Expert Accounting for Missoula, MT

Construction Companies

Missoula construction companies lose margin on every job without proper accounting. The complete guide to job costing, WIP, cash flow, and tax strategy for Montana contractors.

Construction accounting in Missoula, MT is a specialized discipline — and most Missoula contractors are running it wrong. Standard bookkeeping records what happened. Construction accounting tells you whether you're making money on each job before it's too late to do anything about it. That distinction costs Montana contractors an average of 4–8% of gross revenue every year they get it wrong.

This guide covers the complete financial system for Missoula construction companies: job costing, WIP accounting, cash flow management, prevailing wage compliance, equipment depreciation, bonding capacity, and what Missoula lenders actually want to see. Whether you're a $800K residential GC or a $6M commercial contractor, the system is the same — only the scale changes.

Table of Contents

Why Construction Accounting Is a Different Animal

Construction accounting is different from standard business accounting in five fundamental ways. A bookkeeper trained on retail or service businesses will get every one of these wrong — and the errors compound monthly into significant margin loss.

Revenue recognition

Overstated income → unexpected tax billsA restaurant recognizes revenue when a meal is served. A contractor recognizes revenue as a project is completed — percentage-of-completion method. Billing a client $200,000 does not mean you've earned $200,000. If the job is 60% complete, you've earned $120,000. Recording the full invoice as revenue overstates income and makes your P&L unreliable.

Job-level cost tracking

Margin leakage invisible until year-endEvery material, labor hour, equipment charge, and subcontractor invoice must be allocated to a specific job. Without job-level cost tracking, you have a company P&L but no job P&L — you know the business made $180,000 last year but you have no idea which jobs were profitable and which were disasters.

Retainage

Working capital understated → bonding capacity reducedGeneral contractors and owners withhold 5–10% of each progress payment until project completion. That withheld amount is a real asset — money owed to you — but it sits in accounts receivable for months. A balance sheet that doesn't separate retainage receivable from current receivables understates working capital and misrepresents cash availability.

Multi-phase cash timing

Cash crises that were visible 6 months outConstruction cash flow is inherently lumpy. Materials purchased in March. Work performed April through June. Billing submitted June 30. Payment received 30–45 days later. Retainage released in October after punch list. A Missoula framing contractor might do $900,000 in billings between April and September and collect it between June and December. Without a rolling cash flow projection, the winter gap is a surprise every year.

Bonding and lender scrutiny

Denied bonding → locked out of public projectsSurety companies and commercial lenders evaluate construction financials at a level of detail most business owners don't expect. Working capital ratio, backlog-to-equity ratio, and underbilling position are metrics your banker at First Interstate or your surety agent at a regional bonding company will calculate before you get approved. Clean, construction-specific financials are a prerequisite for growth capital.

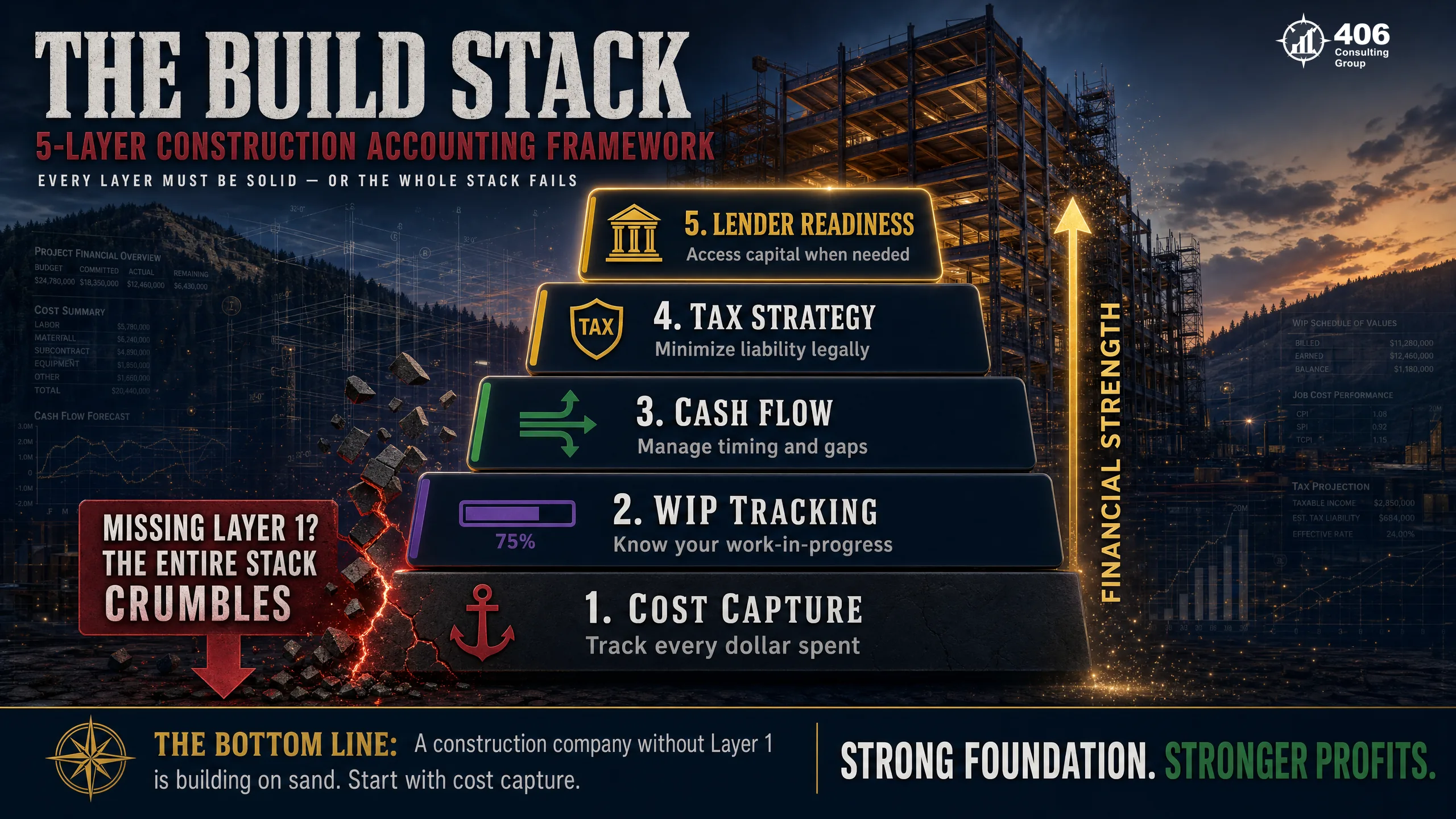

The Build Stack: 5 Layers Every Missoula Contractor Needs

The Build Stack is the five-layer financial system that separates contractors who grow from contractors who grind. Each layer depends on the one below it. You cannot have reliable WIP tracking without job costing. You cannot have accurate cash flow projections without reliable WIP. You cannot satisfy a lender without accurate cash flow history. The stack only works if it's complete.

Cost Capture

Every cost allocated to a job at the point of incurrence — not at the end of the month, not at year-end. Labor hours coded to a job on the timesheet. Material invoices assigned to a job number at the time of purchase. Subcontractor invoices posted to the job the day they arrive.

Without it: No job-level margin visibility. You learn you lost money on a job after it's over.

WIP Tracking

A monthly WIP schedule that shows for every active job: revised contract value, estimated cost to complete, percentage complete, revenue earned to date, and overbilling or underbilling position. Produced within 10 days of month-end without exception.

Without it: Revenue and income are meaningless. You're reporting what you billed, not what you earned.

Cash Flow

A rolling 90-day cash flow projection built from actual receivables, retainage schedule, subcontractor obligations, payroll calendar, and committed material orders. Updated monthly. Validated against bank balance.

Without it: Winter cash gaps ambush you. Equipment purchases happen at the wrong time. Payroll stress is constant.

Tax Strategy

Quarterly coordination between your bookkeeper and tax preparer to time depreciation elections, equipment purchases, retirement contributions, and estimated tax payments. Decisions made from current-year book data — not from a reconstruction in March.

Without it: You miss Section 179 elections. Estimated taxes are wrong. Your tax preparer is cleaning up your books instead of advising you.

Lender Readiness

Financial statements that a commercial lender or surety underwriter can read and underwrite in a single meeting. Consistent with tax returns. Balance sheet that separates retainage, current receivables, and equipment. Working capital ratio, DSCR, and backlog-to-equity clearly calculable.

Without it: Equipment financing denied. Bonding capacity capped. SBA loan delayed by months.

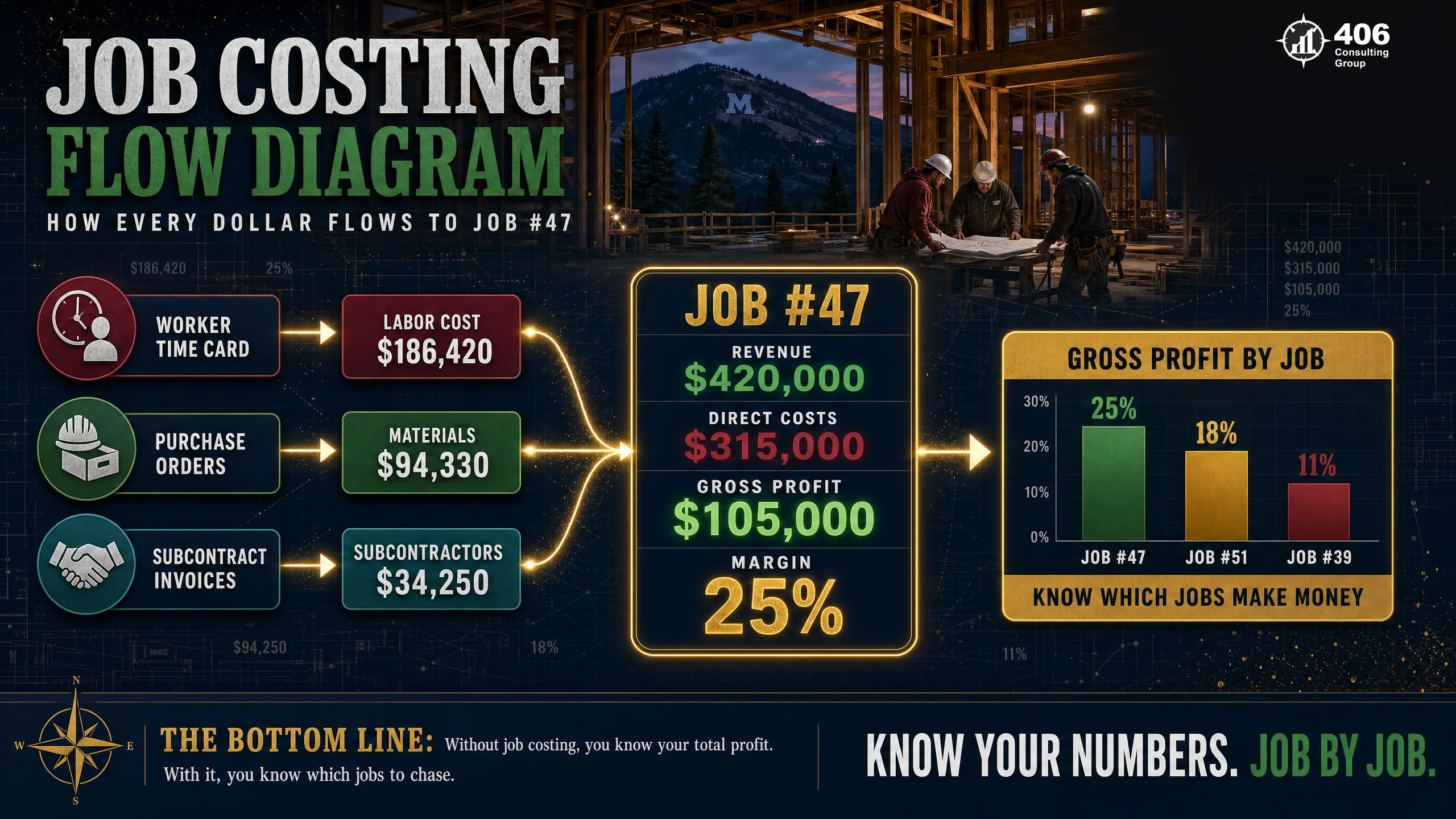

Job Costing for Missoula Contractors: The Foundation of Profitable Work

Job costing is the practice of tracking every cost — labor, materials, subcontractors, equipment, and overhead allocation — against a specific job or project. It is the foundation of the Build Stack, and without it, every financial number above it is unreliable.

Labor Costs

- Timesheets coded to job number daily — not weekly reconstructions

- Labor burden included: payroll taxes (7.65% employer FICA), workers comp premium, benefits

- Foreman time split by project when supervising multiple jobs

- Overtime flagged at job level — critical for prevailing wage projects

Materials Costs

- Purchase orders issued with job number — materials coded at PO creation, not at delivery

- Lumber, concrete, and electrical materials assigned to job at point of order

- Unused materials returned or transferred between jobs recorded in books

- Vendor invoices reviewed against PO before posting — quantity variances caught immediately

Subcontractors Costs

- Each sub invoice coded to the job and subphase (framing, plumbing, electrical, etc.)

- Sub invoices approved against the subcontract scope before payment

- Retainage withheld from sub payments tracked as a payable

- 1099 information (EIN, legal name, address) captured on W-9 before first payment

What job costing produces: a job-level P&L

| Line Item | Budget | Actual | Variance |

|---|---|---|---|

| Contract Value | $420,000 | $420,000 | — |

| Labor | $110,000 | $127,400 | -$17,400 |

| Materials | $98,000 | $94,200 | +$3,800 |

| Subcontractors | $85,000 | $85,000 | $0 |

| Equipment | $18,000 | $21,500 | -$3,500 |

| Overhead Allocation | $24,000 | $24,000 | $0 |

| Total Direct Costs | $335,000 | $352,100 | -$17,100 |

| Gross Profit | $85,000 | $67,900 | -$17,100 |

| Gross Margin | 20.2% | 16.2% | -4.0% |

Labor ran $17,400 over budget — visible at midpoint, not at closeout. With job costing, this was flagged at Week 6. Without it, discovered at year-end.

What I see consistently with Missoula contractors:The labor variance is almost always where the margin disappears. A framing crew that runs 15% over on labor across five jobs in a year is the difference between a profitable company and a breakeven company. Job costing makes that visible at the job level, not at the annual P&L level where it's already too late.

WIP Accounting: Recognizing Revenue the Right Way

WIP (Work in Progress) accounting is the method by which contractors recognize revenue as work is performed — not as invoices are issued. It is required for accurate financial reporting under GAAP, expected by surety underwriters, and the only way to know whether a project is trending profitable or toward a loss before it closes.

Overbilling (Billing in Excess)

LiabilityYou have billed more than you have earned based on percentage complete. The excess is a liability — revenue you've collected but haven't yet performed. Overbilled positions look good on a cash flow basis but are dangerous: if the project stops or goes over budget, you may owe money back.

Contract: $500K | % Complete: 40% | Revenue Earned: $200K | Billed to Date: $260K | Overbilling: $60K (liability)

Underbilling (Costs in Excess)

AssetYou have earned more revenue than you have billed. The underbilled amount is an asset — money you have earned but not yet invoiced. Underbilled positions indicate slow billing, which creates cash flow pressure even when the job is going well.

Contract: $500K | % Complete: 60% | Revenue Earned: $300K | Billed to Date: $240K | Underbilling: $60K (asset)

The WIP schedule: what it looks like in practice

A complete WIP schedule is produced monthly and shows every active job side by side: contract value, estimated cost at completion, costs incurred to date, percentage complete, revenue earned, billed to date, and overbilling or underbilling. The total overbilling on the schedule appears as a current liability on the balance sheet. The total underbilling appears as a current asset.

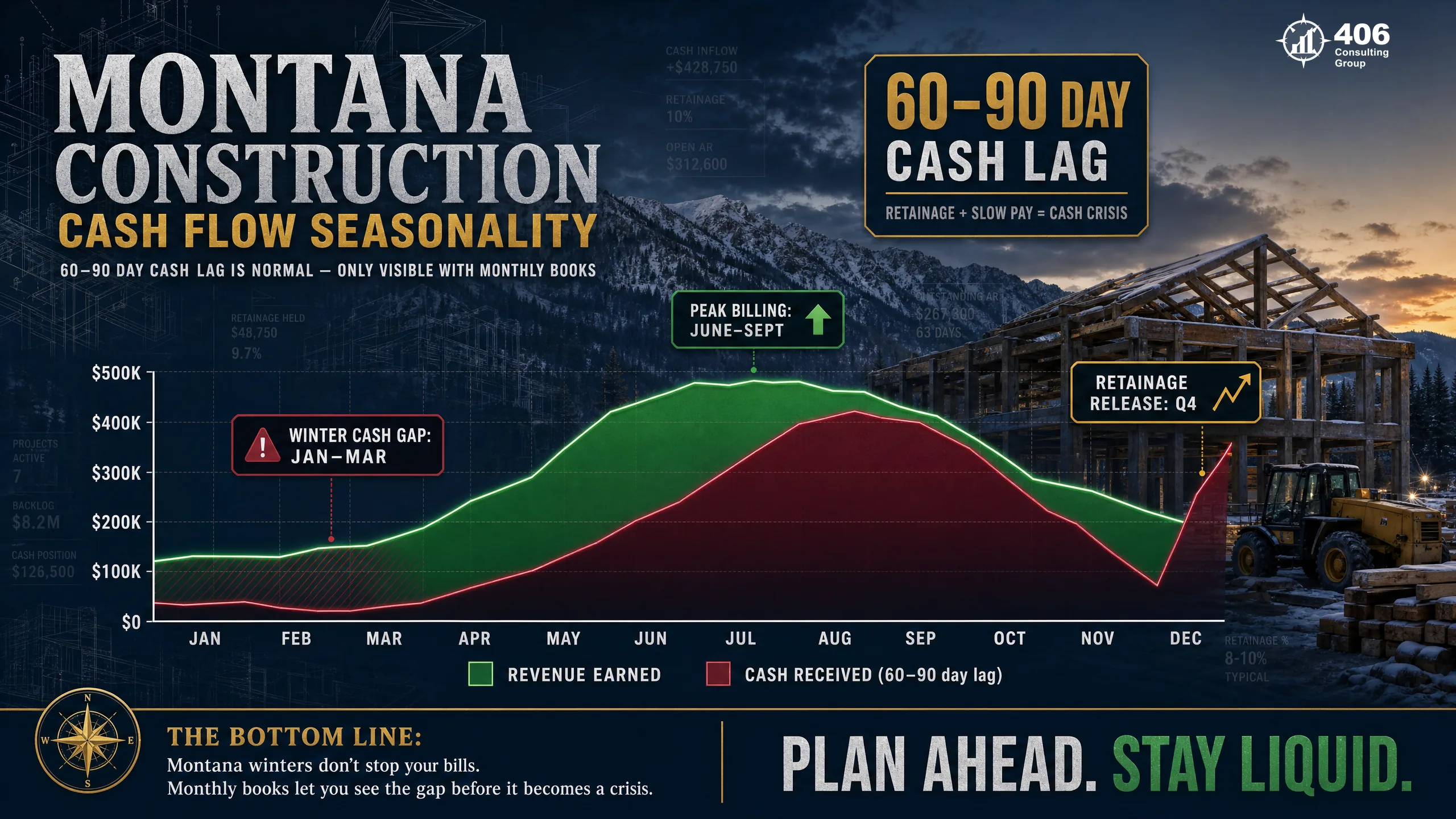

Cash Flow Management for Montana Construction: The Seasonal Reality

Missoula's construction season runs roughly April through October — 7 months of peak activity and 5 months of significantly reduced cash inflows. Contractors who manage cash flow based on their bank balance instead of a projection hit the same crisis every February: payroll is due, materials for spring projects need to be ordered, equipment loans are current, and the account is thin.

The billing-to-collection lag

A Missoula contractor who submits a $95,000 draw on June 30 on a commercial project can reasonably expect payment on or around August 5 — 35 days later. On a GC-managed project, the owner pays the GC first, who pays subs on their own schedule. Retainage on that same draw (typically 10%) isn't released until October or November at the earliest. That means $9,500 of every $95,000 draw is tied up for 4–6 months. A contractor with three active projects has significant capital locked in retainage all summer.

Material pre-purchase timing

Lumber, concrete, and roofing material prices in Western Montana fluctuate seasonally and with supply chain conditions. Contractors who lock in material pricing in February for spring projects need cash to do it — but February is the middle of the winter cash gap. Without a 90-day rolling cash flow projection built in October, that February purchase strains the line of credit unexpectedly.

Payroll continuity through winter

Retaining key employees through winter is essential for a Missoula contractor in a tight labor market. A skilled concrete finisher or electrician who can't count on a paycheck in January will find one elsewhere. Keeping core crew employed through winter requires cash reserved specifically for that purpose — visible only through a projection built in fall.

The rolling 90-day projection

A rolling 90-day cash flow projection starts with the current bank balance, adds all expected collections (receivables, draw schedule by project, retainage release dates), subtracts all committed outflows (payroll by date, sub payments by schedule, material orders, equipment loans, tax deposits), and produces a day-by-day cash position for the next 90 days. Updated monthly. Validated against actual bank balance. The gaps this reveals are actionable — draw the line of credit in November, not in February.

Payroll, Prevailing Wage & Workers Comp for Montana Contractors

Construction payroll is more complex than standard business payroll. Multiple trade classifications, prevailing wage requirements on public projects, workers compensation rates that vary dramatically by trade, and the dual obligation to track labor at the job level while complying with federal and Montana payroll requirements — all of it runs through your books monthly.

Montana Prevailing Wage

Public projects- 1Montana's Prevailing Wage Law (MCA 18-2-401) requires contractors on state-funded public works projects to pay craft workers the prevailing wage rate for their trade in the applicable county — Missoula County rates are set annually by the MT Dept. of Labor

- 2Covered projects include: school construction, university buildings (UM campus), city/county infrastructure, state highway work, and any project with state or federal funding

- 3Certified payroll records (WH-347 or Montana equivalent) must be submitted weekly to the awarding agency — showing each employee, trade classification, hours worked, and rate paid

- 4Misclassifying a journeyman carpenter as a laborer to pay a lower prevailing rate is one of the most audited violations in Montana construction — penalties include back wages plus interest and potential debarment from future public projects

Workers Compensation — Trade Classification

Montana State Fund- 1Workers compensation premiums are calculated on payroll by trade classification — rates vary dramatically: a general laborer might be 8–12% of payroll while a roofing worker is 18–25%

- 2Every employee must be assigned to the correct Montana State Fund classification code for their primary work — misclassification (coding a roofer as a laborer) creates retroactive premium liability at annual audit

- 3Annual payroll audit: Montana State Fund compares actual payroll by classification to your estimated payroll at policy inception — underpayment creates a retroactive bill due immediately, typically in March or April

- 4Your books must capture gross wages by employee and classification monthly to project the annual audit outcome — surprises are always more expensive than preparation

Multi-Trade Payroll Complexity

All contractors- 1A GC with carpenters, laborers, operators, and foremen processes payroll at different rates, different workers comp classifications, and potentially different prevailing wage rates if some workers are on public projects

- 2Montana income tax withholding applies to all W-2 employees at graduated rates — must reconcile to W-2s at year-end

- 3FICA (7.65% employer match) and FUTA must be tracked by employee and deposited on the IRS schedule — construction payroll volumes often trigger semi-weekly deposit requirements

- 4The payroll journal must post labor to the correct job at the correct classification rate to feed job costing — a payroll system that doesn't integrate with job cost accounting requires a manual bridge that is both time-consuming and error-prone

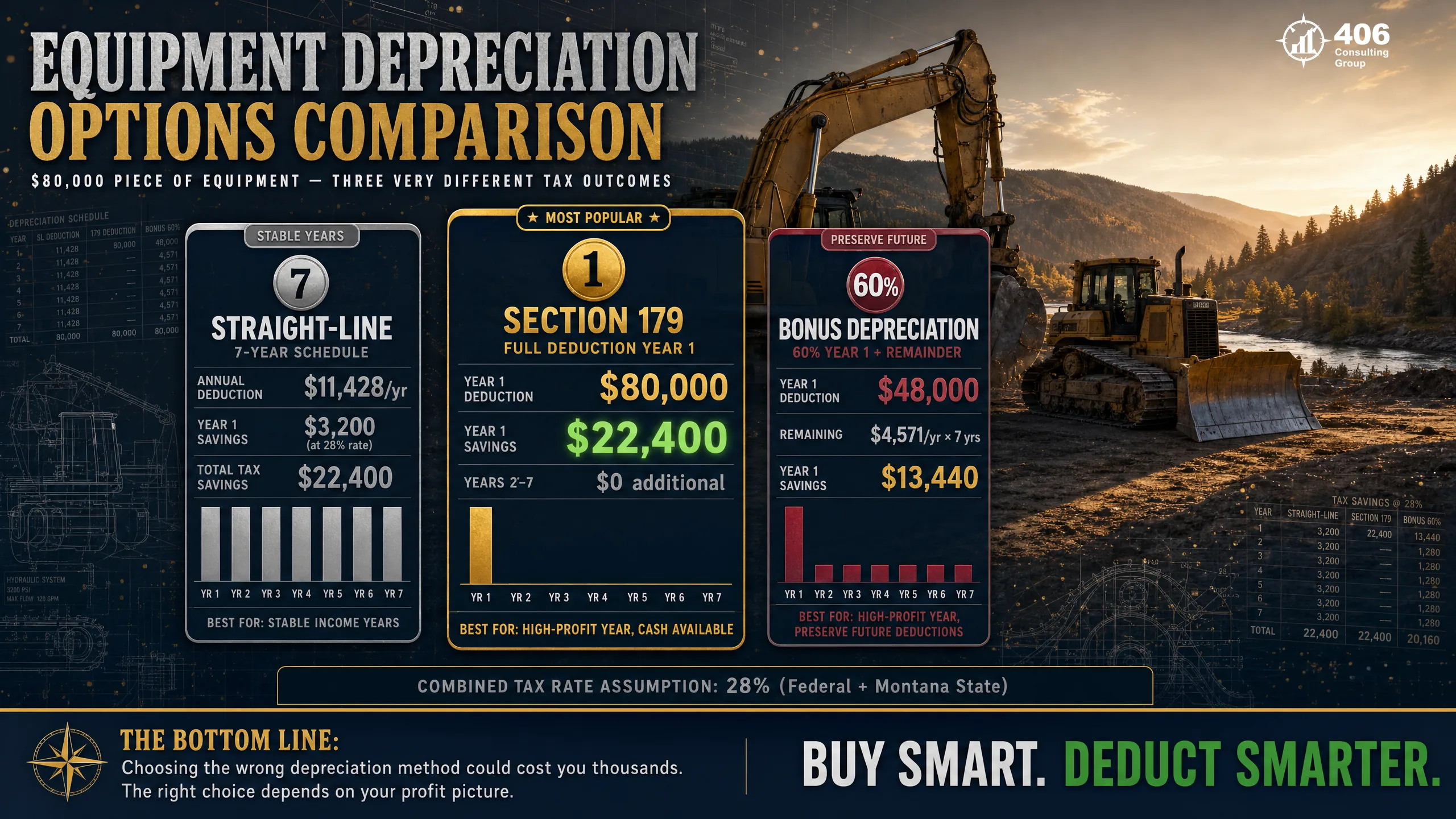

Equipment Accounting & Depreciation for Montana Contractors

Equipment is the largest asset on most Missoula contractors' balance sheets and the source of the largest annual tax decisions. Getting equipment accounting right means more than recording the purchase — it means choosing the right depreciation method, allocating equipment cost to jobs correctly, and maintaining a balance sheet that accurately reflects equipment value for bonding and lending purposes.

Straight-Line

5–7 year life$80,000 excavator ÷ 7 years = $11,429/year

Best for:

Stable income years; when you want consistent deductions without depleting future depreciation

Trade-off:

Smallest first-year deduction — lowest tax savings in Year 1

Section 179

Full Year 1 expensing$80,000 excavator expensed entirely in Year 1 = $80,000 deduction

Best for:

High-profit years when you need maximum deductions immediately; equipment that will be replaced in 3–5 years

Trade-off:

Depletes future depreciation — Years 2–7 have no deduction on this asset

Bonus Depreciation

100% (OBBBA — permanent)$80,000 × 100% = $80,000 Year 1 deduction

Best for:

Any year — full expensing is now permanent under OBBBA (July 2025). Especially powerful in high-profit years to eliminate taxable income quickly.

Trade-off:

Depletes future depreciation — Years 2–7 have no deduction on this asset. Consider implications for bonding capacity and lender financials.

Equipment cost allocation to jobs

Equipment used on specific projects should be charged to those jobs at an internal rate — either an hourly rental rate based on ownership cost, or by allocating actual operating costs (fuel, maintenance, depreciation) proportionally. Without job-level equipment charges, your job P&L understates true project cost and your equipment is essentially subsidizing jobs without visibility. A Missoula excavation contractor with a $280,000 excavator operating 1,200 hours per year has a real equipment cost of $23/hour or more — that cost belongs on each job's cost report.

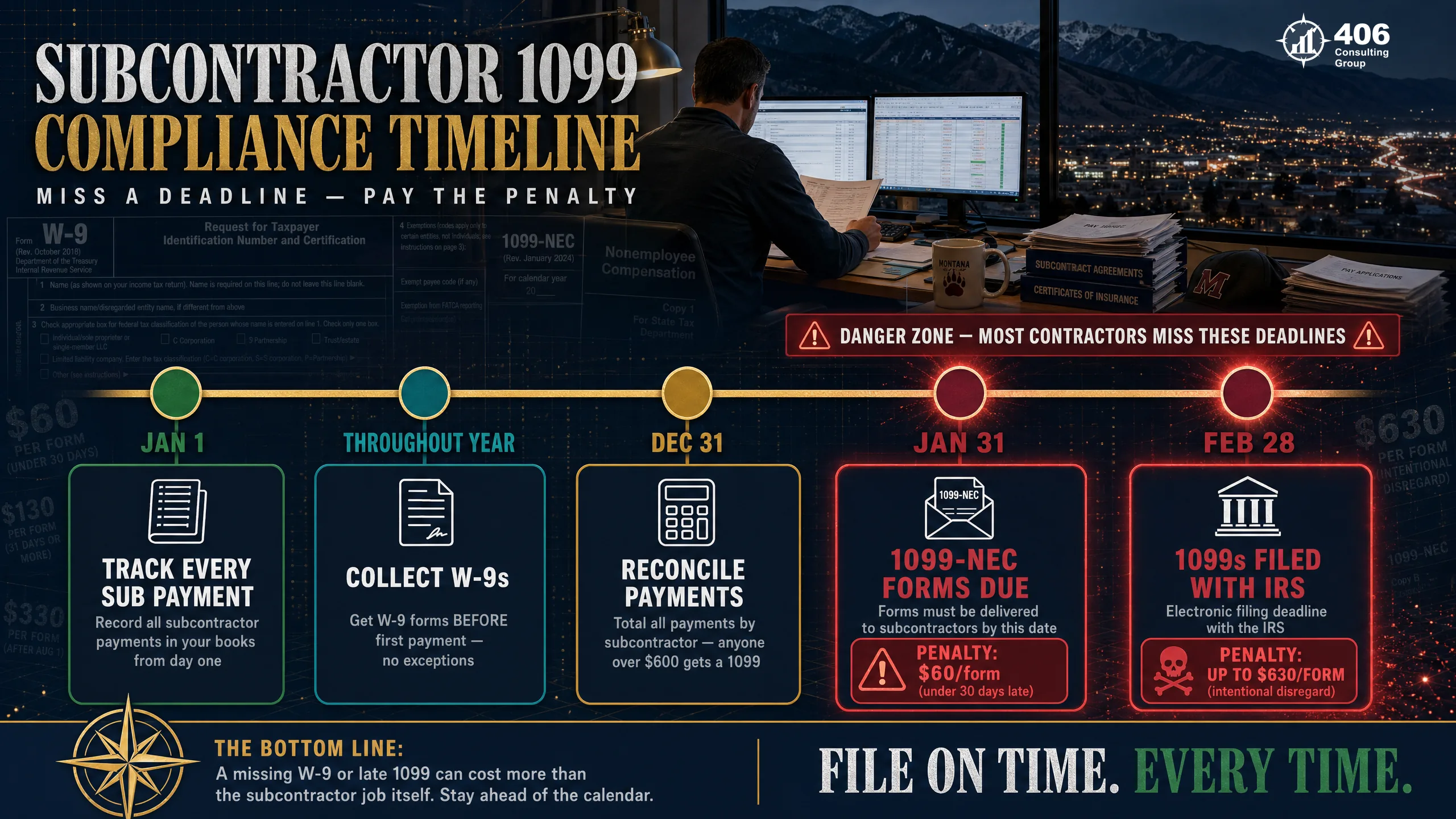

Subcontractor Management & 1099 Compliance

Most Missoula GCs and larger specialty contractors use subcontractors extensively. Subcontractor management has two financial dimensions: cost tracking (capturing sub costs at the job level in real time) and compliance (1099-NEC filing, worker classification, and sub retainage tracking).

W-9 before first payment — no exceptions

The W-9 captures the subcontractor's legal name, EIN or SSN, and address. Without it, you cannot produce a 1099-NEC in January. Chasing subs for W-9s in January is a losing proposition — some will be unreachable, some will have moved, some will refuse. Make it a contract condition: no W-9 on file, no first check issued.

Track cumulative payments throughout the year

Every payment to every sub is posted to their vendor record with job coding. At year-end, pull the vendor payment summary — every sub paid $600 or more gets a 1099-NEC. The IRS deadline is January 31. A business that tracked payments all year produces 1099s in 90 minutes. A business that didn't tracks them over two weeks in January — with errors.

Sub retainage as a separate payable

When you withhold 5–10% retainage from sub payments, that amount is a liability — money you owe but haven't paid. It belongs in accounts payable as 'sub retainage payable,' not lumped with current A/P. Misrepresenting retainage payable overstates working capital and creates problems at bonding renewal when the surety reconciles the balance sheet.

Employee vs. contractor classification

Montana applies the same IRS behavioral and financial control tests used federally. The key questions: Does the company control how and when the worker performs services (behavioral control)? Does the company control the financial aspects of the work — set the rate, provide tools, reimburse expenses (financial control)? Is there a written contract and does the worker perform services for multiple clients? Misclassifying an employee as a 1099 sub avoids payroll taxes in the short term and creates liability for all unremitted taxes plus penalties retroactively. Montana DOR and IRS both audit this actively in the construction sector.

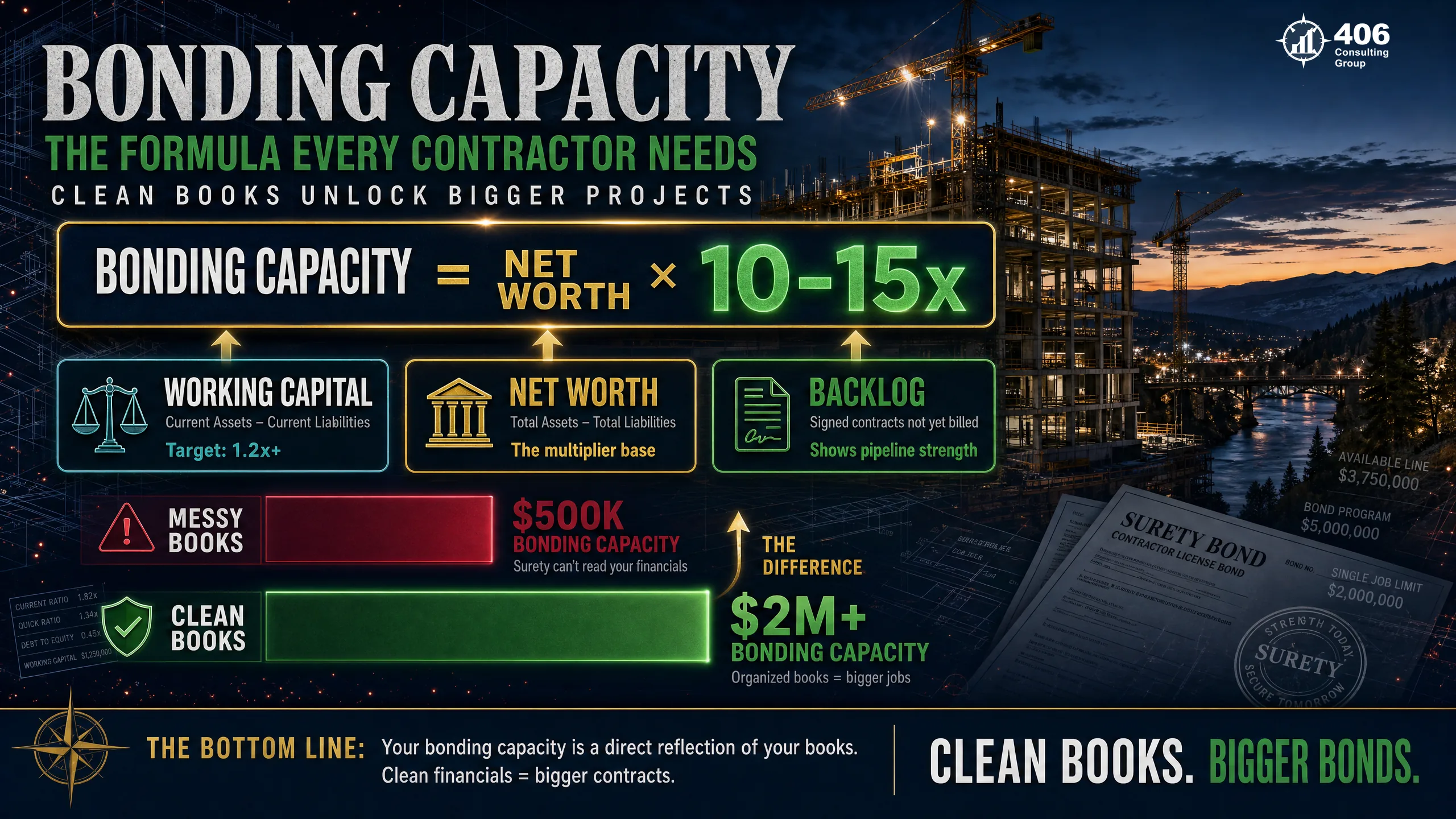

Bonding: How Your Books Determine Your Bonding Capacity

Surety bonding capacity — the maximum value of projects a contractor can bond — is directly calculated from the financial statements your books produce. A Missoula contractor who wants to bid on UM campus projects, City of Missoula infrastructure work, or Missoula County school construction needs bonding. And bonding capacity is a financial metric, not a relationship metric.

Working Capital

Ratio of 1.2x or betterCurrent Assets − Current Liabilities

Surety underwriters treat working capital as the primary liquidity indicator. A contractor with $380,000 in current assets and $290,000 in current liabilities has a working capital ratio of 1.31x — passable. One with $280,000 in current assets and $290,000 in liabilities is upside down. Note: retainage receivable is a current asset. Retainage payable is a current liability. Both must be correctly classified.

Net Worth

Growing year over yearTotal Assets − Total Liabilities

Net worth is the equity base from which bonding capacity is calculated. Most surety programs underwrite single-job limits at 10–15x net worth and aggregate limits at 15–20x net worth. A Missoula contractor with $400,000 net worth can typically bond individual projects up to $4–6M and carry $6–8M in aggregate. Net worth that's eroding year over year triggers surety concern regardless of revenue.

Backlog

Matches workforce capacitySigned contracts not yet billed

Backlog represents future revenue under contract. Surety underwriters compare backlog to the contractor's demonstrated completion capacity — a contractor with $1.2M in revenue history and $4.5M in backlog will face questions about whether they can execute. Backlog must be calculated from contract records and cross-referenced against the WIP schedule monthly.

Underbilling Position

Managed, not excessiveCosts in Excess of Billings

A large underbilling position signals that the contractor is earning revenue they haven't billed — which represents cash flow risk and potential collection exposure. Surety agents review the WIP schedule for unusual underbilling concentrations, particularly on projects with a single owner or GC. Clean, monthly WIP schedules make this conversation straightforward.

What clean books unlock:A Missoula contractor with well-maintained, construction-specific financials — reconciled monthly, WIP scheduled, balance sheet correctly classified — can typically qualify for bonding 2–3x higher than a contractor of the same revenue with reconstructed or generic books. That's the difference between bidding $500K jobs and bidding $1.5M jobs. It's not the business that's the constraint — it's the books.

Lender Requirements for Missoula Contractors

Missoula's construction lending market is served primarily by First Interstate Bank, Stockman Bank, Glacier Bank, and SBA 7(a) and 504 programs for larger capital needs. Each lender underwrites construction company loans differently, but all of them want the same fundamental financial information — and all of them will decline or delay if the financials can't be produced cleanly.

Equipment financing

Two to three years of P&L statements, current balance sheet, equipment list with values, and demonstrated debt service coverage. The equipment being financed is the primary collateral. DSCR of 1.25x required — calculated from your actual net income plus depreciation add-back. Without clean books showing real depreciation, the add-back can't be properly documented.

Operating line of credit

A/R aging report showing collectible receivables that serve as the borrowing base, current balance sheet, and 12 months of bank statements. Lines of credit for contractors are often secured by receivables — the aging report determines how much you can draw. An A/R aging report you can't produce quickly from your books means the line isn't available when you need it.

SBA 7(a) — working capital or acquisition

Three years of business tax returns, three years of P&L and balance sheets, personal financial statement, business plan for acquisition loans. The SBA underwriting process is detailed and slow — adding a books reconstruction to the process adds months and often kills the deal on timing alone.

SBA 504 — commercial real estate or heavy equipment

Same financial package as 7(a) plus appraisal and environmental. Requires the borrower's business financials to demonstrate repayment capacity independent of the collateral. The 504 program is underutilized by Montana contractors — the below-market rate on the CDC portion makes it significantly cheaper than conventional equipment financing for purchases over $250K.

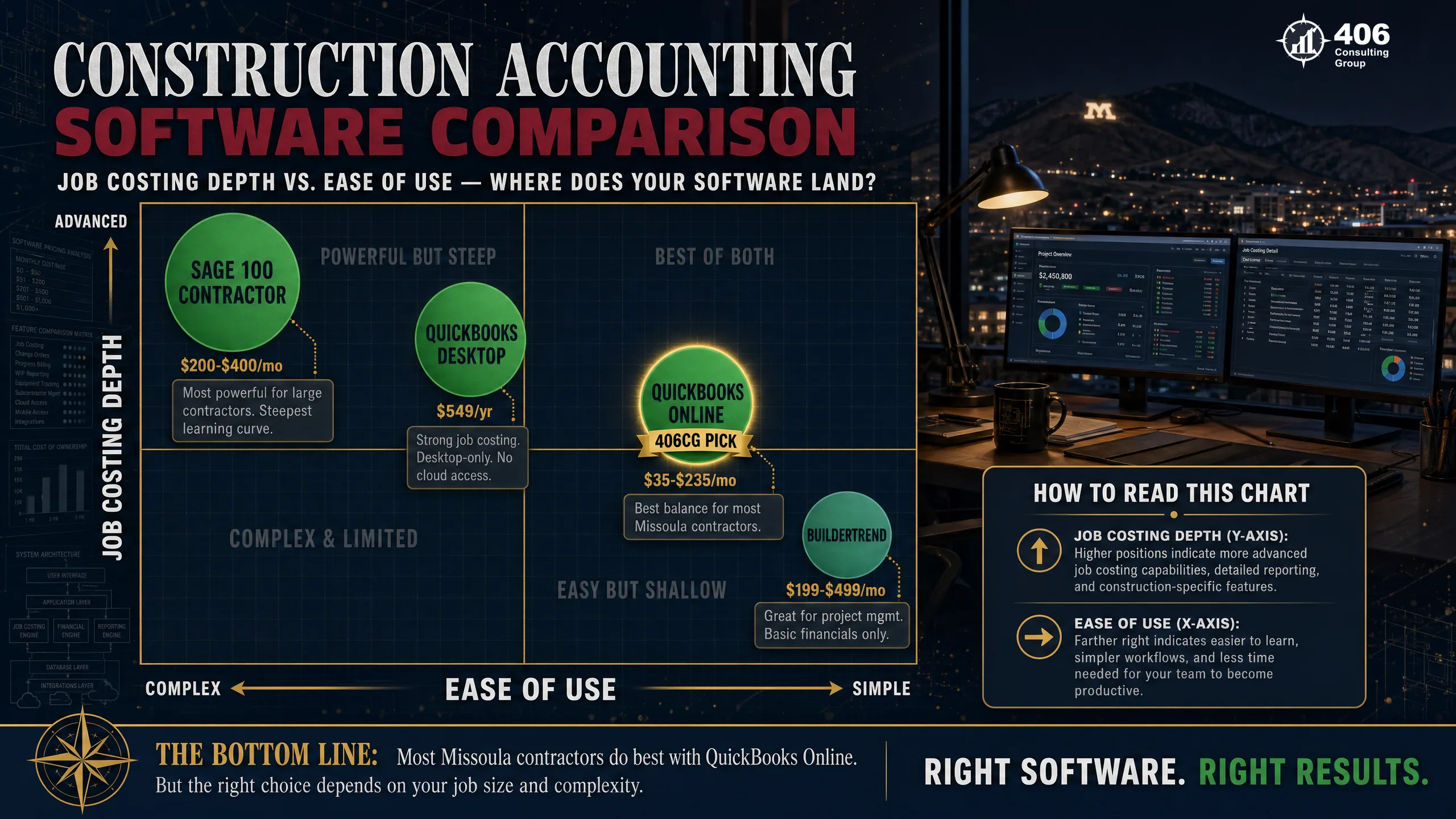

Accounting Software for Missoula Construction Companies

The short answer: most Missoula contractors under $3M in revenue should be on QuickBooks Desktop Premier Contractor Edition or QuickBooks Online with a job costing workaround. Contractors above $3M with complex multi-phase projects should evaluate Sage 100 Contractor. Buildertrend adds project management but is not a replacement for accounting software.

QuickBooks Desktop Premier — Contractor Edition

Best for most Missoula contractors$599–$999/year (Pro/Premier) — $500K–$3M revenue | Up to 5 active projects

Strengths

- Job costing by project phase and cost category

- Estimating module integrates with job cost reports

- Certified payroll report built in (for prevailing wage projects)

- Equipment cost tracking by job

- Change order tracking

- Subcontractor management with retainage tracking

- Widely supported by Montana construction accountants

Limitations

- Single machine (remote access requires add-on)

- Desktop-only — mobile access limited

- Intuit has been pushing toward QBO — long-term platform risk

- No cloud-native collaboration

Sage 100 Contractor

Complex / multi-phase projects$400–$800/user/year — $3M+ revenue | Multi-phase, multi-entity projects

Strengths

- Most robust job costing in the construction market

- Full WIP accounting module with schedule automation

- Union and prevailing wage payroll built in

- Equipment management with cost allocation

- Multi-entity (separate companies) in one system

- Subcontract management with compliance tracking

Limitations

- Steep learning curve — requires dedicated training

- Higher cost (per-user licensing)

- Implementation takes 60–120 days

- Requires a Sage-certified bookkeeper or accountant

QuickBooks Online

Service businesses only$30–$200/month — Service contractors with low project volume

Strengths

- Cloud-based — accessible anywhere

- Easy bank feed integration

- Payroll add-on available

- Low monthly cost

Limitations

- Job costing is inferior to QB Desktop — limited phase tracking

- No certified payroll report

- Equipment tracking requires manual workarounds

- Not recommended for GCs with active WIP schedules

Buildertrend

Project management add-on$499–$799/month — GCs who need scheduling + client communication

Strengths

- Excellent project scheduling and Gantt charts

- Client portal for approvals and communication

- Daily logs and photo documentation

- Integrates with QuickBooks

Limitations

- Not a replacement for accounting software — integrates with QB, does not replace it

- Accounting module is limited and not GAAP-compliant for bonding purposes

- High monthly cost for what is primarily a project management tool

- Integration with QB creates double-entry work if not managed carefully

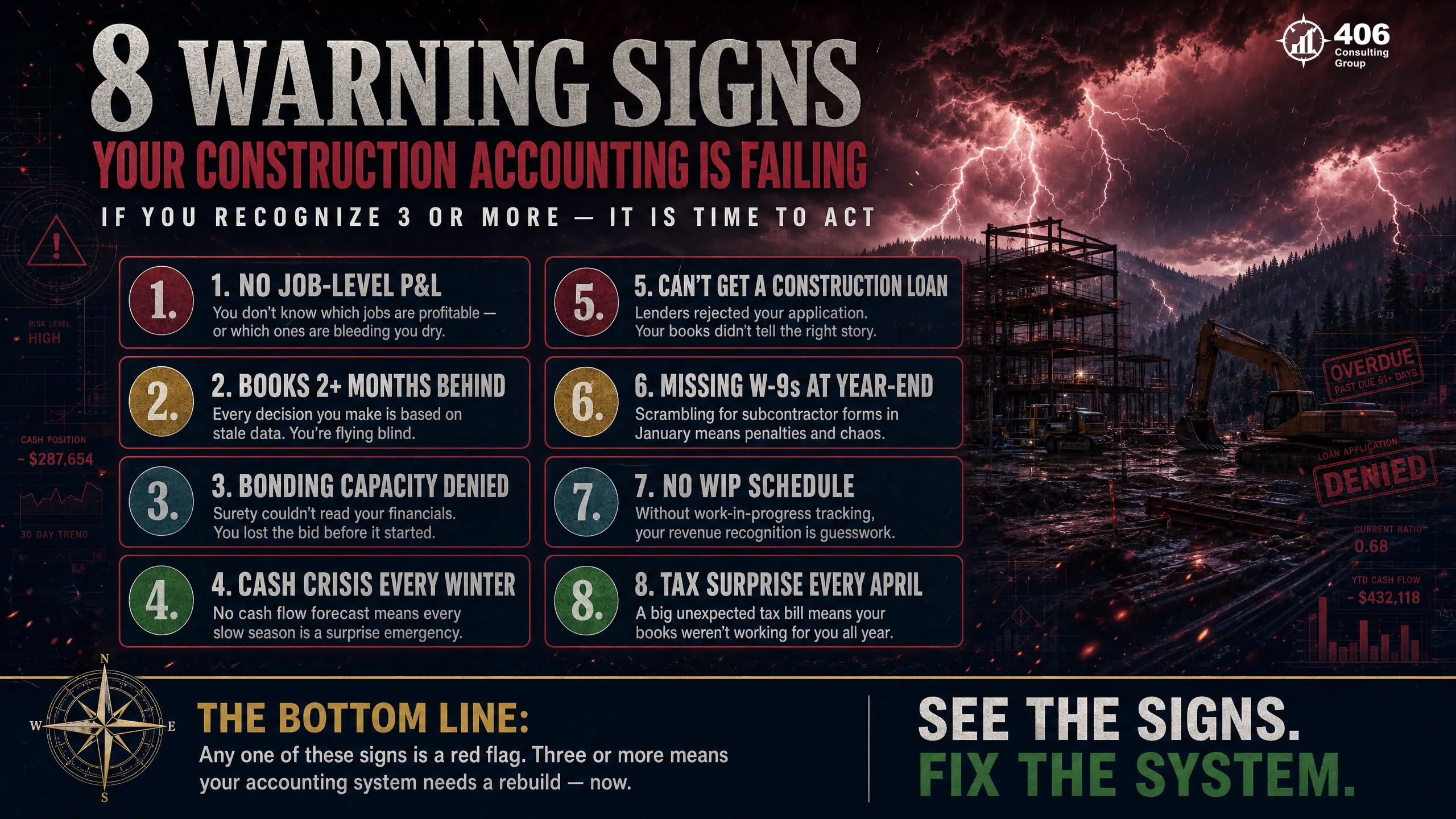

8 Warning Signs Your Construction Accounting Is Failing

Each of these warning signs indicates a specific gap in your financial system. Each gap has a real dollar cost. If more than two apply to your business, the cost of fixing the system is almost certainly less than the cost of continuing to operate without it.

You don't know which jobs are profitable until they close

4–8% margin leakage annually — problem jobs run to completion without intervention

Your tax preparer makes significant adjustments every year

You're paying accounting rates for bookkeeping work; losing a full year of tax strategy

You've been surprised by a cash shortage in January or February

The winter gap is always visible in fall with a 90-day projection — this means you didn't have one

Your bonding capacity is lower than your revenue would suggest

Your financials aren't presenting your business correctly to the surety underwriter

You've had a lender ask for financial statements you couldn't produce quickly

Clean books produce financial statements in minutes; reconstruction takes weeks and signals disorganization

Your books are more than 60 days behind

Every job cost report, WIP schedule, and cash flow projection is based on stale data — decisions are made blind

You've received IRS or Montana DOR correspondence about 1099s or withholding

Penalties plus interest retroactive to original due date; signals to the IRS that your records are incomplete

Labor runs over budget on most jobs but you don't find out until closeout

Job costing with weekly labor variance reports catches this at Week 3, not at project completion

Frequently Asked Questions

What is construction accounting and how is it different from regular bookkeeping?

Construction accounting is a specialized discipline that tracks costs and revenue at the job level, recognizes revenue based on percentage of completion rather than billing dates, manages retainage receivables and payables separately from current accounts, and produces the WIP schedule required by surety underwriters and construction lenders. Regular bookkeeping records transactions at the company level without job-level cost allocation. For a contractor, company-level books tell you whether the business made money last year. Job-level construction accounting tells you which jobs made money — and when a current job is heading toward a loss.

How much does construction accounting cost for a Missoula contractor?

Construction accounting for Missoula contractors typically runs $800–$1,500/month for businesses in the $1M–$5M revenue range, depending on transaction volume, number of active projects, whether payroll is included, and whether a monthly WIP schedule is produced. For context: a construction accountant catching a $17,000 labor overrun on a single job at Week 6 rather than at closeout recovers the monthly bookkeeping cost many times over on a single engagement. The real question isn't what it costs — it's what operating without it costs.

Do I need job costing if I only do 3–4 projects per year?

Yes — especially if you only do 3–4 projects per year. At that volume, a single bad job can define your entire year. If you have four projects and one loses 12% margin instead of the 18% you estimated, that one job moved your annual margin by 3+ percentage points. Job costing on 3–4 projects is simpler than on 20, but the importance per project is higher, not lower.

What is a WIP schedule and do I need one?

A WIP (Work in Progress) schedule is a monthly report that shows every active project's revenue earned based on percentage of completion — as opposed to what has been billed. It identifies overbilling (a liability) and underbilling (an asset) on each project. You need one if: you have any project that spans more than one month, you want your bonding renewed at your current capacity, you apply for commercial financing, or you want to know whether your company is actually profitable — not just whether it's generating cash from billings.

What does prevailing wage compliance require from my books?

Prevailing wage compliance on Montana public works projects requires: certified payroll records submitted weekly to the awarding agency, showing each worker's name, trade classification, hours, and rate paid; payroll records that demonstrate the correct prevailing wage rate for Missoula County was paid for each classification; and books that can separate prevailing wage project labor from non-prevailing wage labor for audit purposes. Your payroll system must post labor to the correct job with the correct classification — a payroll run that lumps all labor into one account without job coding cannot produce compliant certified payroll records.

How do I switch to construction-specific accounting if my books are a mess?

A mid-year switch is almost always better than waiting until January. The process: your new accountant requests your QuickBooks file or records from the prior bookkeeper (they are legally required to provide them), reviews and corrects prior months back to January 1, establishes job cost accounts for all active projects, sets up the WIP schedule framework, and brings books current. For a contractor with 3–5 active projects, this typically takes 3–5 weeks. Starting January 1 with clean books is the goal — starting August 1 with 5 months corrected is far better than starting the following January with 12 months to correct.

Can a regular accountant handle construction accounting, or do I need a specialist?

A generalist accountant can handle your tax return and basic compliance. Construction-specific accounting — job costing, WIP schedules, retainage tracking, certified payroll, surety financial packages — requires someone who has worked with contractors and understands the specific reports surety agents and construction lenders expect to see. The fastest way to test this: ask your current accountant to produce a WIP schedule from your last month-end books. If they don't know what that is, you need a construction accounting specialist.

External Resources

Missoula, MT Construction

Expert Accounting Built for Montana Contractors

406 Consulting Group provides construction-specific accounting, job costing, WIP schedules, and tax strategy for Missoula contractors. Clean books. Accurate job margins. Bonding-ready financials. Built for the way Montana construction businesses actually work.

The Build Stack

5 layers every Missoula contractor needs

Cost Capture

Every cost to every job, in real time

WIP Tracking

Revenue earned vs. billed, monthly

Cash Flow

Rolling 90-day projection, always current

Tax Strategy

Quarterly coordination with your accountant

Lender Readiness

Financials banks and surety can underwrite

Montana Construction Quick Reference

Related Resources