The Ultimate Guide to Payroll Management

in Missoula, MT

Montana payroll has rules most Missoula employers don't know until they get a penalty. Here's the complete guide to compliant, accurate payroll for Missoula businesses.

Payroll management in Missoula, MT requires compliance with Montana-specific requirements that most employers don't know exist — until a penalty notice arrives. Montana has no tip credit, a mandatory workers' compensation requirement for all employees, a 20-day new hire reporting window, and final paycheck rules that differ from federal defaults. Getting any one of these wrong doesn't produce a gentle reminder. It produces a penalty, an audit trigger, or a Department of Labor complaint.

This guide covers Montana payroll law from the ground up — what every Missoula employer must know, the five-component Montana Payroll Stack that defines compliant payroll, industry-specific considerations for Missoula's major sectors, and what professional payroll services actually cost versus what the alternative costs when something goes wrong.

Table of Contents

Why Payroll Management in Missoula Is More Complex Than It Looks

Missoula's economy creates payroll complexity that generic payroll guides don't address. The University of Montana generates a large pool of part-time, student, and seasonal employees — each with specific FICA exemption rules. The outdoor recreation and hospitality sectors run seasonal staffing cycles that test Montana's UI experience rating system. Construction contractors face prevailing wage requirements on public projects. And the city's growing technology and remote-work sector creates multi-state withholding obligations when employees work from Montana for out-of-state employers.

$941

Minimum IRS failure-to-deposit penalty

2% of unpaid tax for deposits 1–5 days late. Reaches 15% for deposits more than 10 days after first IRS notice.

20 days

Montana new hire reporting window

Employers must report every new hire to the Montana DPHHS within 20 days of start date. Missed reports trigger penalties.

$10.55

Montana minimum wage 2025

Indexed annually to inflation. No tip credit — tipped employees receive full minimum wage regardless of tips received.

The short answer:Montana payroll compliance has more moving parts than federal payroll alone. The employers who get penalties are almost never trying to cheat — they simply didn't know Montana's specific rules applied differently. This guide addresses every one of them.

Montana Payroll Law Basics Every Missoula Employer Must Know

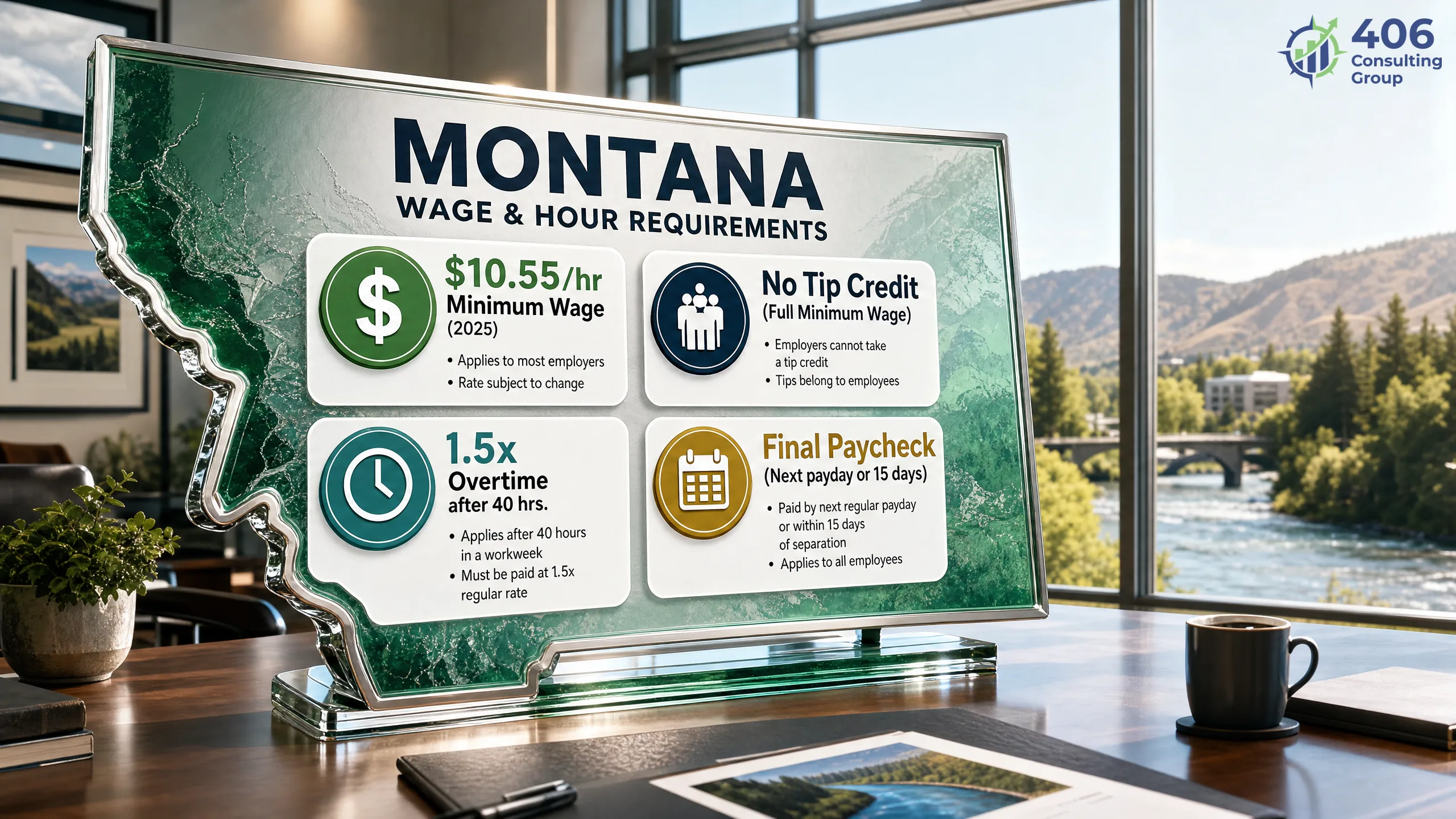

Montana's minimum wage is $10.55 per hour in 2025 — and unlike most states, Montana has no tip credit, meaning tipped employees must receive the full minimum wage regardless of gratuities received. Beyond minimum wage, Montana has several payroll requirements that differ from federal law and from neighboring states. These are not optional — they apply to every Missoula employer with at least one W-2 employee.

Montana Minimum Wage — No Tip Credit

Montana Dept. of Labor & IndustryMontana minimum wage is $10.55/hour in 2025 (up from $10.30/hour in 2024), indexed annually to the Consumer Price Index. Montana does not allow a tip credit — tipped employees in Missoula restaurants, hotels, and hospitality businesses must receive the full minimum wage regardless of tips. This is one of the most frequently violated rules by employers coming from other states.

Overtime — Federal FLSA Standard

FLSA, 29 U.S.C. § 207Montana follows the federal Fair Labor Standards Act overtime standard: 1.5× the regular rate for all hours worked over 40 in a workweek. Montana does not have a daily overtime threshold. Missoula employers with fluctuating workweeks or irregular scheduling must track hours weekly, not daily.

Final Paycheck — Next Regular Payday or 15 Days

Montana Code Annotated § 39-3-205When an employee leaves — voluntarily or involuntarily — their final paycheck must be issued by the earlier of: (1) the next regular payday, or (2) 15 days after separation. There is no exception for terminated employees. Withholding a final paycheck to recover company property or alleged damages is illegal in Montana.

Payday Frequency — Semi-Monthly Minimum

Montana Code Annotated § 39-3-204Montana requires employers to pay wages at least twice per month. Weekly or biweekly pay schedules are permitted. Monthly payroll is not compliant under Montana law for most employees. Payday frequency must be established and posted in the workplace.

New Hire Reporting — 20-Day Deadline

Montana Code Annotated § 40-5-922Every new employee must be reported to the Montana Department of Public Health and Human Services (DPHHS) within 20 days of hire. The report requires employee name, address, SSN, and start date. New hire reporting feeds Montana's child support enforcement and UI fraud detection systems.

Workers' Compensation — Mandatory for All Employees

Montana Code Annotated § 39-71-401Montana requires workers' compensation coverage for all employees, including part-time and seasonal workers. Coverage must be obtained through the Montana State Fund or an approved private insurer before the employee's first day of work. There is no grace period. Operating without coverage exposes Missoula employers to uninsured employer fund liability.

Wrongful Discharge from Employment Act (WDEA)

Montana Code Annotated § 39-2-901 et seq.Montana is the only U.S. state with a statutory just-cause requirement for employee termination. After a probationary period (up to 12 months), employers may only terminate employees for good cause. While this is primarily an employment law issue rather than a payroll one, it affects final paycheck obligations, severance documentation, and HR record retention for Missoula employers.

The Montana Payroll Stack: 5 Components of Compliant Payroll

The Montana Payroll Stack is the five-component framework that defines what compliant, accurate payroll looks like for a Missoula business. Each component depends on the one before it — you cannot calculate correct wages without proper classification, you cannot make accurate tax deposits without correct wage calculations, and year-end compliance fails when any prior component was done poorly throughout the year.

Employee Classification & Onboarding

Every worker classified correctly before day one. W-4 withholding set up. I-9 completed. Montana new hire report filed within 20 days. Workers' comp coverage confirmed.

Wage & Hour Compliance

Every payroll run at minimum wage or above. Overtime calculated on 40-hour weekly basis. No tip credit applied. Final paychecks issued on time. Records kept for 3 years.

Payroll Tax Deposits & Filing

Federal 941 deposits made on correct schedule. FUTA accrued quarterly. Montana income tax withheld and deposited. UI contributions calculated and paid quarterly.

Benefits & Deductions Administration

Workers' comp premiums correctly classified. Health, retirement, and FSA deductions withheld pre- or post-tax as required. Garnishments processed in correct priority order.

Year-End Compliance

W-2s issued by January 31. 1099-NECs issued by January 31. Form 940 FUTA reconciliation filed. Montana MW-3 annual reconciliation filed. All payroll totals reconcile to 941s.

Component 1: Employee Classification & Onboarding

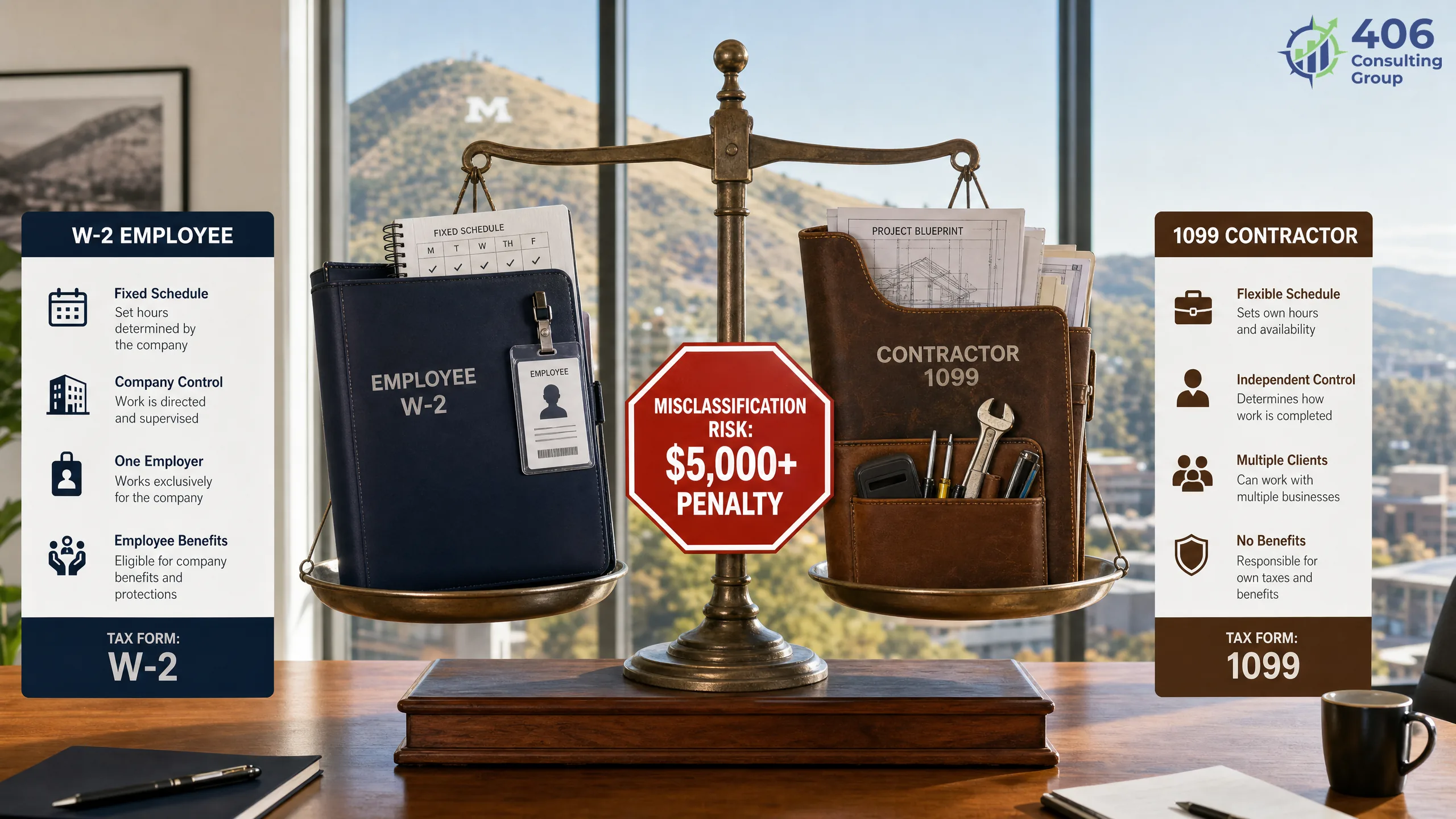

The most expensive payroll mistake Missoula businesses make is misclassifying an employee as an independent contractor. The short answer on classification: the IRS and Montana DLI apply a behavioral control, financial control, and relationship test. If you control how the work is done, the worker is almost certainly an employee — regardless of what the contract says.

W-2 Employee indicators

W-2- You set the work schedule and location

- You provide tools, equipment, or software

- The worker performs the core function of the business

- The relationship is ongoing with no defined end date

- You can terminate without a specific contract clause

- The worker cannot profit or lose based on business decisions

1099 Contractor indicators

1099- Worker controls how and when work is done

- Worker provides their own tools and equipment

- Worker has multiple clients and operates independently

- Engagement is project-specific with a defined end

- Worker can subcontract or hire assistants

- Worker risks profit or loss on the engagement

Onboarding checklist for every new employee:

Form W-4 — Federal Withholding

Complete before first paycheck. 2020+ W-4 does not use allowances — uses specific dollar amounts. Review annually or when employee's tax situation changes.

Montana Employee Withholding Allowance Certificate

Montana Form MW-4. Separate from federal W-4. If not completed, withhold at single/zero allowances — the most conservative default.

Form I-9 — Employment Eligibility Verification

Section 1 completed by employee on or before day one. Section 2 completed by employer within 3 business days of start. E-Verify optional in Montana (not mandatory for most private employers).

Montana New Hire Report

File with Montana DPHHS within 20 days of hire date. Online filing available at dphhs.mt.gov. Required for all employees including part-time and seasonal.

Workers' Compensation Notice

Provide written notice of workers' comp coverage to every new employee. Post required notices in the workplace per Montana State Fund requirements.

Component 2: Wage & Hour Compliance for Missoula Employers

Wage and hour compliance for Montana employers means paying at least $10.55/hour to every employee in 2025, calculating overtime correctly on a 40-hour weekly basis, issuing final paychecks on time, and keeping records for three years. The Montana Department of Labor and Industry investigates wage claims and has authority to recover back wages plus penalties.

| Requirement | Montana Rule | Common Mistake |

|---|---|---|

| Minimum wage (2025) | $10.55/hour — all employees | Applying a tip credit (illegal in Montana) |

| Minimum wage (2024) | $10.30/hour — verify for prior-year corrections | Using the prior year rate after January 1 |

| Overtime threshold | 40 hours/workweek — 1.5× regular rate | Calculating overtime daily instead of weekly |

| Tipped employees | Full minimum wage — no tip credit | Reducing base wage below minimum for tipped workers |

| Final paycheck | Next regular payday or 15 days — whichever is earlier | Holding check to recover unreturned equipment |

| Payday frequency | At least semi-monthly (twice/month) | Running monthly payroll for non-exempt employees |

| Record retention | 3 years for payroll records | Deleting payroll records after 1 year |

| Deduction rules | Only permitted deductions (taxes, benefits, court orders) | Deducting breakage, cash shortages, or training costs |

Missoula restaurant and hospitality employers:Montana's no-tip-credit rule is the single most frequently misapplied wage law in the state. If a Missoula server earns $8.00/hour in base pay and $6.00/hour in tips for a total of $14.00/hour — that is still a Montana wage violation. The base hourly rate must be at least $10.55 regardless of tip income. Back-wage claims in this space are common.

Component 3: Payroll Tax Deposits & Filing

Payroll tax deposits are the highest-penalty area of small business tax compliance. The IRS failure-to-deposit penalty runs 2–15% of the unpaid amount per incident — and it applies per deposit period, not annually. For a Missoula business missing three semi-weekly deposits in a quarter, that's three separate penalties. Here is the complete deposit and filing schedule.

Federal Income Tax + FICA (Form 941)

Monthly or Semi-Weekly — based on lookback periodDeposit schedule is determined by your lookback period (July 1–June 30 preceding year). If you reported $50,000 or less in payroll taxes during the lookback period: monthly depositor — deposit by the 15th of the following month. If you reported more than $50,000: semi-weekly depositor — wages paid Wednesday–Friday deposited by the following Wednesday; wages paid Saturday–Tuesday deposited by the following Friday.

Form 941 quarterly: April 30, July 31, October 31, January 31

Federal Unemployment Tax (FUTA — Form 940)

Quarterly if liability exceeds $500FUTA tax rate is 6% on the first $7,000 of each employee's wages. Montana employers receive a 5.4% credit for state UI contributions paid on time — resulting in a net federal FUTA rate of 0.6%. Deposit FUTA quarterly when cumulative liability exceeds $500. If liability never exceeds $500, pay with the annual Form 940.

Form 940 annual: January 31

Montana Income Tax Withholding

Quarterly, monthly, or accelerated — based on annual withholdingMontana withholding deposit frequency is determined by annual withholding amount: under $1,200/year = annual deposit; $1,200–$6,000/year = quarterly; $6,001–$12,000/year = monthly; over $12,000/year = accelerated (semi-monthly). File Form MW-1 quarterly. Montana withholding rate is 1–6.75% progressive based on income bracket.

Form MW-1 quarterly: April 30, July 31, October 31, January 31

Montana Unemployment Insurance (UI)

QuarterlyMontana's UI taxable wage base is $40,500 for 2025, meaning employers pay state unemployment tax only on the first $40,500 of each employee's wages per year. New employer rate varies by industry — typically 1.0–2.5%. Rates adjust annually based on employer experience rating. Quarterly UI returns filed with the Montana Unemployment Insurance Division. Late payments carry 1.5% monthly interest plus penalty.

Quarterly: April 30, July 31, October 31, January 31

Component 4: Benefits & Deductions Administration

Benefits and deductions administration is the component most likely to cause quiet, accumulating errors — pre-tax vs. post-tax treatment, incorrect workers' comp classification codes, and garnishment processing mistakes that create legal liability. Each deduction type has specific rules governing when it reduces taxable wages, when it doesn't, and how it interacts with Montana withholding.

Workers' Compensation

Tax treatmentEmployer expense — not a payroll deduction

Workers' comp premiums are paid by the employer — not deducted from employee wages. Premiums are calculated by classification code × payroll × rate. Misclassification (putting a roofer in a clerical code) triggers audit and back-premium assessment. Montana employers must verify classification codes annually — especially when adding new job types.

Audit risk for misclassification

Health Insurance Premiums (Group Plan)

Tax treatmentPre-tax (reduces federal and Montana taxable wages)

Employee contributions to employer-sponsored health insurance under a Section 125 cafeteria plan reduce federal and Montana income tax withholding, and reduce FICA wages. Without a formal Section 125 plan document, the pre-tax treatment is not valid. Many Missoula employers deduct health premiums pre-tax without a valid plan — creating retroactive tax liability.

Invalid pre-tax treatment without Section 125

401(k) / Simple IRA Deferrals

Tax treatmentPre-tax for federal income tax; not exempt from FICA

Traditional 401(k) and SIMPLE IRA deferrals reduce federal and Montana income tax withholding but are still subject to Social Security and Medicare. Roth 401(k) contributions are post-tax — withheld after all payroll taxes. Employer matching contributions are reported on W-2 Box 12.

Incorrect pre-tax/post-tax treatment

Wage Garnishments

Tax treatmentPost-tax — garnishments do not reduce taxable wages

Child support, federal tax levies, student loan garnishments, and creditor garnishments are withheld after taxes. Montana follows federal garnishment limits: disposable earnings above 25% (or 30× federal minimum wage — whichever is less) may be garnished. Priority order matters when an employee has multiple garnishments: child support first, then tax levies, then creditor garnishments.

Priority order errors and incorrect limits

Component 5: Year-End Payroll Compliance

Year-end payroll compliance runs from December through January 31 — the hard deadline for W-2s, 1099-NECs, Form 940, and Montana's MW-3 reconciliation. Missing January 31 triggers IRS penalties of $60–$630 per form (depending on size and how late), plus Montana DOR penalties. Here is the complete year-end sequence.

December 31

Final payroll adjustments

Process any bonus payroll, third-party sick pay adjustments, fringe benefit additions to W-2 wages (personal use of company vehicle, group-term life over $50K, employer HSA contributions), and year-end owner distributions.

January 15

December payroll tax deposit (monthly depositors)

Monthly depositors: December 941 taxes due January 15. Semi-weekly depositors: December deposits made on normal semi-weekly schedule.

January 31

W-2s to employees

Every W-2 must be postmarked or delivered (or electronically transmitted with consent) by January 31. Copies B, C, and 2 go to the employee. Late W-2s carry penalties of $60–$330 per form (depending on days late), up to $630 per form for intentional disregard.

January 31

1099-NECs to contractors

Any contractor paid $600 or more during the year receives a 1099-NEC by January 31. This includes subcontractors, freelancers, consultants, and any non-employee individual paid for services. File Copy A with the IRS by January 31 as well (no February 28 extension for 1099-NEC).

January 31

Form 940 (FUTA) annual return

File Form 940 and pay any remaining FUTA balance by January 31. If you deposited all FUTA on time quarterly, you have until February 10. Montana employers should verify the 5.4% FUTA credit — it requires Montana UI contributions to be paid on time throughout the year.

January 31

Form 941 (Q4) quarterly return

Q4 Form 941 is due January 31. Reconcile total wages, tips, and compensation to W-2 Box 1 totals. Reconcile FICA wages to W-2 Boxes 3 and 5. Any discrepancy requires investigation and correction before filing.

January 31

Montana MW-3 annual reconciliation

Montana Form MW-3 reconciles annual Montana withholding to the amounts reported on employee W-2s (Box 17). Attach copies of all W-2s. Any withholding balance due must be paid with the MW-3.

February 28 / March 31

W-2 Copy A and 1099s to SSA/IRS

Paper W-2s filed with Social Security Administration by February 28. Electronic filers (25+ forms required; 10+ recommended) file by March 31. 1099 Copy A to IRS also by February 28 (paper) or March 31 (electronic) — except 1099-NEC which was due January 31.

Missoula Industry Spotlights: Payroll by Sector

Missoula's economic mix — University of Montana, healthcare, outdoor recreation, technology, and construction — creates industry-specific payroll issues that generic guides miss entirely.

University of Montana & Education

Missoula- 1Student FICA exemption: students enrolled at least half-time in a degree program and working for UM may be exempt from Social Security and Medicare withholding — but the exemption requires proper documentation and does not apply during academic breaks

- 2Graduate assistant stipends: taxable wages requiring W-4 withholding, not fellowships — a distinction UM-adjacent employers frequently get wrong

- 3Seasonal and adjunct faculty: part-year employment creates UI base-period complications for unemployment claims

- 4Montana public employer pension: UM employees contribute to PERS (Public Employees' Retirement System) — different from private employer 401(k) rules

Healthcare & Providence St. Patrick

Missoula- 1Shift differentials and on-call pay: must be included in the regular rate for overtime calculation — a compliance gap in many Missoula healthcare staffing arrangements

- 2Travel nurse and agency worker classification: 1099 treatment of traveling clinical staff is frequently challenged; most travel nurses placed through agencies are W-2 employees of the agency

- 3Physician compensation: production-based physician compensation (RVU or collections model) requires careful W-2 structuring for employed physicians

- 4PRN (per diem) staff: hours vary weekly; overtime must be calculated on actual hours worked, not average hours

Outdoor Recreation & Hospitality

Missoula- 1Seasonal layoffs: Montana UI experience rating is affected by seasonal separations — Missoula outfitters and ski-area adjacent businesses should understand how layoff patterns affect their UI rate

- 2No tip credit — full minimum wage required: Missoula restaurant, hotel, and guide service operators cannot reduce base pay below $10.55/hour regardless of tips

- 3Seasonal housing and meals: employer-provided lodging for guide operations may be taxable wages if not meeting the convenience-of-employer test

- 4Non-resident seasonal workers: out-of-state employees working in Montana are subject to Montana income tax withholding for wages earned in Montana

Technology & Remote Work

Missoula- 1Remote workers in Montana: out-of-state employers with Montana remote employees create Montana nexus — Montana income tax withholding required for wages earned in Montana

- 2Multi-state withholding: Montana employees working partly in other states may require withholding in each state where work is performed — reciprocity agreements do not exist between Montana and most states

- 3Stock option and RSU vesting: equity compensation vesting triggers W-2 income — timing and withholding calculation require careful coordination with payroll

- 4PEO arrangements: many Missoula tech companies use Professional Employer Organizations — ensure the PEO handles Montana-specific compliance (no tip credit, WDEA documentation) correctly

Construction & Contractors

Missoula- 1Prevailing wage on public projects: Montana public construction projects subject to the Montana Prevailing Wage Act require certified payroll reports and payment at prevailing wage rates by trade — rates vary by county and trade classification

- 2Subcontractor vs. employee: the construction industry has the highest misclassification audit rate in Montana — day laborers and trade helpers working under close supervision are typically employees

- 3Workers' comp classification codes: roofing, framing, excavation, and electrical carry very different workers' comp rates — misclassification is the most common construction payroll audit trigger

- 4Seasonal cash flow and payroll: construction payroll peaks in summer and drops in winter — Montana UI contributions in peak months create the base for winter UI claims from laid-off workers

DIY vs. Professional Payroll: The Real Cost Comparison

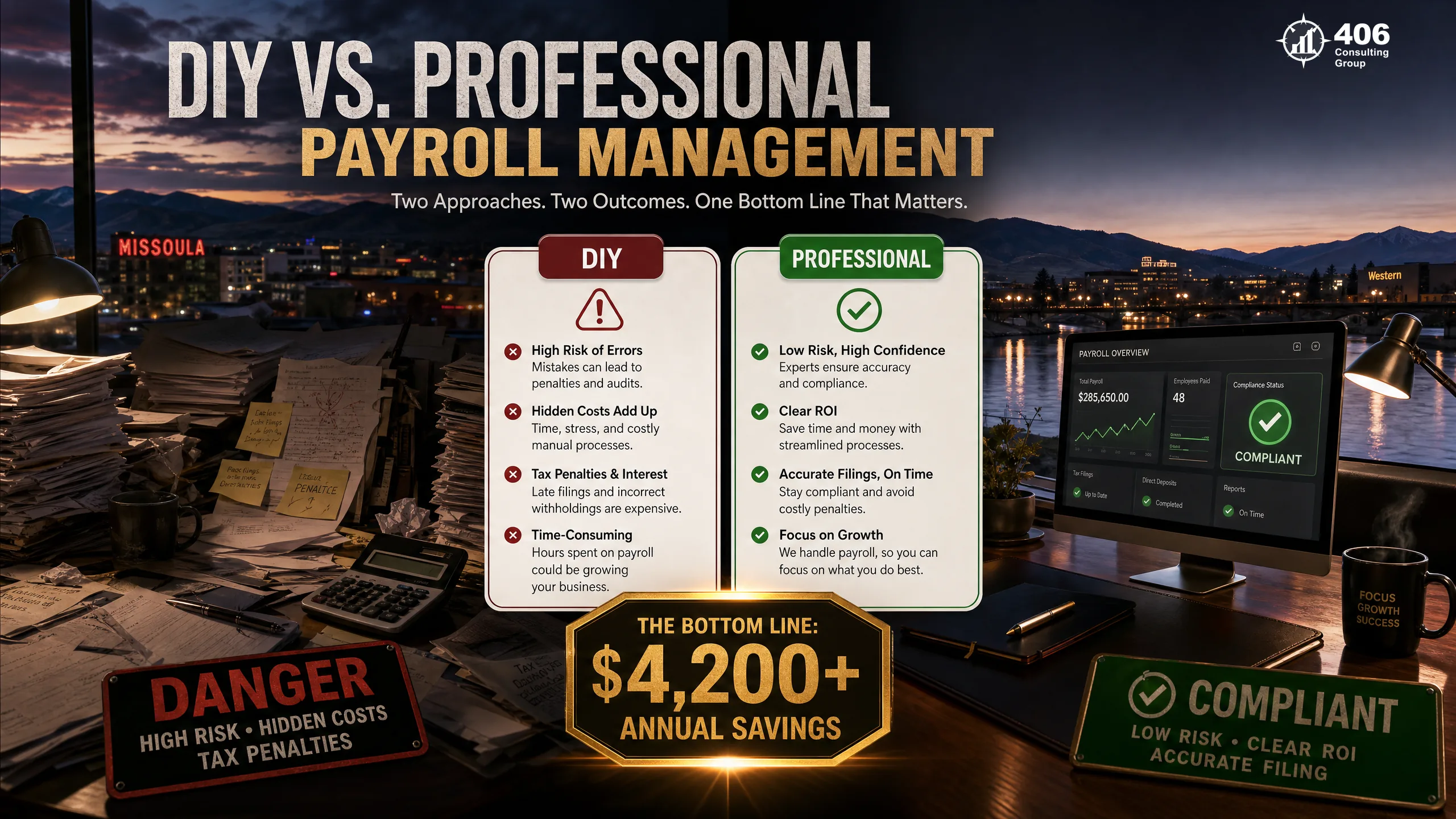

DIY payroll for a Missoula business with 5–15 employees runs 4–8 hours per month of owner or office manager time, carries non-trivial penalty risk on every deposit cycle, and requires staying current with annual rate changes in Montana minimum wage, UI taxable wage base, and withholding tables. Professional payroll eliminates the time, the penalty risk, and the annual compliance maintenance burden.

DIY Payroll — True Annual Cost

True cost: $8,000–$22,000+/yr- Owner/staff time: 4–8 hrs/month × $50–$100/hr = $2,400–$9,600/year

- Software (QuickBooks Payroll, Gusto basic): $600–$1,800/year

- One missed deposit penalty (5–10% of payroll taxes): $500–$5,000/incident

- One W-2 correction or 1099 late filing: $60–$630 per form

- Montana UI rate increase from misclassified separations: $500–$3,000/year

- Legal/HR cost from wage claim (missed tip credit, late final check): $2,000–$15,000+

Professional Payroll — What You Get

$150–$400/month- All payroll processed on time, every pay period

- All federal and Montana tax deposits made on correct schedule

- All quarterly returns filed (941, MW-1, UI) without owner involvement

- W-2s and 1099-NECs issued by January 31, filed with SSA/IRS

- Montana new hire reports filed within 20-day window

- Annual compliance updates (minimum wage, UI rates, withholding tables) applied automatically

Choosing Payroll Software for Missoula Businesses

For Missoula businesses running payroll in-house, the right software handles Montana-specific tax tables automatically, integrates with your bookkeeping software, and files returns without manual intervention. Here's how the major platforms compare for Montana employers.

| Platform | Best for | Montana compliance | Cost (approx.) |

|---|---|---|---|

| Gusto | 1–50 employees, tech-forward | Strong — auto-files Montana returns, handles new hire reporting | $46/mo + $6/employee |

| QuickBooks Payroll | Businesses already on QBO | Good — integrated with QuickBooks, Montana tax tables updated | $45–$125/mo + $6/employee |

| ADP Run | 5–50 employees, growth stage | Strong — Montana compliance supported, dedicated support | $60–$150/mo + $4–$8/employee |

| Paychex Flex | 10+ employees, complex benefits | Strong — Montana certified, prevailing wage support available | $60–$200/mo + $4–$9/employee |

| Patriot Payroll | Budget-conscious, simple payroll | Adequate — Montana taxes handled, fewer integrations | $17–$37/mo + $4/employee |

Our recommendation for most Missoula businesses:Gusto for businesses under 30 employees wanting a clean, modern interface with strong Montana compliance automation. QuickBooks Payroll for businesses already running QuickBooks Online who want one integrated system. ADP or Paychex for businesses with complex benefits, multi-state employees, or prevailing wage obligations that need dedicated support. All of these integrate with a professional bookkeeper's workflow — your payroll data flows directly into your general ledger without manual entry.

Professional Payroll Pricing for Missoula Businesses

Professional payroll services for Missoula businesses typically run $150–$500 per month depending on employee count, pay frequency, and whether the service includes return filing. Here's what to expect at each level — and what you should be getting for the price.

Basic Payroll Processing

$150–$250/mo1–10 employees

- Payroll processing each pay period

- Federal and Montana tax deposits on correct schedule

- Quarterly 941, MW-1, and UI return filing

- Direct deposit for all employees

- January W-2 and 1099-NEC issuance

Full-Service Payroll

$250–$400/mo10–25 employees

- Everything in Basic

- Montana new hire reporting

- Workers' comp audit support

- Benefits deduction administration

- Garnishment processing

- Year-end reconciliation and MW-3 filing

HR-Integrated Payroll

$400–$600+/mo25+ employees or complex

- Everything in Full-Service

- Multi-state withholding (remote workers)

- Prevailing wage certified payroll reports

- ACA reporting (50+ employees)

- PTO accrual tracking

- HR compliance support

Frequently Asked Questions

What is the Montana minimum wage in 2025?

The Montana minimum wage is $10.55 per hour in 2025, up from $10.30 per hour in 2024. Montana indexes its minimum wage annually to the Consumer Price Index — the rate adjusts every January 1. Montana does not allow a tip credit: tipped employees must receive the full $10.55/hour minimum wage regardless of tips earned. Employers who applied a tip credit or paid below minimum wage are subject to back-wage claims.

Does Montana require workers' compensation for all employees?

Yes. Montana requires workers' compensation coverage for all employees — including part-time, seasonal, and temporary workers — before they begin work. Coverage must be obtained through the Montana State Fund or an approved private insurer. There is no grace period and no minimum hours threshold. Operating without workers' comp coverage in Montana exposes employers to uninsured employer fund liability, which means the state pays the claim and seeks reimbursement from the employer — often far exceeding what insurance would have cost.

What's the difference between an employee and an independent contractor in Montana?

The IRS and Montana DLI use a three-factor test: behavioral control (do you control how the work is done?), financial control (does the worker invest in their own tools and risk profit or loss?), and the type of relationship (is it ongoing with benefits, or project-specific?). If you set the schedule, provide the tools, and the worker performs your core business function, they are almost certainly an employee — regardless of what the contract says. Misclassification triggers back taxes, FICA penalties, workers' comp back-premiums, and interest.

When must employers deposit payroll taxes?

Federal payroll tax deposit timing depends on your lookback period. Monthly depositors (under $50,000 in payroll taxes during the lookback period) must deposit by the 15th of the following month. Semi-weekly depositors (over $50,000) deposit within 3 business days of each payroll. Montana income tax withholding deposit frequency is determined separately by annual withholding amount. Montana UI contributions are deposited quarterly.

What happens if I miss a payroll tax deposit deadline?

The IRS failure-to-deposit penalty applies immediately and automatically: 2% for deposits 1–5 days late, 5% for 6–15 days late, 10% for more than 15 days late, and 15% for deposits not made within 10 days of the first IRS notice. The penalty applies to each missed deposit separately — not to the quarter as a whole. For a Missoula business with $15,000/month in payroll tax liability, a single missed semi-weekly deposit can carry a $750–$2,250 penalty.

Do Missoula employers need to pay overtime?

Yes. Montana follows the federal FLSA overtime standard: non-exempt employees must receive 1.5× their regular rate for all hours worked over 40 in a workweek. Montana does not have a daily overtime threshold — overtime is calculated on the weekly 40-hour basis only. Shift differentials, production bonuses, and on-call pay must generally be included in the regular rate for overtime calculation purposes.

External Resources

Missoula, MT

Compliant Payroll for Missoula Businesses

406 Consulting Group handles payroll processing, Montana tax deposits, quarterly returns, and year-end compliance for Missoula businesses — so you focus on the work, not the compliance calendar.

The Montana Payroll Stack

5 components — sequential, interdependent

Employee Classification

W-2 vs. 1099, onboarding, new hire reporting

Wage & Hour Compliance

MT minimum wage, overtime, final paychecks

Tax Deposits & Filing

941, FUTA, MT withholding, UI — on schedule

Benefits & Deductions

Workers' comp, health, 401(k), garnishments

Year-End Compliance

W-2, 1099-NEC, 940, Montana MW-3

Montana Payroll Quick Reference

Related Guides