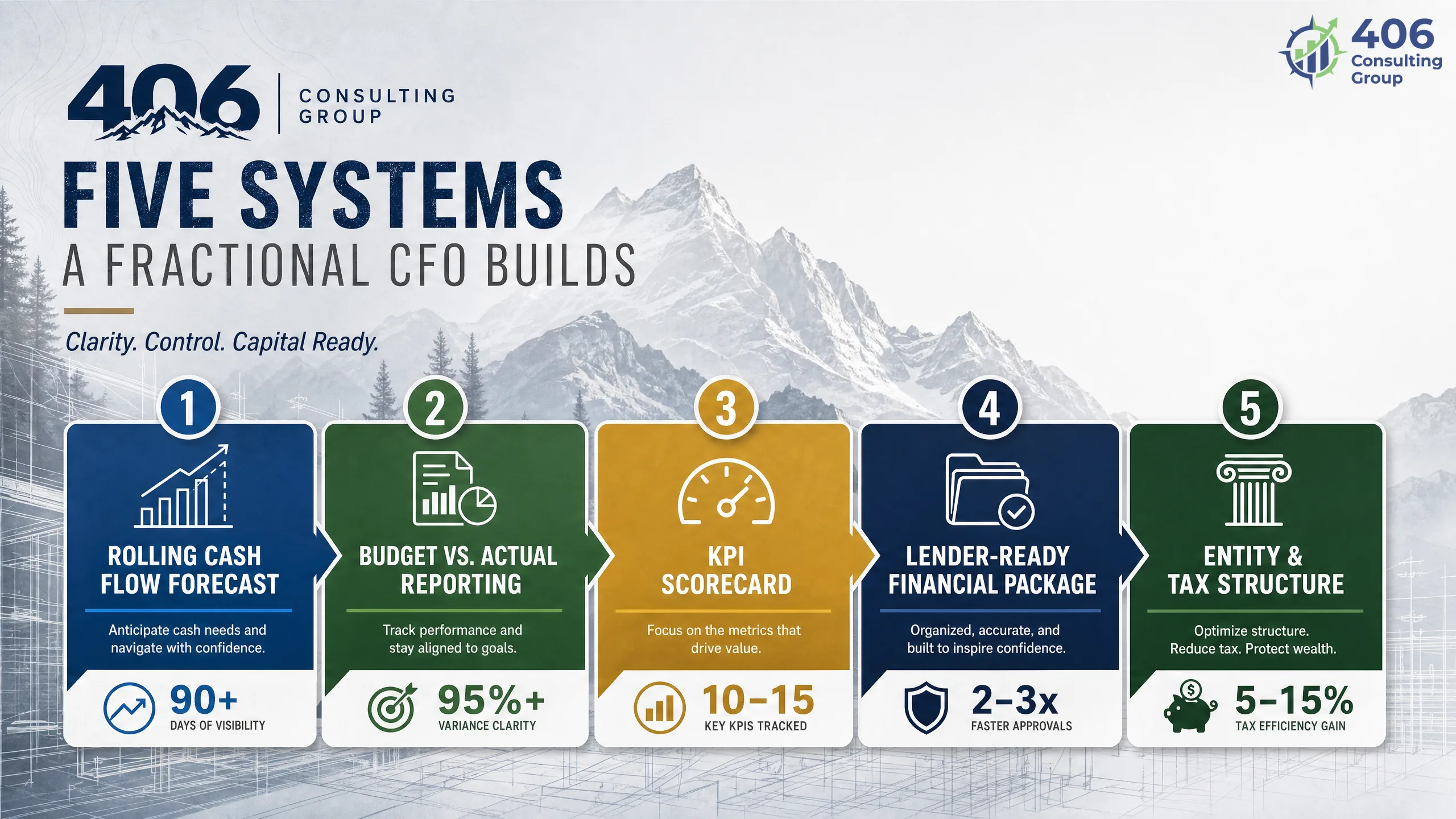

The 5 Financial Systems a Fractional CFO Builds First in Columbia Falls

A fractional CFO does not arrive and improve everything at once. The first 90 days focus on five foundational systems — in order. Each builds on the last. A Columbia Falls business with all five in place can move faster, borrow at better terms, and make decisions with confidence instead of instinct.

Rolling Cash Flow Forecast

What it is

A 13-week projection of cash inflows and outflows by week, updated weekly. Built from the backlog, payment terms, payroll schedule, and known fixed costs. Not a monthly P&L — a weekly cash map.

Why it matters first

Prevents the cash crises that feel sudden but were visible 60–90 days out. For Columbia Falls seasonal businesses, this is the tool that makes the winter gap a managed event instead of a February emergency.

Real result

A Flathead Valley hospitality operator running without a forecast was surprised by a $140,000 cash shortfall every January. With a rolling forecast built in August, they arranged a $120,000 line of credit in October. No emergency in year two.

Budget vs. Actual Reporting

What it is

An annual budget built by revenue stream, cost category, and headcount — tracked monthly against actual results. Variance analysis identifies where the business is running ahead or behind plan, and by how much.

Why it matters first

Without a budget, there is no baseline. Without a baseline, every result looks acceptable. A business running 8% below gross margin expectations does not know it until year-end — when the options for correction are gone.

Real result

A Columbia Falls construction GC doing $2.1M annually had no budget. The first budget build revealed materials costs running 11% over estimate — traced to two projects where subcontractor change orders were not captured in job cost. Fixed before it reached the annual P&L.

KPI Scorecard

What it is

A one-page dashboard of 8–12 key performance indicators specific to the business model. For contractors: gross margin per job, backlog, bonding headroom. For hospitality: revenue per available room, labor cost %, inventory turn. Updated monthly.

Why it matters first

A P&L is a trailing indicator — it tells you what already happened. A KPI scorecard includes leading indicators that signal where the business is going 60–90 days before it appears in financial statements.

Real result

A Columbia Falls trades business owner reviewing P&Ls each month had no visibility into revenue per technician — the metric that actually drove profitability. Once tracked, three underperforming crew configurations were identified and corrected within a single quarter.

Lender-Ready Financial Package

What it is

A prepared set of financial statements, projections, and narrative that can be presented to a commercial lender at any time. Includes balance sheet, income statement, cash flow statement, working capital analysis, and a business narrative explaining financial trends.

Why it matters first

A business that is always ready to borrow can act on opportunities. A business that scrambles to produce financials when a bank asks loses time, loses credibility, and often loses the loan.

Real result

A Columbia Falls contractor had been trying to get a $400,000 equipment line for 14 months before engaging us. Complete lending package submitted in week six of the engagement. Approved in 18 days.

Entity & Tax Structure Optimization

What it is

A review of the current legal entity, owner compensation structure, and tax filing approach — then a recommendation for the optimal structure given current revenue, growth trajectory, and owner objectives.

Why it matters first

Many Columbia Falls businesses are operating in a suboptimal entity structure. An LLC taxed as a sole proprietorship paying full self-employment tax on $400K of net income is leaving $20,000–$35,000 on the table annually compared to an S-Corp election.

Real result

S-Corp election for a Columbia Falls service business in year one of engagement: $28,000 in FICA savings. Cost of the CFO engagement: $1,800 per month. The entity restructure alone paid for the first 16 months of service.

How a Fractional CFO Prepares Columbia Falls Businesses for Lending

Carrie Anderson spent years in commercial banking underwriting loans across Montana and the Pacific Northwest before co-founding 406 Consulting Group. That perspective — sitting on the lender's side of the table — shapes how we prepare clients for bank conversations in a way that purely accounting-focused CFO firms cannot replicate.

Commercial lenders at Glacier Bancorp, First Security Bank, Mountain West Bank, and the other regional institutions serving Flathead County are not looking for a reason to say yes. They are looking for evidence that you understand your business, can manage risk, and will repay the loan. The financial package you bring either supports that narrative or it does not.

DSCR — Debt Service Coverage Ratio

Net Operating Income ÷ Annual Debt Payments

The primary repayment test. A DSCR below 1.0 means operating income does not cover debt payments — automatic decline for most lenders. Below 1.25, most banks require additional collateral. A CFO models DSCR before the application and structures the loan request to meet the threshold.

Working Capital Ratio

Current Assets ÷ Current Liabilities

Liquidity test — can the business meet short-term obligations? Both lenders and surety companies use this ratio. A CFO manages working capital actively: timing accounts payable, managing receivables, and maintaining the ratio that supports both lending approval and bonding capacity.

Debt-to-Equity

Total Liabilities ÷ Net Worth

How leveraged the business is. Heavy equipment financing or a real estate purchase can push this ratio into territory lenders find uncomfortable. A CFO monitors the ratio and advises on timing of major debt additions relative to equity growth so the business stays in a borrowable position.

Financial Statement Quality

Compiled / Reviewed / Audited

Self-prepared or bookkeeper-prepared statements raise immediate lender questions. CPA-compiled statements are the minimum for most commercial loans above $250K. Reviewed statements are required for most loans above $500K and by surety companies for bonds at that level.

What lenders want beyond the numbers: A borrower narrative — a clear explanation of what the business does, how it makes money, what the loan is for, and how it will be repaid — presented by someone who owns the numbers behind it. A CFO prepares that narrative and sometimes joins the bank meeting. See what commercial lenders actually evaluatefor the full picture from Carrie's underwriting background.

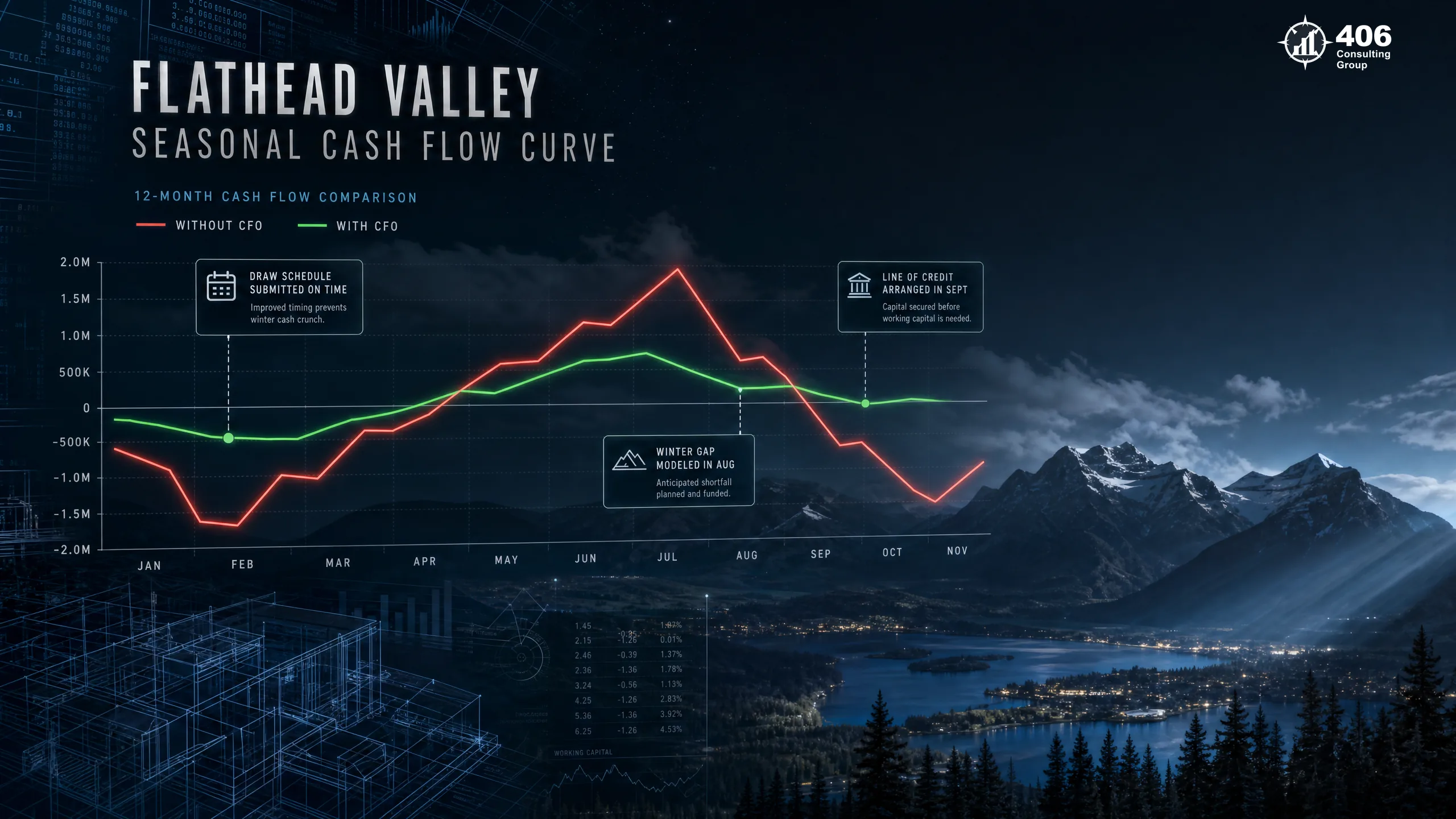

Cash Flow Forecasting for Flathead Valley's Seasonal Business Economy

Columbia Falls businesses face a seasonal cash structure that most generic financial guidance does not account for. Construction, tourism, and hospitality revenue ramps hard from May through September, then drops. Collections lag billing by 30–60 days. Retainage and final payments land anywhere from October through February. Without a forward-looking forecast, the winter cash position is a surprise every year. It should not be — it is structurally predictable from your backlog and payment terms.

April–May

Ramp-upCFO reviews backlog and models summer revenue. Identifies any gaps in the project pipeline that would create fall cash shortfalls. Credit line renewed. Material supplier payment terms negotiated before peak season pricing kicks in.

June–August

Peak volumeCash flowing in from peak revenue — but receivables lag 30–45 days. CFO monitors weekly cash position, tracks retainage accumulating on summer projects, and models when retainage releases will occur relative to cash needs.

September

Critical planning monthCFO models the winter cash gap based on backlog, payment terms, and retainage release schedule. If a credit line is needed for January–February, the application goes in now — not when the gap arrives. Arrangements made in September cost less than emergency draws in January.

October–November

Collections and year-endFinal billings on summer projects. Retainage requests submitted. CFO tracks outstanding receivables and follows up systematically. Year-end tax planning begins: equipment purchase timing, Q4 distributions, retirement plan contribution strategy.

December–February

Winter gap — managedCash position managed against the forecast built in September. Credit line covers the gap if needed. No emergency financing at peak rates. Owner is not surprised because the model predicted this position 90 days ago and the business was positioned for it.

When Is the Right Time to Hire a Fractional CFO in Columbia Falls?

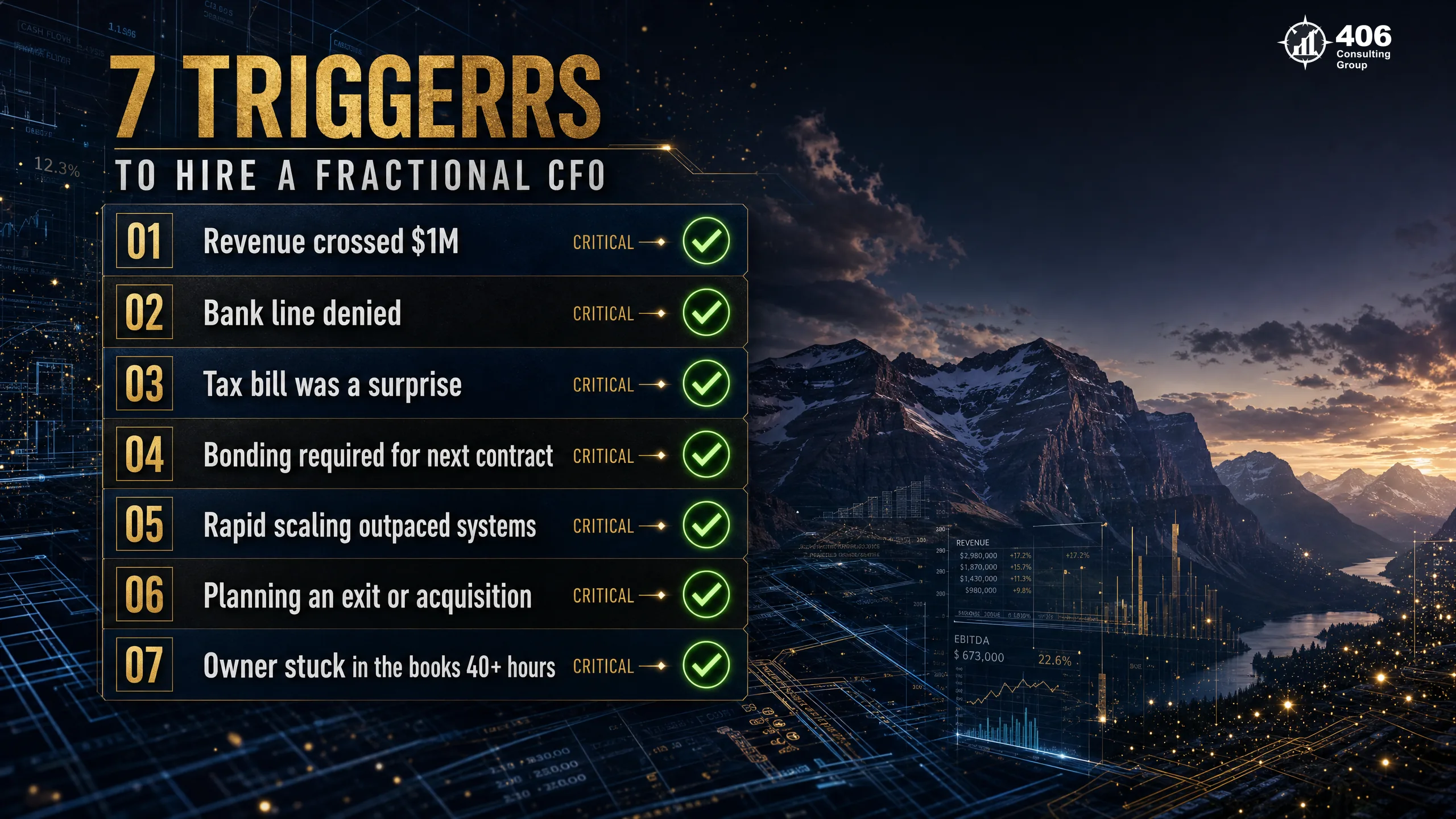

The right time to hire a fractional CFO is not when you can afford one. By that logic, many businesses wait until the financial systems failure has already cost them more than a year of CFO fees. The right time is when one or more of these seven trigger events is present.

Revenue crossed $1M — or is approaching it

At $1M in annual revenue, the financial complexity of running a business jumps materially: more employees, more vendors, more tax complexity, more lender scrutiny. Most businesses benefit from CFO-level support at or before this threshold — not after the complexity has already caused problems.

You have applied for — or plan to apply for — a bank loan

A fractional CFO should be engaged before the application, not after a denial. The preparation period — cleaning up the financial package, modeling the DSCR, building the narrative — is where the CFO earns their fee. A second application is harder than a first one done right.

Hiring decisions feel like guesses

If you do not know whether you can afford the next hire — or what the margin impact will be over 12 months — you need a budget and a cash flow forecast. Both are CFO deliverables. Hiring too fast or too slow both cost money; the CFO builds the model that removes the guess.

Your tax bill was a surprise

If the Q4 or April tax bill was significantly different from what you expected, your financial visibility is insufficient. Tax strategy requires quarterly coordination between the CFO and your CPA — not a single year-end conversation after the numbers are locked.

Bonding is required for your next contract

For Columbia Falls contractors, this is often the clearest trigger. Bonding capacity is determined by financial ratios — working capital, net worth, WIP position. A CFO builds and maintains those ratios systematically, and a well-prepared bonding package is a direct output of that work.

You are considering a major strategic decision

Opening a second location, acquiring a competitor, taking on a significantly larger project, adding a new service line — any major decision with material financial consequences deserves CFO-level scenario modeling before the commitment. Most owners making these decisions are doing it without a financial model.

You are spending more than 20% of your time on financial questions

Owner time spent on financial management — payroll questions, vendor disputes, bank conversations, bookkeeper supervision — is the most expensive financial function a business operates. A CFO removes the owner from the day-to-day financial stack. That time, redirected to revenue-generating activity, is often the highest ROI in the engagement.

CFO vs. Controller vs. Bookkeeper: Which Role Does Your Columbia Falls Business Need?

These three roles are frequently confused — and that confusion causes businesses to hire the wrong function at the wrong stage. Here is the direct comparison.

| Function | Bookkeeper | Controller | Fractional CFO |

|---|---|---|---|

| Primary role | Transaction recording | Reporting & close | Financial strategy & decisions |

| Time orientation | Backward — what happened | Present — accurate right now | Forward — what will happen |

| Reports produced | P&L, balance sheet | Full financials, budget vs. actual | Cash forecast, KPIs, scenario models |

| Bank relationship | No role | Prepares data | Manages relationship, presents package |

| Tax coordination | Data prep | Works with CPA at year-end | Quarterly strategy and timing |

| Typical cost (Montana) | $500–$1,500/mo | $1,500–$3,500/mo | $2,000–$8,000/mo |

| When you need it | From day one | $500K–$1M revenue | $1M+ or at a trigger event |

Most Columbia Falls businesses at Stage 2–3 need both a controller and a fractional CFO — not one or the other. The controller keeps the books accurate and the reporting current. The CFO uses that reporting to drive strategy. At 406 Consulting Group, our controller services and fractional CFO services are designed to work together as a single integrated finance function.

What a Fractional CFO Engagement Looks Like in Practice

A fractional CFO is not a consultant who produces a report and leaves. It is an ongoing engagement with specific deliverables, a defined cadence, and direct integration into how the business makes financial decisions. Here is what the first 90 days and the ongoing monthly engagement look like with 406 Consulting Group.

Month 1: Financial Audit & Foundation

- Complete review of existing financial statements, bank reconciliations, and accounting setup

- Identify the 3–5 highest-priority financial problems or gaps — ranked by cost to the business

- Begin building the rolling 13-week cash flow forecast

- Establish KPI baseline — what are we measuring, and what does it look like today?

- Meet with existing bookkeeper and CPA to align on workflows and data flow

Month 2: Systems Build

- Budget for the current fiscal year, with department or job-level breakdown

- First month of budget vs. actual review — what is the variance and why?

- Cash flow forecast operational and in weekly review with the owner

- KPI scorecard published and reviewed with ownership for the first time

- Bank and lender package assessed — identify gaps and begin preparation if financing is a near-term goal

Month 3: Strategy & Decisions

- First full strategic review — where is the business, where is it going, what are the financial levers?

- Entity and tax structure recommendation presented with supporting analysis

- Any immediate strategic decisions modeled with scenario analysis before the commitment

- Lender package finalized and ready to submit if a loan is in the pipeline

- Quarterly review cadence and ongoing monthly meeting structure established

Ongoing monthly cadence:After the first 90 days, the engagement typically runs 4–8 hours per month — a monthly financial review, budget vs. actual discussion, cash flow update, and decision support on anything that arose. Quarterly, we conduct a deeper strategic review and coordinate with the CPA on tax planning. The owner attends one meeting per month and has access to the CFO for questions throughout. The goal is to remove financial uncertainty from the owner's day — not to add another meeting to their calendar.

Columbia Falls Industries That Benefit Most from a Fractional CFO

Every industry has different financial levers. A fractional CFO who understands the Flathead Valley economy knows which levers matter most for each sector — and where to pull first to get the fastest result.

Construction & General Contracting

Bonding capacity + WIP scheduleBonding is the access control for public work in Flathead County. A CFO builds the financial ratios that determine single-job and aggregate bonding limits — working capital, net worth, WIP overbilling position. WIP schedule management prevents the overbilled portfolio position that triggers surety scrutiny. For Columbia Falls GCs pursuing MDOT, Flathead County, and school district work, the CFO function is the difference between pursuing those contracts and watching competitors take them.

Construction accounting in Columbia FallsHospitality & Glacier-Area Tourism

Seasonal cash modeling + RevPAR trackingGlacier National Park tourism creates a May–September revenue concentration that must support 12 months of fixed costs. A CFO models the off-season cash position in May, arranges credit facilities needed for the slow period, and tracks revenue per available room and occupancy against budget weekly during peak season. The businesses that survive and grow in the Glacier corridor manage their cash seasonality as a system — not as an annual surprise.

Trades & Specialty Contractors

Entity structure + job-level margin trackingElectricians, plumbers, HVAC contractors, and specialty subs in Columbia Falls often operate in an entity structure that does not match their income level. A trades business at $800K in revenue operating as a sole proprietorship is paying 15.3% self-employment tax on net income when an S-Corp election would reduce that exposure significantly. Entity optimization is frequently the highest-ROI CFO deliverable for a trades business in year one.

Retail & Commercial Services

Inventory financing + multi-location expansion readinessColumbia Falls retail and commercial service businesses expanding along the US-2 corridor — or considering a second location in Kalispell or Whitefish — need scenario modeling before they commit. The financial viability of a second location depends on the first location's margin, owner time allocation, capital required, and incremental fixed cost. A CFO builds that model before the lease is signed, not after it is too late to change course.

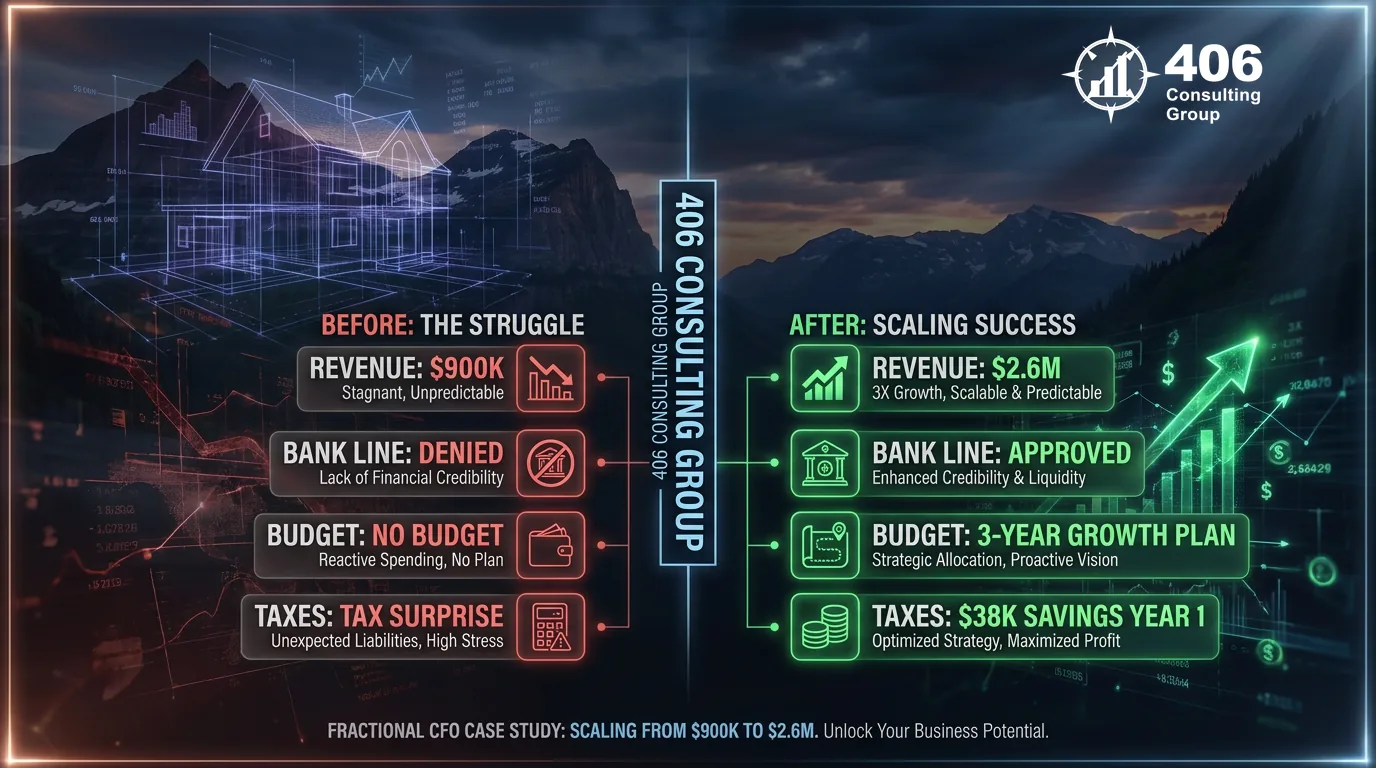

Case Study: Columbia Falls Contractor Scaled from $900K to $2.6M in Three Years

Anonymized — Columbia Falls, MT

Commercial GC — 3-Year Fractional CFO Engagement

When We Started

- $900K annual revenue — growing but stalled at the ceiling

- Bookkeeper only — no budget, no cash flow forecast

- Bank working capital line denied twice in 14 months

- No WIP schedule — bonding limit capped at $250K single job

- Owner spending 30% of time answering financial questions

- Prior-year tax surprise: $62K unexpected liability at filing

Three Years Later

- $2.6M annual revenue — consistent gross margin growth year over year

- $400K working capital line — approved 18 days after package submission in month 2

- WIP schedule current monthly — bonding capacity expanded to $1.2M single job

- S-Corp election completed — $38K in FICA savings in year one alone

- Owner out of day-to-day finance — one monthly CFO meeting

- Tax liability planned quarterly — zero year-end surprises in three consecutive years

The critical unlock: Both prior bank denials cited insufficient working capital documentation and no verifiable cash flow projection. In month two of our engagement, we submitted a complete lending package with a 13-week cash flow model, WIP schedule, and business narrative. Approved at $400,000 in 18 days. The contractor used the line to take on two projects simultaneously for the first time — driving revenue from $900K to $1.5M in year one of the engagement. The subsequent two years of growth were built on the financial systems put in place in months one through three.

Frequently Asked Questions: Fractional CFO in Columbia Falls, MT

What does a fractional CFO do for a small business in Columbia Falls?

A fractional CFO provides part-time CFO-level financial leadership — cash flow forecasting, budget management, lender relationship preparation, KPI tracking, tax strategy coordination, and strategic decision support. The 'fractional' means you access CFO expertise at a fraction of the cost of a full-time hire. For a Columbia Falls business at $1M–$3M in revenue, a fractional CFO typically costs $2,000–$6,000 per month and provides 6–15 hours of high-level financial leadership working alongside your existing bookkeeper and CPA.

When should a Columbia Falls business hire a fractional CFO?

The seven most reliable trigger events are: revenue crossed $1M, a bank loan is needed or has been denied, hiring decisions feel like guesses, tax bills arrive as surprises, bonding is required for a new contract, a major strategic decision is on the table, or the owner is spending more than 20% of their time on financial questions. Any one of these is worth a conversation. Two or more together means the business is operating without the financial infrastructure it needs to grow efficiently.

What is the difference between a fractional CFO and a bookkeeper?

A bookkeeper records transactions — what happened in the past. A fractional CFO leads financial strategy — what should happen next. A bookkeeper reconciles accounts and produces basic financial statements. A CFO builds cash flow forecasts, manages lender relationships, coordinates tax strategy with your CPA, tracks KPIs, and models the financial impact of major decisions before they are made. Most businesses need both — the bookkeeper keeps records accurate, and the CFO uses those records to drive growth.

How much does a fractional CFO cost for a Montana small business?

Fractional CFO engagements in Montana typically range from $2,000 to $8,000 per month depending on scope, hours, and complexity. A Columbia Falls business at $1M–$2M in revenue with standard needs typically falls in the $2,000–$4,000 range. The ROI calculation is straightforward: if the CFO recovers $30,000 in tax savings in year one and secures a bank line that funds $200,000 in incremental revenue, the engagement pays for itself many times over. See our full breakdown of what a fractional CFO costs and what return to expect.

Can a fractional CFO help a Columbia Falls business qualify for a bank loan?

Yes — this is one of the highest-value CFO deliverables. A fractional CFO prepares the complete financial package lenders require: CPA-quality financial statements, a 13-week cash flow model, working capital analysis, DSCR calculation, and a borrower narrative explaining what the business does and how the loan will be repaid. Carrie Anderson's commercial banking background at 406 Consulting Group gives us direct insight into what lenders at Glacier Bancorp, Mountain West Bank, and regional Montana institutions evaluate — and how to structure the package for approval.

How does a fractional CFO handle seasonal cash flow for Flathead Valley businesses?

Seasonal cash management starts with modeling the winter gap in the summer — not when it arrives in January. A CFO builds a rolling 13-week cash flow projection updated weekly that maps every inflow and outflow by week. The model makes the winter cash position visible in September so credit facilities are arranged, vendor terms are negotiated, and the owner is not surprised. The Flathead Valley winter gap is structurally predictable from backlog and payment terms. The CFO's job is to ensure the business is positioned for it every year — not just the years when the owner happened to plan ahead.

Does 406 Consulting Group provide fractional CFO services in Columbia Falls, MT?

Yes. 406 Consulting Group provides fractional CFO services to businesses across Columbia Falls, Kalispell, Whitefish, Missoula, Bozeman, and throughout Montana and the Intermountain West. Jason Anderson's background in operational finance and strategic planning and Carrie Anderson's experience in commercial banking and underwriting are particularly relevant for construction, trades, hospitality, and service businesses in the Columbia Falls and Flathead Valley market. Contact us to discuss what a CFO engagement would look like for your business.

External Resources

Columbia Falls, MT

Fractional CFO Services for Columbia Falls Businesses Ready to Scale

406 Consulting Group provides fractional CFO services, controller services, and bookkeeping for Columbia Falls and Flathead Valley businesses. Whether you are approaching the bookkeeper ceiling or actively scaling past $2M, we build the financial infrastructure that gets you there.

Montana Business Scale Roadmap

4 stages — where does your business sit?

Survival

Under $500K — bookkeeper sufficient

Stability

$500K–$1.2M — controller needed

Leverage

$1.2M–$3M — fractional CFO is the unlock

Scale

$3M+ — full finance function

7 CFO Trigger Events

Any one = time to act

Revenue crossed $1M

Bank loan needed or denied

Hiring decisions feel like guesses

Tax bill was a surprise

Bonding required for next contract

Major strategic decision pending

Owner in finance more than 20% of time

Key Lender Ratios

What Columbia Falls banks evaluate

Related Articles

Ready to scale past the ceiling?

406 Consulting Group — Columbia Falls & Flathead Valley

Schedule a ConsultationNot yet at the CFO stage?

Our bookkeeping services and controller services build the financial foundation that makes a future CFO engagement more effective — and less expensive to ramp up.