Strategic Financial Leadership:

CFO Services in Missoula, MT

Missoula businesses outgrowing their bookkeeper need CFO-level financial leadership. Here's what a fractional CFO delivers — and when Missoula companies need one.

CFO services in Missoula, MT are no longer reserved for corporations. A fractional CFO gives Missoula's growing businesses — outdoor and recreation companies, healthcare practices, technology firms, construction contractors, and professional services — the financial leadership that turns good revenue into actual wealth. The question isn't whether you need it. It's whether you can afford to keep operating without it.

This guide covers what a fractional CFO actually delivers month-to-month, the five-module system that separates CFO-level thinking from bookkeeping, when Missoula businesses hit the inflection point where CFO involvement pays for itself, and what to expect from a real engagement — not a sales pitch.

Table of Contents

Why Missoula Businesses Need CFO-Level Leadership Now

Missoula is growing faster than its financial infrastructure. The city's economic diversification — driven by University of Montana expansion, a booming outdoor and recreation economy, an influx of remote workers and technology firms, downtown development, and a healthcare sector anchored by Providence St. Patrick Hospital — is producing businesses that have outpaced their current financial systems without realizing it.

$1M–$10M

The CFO inflection zone

Where most Missoula businesses are operating without the financial leadership the revenue demands

300+

Commercial loans analyzed

Our team brings the lender's perspective to every capital conversation — from the inside

$8M→$40M

Construction client growth

Multi-year CFO engagement — financial infrastructure that made scaling possible without breakdown

The pattern is consistent: a Missoula business crosses $800K in revenue, adds employees, takes on more complex projects or service lines, and suddenly the bookkeeper who was adequate at $400K is the ceiling on growth. Not because they're bad at their job — but because CFO work is a different discipline entirely.

The infrastructure gap:Most financial advisory underperforms when strategy is layered onto weak reporting, inconsistent books, or missing financial infrastructure. The advice is real — the foundation isn't there to support it. The right sequence is always: build the infrastructure first, then drive strategy on top of it.

What a Fractional CFO Actually Does

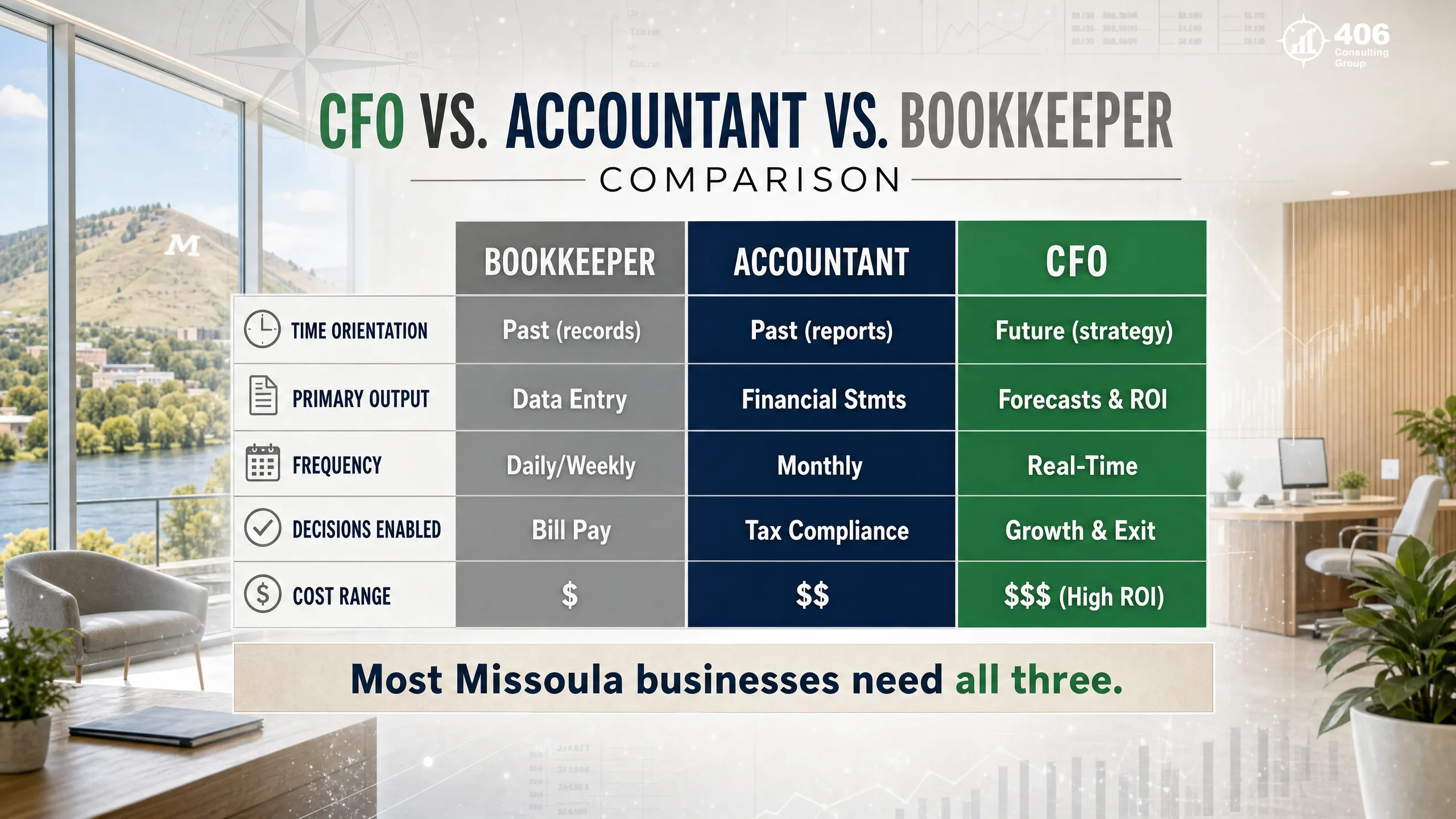

A fractional CFO is a senior financial executive who works with your business part-time or on a retainer basis — delivering the same strategic financial leadership a full-time CFO provides, without the $200,000+ annual salary. The short answer: a fractional CFO shapes where your business is going financially. A bookkeeper records where it's been.

Bookkeeper

Records the pastPrimary output

Reconciled accounts, categorized transactions, monthly reports

Frequency

Monthly close

Decisions enabled

None — provides the data

Accountant / CPA

Reports the pastPrimary output

Tax returns, compiled financials, compliance filings

Frequency

Annual (primarily)

Decisions enabled

Tax position, entity structure

CFO

Shapes the futurePrimary output

Forecasts, capital strategy, KPI dashboards, growth planning

Frequency

Monthly + quarterly

Decisions enabled

Pricing, hiring, capital, exit, growth

Most Missoula businesses that engage 406 Consulting Group need all three — and most are missing the CFO layer entirely. What that missing layer costs shows up everywhere: in pricing decisions made without margin data, in hiring decisions made without a cash flow projection, in loan applications that take months instead of weeks, and in tax bills that are higher than they had to be.

What a fractional CFO is not: A fractional CFO is not a glorified bookkeeper with a better title. They are not someone who reviews your QuickBooks once a month and sends you a report you already have. A real CFO engagement produces decisions — about pricing, capital allocation, hiring timing, tax strategy, and growth sequencing — that measurably improve business outcomes.

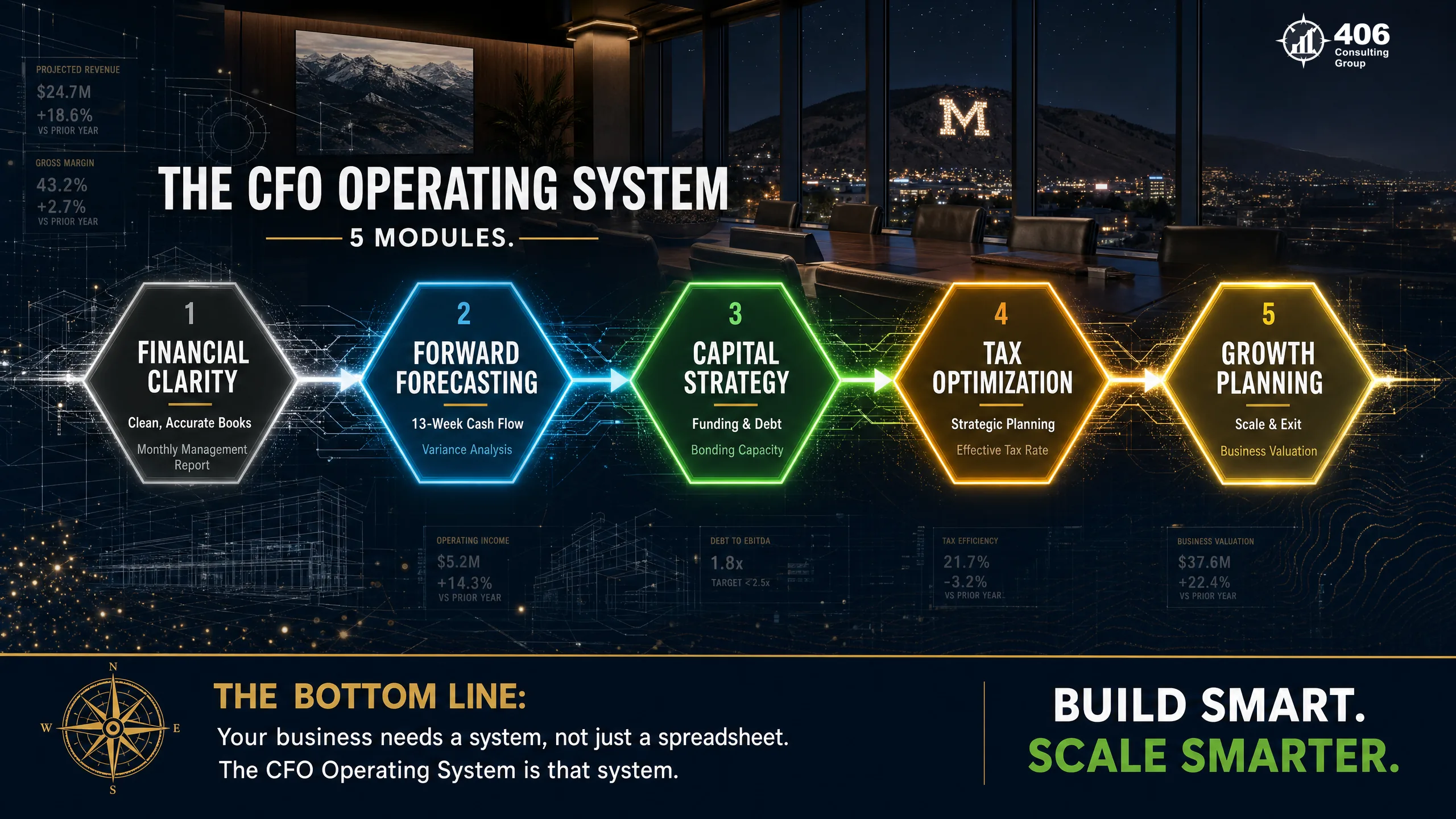

The CFO Operating System: 5 Modules That Drive Financial Leadership

The CFO Operating System is the five-module framework that defines what professional financial leadership looks like in practice. Each module depends on the one before it. You cannot forecast accurately without financial clarity. You cannot access capital without a credible forecast. You cannot optimize taxes without knowing your current-year position. The system only produces growth when all five are running.

Financial Clarity

You cannot manage what you cannot see.Monthly management reporting package — not just P&L and balance sheet, but a KPI dashboard built for your specific business. Revenue by service line or product. Gross margin by job or offering. Labor as a percentage of revenue. Receivables aging. Cash runway. The numbers that actually drive your business, visible every month without waiting for your accountant to call.

Forward Forecasting

Strategy is just a guess without a model.A rolling 13-week cash flow projection updated monthly. An annual budget built from real historical data — not aspirational revenue goals. Scenario modeling: what does the business look like if revenue is 15% lower than plan? If a key contract doesn't renew? If you add two employees in Q2? Decisions made with a forecast are better than decisions made from a bank balance.

Capital Strategy

Capital is available. Readiness is not.A complete view of your debt options — SBA programs, First Interstate and Stockman commercial lines, equipment finance, and Montana-specific resources including MBAC and SBDC programs — with a debt service model showing exactly what each option costs against your projected cash flow. When you're ready to borrow, the package is already built. The answer isn't months away — it's ready.

Tax Optimization

Tax strategy requires current-year data.Quarterly coordination between your CFO, your bookkeeper, and your tax preparer to time depreciation elections, equipment purchases, retirement contributions, entity distributions, and estimated payments. S-Corp election analysis. Retirement plan structuring. Decisions made in October, not discovered in March. At 406, Jason's 10+ years of tax preparation experience means tax strategy is built into the CFO engagement — not siloed in a separate firm that doesn't see your books until year-end.

Growth Planning

Growth without a plan is just bigger risk.Profitability by service line — which offerings to expand, which to exit, which to reprice. Acquisition target evaluation if M&A is in the plan. Exit readiness: financial statements that survive due diligence, valuation modeling, owner compensation structured for maximum after-tax proceeds. A Missoula business that grows from $2M to $8M without a growth plan often finds it arrived there without the margin it expected.

Module 1: Financial Clarity — Management Reporting That Actually Manages

Most Missoula business owners receive financial reports. Very few receive management reports. The difference is significant: a financial report records what happened. A management report tells you what it means and what to do about it.

Standard financial reporting

What most businesses have- P&L statement — company-wide, monthly

- Balance sheet — assets, liabilities, equity

- Bank reconciliation confirmation

- Delivered 15–20 days after month-end

- Reviewed once, filed away

CFO-level management reporting

What the CFO Operating System delivers- Revenue and gross margin by service line or product

- Labor efficiency ratio tracked monthly against target

- Receivables aging with 30/60/90+ day breakdown and commentary

- Cash runway — days of operating expenses covered by current cash

- 3 KPIs specific to your business reviewed and flagged monthly

- Delivered within 10 days, reviewed with the owner, not just emailed

Module 2: Forward Forecasting — Decisions Before the Crisis

Forecasting is the most underutilized financial tool in small and mid-market business — and the one that pays for CFO engagement fastest. A rolling 13-week cash flow projection, updated monthly from actual data, answers the questions that keep Missoula business owners awake at night: Can I make payroll in February? Can I hire in Q2? What happens if my largest client doesn't renew?

Rolling 13-Week Cash Flow

Starting from today's bank balance, adding all expected collections by date (receivables, retainage releases, recurring revenue, contract draws), and subtracting all committed outflows (payroll by date, vendor payments by schedule, debt service, tax deposits, owner distributions). Updated monthly. Validated against actual. The gaps this reveals are actionable — six weeks out, not six days.

Annual Budget

Built from actual historical data — not revenue goals. Revenue by service line based on signed contracts, pipeline probability, and seasonal pattern. Expenses broken into fixed and variable. Headcount plan with timing. Capital expenditure schedule. Owner compensation modeled explicitly. The budget becomes the benchmark — monthly actuals compared against it, variances explained.

Scenario Modeling

Three scenarios — base, upside, downside — built in parallel. Base: current trajectory. Upside: specific growth assumptions (new contract won, expansion complete). Downside: key risk materializes (large client lost, revenue 20% below plan). Each scenario shows cash position month by month. Decisions made in the context of all three are materially better than decisions made from a single forecast.

What Carrie built for a Flathead Valley client:When a hospitality client needed a line of credit in 30 days, 12 months of clean, lender-ready financials were already in place. They got approved. The forecast wasn't built under pressure — it was already running. That's the difference between a business that can move fast and one that has to wait.

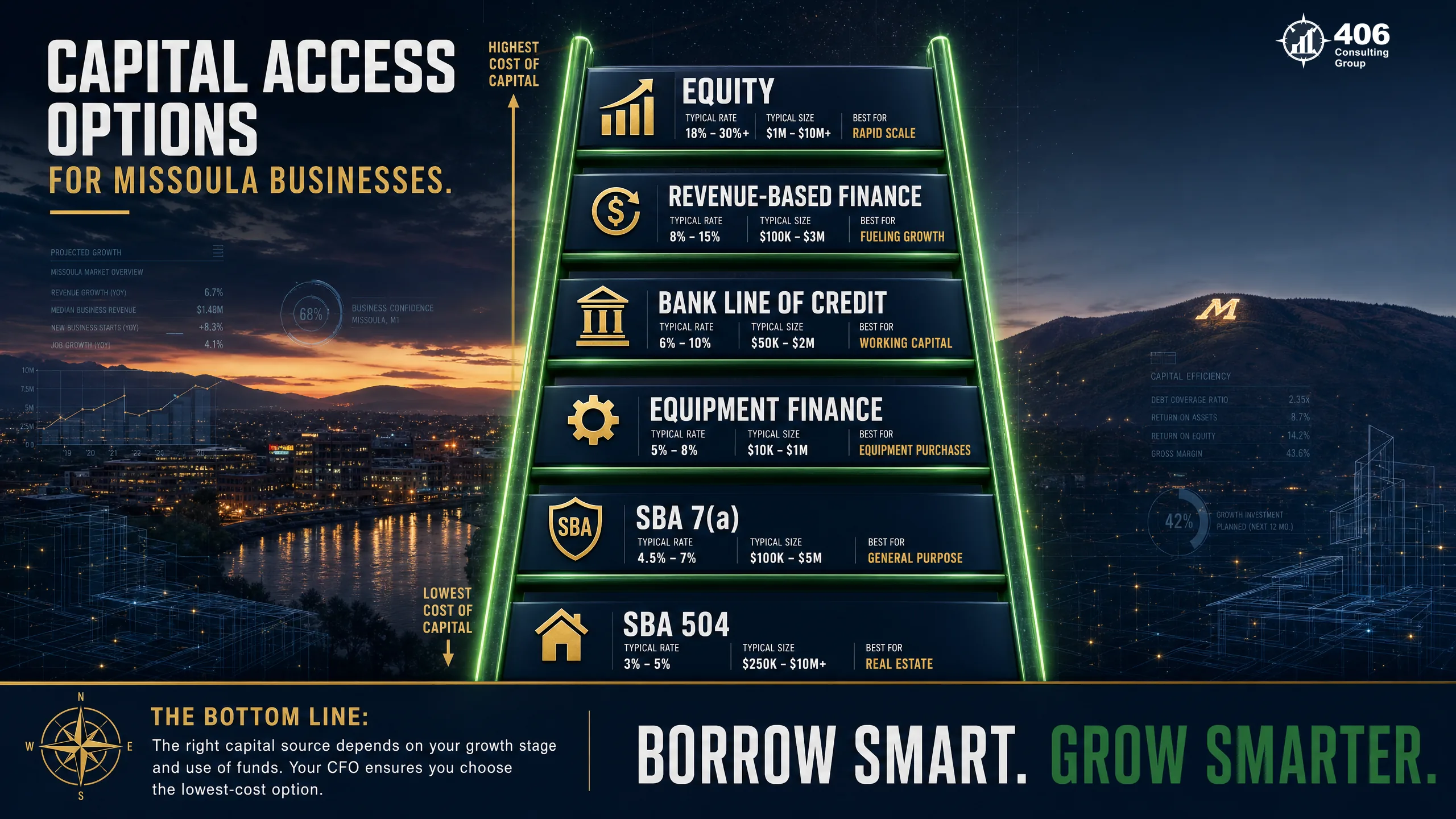

Module 3: Capital Strategy — Accessing the Right Capital at the Right Time

Capital is available to Missoula businesses. Readiness is the constraint — not the money itself. The difference between a Missoula business that closes an SBA 504 in 60 days and one that waits six months is almost always the quality of its financial package, not the strength of the business. Our team has been on both sides of that table.

SBA 504 — Commercial Real Estate & Heavy Equipment

Real estate acquisition, major equipment purchases. The CDC portion carries a fixed below-market rate — significantly cheaper than conventional financing for purchases over $250K. Underutilized by Montana businesses.

Readiness requirements: Three years financials, forecast, appraisal, environmental

SBA 7(a) — Working Capital & Acquisition

Business acquisition, working capital, expansion. Detailed underwriting — SBA-standard projections required. Carrie rebuilt the books and delivered bank-grade projections for an auto body group with five locations and multiple entities, closing a $7M SBA outcome after their prior CPA's forecasts weren't bank-grade.

Readiness requirements: Three years financials, SBA-format projections, personal financial statement

First Interstate / Stockman / Glacier — Commercial Lines

Operating lines of credit secured by receivables, equipment financing, project financing. Missoula lenders underwrite construction, healthcare, and professional services companies regularly. Approval depends on financial statement quality, DSCR, and working capital ratio.

Readiness requirements: Current financials consistent with tax returns, AR aging, 12 months bank statements

Montana SBDC / MBAC — Montana-Specific Programs

Montana Big Sky Economic Development Trust Fund, Montana SBDC loan packaging assistance, rural development programs. Less utilized — significant opportunity for Missoula businesses that qualify.

Readiness requirements: Business plan, financials, demonstrated community economic impact

Module 4: Tax Optimization — Strategy Requires Current-Year Visibility

Tax optimization is not something that happens in March. It happens throughout the year, in real time, from current book data. The decisions that actually reduce a Missoula business owner's tax liability — retirement contributions, depreciation elections, equipment timing, distribution strategy, entity structure — are made in October, not discovered after the fact.

S-Corp Election Timing

$10,000–$25,000+/yearMarch 15 deadline for current year

For Missoula service businesses with net income above $60,000–$80,000, S-Corp election is often the single highest-impact tax decision available. At 406, we don't wait for clients to ask — when a client came in to sign their taxes, the S-Corp election paperwork was already prepared and the $13,000 in projected annual savings was already calculated. That's the difference between reactive and proactive.

Retirement Plan Optimization

$10,000–$60,000+/year deductionSEP-IRA: tax filing deadline | Solo 401(k): Dec 31

SEP-IRA contributions of up to 25% of net income. Solo 401(k) with employee and employer contributions. Defined benefit plan for highest earners. The optimal contribution requires accurate current-year net income — only calculable from monthly books. A business owner with $200,000 in net income choosing between plan types without current-year data is leaving $10,000–$40,000 in deductions on the table.

Depreciation Election Strategy

Varies — $5,000–$40,000+ impactAt time of purchase — not retroactively

Section 179 full expensing, 100% bonus depreciation (permanently restored under OBBBA, July 2025), or straight-line — the right choice depends on current-year income, future income projections, and balance sheet implications for bonding and lending. An $80,000 equipment purchase fully expensed in a $280,000 net income year vs. a $140,000 year produces materially different outcomes. This decision requires a CFO, not a tax preparer seeing the books in March.

Entity Structure & Owner Compensation

$5,000–$20,000+/yearReviewed annually

For Missoula S-Corp owners, the balance between W-2 salary and distributions is the primary driver of payroll tax savings. Too low a salary is an IRS audit flag. Too high eliminates the savings. The right number requires knowing current-year net income, industry reasonable compensation benchmarks, and the owner's personal financial situation. Jason's accounting background and 10+ years of tax preparation experience make this analysis a core part of every CFO engagement.

Module 5: Growth Planning — Building a Business Worth What It Should Be Worth

Growth planning at the CFO level is the difference between a Missoula business that grows and a Missoula business that compounds. Revenue growth without margin discipline, capital efficiency, and exit readiness produces a larger business — not necessarily a more valuable one.

Profitability by service line

Which of your offerings actually makes money? Which are subsidizing underperformers? A Missoula professional services firm with four service lines often finds that two are generating 80% of the margin. A CFO-level profitability analysis by offering — with fully loaded costs including overhead allocation — answers this question and enables re-pricing, expansion, or exit of the right lines.

Acquisition target evaluation

For Missoula businesses considering growth through acquisition, the CFO provides the financial due diligence framework: normalized EBITDA calculation, working capital adjustment, off-balance-sheet liability identification, and integration cost modeling. Jason's background identifying $75M in unbilled inventory at BP — money the company didn't know it was owed — reflects the kind of analytical discipline that finds what others miss in a financial review.

Exit readiness & valuation modeling

Whether you're planning a sale in 2 years or 10, the work that makes a business worth more starts now. Financial statements that survive due diligence. Owner compensation structured for maximum after-tax proceeds from a sale. Systems and documentation that reduce key-person dependency. Valuation modeling showing your current multiple and the specific actions that move it. Carrie grew up in a family that acquired underperforming businesses, fixed the operations and financials, and sold them at a profit — that background shapes how 406 approaches every engagement from day one.

Pricing strategy modeling

Most Missoula businesses price by instinct, by competitive benchmarking, or by cost-plus — rarely from a model that captures true cost-to-serve including overhead allocation, customer acquisition cost, and service delivery time. A CFO pricing analysis identifies which clients and service combinations are profitable and which are consuming capacity without returning adequate margin.

Missoula Industry Spotlights: CFO Services by Sector

Missoula's economic diversity means CFO priorities differ significantly by sector. Here's what financial leadership looks like in each of Missoula's primary business categories.

Outdoor & Recreation

Missoula sector- 1Seasonal cash flow modeling — 4–5 month revenue window financing 12 months of operations

- 2Inventory financing for equipment-intensive retail and rental operations

- 3Revenue diversification modeling — reducing dependence on peak season

- 4Brand valuation for exit — outdoor brands carry premium multiples when financials are clean

Technology & Remote Work

Missoula sector- 1Recurring revenue tracking — MRR, ARR, churn rate, and lifetime value as core KPIs

- 2R&D tax credit eligibility — significant deduction many Montana tech firms miss

- 3Multi-state revenue allocation as remote client base grows — Montana plus income-sourced elsewhere

- 4Equity and option plan modeling for businesses considering investor capital

Healthcare & Medical Practices

Missoula sector- 1Insurance reimbursement modeling — billed vs. collected and contractual allowance tracking

- 2Provider compensation structuring — physician partner W-2 vs. K-1 optimization

- 3Multi-entity structure management — professional corporation plus management services entity

- 4HIPAA-compliant financial systems and reporting for PE interest or partnership transactions

Construction & Contractors

Missoula sector- 1WIP schedule and percentage-of-completion revenue recognition — see our full guide on construction accounting for Missoula contractors

- 2Job costing with labor variance reporting — catching overruns at Week 3, not at closeout

- 3Bonding capacity modeling — balance sheet management to maximize surety limits

- 4Seasonal cash flow with retainage schedule — rolling 90-day projection essential

Professional Services

Missoula sector- 1Profitability by client and service line — identifying which work to pursue and which to exit

- 2Billing rate analysis — comparing realized rate to standard rate to identify revenue leakage

- 3Owner compensation optimization — S-Corp reasonable salary vs. distributions at each revenue level

- 4Practice valuation for merger, partnership, or exit — financial statement quality drives multiple

Hospitality & Food & Beverage

Missoula sector- 1Prime cost management — labor plus food cost as the primary margin lever in hospitality

- 2Seasonal revenue smoothing and off-season cash management

- 3Multi-location financial infrastructure — entity structure, intercompany, and consolidated reporting

- 4Lender package for expansion — Missoula hospitality expansion often involves SBA 504 real estate financing

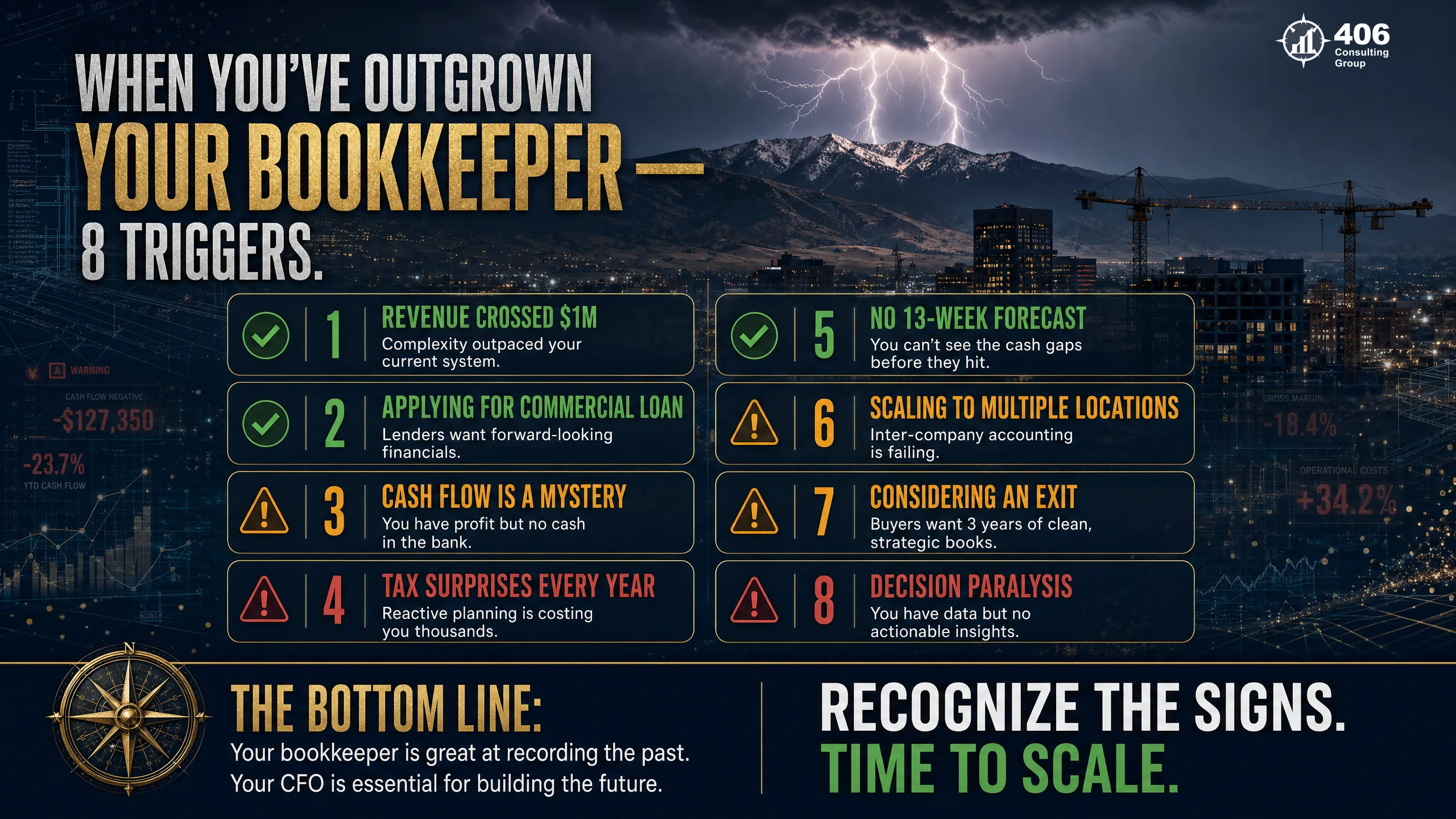

When You've Outgrown Your Bookkeeper: 8 Triggers

The moment a Missoula business needs CFO-level involvement is almost always visible in hindsight — and almost always identifiable in advance if you know what to look for. Here are the eight most reliable signals.

Revenue crossed $1M

The complexity of managing cash flow, multiple employees, and tax obligations at $1M+ consistently exceeds what monthly bookkeeping provides. This isn't about the bookkeeper — it's about the scope of the role.

You're applying for a commercial loan

Lenders want forward-looking financials — forecasts, projections, and a clear narrative about the business. A bookkeeper produces historical reports. A CFO produces the package that gets the loan.

You made a major hiring or investment decision and weren't sure it was right

If you hired someone or bought equipment and you're not sure whether the cash flow supports it, you made the decision without a forecast. That's the signal.

Your tax preparer surprised you with a large bill in March

Tax surprises are a forecasting failure — not a tax law problem. A CFO coordinates tax timing throughout the year from current book data. Surprises don't happen.

You don't know which parts of your business are profitable

Revenue tells you what you sold. Margin by service line tells you what made money. If you can't answer the second question quickly, you're running on incomplete information.

You're thinking about selling or bringing on a partner in the next 3–5 years

The financial work that increases a business's value at exit starts years before the transaction. Clean books, owner compensation restructuring, and entity optimization done now produce real money at close.

You've had a cash flow crisis that felt like it came out of nowhere

Cash flow crises are almost always visible in advance with a rolling 13-week projection. 'Out of nowhere' means the projection didn't exist.

Your financial infrastructure hasn't kept pace with your headcount or revenue

A business with 12 employees and $3M in revenue running on the same financial system as when it had 2 employees and $600K in revenue has an infrastructure gap. It shows up in decisions, taxes, and lender conversations.

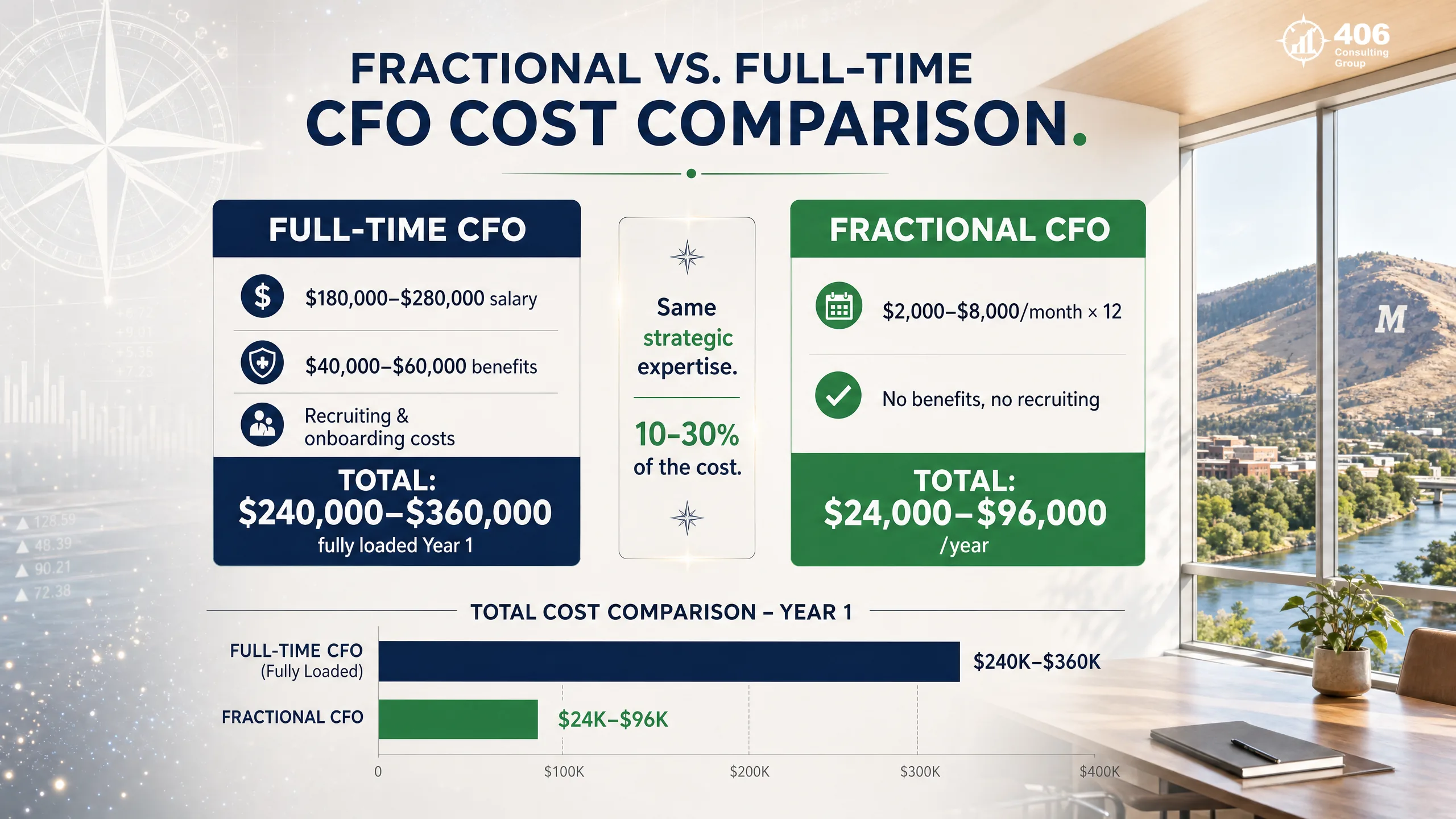

Fractional vs. Full-Time CFO: The Decision Framework

A full-time CFO makes sense for businesses above $20–$30M in revenue with sufficient complexity to justify a dedicated executive. Below that threshold, a fractional CFO delivers the same quality of strategic financial leadership at 10–30% of the cost — without the recruiting timeline, onboarding lag, or fixed overhead.

| Factor | Fractional CFO | Full-Time CFO |

|---|---|---|

| Annual cost | $24,000–$96,000 | $200,000–$350,000+ fully loaded |

| Time to start | 2–4 weeks | 3–6 months (recruiting + onboarding) |

| Expertise breadth | Cross-industry, cross-company pattern recognition | Deep expertise in one company |

| Flexibility | Scales up or down with business needs | Fixed overhead regardless of workload |

| Best for | $500K–$20M revenue businesses | $20M+ revenue with dedicated CFO scope |

| Commitment | No long-term contract required | Executive employment agreement |

| Infrastructure | Brings systems and processes from multiple engagements | Builds from scratch |

| Lender relationships | Active relationships across multiple transactions | Single-company network |

For more detail on fractional CFO pricing and ROI:

See our guide on what a fractional CFO actually costs and what you should get back — which covers the specific ROI calculations and engagement structures in detail.

Pricing & ROI: What a Fractional CFO Costs and What It Returns

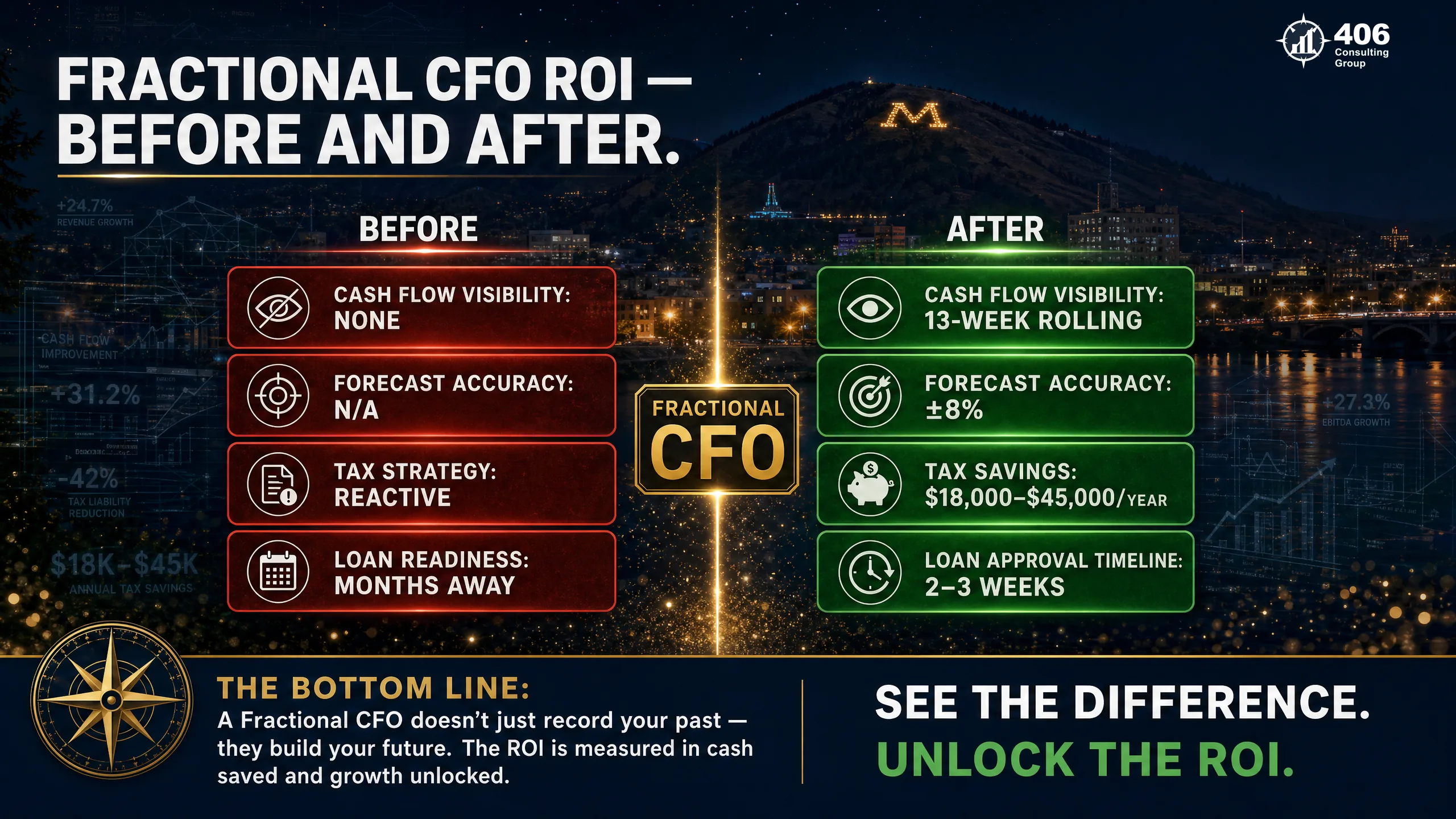

Fractional CFO services for Missoula businesses typically run $2,000–$8,000 per month depending on engagement scope, business complexity, and how many of the five CFO Operating System modules are active. The ROI framework is straightforward: add up what the engagement produces in tax savings, financing outcomes, margin recovery, and decision improvement — compare to monthly fee.

Foundation

$2,000–$3,500/moBusinesses $500K–$2M revenue

- Monthly management reporting package

- Rolling cash flow projection

- Quarterly tax coordination

- Monthly 60-minute owner review call

- Ad-hoc financial questions

Operating

$3,500–$6,000/moBusinesses $2M–$8M revenue

- Everything in Foundation

- Annual budget and scenario modeling

- Capital strategy and lender package prep

- KPI dashboard with industry benchmarks

- Quarterly board-level financial presentation

- Entity and compensation structure review

Growth

$6,000–$8,000+/moBusinesses $8M+ or pre-transaction

- Everything in Operating

- M&A due diligence support

- Exit readiness and valuation modeling

- Multi-entity financial infrastructure

- Investor and lender relationship management

- Weekly owner touchpoints during capital events

What 406 has delivered for clients — real outcomes:

An auto body group with five locations and multiple entities needed a $7M SBA loan. Their prior CPA's forecasts weren't bank-grade. Carrie rebuilt the books, delivered SBA-standard projections, and got the loan closed. The prior attempt had failed — not because the business wasn't creditworthy, but because the financial package didn't meet lender standards.

A trucking company was 45 days from running out of cash. Carrie stepped in, identified the cash flow gaps, restructured the reporting, and stabilized the business. It's still operating today. Steve, the owner, later said: 'What blew me away was how quickly Carrie understood our entire operation — top to bottom — in less than a month. I've never seen anyone do that.'

A multi-location business owner came in to sign their taxes. The S-Corp election paperwork was already prepared — they didn't ask for it. 'Jason had already filled out the paperwork and walked us through exactly how it would save us $13,000 this year. That's not something we've ever experienced from an accountant before.'

What to expect in the first 90 days:

Days 1–30: Foundation

- Financial review and gap identification

- Chart of accounts audit and restructure

- KPI identification specific to your business

- Baseline management reporting established

Days 31–60: System

- Forecast model built and calibrated

- Management reporting package live

- Capital needs assessment completed

- Tax strategy memo delivered

Days 61–90: Strategy

- First quarterly business review

- Growth plan draft

- Lender or bonding package (if needed)

- Year 1 tax optimization plan

Frequently Asked Questions

What is a fractional CFO?

A fractional CFO is a senior financial executive who provides CFO-level strategic financial leadership to a business on a part-time or retainer basis. They deliver the same functions as a full-time CFO — financial clarity, forecasting, capital strategy, tax optimization, and growth planning — at a fraction of the cost. For Missoula businesses between $500K and $20M in revenue, a fractional CFO is almost always the right answer to the question 'do I need more financial leadership?'

When does a Missoula business need a CFO?

The clearest signals: revenue has crossed $1M and financial complexity has outpaced your current system; you're applying for commercial financing and need forward-looking projections; you've had a cash flow surprise that felt unexpected; you don't know which parts of your business are profitable; or you're thinking about a sale, merger, or significant capital event in the next few years. If more than two of these apply, the CFO engagement will pay for itself.

How is 406 Consulting Group different from other fractional CFO firms?

Most fractional CFO firms layer strategy onto whatever financial infrastructure exists — and the advice underperforms because the foundation isn't there to support it. 406 builds the infrastructure first. Carrie's background includes 300+ commercial loans analyzed as an active contracted analyst for a Montana community bank, work that has held up through KPMG and Wipfli review environments, and a family background in business acquisition and turnaround. Jason identified $75M in unbilled inventory at BP, built the recovery system, and that system has been in use for 25+ years. The judgment that comes from operating at that scale is what we bring to every Missoula engagement — not a playbook from a business school case study.

Do I still need a bookkeeper if I have a fractional CFO?

Yes. The CFO and the bookkeeper serve different functions. Your bookkeeper maintains clean monthly books — the foundation the CFO works from. Your CFO interprets those books, produces forecasts, advises on strategy, and coordinates with your tax preparer. Without clean monthly books, CFO-level work is impaired. Without a CFO, clean books produce accurate history but not forward-looking strategy. The two roles are complementary, not substitutes.

How long before I see results from a fractional CFO engagement?

The foundation work — management reporting package live, forecast model built, tax strategy memo delivered — is typically complete within 60 days. The first decision improvement that pays for itself (a tax election, a financing outcome, a pricing decision made with actual margin data) often happens within the first quarter. The compounding value — better decisions made consistently, tax liability reduced year over year, capital accessed when needed — builds over the full engagement.

Can a fractional CFO help me sell my business?

Yes — and the earlier you engage, the more impact it has. The work that increases a business's value at exit (clean financials that survive due diligence, owner compensation restructured for maximum after-tax proceeds, key-person dependency reduced through documented systems, valuation modeling showing the specific actions that improve your multiple) takes time. A business that engages a CFO two years before a planned sale captures substantially more value than one that engages six months out.

How much does a fractional CFO cost in Missoula, MT?

Fractional CFO engagements for Missoula businesses typically run $2,000–$8,000 per month depending on scope, revenue complexity, and which modules of the CFO Operating System are active. For a detailed breakdown of what drives the range and how to calculate ROI, see our full guide on fractional CFO cost and ROI. The short version: for most Missoula businesses in the $1M–$10M revenue range, the engagement pays for itself in tax savings alone in the first year — before accounting for financing outcomes or margin improvements.

External Resources

Missoula, MT

CFO-Level Financial Leadership for Missoula Businesses

406 Consulting Group brings enterprise operational experience, 300+ commercial loans analyzed, and a track record of real outcomes to every Missoula CFO engagement. Infrastructure first. Strategy on top of it. Results that hold up under scrutiny.

The CFO Operating System

5 modules — sequential, interdependent

Financial Clarity

Management reporting that drives decisions

Forward Forecasting

Rolling cash flow + scenario modeling

Capital Strategy

Right capital at the right time

Tax Optimization

Year-round, from current book data

Growth Planning

Margin by service line + exit readiness

Why 406 Consulting Group

Commercial loans analyzed — Carrie brings the lender's perspective to every capital conversation

Unbilled inventory identified by Jason at BP — the analytical discipline that finds what others miss

Oldest system still in production — built by Jason, replicated by Accenture

Construction client growth over a multi-year CFO engagement

SBA loan closed after prior CPA's package was rejected by the bank

Related Resources