Navigating Payroll Compliance

in Columbia Falls, MT

Columbia Falls employers face Montana payroll compliance rules most never learned. Here's the complete compliance guide for Flathead Valley small businesses.

Payroll compliance in Columbia Falls, MT is not optional — and most of the employers who get penalties weren't trying to cut corners. They simply never learned that Montana requires workers' compensation before a new hire's first day, that new employees must be reported to the state within 20 days, that there is no tip credit in Montana, or that missing a single payroll tax deposit triggers an IRS penalty that starts at 2% and compounds with every notice. The rules are not complicated once you know them. The problem is that most Columbia Falls small business owners never got the roadmap.

This guide gives you that roadmap — from what must be in place before you cut your first check, through every compliance obligation by quarter and year-end, to how Columbia Falls' specific industries (Glacier tourism, timber, construction, retail) create payroll situations that generic guides miss.

Table of Contents

Why Payroll Compliance Matters for Columbia Falls, MT Businesses

Columbia Falls sits at the gateway to Glacier National Park — which means its economy runs on seasonal hiring, tourism-driven hospitality, construction tied to Flathead County's growth, and the timber and manufacturing heritage that shaped the town. Each of those industries brings its own compliance exposure: seasonal workers and UI claims, tipped hospitality employees and Montana's no-tip-credit rule, construction subcontractors and misclassification risk, and the payroll record-keeping requirements that don't care how small the business is.

2%–15%

IRS failure-to-deposit penalty range

Per missed deposit, per incident. A $10,000 payroll tax deposit missed for 10 days costs $500 — before any notices.

20 days

Montana new hire reporting window

Every new hire — including seasonal and part-time — must be reported to Montana DPHHS within 20 days of start date.

Day 1

Workers' comp required by

Coverage must be in force before the employee's first shift. No grace period. No minimum hours or days threshold.

The compliance gap for small businesses:Payroll compliance knowledge doesn't scale with business size — a Columbia Falls restaurant with 6 employees faces the same IRS deposit requirements and Montana DLI obligations as a company with 60. The penalties don't scale either. This guide covers every requirement regardless of headcount.

Montana Payroll Compliance Requirements Every Columbia Falls Employer Must Know

Montana's payroll compliance requirements apply to every employer in the state — including Columbia Falls businesses with one employee. The short answer: Montana minimum wage is $10.85/hour (2026, adjusted annually), there is no tip credit, workers' compensation is mandatory before day one, new hires must be reported within 20 days, and employees cannot be terminated without cause after a probationary period under the Montana Wrongful Discharge from Employment Act.

Minimum Wage

$10.85/hr (2026)

Indexed annually to CPI — verify current rate each January 1. No tip credit permitted in Montana.

Overtime

1.5× after 40 hrs/week

Federal FLSA standard. No daily overtime threshold. Calculated weekly, not daily.

Workers' Compensation

Mandatory — all employees

Obtained through Montana State Fund or approved private insurer. Required before first day of work.

New Hire Reporting

Within 20 days of hire

Report to Montana DPHHS. Required for all employees including part-time and seasonal.

Final Paycheck

Next payday or 15 days

Whichever is earlier. No exception for terminated employees. Cannot withhold for unreturned property.

Payday Frequency

Semi-monthly minimum

Must pay wages at least twice per month. Monthly payroll is non-compliant for most employees.

Montana Income Tax

4.7% / 5.9% (two brackets)

Withheld using Montana Form MW-4 (state equivalent of W-4). Filed using Montana MW-1 quarterly. Montana restructured to two brackets effective January 1, 2024.

UI Contributions

Quarterly, first $47,300

Montana UI taxable wage base: $47,300/employee/year (2026 — verify at dli.mt.gov each January). Rate varies by employer experience.

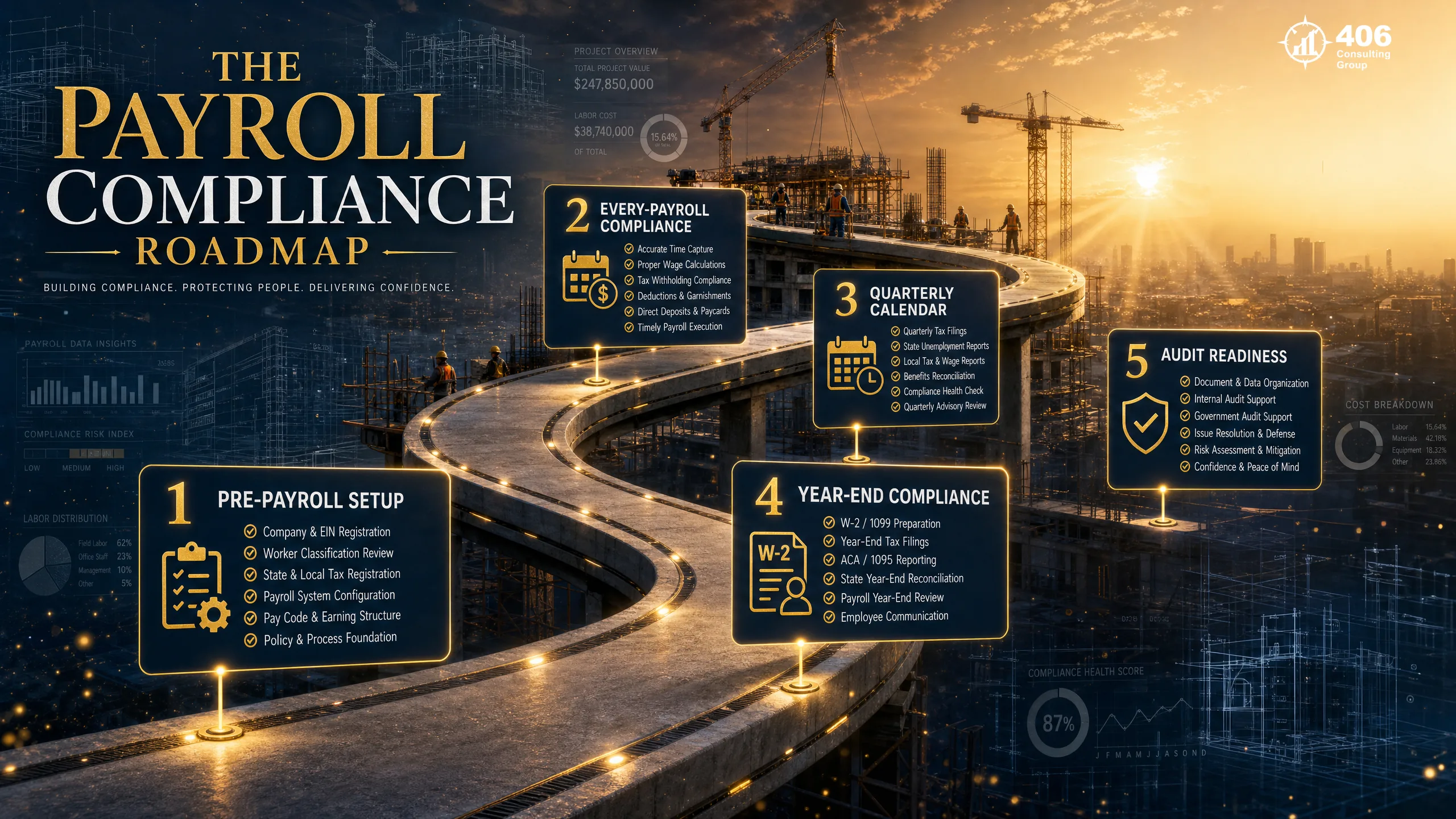

The Payroll Compliance Roadmap: 5 Stages Every Columbia Falls Employer Must Build

The Payroll Compliance Roadmap is the five-stage framework that organizes every Montana payroll obligation into a logical sequence. Compliance isn't a single event — it's a system that runs continuously. Each stage handles a different frequency of obligation: one-time setup, every payroll, quarterly, annual, and ongoing maintenance. Missing any stage creates exposure in the next one.

Pre-Payroll Setup

One-time (per new employee)Everything that must be in place before the first paycheck — registrations, accounts, workers' comp, and new hire paperwork.

Every-Payroll Compliance

Every pay periodWage floor verification, overtime calculation, authorized deductions only, correct withholding on each run.

Quarterly Compliance Calendar

4× per year941 filing and deposit, Montana MW-1, UI return — all due within 30 days of quarter-end.

Year-End Compliance

January 31 hard deadlineW-2s, 1099-NECs, Form 940, Montana MW-3 reconciliation — all on the same January 31 deadline.

Ongoing Audit Readiness

Continuous3-year record retention, I-9 maintenance, workers' comp classification accuracy, wage claim documentation.

Stage 1: Pre-Payroll Setup — Everything Before the First Check

Pre-payroll setup must be complete before the new employee's first shift — not before their first paycheck. Workers' compensation must be in force on day one. The new hire report must be filed within 20 days of their start date. These are not administrative tasks to get to eventually.

Obtain Federal Employer Identification Number (EIN)

Before first hire — one-timeApply at IRS.gov — issued immediately online. Required to open payroll accounts, file 941s, and issue W-2s. Sole proprietors paying a household employee also need an EIN (Social Security number is not sufficient for payroll purposes).

Register Montana Withholding Tax Account

Before first Montana payrollRegister with the Montana Department of Revenue at mtrevenue.gov to obtain a Montana withholding account number. Required to file MW-1 quarterly returns and remit Montana income tax withholding. Cannot file without a valid account number.

Register Montana UI Account

Before first payrollRegister with the Montana Unemployment Insurance Division at uid.dli.mt.gov. New employers are assigned a standard UI rate based on industry. Rate adjusts after 2 years based on claim experience. Required to file quarterly UI returns.

Obtain Workers' Compensation Coverage

Before employee's first dayContact Montana State Fund (montanastatefund.com) or an approved private insurer. Provide employee count, job classifications, and estimated annual payroll. Policy must be in force before the employee begins work — no retroactive coverage. Post the required Montana State Fund notice in the workplace.

Collect W-4 and Montana MW-4

On or before first dayFederal W-4 establishes federal withholding. Montana MW-4 establishes state withholding allowances — it is a separate form. If the employee does not complete MW-4, withhold at the single/zero allowances default (most conservative). Both forms must be retained for 4 years.

Complete Form I-9 — Employment Eligibility

Section 1: day one | Section 2: within 3 business daysEmployee completes Section 1 on or before their first day. Employer completes Section 2 within 3 business days by examining identity and work authorization documents. E-Verify is optional for most Montana private employers. Retain I-9s for 3 years from hire date or 1 year after termination, whichever is later.

File Montana New Hire Report

Within 20 days of start dateReport to Montana DPHHS at dphhs.mt.gov/csed/newhire. Required information: employee name, address, SSN, start date, and employer EIN and name. Applies to all employees including part-time, seasonal, and rehires. Electronic filing is fastest — paper forms accepted but slower to process.

Set Up Payroll Software and Direct Deposit

Before first payroll runChoose payroll software that handles Montana tax tables automatically (Gusto, QuickBooks Payroll, ADP). Collect direct deposit authorization from employee. Verify bank routing and account numbers before first run — incorrect bank information delays payment and creates final paycheck compliance risk.

Stage 2: Every-Payroll Compliance — What Must Be Right on Every Run

Every payroll run carries the same compliance obligations regardless of how routine it feels. A single payroll where overtime was miscalculated, a deduction wasn't authorized, or an employee was paid below minimum wage creates a wage claim liability that doesn't expire until it's resolved.

Minimum wage floor

$10.85/hr (2026) — verify current year rate each January 1

Every employee, every hour. Part-time, seasonal, and salaried non-exempt employees all subject to the same floor. Salaried non-exempt employees: divide salary by hours worked — if the effective hourly rate falls below minimum wage in a heavy week, the employer owes the difference.

Overtime calculation

1.5× regular rate for hours over 40/workweek

Overtime is calculated on the workweek — Sunday through Saturday (or your established workweek). Cannot average hours across two weeks to avoid overtime. Shift differentials and non-discretionary bonuses must be included in the regular rate for overtime purposes.

Authorized deductions only

Only taxes, benefits, and court-ordered deductions

Montana law prohibits deductions for breakage, cash shortages, uniforms, or training costs without specific written authorization that meets state standards. Deducting from wages to recover a cash register shortage or broken equipment without proper authorization is a wage violation.

Montana withholding calculation

Per MW-4 on file — verify tables updated annually

Montana income tax withholding tables update each January. If your payroll software does not auto-update Montana tables, you are withholding at the wrong rate. Underwithholding creates employee tax liability — overwithholding creates overpayment that must be corrected on the MW-3.

Pay stub requirements

Montana requires pay stubs with each payment

Montana employers must provide employees with a wage statement (pay stub) showing gross wages, deductions itemized, and net pay. Electronic pay stubs are permitted if the employee can access and print them. Failure to provide a pay stub is a wage law violation.

Tipped employee minimum wage

Full $10.85/hr — no tip credit

Columbia Falls hospitality employers: tipped employees receive full Montana minimum wage in base pay — tips earned on top of that. Reducing base pay below minimum wage because the employee earns tips is illegal in Montana and the most common wage violation in the state's food service and lodging sector.

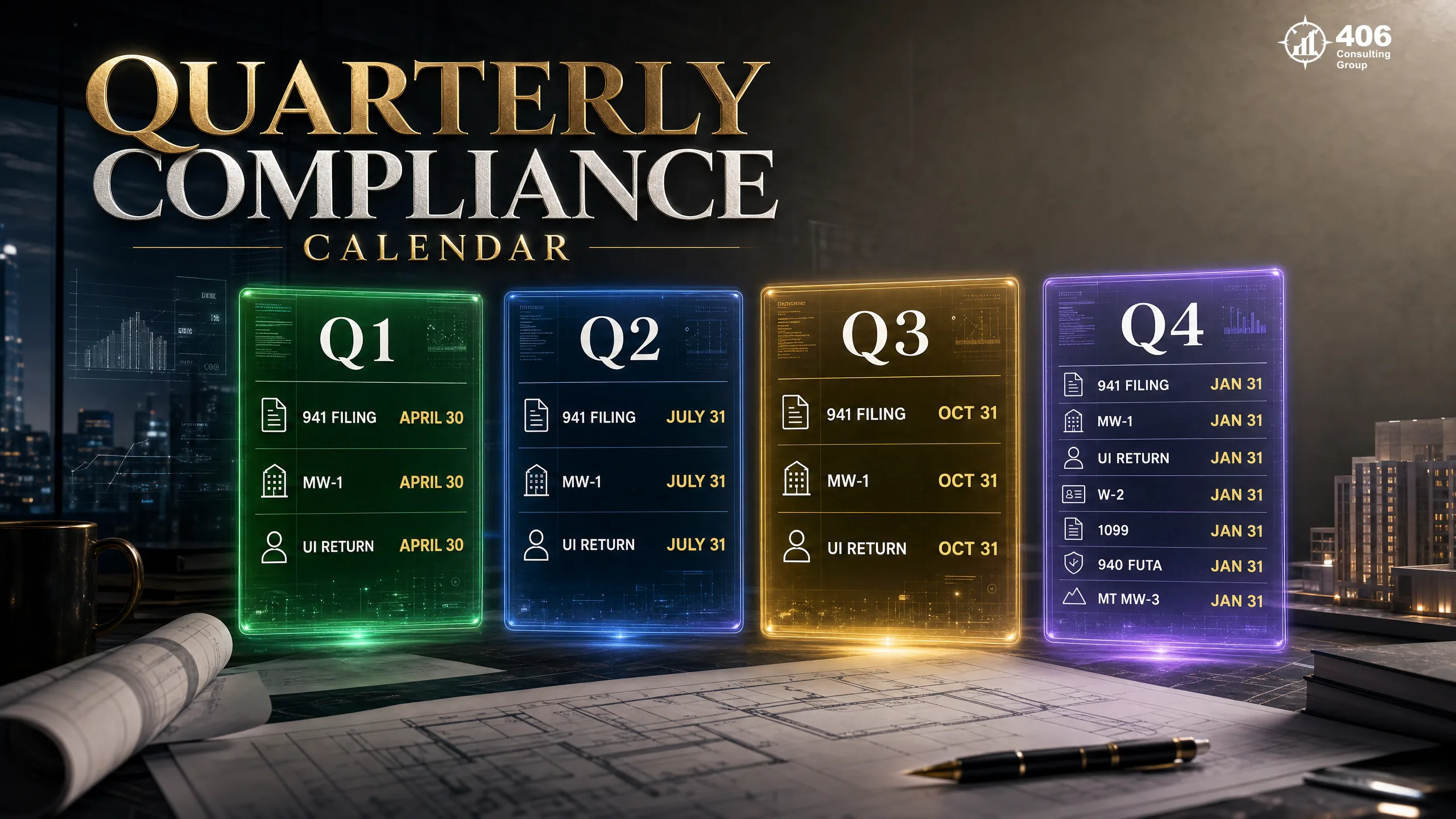

Stage 3: Quarterly Compliance Calendar for Columbia Falls Employers

Four times per year, three separate filings are due within 30 days of quarter-end — all on the same deadlines. Missing any one of them triggers penalties that compound with every notice cycle.

| Quarter | Form 941 (Federal) | Montana MW-1 | Montana UI Return |

|---|---|---|---|

| Q1 (Jan–Mar) | April 30 | April 30 | April 30 |

| Q2 (Apr–Jun) | July 31 | July 31 | July 31 |

| Q3 (Jul–Sep) | October 31 | October 31 | October 31 |

| Q4 (Oct–Dec) | January 31 | January 31 | January 31 |

Form 941 — Employer's Quarterly Federal Tax Return

Reports total wages paid, federal income tax withheld, and FICA taxes (employee + employer share) for the quarter. Must reconcile exactly to the deposits made during the quarter. Discrepancy between deposits and return triggers an IRS notice. Small employers (annual 941 tax liability under $1,000) may file Form 944 annually instead — IRS must authorize this in writing.

Montana Form MW-1 — Quarterly Withholding Return

Reports Montana income tax withheld from employee wages during the quarter. Amount must equal deposits made to the Montana DOR during the quarter. Filing frequency (accelerated, monthly, quarterly) is determined by annual withholding amount. Most Columbia Falls small businesses file quarterly.

Montana UI Quarterly Return

Reports total wages paid and UI taxable wages (first $47,300 per employee per year — 2026 wage base) to the Montana Unemployment Insurance Division. Calculates UI tax owed at the employer's experience-rated tax rate. Late UI returns carry 1.5% monthly interest on unpaid tax plus a penalty of 10% of unpaid tax or $25, whichever is greater.

Stage 4: Year-End Compliance — Every Deadline Lands on January 31

Year-end payroll compliance for Columbia Falls employers means six separate deadlines — all landing on January 31. This is not a coincidence and it is not optional. The IRS, Montana DOR, and Montana UI Division all enforce January 31 as the hard deadline for annual reconciliation filings.

January 31

W-2s to Employees

Every employee who received wages during the year receives a W-2 by January 31 — postmarked, delivered, or electronically transmitted (with consent). Boxes must reconcile to your quarterly 941 filings. A W-2 where Box 1 wages don't match cumulative 941 wages triggers IRS reconciliation.

January 31

1099-NECs to Contractors

Every contractor paid $2,000 or more during 2026 (raised from $600 under OBBBA, signed July 2025 — verify current threshold at IRS.gov) receives a 1099-NEC by January 31. This is the same deadline as Copy A to the IRS — unlike other 1099 types, there is no extended paper filing window for 1099-NEC.

January 31

Form 940 — Annual FUTA

Annual federal unemployment tax return reconciling the year's FUTA liability. Montana employers receive a 5.4% FUTA credit for state UI contributions paid on time — resulting in a 0.6% net FUTA rate on the first $7,000 per employee. If Montana UI was paid late, you lose part of the credit.

January 31

Q4 Form 941

Q4 941 is due January 31 along with everything else. Reconcile total prior-year wages across all four 941s to total W-2 wages. Any discrepancy requires a 941-X correction before the IRS finds it.

January 31

Montana Form MW-3

Montana's annual withholding reconciliation. MW-3 reconciles total Montana income tax withheld across all four MW-1 quarterly returns to total Montana withholding shown on W-2 Box 17. Attach copies of all employee W-2s. Any withholding balance due must be paid with the MW-3.

January 31

Montana UI Q4 Return

Q4 UI return follows the same January 31 deadline as federal filings. Ensure all UI taxable wages are correctly reported — wages over $47,300 per employee (2026 wage base) are excluded from UI tax but must still appear in total wages reported.

Stage 5: Ongoing Audit Readiness — Compliance Between the Deadlines

Audit readiness is not a one-time project — it's the continuous maintenance that makes every compliance deadline less stressful and every regulatory inquiry less expensive. For Columbia Falls small businesses, this means three ongoing obligations.

Payroll Record Retention — 3 Years Minimum

Federal law requires payroll records to be retained for at least 3 years. Montana DLI wage and hour investigations can go back 2 years (5 years for willful violations). Workers' comp auditors typically request 3 years of payroll records. The records must include: employee name, address, SSN, occupation, pay rate, hours worked each day and week, straight-time and overtime pay, deductions, and total wages paid each pay period.

Keep: payroll registers, timecards, W-4s, MW-4s, direct deposit authorizations, garnishment orders, and workers' comp classification documentation.

I-9 Audit Readiness

I-9s must be retained for 3 years from hire date or 1 year after termination, whichever is later. ICE audits are conducted without advance warning — employers must produce I-9s within 3 business days of a Notice of Inspection. Common I-9 violations: missing Section 2 completion date, unacceptable documents accepted, Section 2 completed more than 3 days after start date.

Action: Conduct an internal I-9 audit annually. Use the M-274 Handbook for Employers as your guide. Correct good-faith errors on the original form with a single line through the error, corrected information, and initials/date.

Workers' Comp Classification Accuracy

Montana State Fund and private carriers conduct annual payroll audits — they compare your estimated payroll at policy inception to actual payroll at year-end. If your workforce classification changed (e.g., you added a roofing crew to a landscaping business), premium adjustments can be significant. Misclassification — intentional or not — is an audit trigger.

Action: Review classification codes with your workers' comp carrier annually. Notify your carrier within 30 days of adding a new job type not previously covered.

Columbia Falls Industry Spotlights: Payroll Compliance by Sector

Columbia Falls' economy creates industry-specific payroll compliance issues that general Montana guides don't address. Here's what each major sector needs to know.

Glacier Tourism & Hospitality

CF sector- 1Seasonal hiring spike: May–September creates new hire reporting obligations for every seasonal employee — 20-day rule applies regardless of season length

- 2No tip credit: full $10.85/hr minimum wage required for servers, bartenders, and housekeeping regardless of tip income — most common wage violation in Montana hospitality

- 3Seasonal layoffs and UI rate impact: mass seasonal separations in October affect the employer's UI experience rating starting the following year — understanding the rate calculation prevents budget surprises

- 4Non-resident seasonal workers: employees from out of state working in Montana are subject to Montana income tax withholding — their home state exemption (if any) does not eliminate Montana withholding obligation

Timber, Logging & Manufacturing

CF sector- 1Workers' comp classification codes: timber felling, skidding, and mill operations carry among the highest workers' comp rate codes in Montana — misclassifying a faller in a lighter-duty code triggers audit and retroactive premium assessment

- 2Piece-rate pay and overtime: workers paid by the piece (board feet, loads) must still receive overtime at 1.5× their regular rate for hours over 40/week — the regular rate calculation for piece workers is specific and different from hourly workers

- 3Subcontractor vs. employee: logging operations frequently use owner-operators who may qualify as contractors — but the behavioral control test must be carefully evaluated; DLI investigates this sector regularly

Construction & Trades

CF sector- 1Prevailing wage on Montana public projects: construction contracts with state, county, or city entities in Flathead County require certified payroll and payment at Montana Department of Labor prevailing wage rates — rates vary by county and trade

- 2Subcontractor management: general contractors can be held liable for subcontractors' payroll tax failures in certain situations — verify that subcontractors carry their own workers' comp before each project

- 3Seasonal cash flow and payroll timing: construction payroll peaks in summer — quarterly UI deposits and 941 deposits in Q2 and Q3 are typically your largest — cash flow planning around deposit dates prevents late payment

Retail & Service Businesses

CF sector- 1Part-time employee compliance: Montana minimum wage, workers' comp, and new hire reporting apply equally to part-time and full-time employees — no exemption for fewer than X hours per week

- 2Montana has no general sales tax, but payroll compliance obligations are identical to states that do — don't let the sales tax simplicity create a false sense of overall tax compliance ease

- 3Employer-provided meals and lodging: retail and service employers who provide housing or meals to employees may have taxable wages to add — value of housing is generally taxable unless meeting the convenience-of-employer test

Healthcare & Home Services

CF sector- 1Home care worker classification: home health aides and personal care workers employed by agencies are W-2 employees — the in-home setting does not create contractor status

- 2Live-in domestic workers: different FLSA overtime rules may apply for live-in domestic service employees — consult current DOL guidance as this area has changed

- 3Healthcare staffing agencies: if using a staffing agency, verify the agency handles all payroll tax obligations for the placed workers — the host business may have joint-employer liability if the agency fails to comply

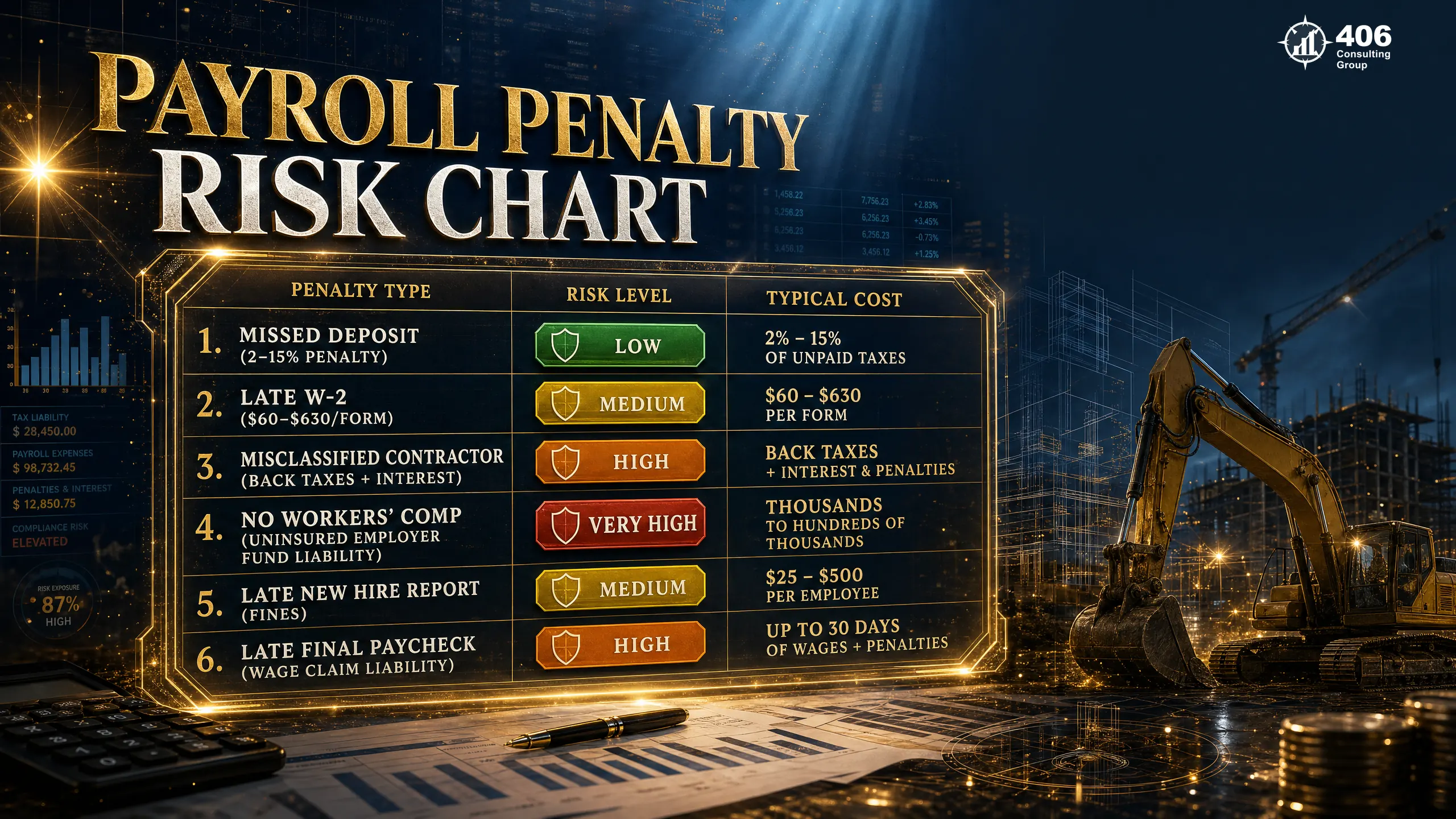

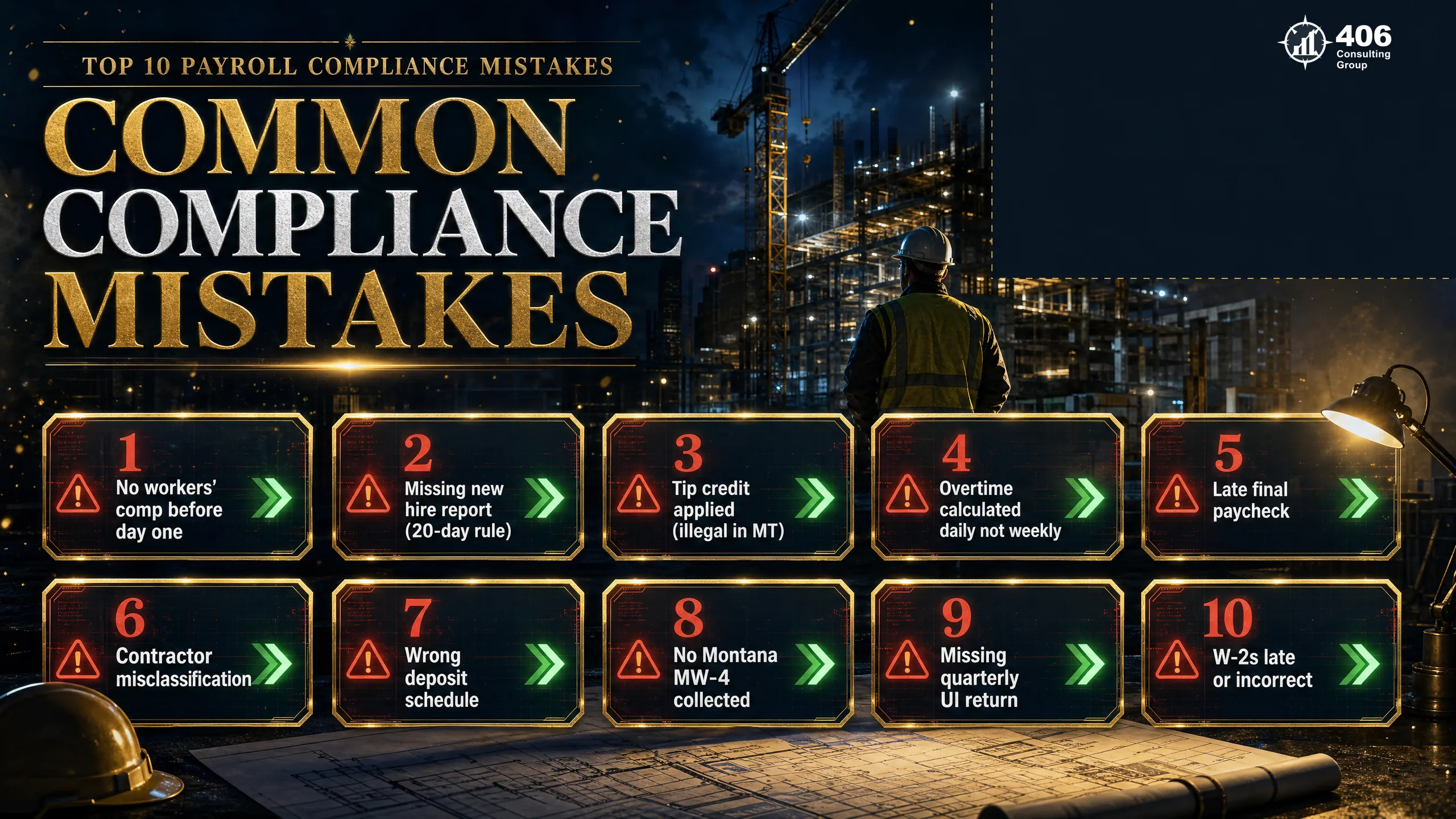

10 Payroll Compliance Mistakes Columbia Falls Employers Make

These are the ten most common payroll compliance mistakes made by Columbia Falls and Flathead Valley small businesses — each with the consequence and the fix.

No workers' comp coverage on day one

Consequence

Uninsured employer fund liability — state pays the claim, then sues the employer for reimbursement plus penalties

Fix

Contact Montana State Fund before the hire is confirmed. Coverage can be obtained in 24–48 hours for most businesses.

Missing the 20-day new hire report

Consequence

Montana DPHHS fines for non-reporting; state may conduct a compliance audit across all recent hires

Fix

Make new hire reporting part of the day-one onboarding checklist — file online at dphhs.mt.gov the same day the employee starts.

Applying a tip credit to tipped employees

Consequence

Back wages owed to every affected employee for every underpaid hour, plus Montana DLI penalties and potential lawsuit

Fix

Pay every tipped employee at least $10.85/hr as a base wage — tips are on top of that, not in place of it.

Calculating overtime daily instead of weekly

Consequence

Underpaid overtime liability for any week where the daily calculation missed the weekly trigger

Fix

Set payroll software to calculate overtime on the 7-day workweek. Verify the workweek start day is established and consistent.

Missing federal tax deposit deadlines

Consequence

2–15% IRS failure-to-deposit penalty per incident; multiple missed deposits in a quarter compound rapidly

Fix

Know your deposit schedule (monthly or semi-weekly based on lookback period). Set calendar reminders. Never wait for the quarterly 941 to reconcile — deposits must be made throughout the quarter.

Misclassifying employees as contractors

Consequence

Back FICA taxes, income tax withholding, UI contributions, workers' comp back-premiums, interest, and penalties — typically $25,000–$80,000+ per reclassified worker over 2 years

Fix

Apply the IRS three-factor test before issuing a first 1099. When in doubt, classify as W-2. The cost of a wrong contractor classification vastly exceeds the cost of correct employment.

Skipping the Montana MW-4 for new hires

Consequence

Withholding at wrong rate — over or underwithholding creates both employee and employer liability

Fix

Collect Montana MW-4 alongside the federal W-4 on day one. Default to single/zero allowances if the employee doesn't complete it.

Late or missing W-2s

Consequence

$60–$630 per W-2 depending on how late; $630/form for intentional disregard (no cap on total penalty)

Fix

Start W-2 preparation in early January. Verify all addresses and SSNs in December. Issue by January 31.

No records retained past tax season

Consequence

Cannot defend wage claim, workers' comp audit, or DLI investigation without payroll records going back 3 years

Fix

Retain all payroll records for a minimum of 4 years (3 years plus current). Store digitally with backup — cloud storage in payroll software is sufficient.

Paying the final paycheck late

Consequence

Montana wage claim — back wages plus potential DLI complaint; attorney fees if the employee pursues legal action

Fix

Know your state-required final paycheck deadline before an employee leaves: next regular payday or 15 days — whichever is earlier. Have a process to generate off-cycle checks immediately when an employee separates.

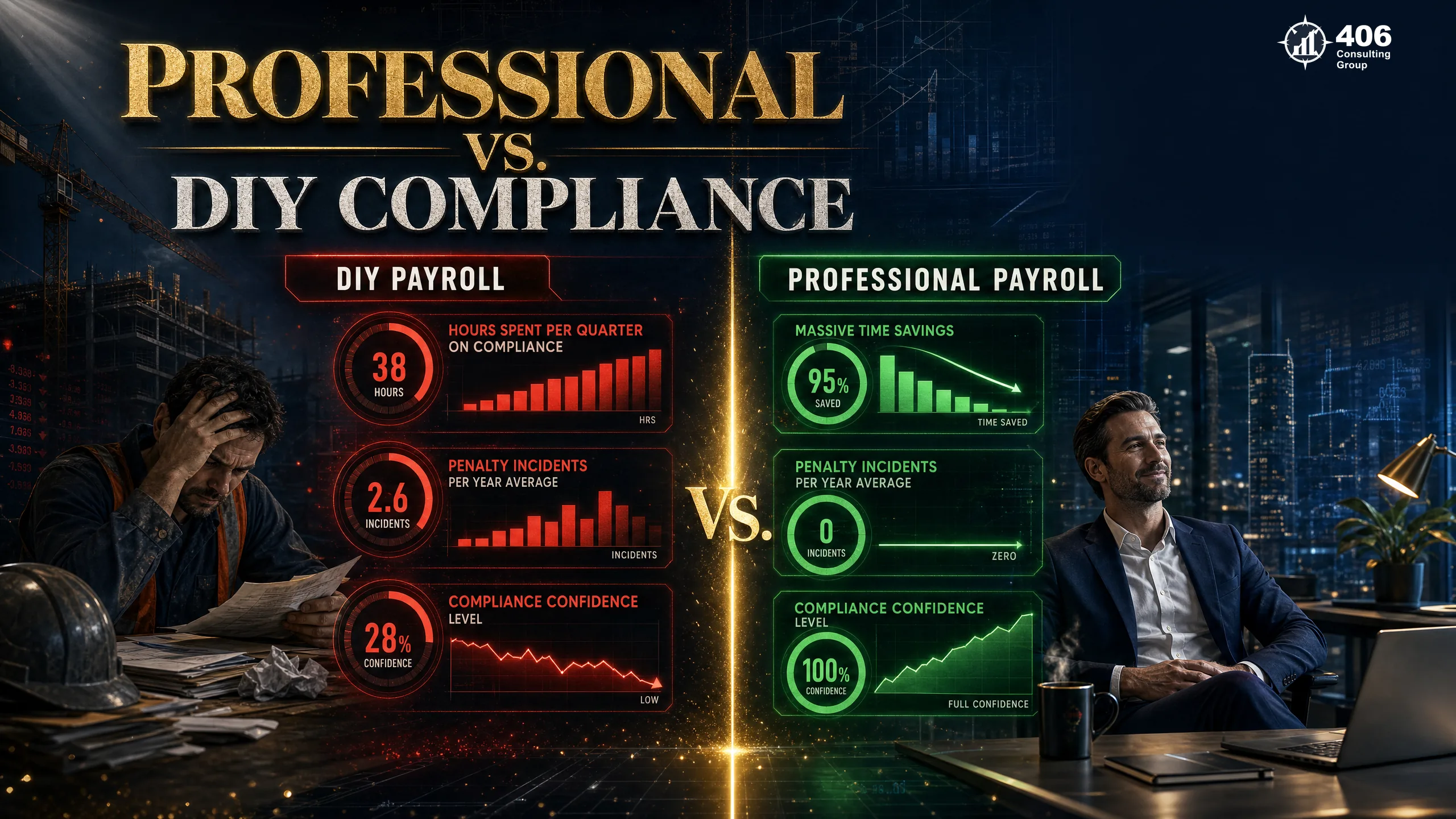

When to Hire Professional Payroll Help in Columbia Falls

Professional payroll services for Columbia Falls businesses typically run $150–$350 per month for a business with 5–15 employees. That cost pays for itself the first quarter a deposit is made correctly that would otherwise have been late, or the first year-end season where W-2s go out January 28 instead of February 15 with a penalty notice attached.

You have your first employee

The moment you hire, all five stages of the compliance roadmap activate simultaneously. First-time employers are the most common source of compliance errors — everything is new at once.

You missed a tax deposit deadline

One missed deposit is a sign that the monitoring system isn't in place. Professional payroll eliminates the monitoring burden — deposits are made automatically on the correct schedule.

You received a notice from the IRS or Montana DOR

A notice is a signal that something in your payroll system produced an error. Professional payroll prevents the errors that trigger notices — and responds to existing notices correctly.

You have seasonal employees you hire and lay off annually

Seasonal payroll creates the highest compliance density: repeated new hire reports, UI experience rating exposure, and final paycheck obligations every season. Professional payroll handles each cycle correctly.

Your bookkeeper is doing payroll manually

Manual payroll — spreadsheet-based deposit tracking, manual tax table lookups, hand-calculated overtime — is the highest-error-rate approach. Modern payroll software with professional oversight eliminates the manual calculation errors.

You want to spend time running your business

For a Columbia Falls business owner, the 4–8 hours per month spent on DIY payroll is time not spent on sales, operations, or customer service. Professional payroll gives that time back.

Frequently Asked Questions: Payroll Compliance in Columbia Falls, MT

What do I need to set up payroll for the first time in Montana?

To set up payroll for the first time in Montana, you need: (1) a federal Employer Identification Number (EIN) from IRS.gov, (2) a Montana withholding tax account registered with the Montana Department of Revenue, (3) a Montana UI account registered with the Unemployment Insurance Division, (4) a workers' compensation policy from Montana State Fund or an approved private insurer in force before the employee's first day, (5) a completed federal W-4 and Montana MW-4 from each employee, (6) a completed I-9, and (7) a new hire report filed with Montana DPHHS within 20 days of the employee's start date.

How often do I need to deposit payroll taxes as a small business in Montana?

Most small Columbia Falls businesses are monthly depositors — deposit federal payroll taxes by the 15th of the month following each payroll. Deposit frequency is determined by your lookback period (July 1–June 30 of the prior year). If your annual payroll tax liability exceeds $50,000, you become a semi-weekly depositor. Montana income tax withholding deposit frequency is separate — most small Columbia Falls businesses deposit quarterly. Montana UI contributions are also paid quarterly.

Does Montana require workers' compensation for part-time employees?

Yes. Montana requires workers' compensation coverage for all employees — including part-time, seasonal, and temporary workers — with no minimum hours threshold. Coverage must be in force before the employee's first shift. A Columbia Falls restaurant that hires a part-time dishwasher for 15 hours per week has the same workers' comp obligation as one that hires a full-time cook. Operating without coverage exposes the employer to uninsured employer fund liability.

What records do I need to keep for Montana payroll compliance?

Columbia Falls employers must retain payroll records for at least 3 years (4 years recommended to match IRS statute of limitations). Required records include: employee name, address, and SSN; pay rate and pay period; hours worked each day and week; straight-time and overtime earnings; deductions with authorization; total wages paid; W-4s and Montana MW-4s; and workers' comp classification documentation. I-9s must be retained for 3 years from hire date or 1 year after termination, whichever is later.

What is the penalty for paying a final paycheck late in Montana?

If a final paycheck is not issued by the next regular payday or within 15 days of separation (whichever is earlier), the employee may file a wage claim with the Montana Department of Labor and Industry. The DLI has authority to recover unpaid wages plus penalties. Employers who willfully withhold a final paycheck — for example, to pressure an employee to return company property — face additional penalties. Montana does not allow an employer to withhold wages for unreturned property or alleged damages without a court order.

Are Montana payroll compliance requirements the same in Columbia Falls as in Billings or Missoula?

The Montana payroll compliance requirements are identical regardless of city size — every employer in Flathead County faces the same minimum wage, workers' comp, new hire reporting, and deposit rules as employers in Billings or Missoula. The difference in Columbia Falls is practical: there are fewer local payroll services, less institutional knowledge among small business owners who may have never had to run payroll before, and industries (Glacier tourism, timber, seasonal construction) that create compliance situations most generic guides don't cover. The rules are the same — the context is different.

External Resources

Columbia Falls, MT

Payroll Compliance Done Right for Flathead Valley Businesses

406 Consulting Group handles payroll processing and compliance for Columbia Falls businesses — new hire reporting, tax deposits, quarterly returns, and year-end filings. All five stages of the Compliance Roadmap, handled.

The Payroll Compliance Roadmap

5 stages — build them in order

Pre-Payroll Setup

EIN, accounts, workers' comp, new hire forms

Every-Payroll Compliance

Minimum wage, overtime, authorized deductions

Quarterly Calendar

941, MW-1, UI — all due 30 days after quarter

Year-End Compliance

W-2, 1099, 940, MW-3 — all January 31

Audit Readiness

Record retention, I-9, workers' comp accuracy

Montana Payroll Quick Reference

Related Guides