Construction Accounting in Columbia Falls, MT:

Job Costing, WIP, and Bonding Support

Columbia Falls contractors lose margin on every job without proper accounting. Job costing, WIP, cash flow, and bonding support for Flathead Valley contractors.

Construction accounting in Columbia Falls, MT is not bookkeeping with a hard hat on. It is a specialized financial discipline — and most Flathead Valley contractors are running it on tools designed for retail or service businesses. The result is the same every time: a company P&L that looks profitable while individual jobs quietly bleed margin, a WIP schedule that doesn't exist until the surety agent asks for one, and a bank line that runs dry in February because nobody modeled the winter cash gap in April.

This guide covers the complete construction accounting system for Columbia Falls contractors — job costing, WIP schedule management, cash flow and draw cycle planning, and the bonding-ready financials that determine your single-job limit and aggregate capacity. Whether you're a residential GC doing $800K in Flathead County or a commercial contractor chasing MDOT and school district work at $4M, the system is the same. The scale just changes what it costs you to run it wrong.

Table of Contents

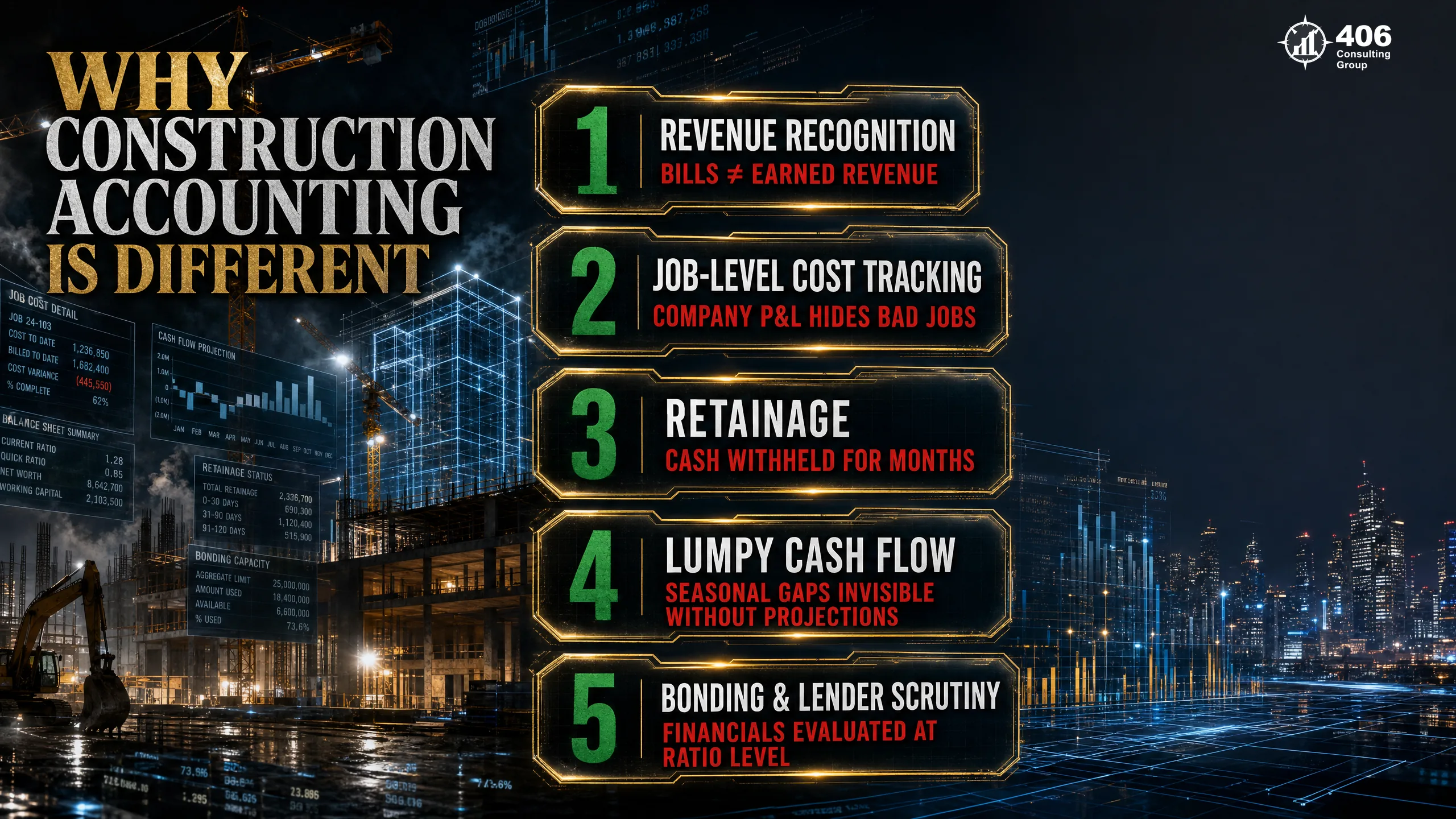

Why Construction Accounting Is Different from Standard Bookkeeping

Construction accounting in Columbia Falls, MT operates on a different set of rules than the bookkeeping software most Flathead Valley contractors are running. The five differences that matter most are not theoretical — each one translates into a specific financial failure that repeats every year until the system gets fixed.

Revenue recognition

Overstated income → unexpected tax billsA restaurant recognizes revenue when a meal is served. A contractor recognizes revenue as a project is completed — percentage-of-completion method. Billing a client $200,000 does not mean you have earned $200,000. If the job is 60% complete, you have earned $120,000. Recording the full invoice as revenue overstates income, makes your P&L unreliable, and surprises you at year-end with a tax bill based on money you haven't collected.

Job-level cost tracking

Margin leakage invisible until year-endEvery material purchase, labor hour, equipment charge, and subcontractor invoice must be allocated to a specific job. Without job-level tracking, you have a company P&L but no job P&L. You know the business made $180,000 last year — but you have no idea which jobs were profitable and which were disasters. By the time you figure it out, the bad patterns have already repeated on three more projects.

Retainage

Working capital understated → bonding reducedGeneral contractors and owners withhold 5–10% of each progress payment until project completion. On a $900,000 project, that is $45,000–$90,000 sitting in accounts receivable for months. A balance sheet that doesn't separate retainage receivable from current receivables understates working capital, misrepresents cash availability, and causes surety companies to understate your bonding capacity.

Lumpy seasonal cash flow

Cash crises that were predictable 6 months outColumbia Falls construction cash flow has a hard seasonal shape: work ramps April through October, billing follows with a 30–45 day lag, collections trail by another 30 days, and retainage doesn't land until punch list is cleared — sometimes February. Without a rolling 13-week cash flow projection, the winter gap is a surprise every year. It shouldn't be — it is structurally predictable from your backlog and payment terms.

Bonding and lender scrutiny

Denied bonding → locked out of public projectsSurety companies and commercial lenders evaluate construction financials at a level of detail most business owners don't expect. Working capital ratio, backlog-to-equity, and underbilling position are ratios your surety agent calculates before approving any single job over $500,000. Clean, construction-specific financials — prepared by a CPA — are a prerequisite for Flathead County public work, MDOT contracts, and school district projects.

The Columbia Falls, MT Construction Market

Columbia Falls sits at the eastern edge of the Flathead Valley corridor — between Kalispell's commercial core and the Glacier National Park gateway. That position creates a construction market with characteristics that don't appear in generic contractor guides: Glacier-driven tourism infrastructure work, a residential growth wave pushing east from Whitefish and Kalispell, Flathead County public works projects, and a subcontractor network with deep roots in timber and logging. Each of these creates specific accounting situations.

Glacier Tourism Infrastructure

Davis-Bacon + certified payrollLodge renovations, access road improvements, visitor center construction, and private resort development in the Glacier corridor. Federal Davis-Bacon prevailing wage applies to NPS-funded work. Seasonal construction windows are compressed — most Glacier-adjacent sites are inaccessible November through April.

Residential Growth Corridor

Construction lending + lien complianceColumbia Falls and the Hungry Horse / Martin City corridor are absorbing Flathead Valley residential growth. Custom homes, spec builds, and subdivision infrastructure. Draw schedules tied to construction lenders (Glacier Bancorp, First Security Bank of Bozeman, Mountain West Bank). Retainage on residential projects is less common but lien exposure is real.

Flathead County Public Works

Prevailing wage + bonding requiredCounty road maintenance and reconstruction, bridge work, school district capital projects (Columbia Falls School District, Flathead High School feeder projects), and fire district facilities. Montana prevailing wage applies to all. Certified payroll required weekly. Bonding typically required above $25,000.

MDOT Highway Work

MDOT bonding + certified payrollUS-2 corridor (the primary access route to Glacier) sees regular pavement, bridge, and drainage work. MDOT contracts are heavily bonded, require certified payroll, and typically mandate equipment and labor classifications at Davis-Bacon or Montana DLI prevailing wage rates.

Timber-Adjacent Construction

Workers' comp classificationMany Columbia Falls contractors emerged from the logging and timber industry — equipment-heavy operations with owner-operators and subcontractors who blur the employee/contractor line. Timber site clearing, logging road construction, and mill facility work creates specific workers' comp classification exposure.

Commercial & Industrial

AIA billing + subcontractor managementLight industrial, retail, and mixed-use commercial development driven by Flathead Valley population growth. Columbia Falls is developing commercial nodes along US-2. These projects typically involve GC-subcontractor relationships with retainage, lien waivers, and monthly AIA billing format.

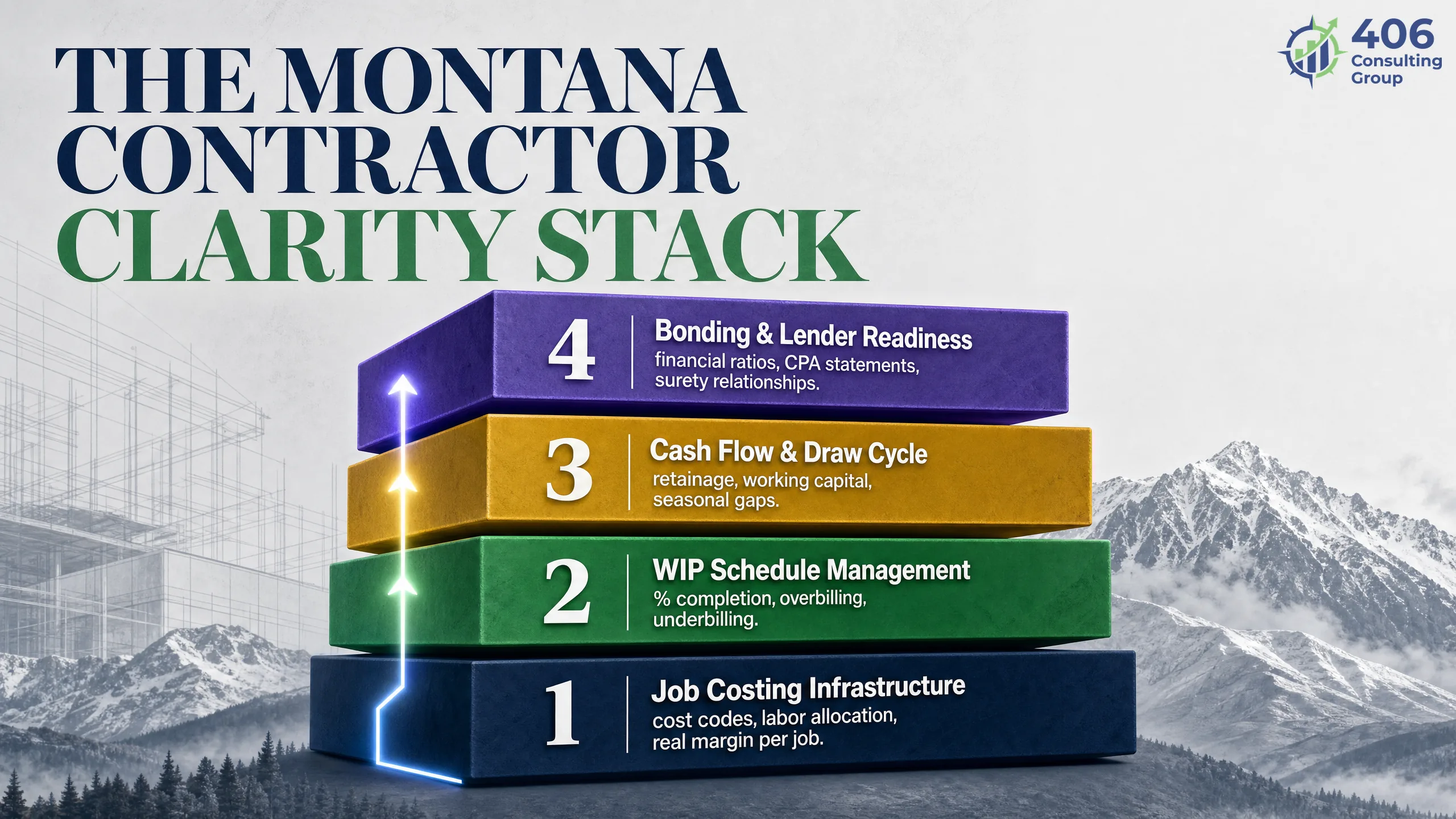

The Montana Contractor Clarity Stack: 4 Components of Construction Accounting

The Montana Contractor Clarity Stack organizes construction accounting into four sequential components. Each component builds on the one before it — you cannot produce a reliable WIP schedule without job costing data, you cannot manage cash flow without an accurate WIP position, and you cannot qualify for bonding without clean financials that reflect both. The stack works because it mirrors how surety companies and lenders evaluate your business: from the ground up.

Job Costing Infrastructure

Every pay period + every invoiceCost codes, labor allocation, equipment tracking, and subcontractor management at the job level. Produces a job-level P&L that shows real margin — not just company-wide average margin — on every project.

WIP Schedule Management

Monthly — before financial closePercentage-of-completion calculation, overbilling and underbilling position, revenue recognition. The WIP schedule is both a financial statement and a surety document — it must be current and accurate at all times.

Cash Flow & Draw Cycle

Rolling 13-week projectionDraw schedule management, retainage tracking, working capital gap modeling, and line-of-credit coordination. The document that prevents the February cash crisis from being a surprise in October.

Bonding & Lender Readiness

Annual + per-projectCPA-prepared financial statements, key ratio maintenance (working capital, quick ratio, backlog-to-equity), surety relationship management, and bank covenant compliance. The component that determines your access to public work.

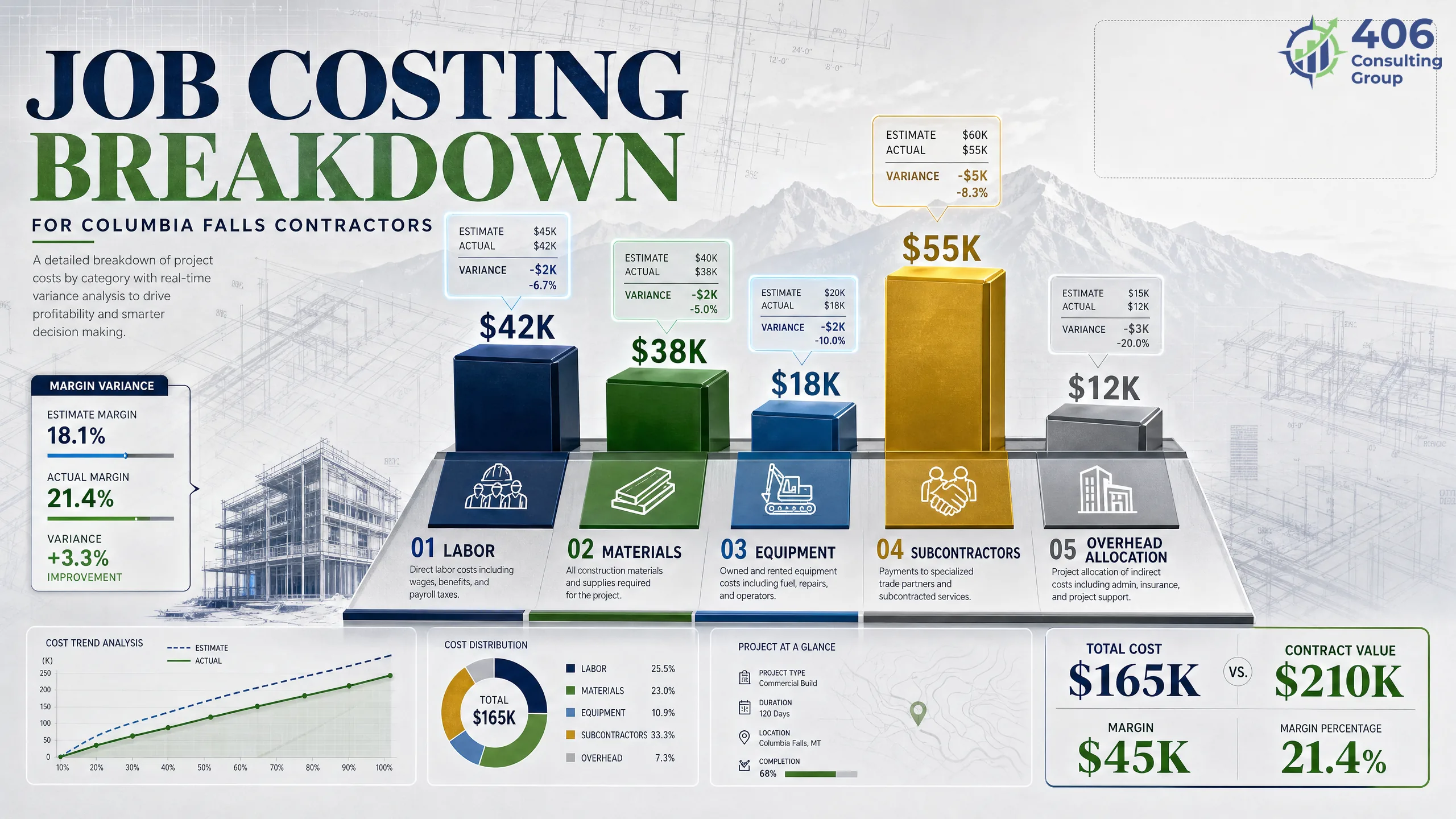

How Does Job Costing Work for Columbia Falls Contractors?

Job costing is the practice of allocating every dollar of cost — labor, materials, equipment, subcontractors, and overhead — to a specific project. A Columbia Falls contractor doing $2M in annual revenue across 15 projects does not have one business financially — they have 15 simultaneous businesses, each with its own margin. Job costing makes that visible in real time instead of at year-end.

Labor Cost Codes

Every hour of field labor allocated to a job — by trade, by crew, by phase. Includes base wages, payroll taxes, workers' comp premium, and fringe benefits. In Columbia Falls, drive time to remote Flathead County job sites is a real labor cost that must be captured per project, not absorbed into overhead.

Materials Cost Codes

Every lumber delivery, concrete pour, electrical supply order, and hardware purchase tied to a specific job number before the receipt hits the books. Materials purchased without a job code allocation are overhead by default — and invisible in your job margin analysis.

Equipment Cost Codes

Owned equipment charged to jobs at an internal rate (depreciation + fuel + maintenance ÷ hours). Rented equipment charged at invoice. Heavy equipment hours for Columbia Falls contractors doing site work, excavation, or timber clearing — logged per project. Without equipment job costing, high-equipment projects systematically understate true cost.

Subcontractor Cost Codes

Every sub invoice coded to the project and phase before payment. Match sub invoices against the executed subcontract — an invoice that exceeds the sub's approved contract value needs a change order before payment, not after. Electrical, plumbing, HVAC, and specialty subs are the most common source of unallocated costs in Flathead Valley construction.

Overhead Allocation

Indirect costs — insurance, vehicle costs, small tools, shop expenses — allocated to jobs using a predetermined overhead rate (typically % of direct labor or % of revenue). Overhead allocation is often skipped by small contractors, which means all of those costs hit the company P&L as unexplained overhead instead of job costs.

Job-Level P&L vs. Company P&L

Every job produces its own profit and loss statement: contract value, cost-to-date, projected final cost, projected margin, and margin variance vs. original bid. A company-level P&L shows aggregate performance. Job-level P&Ls show which project types, which clients, and which crew configurations actually make money — the only data that drives better bidding.

What job costing tells you that your P&L doesn't:Which project types have the highest margin. Which crew configurations are most efficient. Which clients routinely generate change orders that erode bid margin. Which seasons produce the best job-level returns. Job costing data is the only reliable input for next year's bidding strategy — without it, you're repricing based on instinct.

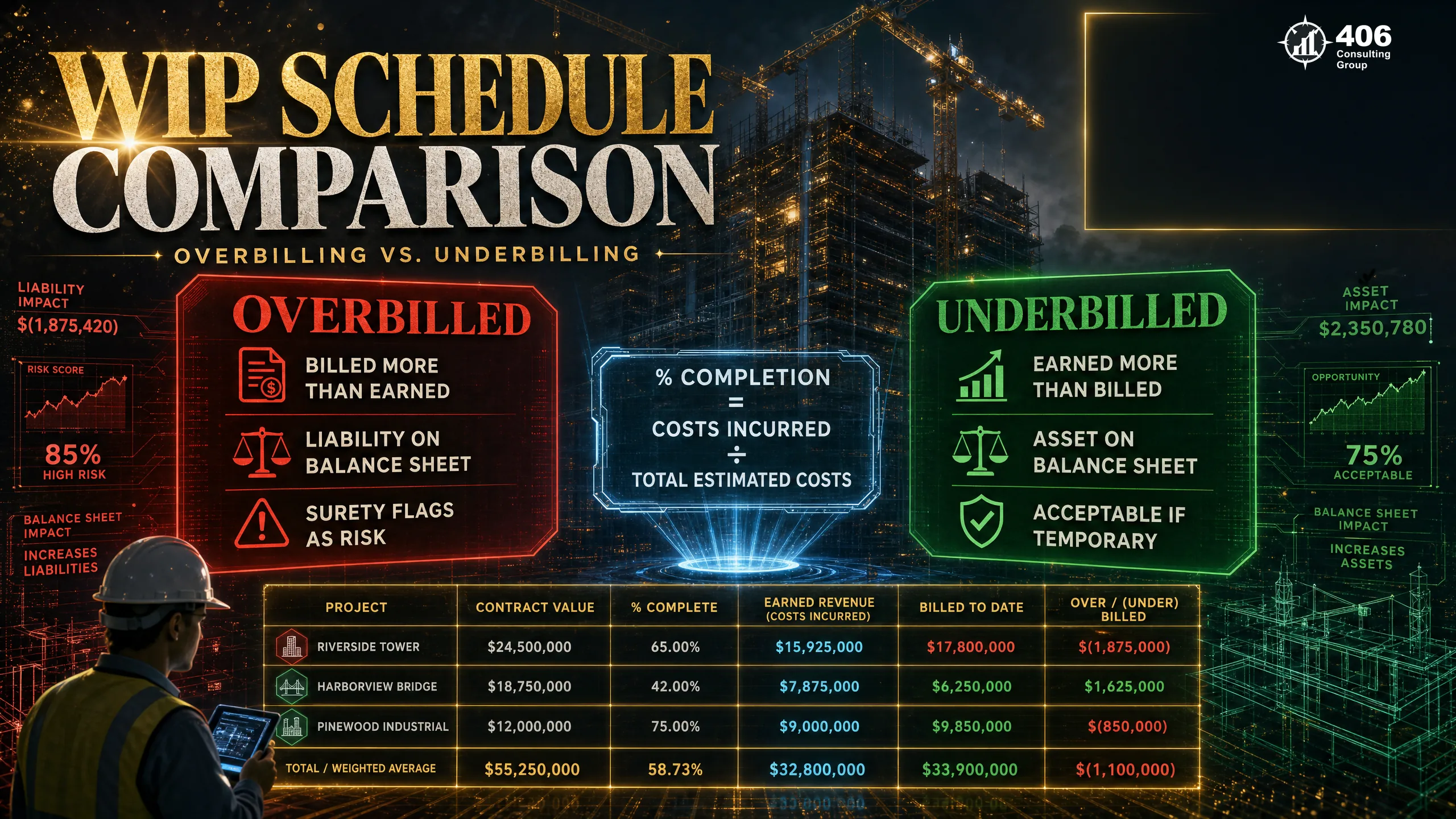

What Is a WIP Schedule and Why Do Montana Contractors Need One?

The WIP schedule — Work in Progress schedule — is the financial document that shows every active project's billing position at a point in time. Montana surety companies and commercial lenders require a current WIP schedule for any bonding or construction lending request. A contractor who cannot produce a WIP schedule within 48 hours of a surety request is a contractor who does not get bonded for public projects. The schedule is also the only reliable basis for revenue recognition on multi-month projects.

Percentage of Completion

Costs incurred ÷ Total estimated costsThe foundation of WIP accounting. If you have incurred $165,000 on a project with total estimated costs of $275,000, the project is 60% complete. Earned revenue = contract value × 60%. The percentage-of-completion method smooths revenue recognition across the project lifecycle and produces a P&L that reflects actual work performed — not just cash billed or collected.

Overbilling (Billing in Excess of Costs)

Billed > Earned RevenueWhen you have billed more than your percentage-of-completion warrants, the difference is overbilled. Overbilling is a liability — you owe the owner that work. Moderate overbilling is acceptable on fast-moving projects; systematic overbilling across a portfolio is a red flag for surety companies because it signals that cash is being used from future project revenue to fund current operations.

Underbilling (Costs in Excess of Billings)

Earned Revenue > BilledWhen you have earned more than you have billed, the difference is underbilled — an asset on your balance sheet. Temporary underbilling is normal when billing falls behind work performed. Chronic underbilling signals billing management problems: draws not submitted on time, change orders not billed, or project managers who don't understand the billing cycle. Each underbilled dollar is working capital you are loaning to the owner interest-free.

WIP Schedule as a Financial Statement

Required for bonding reviewThe WIP schedule is not an internal management report — it is a financial statement presented to sureties and lenders alongside your balance sheet and income statement. It must reconcile to your financial statements: total costs in the WIP must match costs booked in your accounting system, and billed amounts must match your AR. A WIP that doesn't reconcile raises immediate questions about the reliability of your entire financial package.

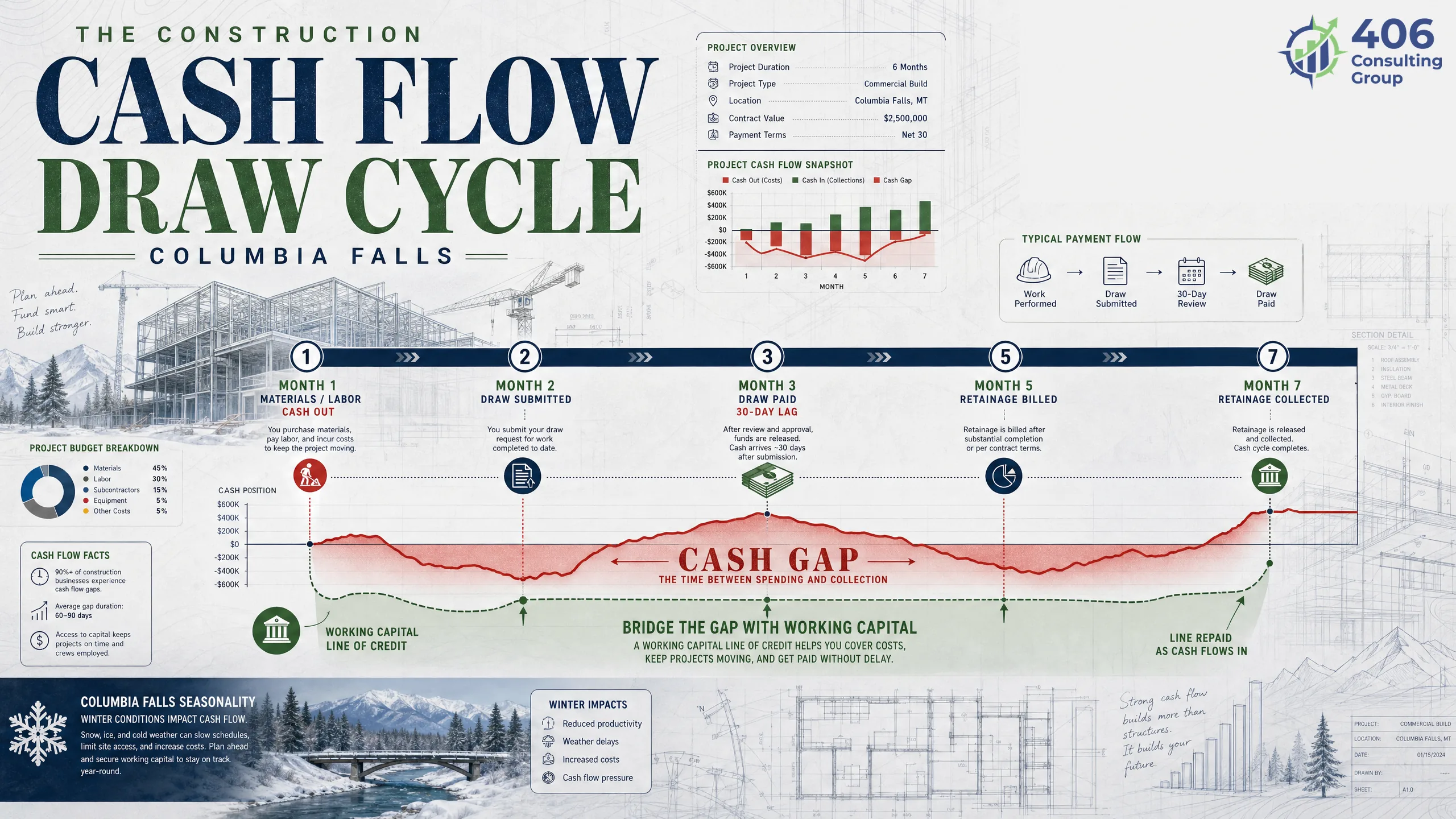

Component 3: Cash Flow & Draw Cycle Management

Cash flow management for Columbia Falls contractors means understanding that money flows out — for materials, labor, and equipment — weeks or months before it flows in from client payments. A contractor with a full backlog and strong margins can still fail in February if they didn't model the winter cash gap in April.

Draw Schedule Management

Monthly or milestoneDraw schedules define when you bill and when you collect. Commercial projects typically use monthly AIA G702/G703 pay applications. Residential projects use milestone-based draws tied to construction lender inspection. Submit every draw on time — a delayed draw is a delayed collection, and 30 days of delayed draws on a $500K project is $15,000–$25,000 of unnecessary cash gap at the busiest point in the season.

Retainage Tracking

Per projectRetainage — typically 5–10% withheld per payment — accumulates throughout a project and is released upon substantial completion and punch list. On a $1.2M project at 10% retainage, $120,000 is sitting in a client receivable that won't convert to cash until project closeout, potentially 6–9 months after the bulk of your costs were incurred. Track retainage receivable separately from current receivables — both on your balance sheet and in your cash flow projection.

Rolling 13-Week Cash Flow Projection

Weekly updateA rolling 13-week projection maps every cash inflow (upcoming draws, retainage releases, change order payments) and every cash outflow (payroll, material orders, sub payments, equipment payments, taxes) by week. It is the single most valuable cash management tool for a Columbia Falls contractor with 3–8 active projects. The projection doesn't prevent the winter gap — it makes the gap visible in July so you have time to arrange financing before it arrives in January.

Working Capital Line of Credit

Annual renewalA revolving line of credit — typically 10–15% of annual revenue — bridges the gap between costs incurred and payments collected. Glacier Bancorp, First Security, and Mountain West Bank all provide construction lines to qualified Flathead Valley contractors. The line is sized on your working capital ratio and financial statement quality. Contractors without a line of credit rely on vendor credit terms and payroll timing flexibility — neither is reliable.

Seasonal Cash Flow Planning

Q3 planning for Q1 gapMost Columbia Falls contractors have a structurally predictable winter slowdown: new starts drop in October, billing drops in November, collections drop in December and January, and payroll obligations for core crew continue year-round. Model the winter cash position every August using your backlog and payment terms. If the model shows a February deficit, arrange financing in September — not in January when the bank is looking at three months of declining revenue.

How Do Columbia Falls Contractors Qualify for Construction Bonding?

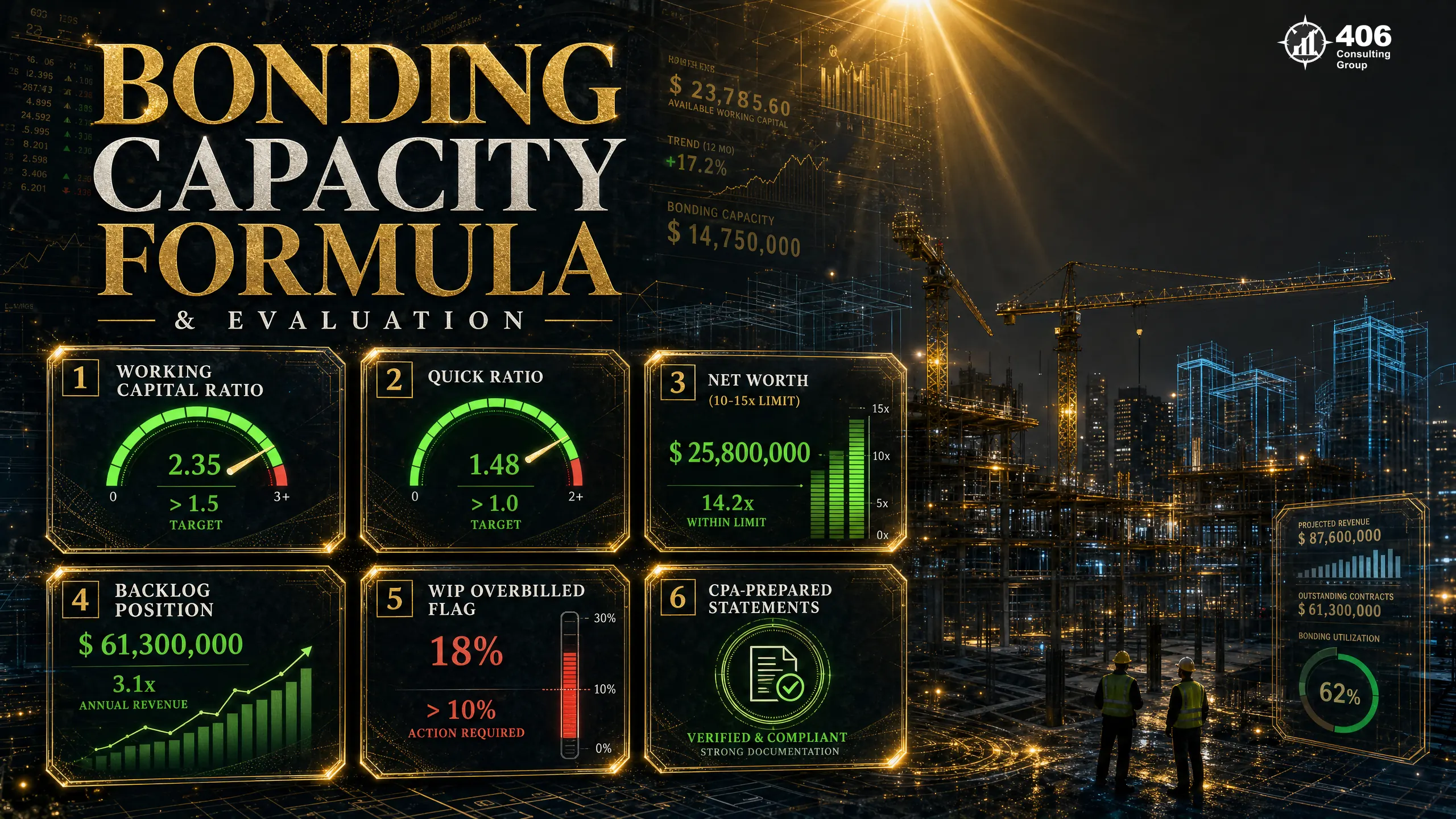

Bonding capacity determines which projects a Columbia Falls contractor can pursue — and which remain out of reach. Montana prevailing wage projects, MDOT contracts, Flathead County public works, and school district construction all require performance and payment bonds. A contractor without adequate bonding capacity is locked out of public work entirely. Bonding is not determined by relationships — it is determined by financial ratios.

Working Capital Ratio

Current Assets ÷ Current Liabilities

The primary liquidity test. Surety companies want to see that current assets cover current liabilities by at least 1.5×. Working capital below 1.2 signals operational stress; below 1.0 signals potential insolvency. Retainage receivable classified as current — when it will actually be collected in 60–90 days — inflates working capital artificially. Sureties who review regularly will reclass it.

Quick Ratio

(Cash + Receivables) ÷ Current Liabilities

A more conservative liquidity test that excludes inventory and prepaid assets. For contractors, the quick ratio is nearly identical to the working capital ratio since inventory is minimal. A quick ratio below 1.0 means you cannot pay current liabilities from liquid assets alone — a surety red flag for any single-job bond above $250,000.

Net Worth / Equity

Total Assets − Total Liabilities

The equity base directly determines aggregate bonding capacity. The rule of thumb: bonding capacity = 10–15× net worth. A contractor with $400,000 in equity can generally support $4M–$6M in aggregate bonds. To grow bonding capacity, equity must grow — through retained earnings, not owner distributions that strip cash from the business at year-end.

Backlog-to-Equity Ratio

Remaining Contract Value ÷ Net Worth

How much uncompleted work exists relative to equity. Excessive backlog relative to equity means the contractor is financially leveraged on uncompleted work — a default on one large project could wipe the equity base. Most sureties become cautious when backlog exceeds 12–15× net worth, regardless of the individual job size.

WIP Overbilling Position

Overbilled − Underbilled (portfolio)

A portfolio that is net overbilled means cash has been pulled forward from future project revenue. Moderate net overbilling is accepted; heavy net overbilling signals that cash from progress draws is funding overhead rather than project costs — a solvency signal. Net underbilling is preferred by sureties but may signal billing management problems.

CPA-Prepared Financial Statements

Compiled, reviewed, or audited

Self-prepared financial statements are insufficient for bonding above $500,000 per project. Compiled statements suffice for smaller bonds. Reviewed statements are required for most projects in the $1M–$5M range. Audited statements are required for large programs. The CPA preparing your construction statements must understand contractor accounting — a generalist firm misclassifying retainage or WIP creates a statement that sureties immediately question.

Related guides: WIP and Job Costing for Billings Contractors covers the WIP schedule in depth for contractors working larger commercial programs. Construction Accounting in Missoula, MT covers equipment depreciation and subcontractor management in detail.

Does Montana Prevailing Wage Apply to Columbia Falls Construction Projects?

Montana prevailing wage law (MCA § 18-2-401 et seq.) requires that workers on public construction contracts over $25,000 be paid at least the Montana Department of Labor prevailing wage rate for their trade classification in their county. In Flathead County, this applies to Flathead County road and bridge work, Columbia Falls School District construction, MDOT projects, and any project funded by state or local government.

Prevailing Wage Threshold

$25,000 contract valueAny public works construction contract exceeding $25,000 triggers Montana prevailing wage requirements. This threshold applies to the total contract value — a $30,000 parking lot at a county facility requires prevailing wage, even if a single subcontractor does the work.

Wage Rates by County and Trade

Set annually by MT DLIMontana DLI publishes prevailing wage rates by county and trade classification each year. Flathead County rates apply to Columbia Falls public projects. Rates differ by trade: carpenter, electrician, plumber, heavy equipment operator, and laborer rates are all distinct. Using the wrong classification — e.g., paying a carpenter at laborer rate — is a prevailing wage violation.

Certified Payroll Reports

Weekly — due to contracting agencyEvery contractor and subcontractor on a prevailing wage project must submit certified payroll reports weekly to the contracting agency (county, school district, MDOT). The report shows each worker's name, classification, hours worked, rate paid, and deductions. Submitting certified payroll is the contractor's responsibility — not the subcontractor's alone on projects where the GC holds the public contract.

Davis-Bacon for Federal Projects

NPS and FHWA-funded workGlacier National Park construction projects funded by the National Park Service use Davis-Bacon federal prevailing wage rates — different from Montana state prevailing wage. MDOT projects with FHWA funding also use federal Davis-Bacon rates. A contractor bidding Glacier-adjacent work must determine whether state or federal rates apply before the bid is submitted.

Accounting Impact

Higher labor cost assumptions requiredPrevailing wage work requires accounting systems that track hours by worker, by day, by project, and by trade classification simultaneously — not just total hours per job. Payroll software must be configured to produce certified payroll reports in the required format. Contractors who manually reconstruct certified payroll after the fact routinely make errors that trigger compliance reviews.

Payroll compliance for Columbia Falls public works contractors: See our guide on payroll compliance in Columbia Falls, MTfor the full picture on workers' comp classifications, certified payroll setup, and Montana DLI wage and hour obligations that apply alongside prevailing wage requirements.

Subcontractor Management & 1099 Compliance for Columbia Falls GCs

General contractors in Columbia Falls typically coordinate 3–8 specialty subcontractors per commercial project. Each of those relationships creates financial, compliance, and lien exposure that must be managed systematically — not project by project as problems arise.

W-9 Before First Payment

Collect a completed IRS Form W-9 from every subcontractor before issuing the first check. A W-9 provides the SSN or EIN needed for 1099-NEC filing. A sub who refuses to provide a W-9 requires 24% backup withholding on every payment — which creates reconciliation complexity and sub relationship friction. Collect it at contract signing, not at year-end.

Certificate of Insurance Verification

Every subcontractor must provide a current Certificate of Insurance showing general liability and workers' compensation before starting work. Montana requires workers' comp on all employees — if a subcontractor's workers' comp lapses mid-project, the GC's policy may become the backstop. Verify COIs before project start and at each policy renewal period.

1099-NEC Filing — January 31 Deadline

Any subcontractor paid $600 or more during the year receives a 1099-NEC by January 31. The same deadline applies for Copy A to the IRS. For a Columbia Falls GC with 12 active subs per year, this means 12 1099-NECs due simultaneously with W-2s, Q4 941, and 940. Start pulling sub payment totals from your accounting software in December — don't wait until January 28.

Lien Waivers

Collect conditional lien waivers from subcontractors upon each progress payment, and unconditional waivers upon final payment. In Montana, mechanics lien rights attach to the project when sub invoices go unpaid — even if the GC has already paid the owner. Lien waivers document the sub's release of that right. On commercial projects with lenders involved, lien waivers are a draw condition.

Subcontractor Pay Application Review

Verify that subcontractor pay applications reconcile to approved change orders and the executed subcontract. A sub who bills above their approved subcontract amount needs a GC-approved change order before payment — not an invoice that slides through because the project manager approved it verbally. Back payments against approved work scope protect your bonding position and your lien exposure.

Employee vs. Subcontractor Classification

Columbia Falls contractors with workers from timber and logging backgrounds frequently blur the line — equipment operators who work for one GC exclusively, on GC-owned equipment, under GC supervision, are employees under the IRS behavioral control test regardless of how they are paid. Misclassification creates FICA back-taxes, workers' comp back-premiums, and Montana DLI penalties averaging $25,000–$80,000 per reclassified worker over 2 years.

Year-End Tax Strategy for Columbia Falls, MT Contractors

Construction contractors have access to tax strategies that most generic small business tax guides never mention. The combination of heavy equipment, seasonal income, and multi-year project structures creates planning opportunities — and traps — that are specific to the industry.

Section 179 and Bonus Depreciation on Equipment

Q4 planning — before December 31Equipment purchased and placed in service before December 31 can be fully expensed under Section 179 (2026 limit: $2.56M under OBBBA) or 100% bonus depreciation (permanently restored under the One Big Beautiful Bill Act, signed July 2025). A Columbia Falls contractor buying a $180,000 excavator in December can deduct the full purchase price in the current tax year — rather than depreciating over 5–7 years. Timing matters: equipment must be placed in service, not merely ordered, before year-end.

Completed-Contract Method vs. Percentage-of-Completion

Method election — coordinate with CPASmall contractors averaging under $30 million in annual gross receipts over the prior 3 years may elect to use the completed-contract method (CCM) for long-term contracts — deferring all revenue and costs on a project until the project is substantially complete. For a Columbia Falls contractor finishing a large commercial project in February, CCM can defer $400,000+ of income from one tax year to the next. PCM is required for all contractors above the small contractor threshold.

S-Corp Reasonable Compensation Planning

September — before Q4 distributionsOwner-operators of S-Corps must pay themselves a reasonable salary for services rendered — the IRS scrutinizes S-Corp owners who take low salaries to minimize payroll taxes. For a Columbia Falls construction S-Corp with $350,000 in net income, reasonable compensation typically falls between $90,000 and $130,000 for an owner-operator GC. Underpaying triggers IRS reclassification of distributions as wages, with FICA penalties.

Cost Segregation on New Construction or Renovation

After project completion — before filingIf your company constructed or significantly renovated a building in the current year, a cost segregation study reclassifies portions of the real property cost into 5-, 7-, or 15-year personal property — accelerating depreciation and reducing current-year taxable income. For a Columbia Falls contractor who built a $600,000 shop facility, cost segregation may accelerate $150,000–$200,000 in depreciation into the first year.

Retirement Plan Contributions

Up to tax filing deadline + extensionsContractor owner-operators can shelter significant income through SEP-IRAs (25% of net self-employment income, up to $69,000 for 2024) or Solo 401(k)s (up to $69,000 employee + employer combined). Contributions must be made by the tax filing deadline, including extensions. A $69,000 SEP-IRA contribution by a contractor in the 24% federal bracket saves $16,560 in federal taxes.

8 Construction Accounting Mistakes Columbia Falls Contractors Make

These are the eight most common construction accounting failures among Flathead Valley contractors — each with what it costs and how to fix it.

No job costing system — using company P&L only

Consequence

Cannot identify which projects are profitable until year-end. Bad bidding patterns repeat every season.

Fix

Implement job cost tracking in QuickBooks Contractor or Sage 100 Contractor before the next project start. Retroactive costing is better than nothing but forward implementation is the goal.

Overbilling without tracking underbilled position across the portfolio

Consequence

Cash pulled forward from future revenue without visibility — bonding agent sees the overbilled position and reduces the aggregate limit.

Fix

Produce a WIP schedule monthly, reconcile to your balance sheet, and review overbilling/underbilling ratios before submitting any new bonding request.

Retainage not separated from current receivables on the balance sheet

Consequence

Working capital appears higher than it is. Surety and lender calculate working capital ratio against inflated current assets — then discover the overstatement and question the accuracy of all financial data.

Fix

Book retainage receivable as a separate balance sheet line item. It is a real asset — but not a current asset if it won't be collected for 6–9 months.

No cash flow projection — surprised by winter gap every year

Consequence

Emergency credit draws in January and February at maximum rates. Missed payroll for core crew in slow months. Owner injects personal funds into the business because there was no model to show the gap was coming.

Fix

Build a 13-week rolling cash flow projection updated weekly by your bookkeeper. Model the winter gap every August using your fall backlog and payment terms. Arrange the line of credit in September.

Misclassifying workers as subcontractors to avoid payroll taxes and workers' comp

Consequence

$25,000–$80,000+ per reclassified worker in back FICA taxes, workers' comp premiums, interest, and penalties. Montana DLI investigates construction misclassification regularly.

Fix

Apply the IRS three-factor test before any first 1099. Equipment operators working exclusively for one GC on GC-owned equipment under GC supervision are employees. When in doubt, W-2.

Using a non-construction bookkeeper or generic accounting software

Consequence

Retainage misclassified. WIP not tracked. Overhead not allocated. Job cost reports either don't exist or don't reconcile to the general ledger. Surety declines the bond package.

Fix

Use a bookkeeper with construction accounting experience and software designed for the industry (QuickBooks Contractor, Sage, Buildertrend, or Foundation). The cost differential is small relative to the financial statement accuracy improvement.

No WIP schedule — cannot produce one when surety requests it

Consequence

Bond denied. Contract opportunity lost. The surety agent moves to the next contractor on the bid list.

Fix

Produce a WIP schedule monthly regardless of whether bonding is currently needed. It takes 2–3 hours monthly to maintain and is immediately available when a bond opportunity arises.

Missing Section 179 and bonus depreciation on equipment purchases

Consequence

Equipment depreciated over 5–7 years when it could have been fully expensed in year one. Tax liability $20,000–$50,000 higher than necessary on a single equipment purchase.

Fix

Coordinate every major equipment purchase with your CPA before year-end — not after. Timing a $180,000 excavator purchase to December instead of January is a one-year tax deferral worth the cost of a phone call.

Frequently Asked Questions: Construction Accounting in Columbia Falls, MT

What accounting software do Columbia Falls contractors use for job costing?

The most common construction accounting platforms for Flathead Valley contractors are QuickBooks Desktop Contractor Edition, QuickBooks Online with a job cost add-on, Sage 100 Contractor, and Foundation Software. QuickBooks Contractor is the most widely adopted for contractors under $3M in annual revenue — it handles job costing, WIP reporting, subcontractor management, and certified payroll. Sage and Foundation scale better for larger multi-project contractors needing more granular cost code structures. Field management platforms like Buildertrend or CoConstruct integrate with QuickBooks and add project management, draw requests, and client communication to the accounting backbone.

What financial ratios do Montana surety companies look at for bonding?

Montana surety companies evaluate six primary ratios when determining bonding capacity for Columbia Falls contractors: (1) Working capital ratio (current assets ÷ current liabilities — target above 1.5); (2) Quick ratio (cash + receivables ÷ current liabilities — target above 1.0); (3) Net worth or equity base (determines aggregate limit — rule of thumb 10–15× net worth); (4) Backlog-to-equity ratio (remaining contract value ÷ net worth — below 15× preferred); (5) WIP overbilling position (net overbilled across portfolio); and (6) Profitability trend (3 years of income statements showing consistent or growing margins). These ratios are calculated from your CPA-prepared financial statements and WIP schedule.

How does the WIP schedule affect bonding capacity in Montana?

The WIP schedule directly affects bonding capacity because it is one of the three primary financial documents — alongside the balance sheet and income statement — that Montana surety companies use to evaluate a contractor's financial health. A WIP schedule showing heavy net overbilling (billed far more than earned across the portfolio) signals that cash from progress draws is funding operations rather than project costs — a solvency concern. A WIP schedule with large underbilled positions reduces working capital on the balance sheet. A WIP schedule that doesn't reconcile to the financial statements raises questions about the reliability of all the financial data presented.

Does Montana prevailing wage apply to Columbia Falls school district construction?

Yes. Montana prevailing wage law (MCA § 18-2-401 et seq.) applies to all public works construction contracts over $25,000 with any government entity — including school districts. Columbia Falls School District construction projects, Flathead County facility work, and any Columbia Falls city infrastructure project above the $25,000 threshold all require prevailing wage payment and certified payroll reporting. The applicable wage rates are the Flathead County rates published annually by the Montana Department of Labor and Industry. Certified payroll reports must be submitted weekly to the contracting school district or county.

What is the difference between job costing and standard bookkeeping for contractors?

Standard bookkeeping records what the business spent and received in aggregate — a company-level view. Job costing adds a layer of allocation: every dollar of cost is attributed to a specific project, phase, and cost code before it is recorded. The result is a job-level profit and loss statement for every active project, showing original estimated margin vs. actual margin to date vs. projected final margin. Standard bookkeeping tells you whether the company made money last year. Job costing tells you which projects made money, which didn't, and why — the only data that produces better bids, better crew assignments, and better project selection next year.

How do Columbia Falls contractors qualify for larger bonding limits?

To qualify for larger bonding limits — both single-job and aggregate — Columbia Falls contractors need to systematically grow the financial metrics that surety companies measure. The most direct levers are: (1) Retain earnings rather than distributing all profit — equity growth directly increases bonding capacity; (2) Improve working capital ratio by managing accounts payable terms and reducing short-term debt; (3) Produce CPA-reviewed or audited financial statements rather than compiled or self-prepared statements — reviewed statements qualify for higher bond limits; (4) Maintain an accurate, current WIP schedule that reconciles to your financials; and (5) Build a multi-year relationship with a surety agent who understands Flathead County construction — surety is a relationship business, and agents advocate for contractors whose financial management they trust.

External Resources

Columbia Falls, MT

Construction Accounting Built for Flathead Valley Contractors

406 Consulting Group provides job costing setup, WIP schedule management, bonding-ready financial statements, and year-end tax strategy for Columbia Falls construction companies. All four components of the Contractor Clarity Stack.

Montana Contractor Clarity Stack

4 components — build them in order

Job Costing Infrastructure

Cost codes, labor, equipment, subs per job

WIP Schedule Management

% complete, overbilling, underbilling

Cash Flow & Draw Cycle

Retainage, 13-week projection, LOC

Bonding & Lender Readiness

Ratios, CPA statements, surety relationships

Bonding Ratio Quick Reference

Related Guides

External Resources