Succession Planning for a Family Business:

The Numbers Side

The financial side of family business succession — valuation, deal structure, tax strategy, and financing — is where most transfers succeed or fail. Here's how to get it right.

Succession planning for a family business fails most often not because of family dynamics — but because of the numbers. The valuation is wrong, the deal structure creates an unexpected tax bill, the financing falls apart at the bank, or the books were never clean enough to support a transaction. The financial side of a business transfer is the hardest part and the least understood — and most families start planning it far too late.

This guide covers the financial mechanics of family business succession: how to value the business, how to structure the transfer to minimize taxes, how to finance a buyout within the family, where estate planning intersects, and what the books need to look like before any of this can happen. It is the side of succession planning that accountants and CFOs handle — and the side that determines whether the transfer actually works.

Carrie Anderson co-founded 406 Consulting Group after years in commercial banking, where she reviewed and financed business acquisitions across Montana and the Pacific Northwest. The perspective here is from someone who has sat on both sides of the transaction table — and seen what makes business transfers work financially and what makes them collapse.

Table of Contents

Why the Numbers Side of Succession Gets Ignored Until It's Too Late

The short answer:Most family business owners plan the "who" — who takes over — long before they plan the "how much, structured how, taxed how, and financed how." The financial side of a business succession is a 3-to-5-year process done properly. Most owners start it 12 to 18 months before they want to exit. That gap costs them money — sometimes a lot of it.

3–5 years

Time needed to properly prepare a business for financial succession

12–18 months

Time the average family business owner actually starts financial planning before exit

30–40%

Estimated value increase possible with proper pre-sale financial preparation vs. unprepared transfer

The soft side is more visible and emotionally urgent

Family conversations about who runs the business, what role the founder plays after the transition, and how other family members are treated — these feel immediate and personal. The financial mechanics feel abstract until they become a problem. By then, options are limited.

Owners underestimate how long financial preparation takes

Getting 3 years of CPA-quality financial statements takes 3 years. Normalizing owner compensation, removing personal expenses, and building a track record of consistent EBITDA that a lender will underwrite — all of this takes time. Starting at month 18 means the books available for review are still messy at the moment of transfer.

The tax strategy window closes before owners realize it exists

Many of the most effective tax strategies for business succession — installment sale elections, entity restructuring, gifting programs, trust strategies — require planning years in advance to execute properly. A family that starts financial planning in year one of a three-year window has options. A family that starts six months before closing has almost none.

The Montana context: Family businesses in Montana — construction, agriculture, hospitality, trades — often have complicated ownership structures, real estate intertwined with business assets, and informal financial management practices built over decades. These are solvable, but not quickly. The businesses that transfer cleanly are the ones that started cleaning up the financial picture years before anyone signed anything.

What "The Numbers Side" Actually Covers

The financial side of family business succession spans six distinct disciplines — each handled by a different professional, each requiring lead time, and each capable of derailing the transfer if not addressed. Most families engage only one or two of these. A well-executed succession plan addresses all six.

Business Valuation

Business appraiser or CPA with valuation expertise

What the business is worth — using income, asset, and market approaches — and how that number differs depending on whether the transfer is a sale, a gift, an estate, or a combination.

Operational Financial Readiness

Controller or professional accountant

Getting the books clean enough to support a transaction: 3 years of CPA-quality statements, normalized earnings, personal expenses removed, consistent accounting method.

Deal Structure

Attorney + CPA + financial advisor

How the transfer is legally and financially executed: asset sale vs. stock sale, installment payments vs. lump sum, seller note terms, earnout provisions.

Tax Strategy

CPA + estate planning attorney

Minimizing what the government takes from the transfer: timing gains, choosing the right deal structure, gifting strategies, trust vehicles, entity elections.

Financing

Commercial banker + SBA lender

How the buyer — even a family member — actually pays for the business: seller financing, SBA 7(a) loans, bank financing, earnouts, hybrid structures.

Estate Planning Intersection

Estate planning attorney + CPA

Where business succession overlaps with personal wealth transfer: gift tax exclusions, lifetime exemptions, step-up in basis, trusts designed specifically for business interests.

Who coordinates all six? This is the gap most family business successions fall into. The attorney handles legal documents. The CPA handles tax returns. The banker handles the loan. But no one is sitting at the center — modeling scenarios, preparing the financial package, making sure the deal structure the attorney is drafting actually produces the tax outcome the CPA is expecting. A fractional CFO fills that role.

Business Valuation: What Your Business Is Actually Worth

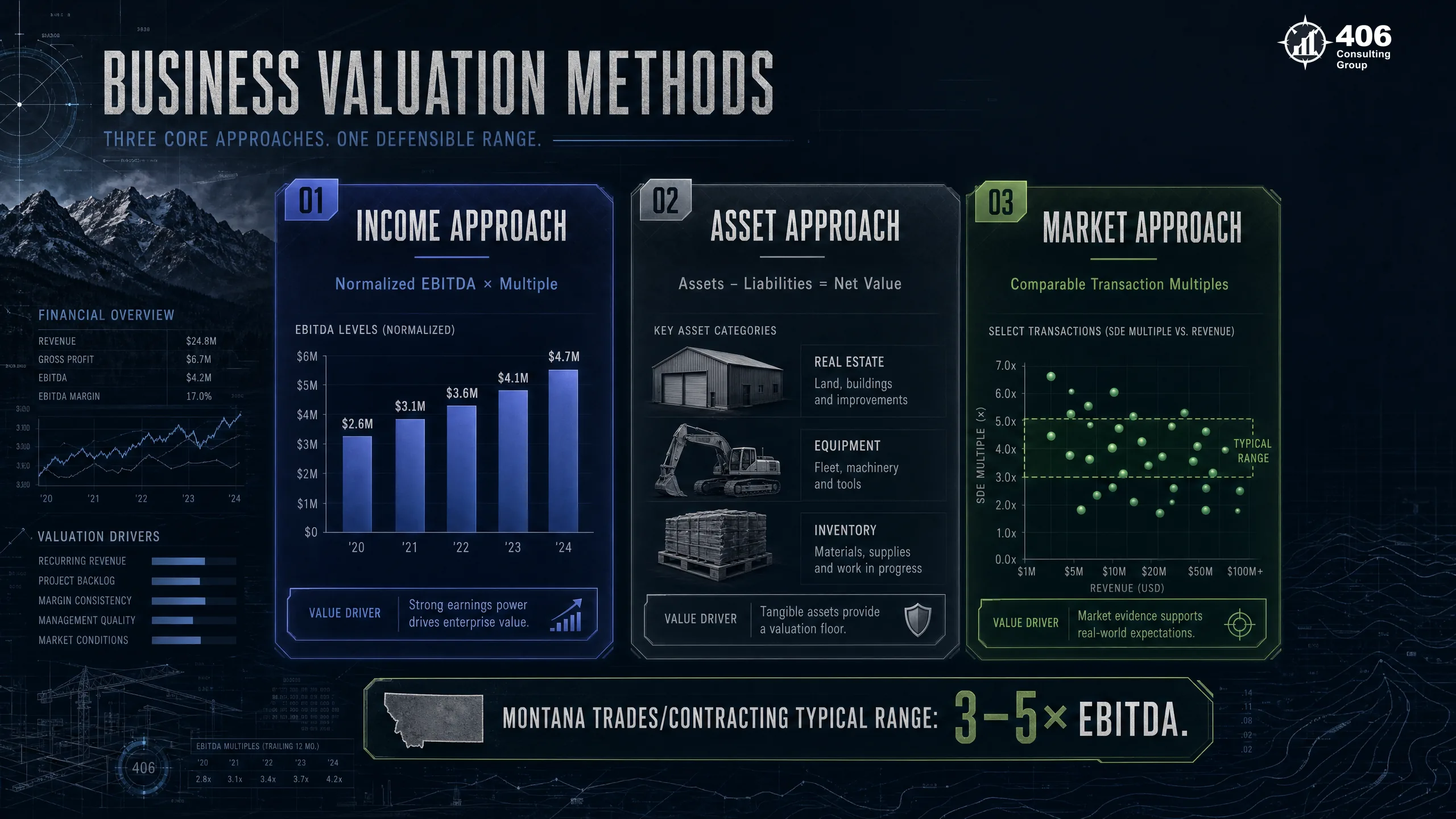

Business valuation is the financial foundation of any succession plan. Without a defensible, methodology-supported value, every other number in the succession plan — the purchase price, the installment payments, the gift tax implications, the estate tax exposure — is a guess. There are three primary approaches, and a credible valuation uses at least two of them.

Income Approach (Most Common for Operating Businesses)

Normalized EBITDA × Industry Multiple

The income approach values the business based on its earnings power. Normalized EBITDA — earnings before interest, taxes, depreciation, and amortization, adjusted to remove personal expenses and one-time items — is multiplied by an industry-specific multiple. A Montana construction business might trade at 3–5× EBITDA. A technology or professional services firm might trade at 6–10×. The multiple is driven by growth rate, customer concentration, owner dependence, and market conditions.

Watch out for

The owner's compensation adjustment is critical. A business owner paying themselves $80K when market compensation for their role is $180K has $100K in understated expenses. Normalizing this reduces EBITDA — and value — significantly. Do this before the buyer does.

Asset Approach (Common for Asset-Heavy or Distressed Businesses)

Fair Market Value of Assets − Liabilities

The asset approach values the business based on the net fair market value of its assets — equipment, real estate, inventory, receivables — minus liabilities. It is most relevant for businesses with significant hard assets and limited earnings power: construction equipment dealers, agricultural operations, real estate businesses. For most operating businesses, this approach produces a floor value rather than a market value.

Watch out for

Real estate owned by the business is often separated from the operating business in a transfer — the operating company is sold separately, and the real estate is leased back to the buyer. This structure has significant tax and financing implications that need to be modeled in advance.

Market Approach (Benchmarks Against Comparable Sales)

Revenue or EBITDA Multiple from Comparable Transactions

The market approach values the business by comparing it to similar businesses that have recently sold. Databases of private company transactions — BizBuySell, Pratt's Stats, DealStats — provide multiples by industry and revenue range. For a Montana family business, the relevant comps are often regional small business transactions in the same industry. The market approach provides a useful sanity check on the income approach.

Watch out for

Private company transaction data is limited and lagged. Market multiples from 2021–2022 (a peak period for business valuations) are not reliable guides for a 2025–2026 transfer. Use current data and apply a discount for illiquidity, customer concentration, and owner dependence.

Gift vs. sale valuations differ.If you are gifting a minority interest in the business to a family member — not selling it — the valuation for gift tax purposes may apply discounts for lack of control (20–40%) and lack of marketability (15–35%). These discounts are legitimate and IRS-recognized, but they require a qualified business appraiser to document. A "back of napkin" valuation for a taxable gift is an audit waiting to happen.

The Business Succession Financial Roadmap: 5 Stages to a Clean Transfer

The Business Succession Financial Roadmap organizes the financial side of succession into five sequential stages. Each stage has specific deliverables, a timeframe, and a warning sign that tells you when you are trying to move to the next stage before the current one is complete. Most failed transfers skip Stage 1 and Stage 2 and pay for it in Stage 3.

Stage 1: Foundation

Years 3–5 before transfer- 3 years of CPA-compiled or reviewed financial statements

- Personal expenses removed from business P&L

- Owner compensation normalized to market rate

- Consistent accounting method established

- All related-party transactions documented and disclosed

Warning sign: You are not ready for Stage 2 if a buyer or banker cannot review 3 years of clean, consistently prepared financial statements and immediately understand the business's earnings power.

Stage 2: Valuation

Years 2–3 before transfer- Formal business valuation using income and market approaches

- Normalized EBITDA calculated and documented

- Minority interest discounts analyzed if gifting is part of the plan

- Value drivers identified — what increases the multiple

- Value detractors identified — customer concentration, owner dependence

Warning sign: A valuation based on messy books produces a wrong number. Stage 2 can only be done well after Stage 1 is complete.

Stage 3: Structure

Year 1–2 before transfer- Deal structure selected: asset vs. stock sale, installment vs. lump sum

- Buy-sell agreement drafted and funded

- Entity structure reviewed and optimized for the transfer

- Tax strategy modeled under multiple deal structure scenarios

- Financing approach identified and pre-qualified

Warning sign: The deal structure cannot be optimized after the purchase agreement is signed. All tax strategy decisions must be made before the letter of intent.

Stage 4: Transfer

Transaction year- Purchase agreement executed with agreed financial terms

- Financing closed (bank loan, seller note, or both)

- Tax elections filed correctly and on time

- Ownership transferred per the agreed structure

- Earnout or consulting agreement established if applicable

Warning sign: Last-minute changes to deal structure in Stage 4 are expensive — legally and in lost tax strategy opportunities. Everything should be decided in Stage 3.

Stage 5: Optimization

Years 1–3 post-transfer- Seller's post-sale tax planning (installment reporting, investment strategy)

- Successor's financial systems built for ownership responsibility

- Seller consulting period managed and transitioned out cleanly

- Estate plan updated to reflect post-sale net worth

- Successor qualified for the next level of banking relationship independently

Warning sign: Stage 5 is frequently skipped. The seller exits and the successor is left without the financial infrastructure to run the business at the level the sale assumed.

Operational Financial Readiness: Getting the Books Ready for Transfer

A business cannot be accurately valued, financed, or transferred if the books are not clean. "Clean" in this context means something specific: three or more years of consistently prepared financial statements that a buyer, a banker, and an appraiser can review without finding material errors, unexplained adjustments, or personal expenses mixed into business costs. Most family businesses are not there. Getting there takes time.

Personal expenses in the business P&L

Remove all non-business expenses from the books — owner's personal vehicle, personal insurance, family member salaries above market rate, vacation disguised as business travel. Document the normalization adjustments clearly. A buyer will find these; it is better to present them proactively.

Impact: Affects EBITDA and therefore the valuation multiple applied to it

Owner compensation not at market rate

If the owner is paying themselves $90,000 when a professional manager doing the same job would cost $160,000, the books show artificially high EBITDA. Normalize by adjusting to market compensation. This reduces reported EBITDA — but it prevents the buyer from doing it first, less favorably.

Impact: Often the single largest normalization adjustment in a family business

Inconsistent accounting method

Cash basis vs. accrual basis switching between years, changing depreciation schedules, inconsistent revenue recognition — all of these make year-over-year comparisons unreliable. Standardize on accrual accounting (required by most lenders for loans above $500K) and maintain it consistently for 3+ years.

Impact: Lenders require accrual-basis statements; inconsistency creates audit risk

Related-party transactions not disclosed

Rent paid to an LLC owned by the owner's spouse, management fees to a holding company, loans between the business and family members — all must be disclosed, documented, and priced at arm's length. Undisclosed related-party transactions are a deal killer in due diligence.

Impact: Undisclosed related-party transactions can void a purchase agreement

Real estate mixed into the operating business

If the business owns the building it operates from, separate the entities before the transfer. Create a real estate LLC, transfer the property, and establish a lease between the operating business and the real estate entity. This structure gives the seller ongoing rental income and simplifies the business sale.

Impact: Simplifies valuation and gives seller ongoing cash flow post-transfer

Informal revenue and cash transactions

Any revenue not running through the business bank account and reported on financial statements cannot be included in the valuation or the loan application. Informal cash transactions — however common in the industry — must be run through the books for 2–3 years before the transfer for them to count.

Impact: Unreported revenue cannot support the purchase price or loan underwriting

Buy-Sell Agreements: The Financial Terms That Actually Matter

A buy-sell agreement is the legal contract that establishes how ownership of the business transfers under specific trigger events — death, disability, retirement, divorce, bankruptcy, or voluntary exit. Every family business with more than one owner needs one. Most family businesses either do not have one, or have one that was written 15 years ago and has not been updated since the business was worth a fraction of its current value.

Trigger Events

The specific circumstances that activate the buy-sell agreement. At minimum: death, permanent disability, voluntary retirement, and involuntary transfer (divorce, bankruptcy, creditor seizure). Each trigger should be defined precisely — "permanent disability" requires a medical definition. "Retirement" requires an age or years-of-service threshold. Ambiguous trigger language leads to litigation.

Critical point

Review trigger definitions every 3–5 years. A trigger defined in 2005 may not reflect current law or the actual circumstances of the business.

Valuation Mechanism

How the price is determined when a trigger event occurs. Three approaches: (1) Fixed price — set in the agreement and updated regularly; (2) Formula — agreed calculation, typically EBITDA × multiple; (3) Appraisal — independent appraisal at the time of the trigger event. Appraisal is the most accurate and most contentious. Formula is the most predictable. Fixed price is reliable only if it is updated annually.

Critical point

A buy-sell agreement with a fixed price that was set 10 years ago and never updated is worse than no agreement — it creates false expectations and a guaranteed dispute.

Funding Mechanism

How the buying party actually pays for the transferred interest. Common mechanisms: (1) Life insurance — company-owned or cross-owned policies fund death buyouts; (2) Installment payments — the business or the buying owners pay over time from operating cash flow; (3) Sinking fund — the business accumulates cash over time to fund a future buyout; (4) Bank financing — the buyer obtains a loan at the time of the trigger event.

Critical point

An unfunded buy-sell agreement is not a plan — it is a hope. If a 50% owner dies and the surviving owner cannot fund the buyout, the deceased's estate retains 50% ownership. The heir is now your business partner.

Cross-Purchase vs. Entity Redemption

Cross-purchase: the individual owners buy the departing owner's shares directly. Entity redemption: the business entity buys back the shares. The tax treatment is different. In a cross-purchase, the buying owners get a stepped-up basis in the acquired shares — reducing future capital gains when they eventually sell. Entity redemption does not provide this basis step-up. For C-Corps and S-Corps, the choice has material tax consequences.

Critical point

Consult a CPA before choosing the structure. The basis step-up in a cross-purchase agreement can be worth hundreds of thousands of dollars in a future sale.

Tax Strategy for Business Succession: Keeping More of What You Built

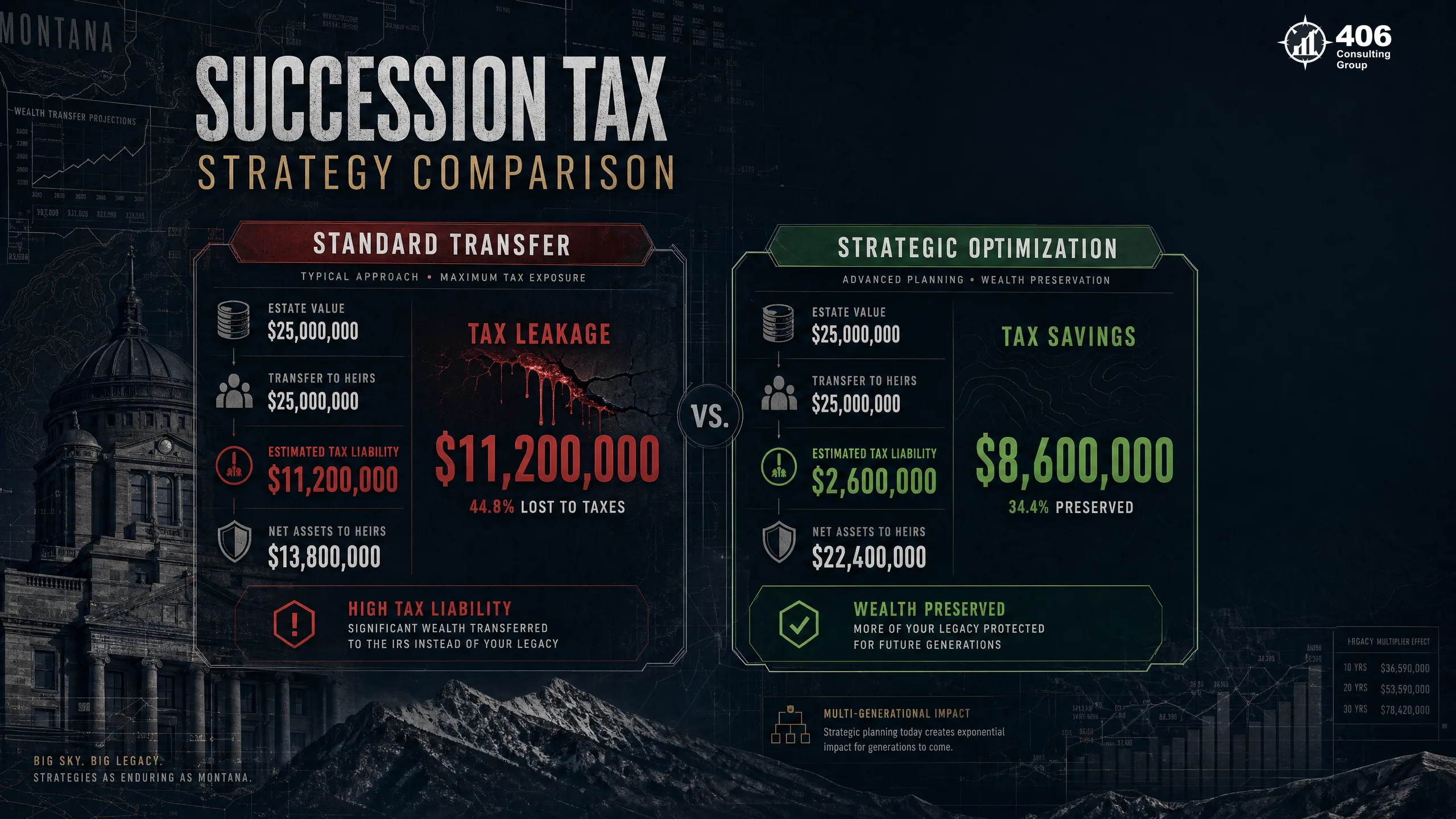

The tax implications of a business succession are substantial — and almost entirely dependent on decisions made before the transfer closes. A family business sold for $3M under the wrong structure can generate a tax bill $400,000–$600,000 higher than the same transaction structured correctly. Most of those planning opportunities close at the letter of intent, not at closing.

Asset Sale vs. Stock Sale

Seller benefit

Stock sale — gains taxed at lower long-term capital gains rates

Buyer benefit

Asset sale — buyer gets stepped-up basis in assets, reducing future depreciation and gain

This is the most fundamental tax decision in a business transfer. In an asset sale, individual assets are sold and gains are allocated across asset classes — some ordinary income, some capital gain. In a stock sale, the seller sells ownership interest and typically qualifies for long-term capital gains rates on the full gain. Buyers strongly prefer asset sales; sellers strongly prefer stock sales. The allocation of this tax burden is a negotiation, and who wins depends on the relative leverage of the parties.

Installment Sale (Section 453)

Seller benefit

Spreads gain recognition over the payment period — reduces the tax hit in year one

Buyer benefit

Aligns payments with the cash flow the business generates

An installment sale allows the seller to report gain proportionally as payments are received, rather than recognizing all gain in the year of sale. For a family business transfer where the buyer (a family member) is paying from business cash flow over 5–10 years, this is often the most practical structure — and it defers the seller's tax liability across the payment period. Interest on the seller note is ordinary income. Principal payments allocate between basis recovery and taxable gain.

Gifting Program (Annual Exclusion + Lifetime Exemption)

Seller benefit

Transfers ownership to family members before a sale — reduces the estate subject to tax

Buyer benefit

Receives ownership interest at no cost or reduced cost

The annual gift tax exclusion ($19,000 per recipient in 2025–2026) and the lifetime gift and estate tax exemption ($15M per individual — permanent under the One Big Beautiful Bill Act signed July 2025) allow business owners to transfer significant ownership interests to family members without gift or estate tax. Minority interest discounts (lack of control, lack of marketability) can reduce the taxable value of gifted interests by 30–50%, allowing more ownership to transfer within the annual exclusion.

Step-Up in Basis at Death

Seller benefit

The most tax-efficient transfer — heirs receive assets at fair market value as of date of death

Buyer benefit

No capital gains tax on appreciation during the deceased's lifetime

If a business owner dies holding appreciated business interests, the heirs receive a stepped-up basis equal to fair market value at the date of death. All the capital gains accumulated during the owner's lifetime are eliminated. For a business worth $4M with a $200K basis, the step-up eliminates roughly $3.8M in capital gain — which at 20% capital gains rate is $760K in avoided tax. Planning for this eventuality — while also planning for a lifetime transfer — is the core of estate planning for business owners.

Grantor Retained Annuity Trust (GRAT)

Seller benefit

Transfers business appreciation to heirs with minimal or zero gift tax

Buyer benefit

Receives growing business interest outside the estate

A GRAT allows a business owner to transfer appreciation in the business to heirs at low gift tax cost. The owner transfers business interests to the trust, receives annuity payments for a fixed term, and at the end of the term, whatever appreciation in excess of the IRS hurdle rate passes to heirs gift-tax-free. For a rapidly appreciating business, this can transfer substantial value. The risk: the grantor must survive the trust term for the strategy to work as intended.

Estate tax update (July 2025): The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, made the $15M per person lifetime gift and estate tax exemption permanent — eliminating the previously scheduled 2026 sunset. The exemption is now $15M per individual ($30M per couple), indexed for inflation. The urgency of "act before the sunset" no longer applies. That said, estate planning for business owners still matters: removing appreciation from your estate over time, utilizing minority interest discounts on gifted interests, and building inter-generational equity through annual exclusion gifts ($19K per recipient in 2025–2026) remain powerful strategies regardless of exemption level. Consult a CPA and estate planning attorney about your specific situation. See our tax planning services for how we coordinate with your estate attorney.

Financing a Family Business Transfer: How the Buyer Actually Pays

One of the most common misconceptions in family business succession is that a family member taking over the business can simply be "given" ownership. In many cases, the transferring owner has a substantial net worth tied up in the business — and needs proceeds from the sale to fund retirement. The successor needs a realistic financing plan. Here are the four primary structures.

Seller Financing (Most Common in Family Transfers)

The selling owner holds a promissory note for part or all of the purchase price. The buyer makes payments from business cash flow over 5–10 years.

Advantages

No bank approval required

Interest rate negotiable between family members

Can be structured as an installment sale for tax deferral

Allows seller to remain financially connected to business performance

Watch out for

Seller bears risk if business underperforms

Payments are taxable income to seller as received

Requires business to generate sufficient cash flow to service the note

Can complicate family relationships if business struggles

SBA 7(a) Loan

The Small Business Administration guarantees up to 75% of a loan above $150,000 for business acquisition (85% for loans $150,000 and under). Maximum loan amount is $5M.

Advantages

Allows buyer to finance up to 90% of the purchase price with less equity

Longer terms (up to 10 years) than conventional loans

SBA experience requirement waived for family transfers in some cases

Can combine with seller note for full financing

Watch out for

Extensive documentation required: 3 years of business and personal tax returns, financial statements, business plan

Personal guarantee required from all owners with 20%+ stake

Seller may be required to subordinate their note to the SBA lender

Process takes 60–90 days minimum

Conventional Bank Financing

A commercial bank loan secured by business assets and the personal guarantee of the buyer. Typically 5–7 year term for business acquisition.

Advantages

Faster than SBA (30–45 days)

No SBA guarantee fee

More flexible on structure than SBA program

Watch out for

Requires stronger personal financials from buyer

Lower loan-to-value than SBA — typically 70–80% of purchase price

Requires business to show DSCR of 1.25× or better

Collateral requirements may include personal real estate

Earnout Structure

Part of the purchase price is contingent on future business performance — the seller receives additional payments if the business hits revenue or EBITDA targets post-transfer.

Advantages

Bridges valuation gap between buyer and seller

Aligns seller incentives with post-transfer success

Reduces buyer's upfront financing requirement

Can reflect the risk of customer or revenue concentration

Watch out for

Creates incentive conflicts if seller is no longer managing the business

Earnout metrics must be defined precisely — disputes are common

Earnout payments are taxable to seller as ordinary income or capital gain depending on structure

Accounting for earnout liability complicates the business's books

Most family business transfers use a combination: A portion financed through an SBA 7(a) or bank loan, a portion through a seller note, and occasionally a gifted equity component. The mix depends on the buyer's personal financials, the business's DSCR, and the seller's need for immediate vs. deferred proceeds. See what commercial lenders actually evaluate to understand what the bank will require.

The Estate Planning Intersection

For most family business owners, the business is their largest asset — often comprising 60–80% of their total net worth. That means business succession planning and estate planning are not separate conversations. They are the same conversation, approached from different angles. The decisions made in one directly affect the other.

| Tool | What It Does | Best For | Key Limitation |

|---|---|---|---|

| Annual Gift Tax Exclusion | Transfer up to $19K/year per recipient ($38K if married, gift-splitting) with no gift tax (2025–2026 amount) | Gradual minority interest transfers to successors starting early | Limited to $19K/year per recipient — small relative to most business values |

| Lifetime Gift/Estate Exemption | Shield up to $15M of lifetime gifts and estate from federal tax per person — permanent under OBBBA (July 2025) | Large business interest transfers and inter-generational estate planning | Indexed to inflation; business appreciation and real estate can still push estates above the threshold over time |

| Step-Up in Basis at Death | Heirs inherit business interest at fair market value — all lifetime appreciation avoids capital gains | When the owner does not need liquidity during lifetime and wants to maximize heir's tax position | Only applies at death; requires estate planning to address liquidity for estate tax if applicable |

| Grantor Retained Annuity Trust (GRAT) | Transfer appreciation above IRS hurdle rate to heirs with minimal gift tax cost | Rapidly appreciating businesses where the owner can survive the trust term | Owner must survive the trust term; works best in low-interest-rate environments |

| Intentionally Defective Grantor Trust (IDGT) | Owner sells business interest to trust in exchange for installment note; future appreciation outside estate | Large estates where the owner wants to freeze the value of the business in the estate | Complex — requires coordinated legal, tax, and financial planning |

| Family Limited Partnership (FLP) | Business interests held in a partnership; minority discounts applied for gifts of limited partner interests | Multi-generational business ownership transitions; families with multiple assets | IRS scrutiny high; must be structured with legitimate business purpose beyond tax savings |

What the Successor Needs Financially to Take Over

Succession planning focuses heavily on the seller — the valuation, the tax strategy, the estate plan. The successor's financial readiness is equally important and equally often ignored. A family member who cannot personally qualify for a bank loan, who has insufficient working capital to fund the transition period, or who has never managed a business's finances at this scale is a risk to the transaction and to the business.

Personal credit and financial statement readiness

Any bank or SBA lender will require the successor's personal financial statement and tax returns for 3 years. Personal credit above 680 is a baseline minimum for most SBA lenders. Personal net worth and liquidity requirements vary — typically the buyer must contribute 10–30% equity. A successor who has not been building personal financial strength alongside business experience will fail bank qualification.

Compensation structure during transition

How the successor is paid during the transition period — while both the seller and successor may be active in the business — has tax and operational implications. If the seller is receiving consulting payments from the business while the successor is drawing a salary, the combined compensation expense must be sustainable from operating cash flow. Model this before the transition begins.

Financial management capability

The successor must be able to manage the financial aspects of ownership that the previous owner handled — or must immediately engage a controller or CFO to handle them. Reading a P&L, understanding cash flow, managing bank relationships, handling payroll and tax compliance — these are skills the successor needs or needs to hire for. Many family businesses transfer successfully operationally and then fail because the successor was not prepared for financial management.

Contingency planning for transition period underperformance

The first 12–24 months after a business transfer are high-risk. Key customers may leave when the founder steps back. Key employees may follow the seller out. Revenue may dip before the successor establishes their own relationships. The financing structure must account for this possibility — particularly if the seller's note payment begins immediately. Build in a payment holiday provision or a grace period tied to performance milestones.

The Fractional CFO's Role in Family Business Succession

The attorney drafts the purchase agreement. The CPA handles the tax return. The banker processes the loan. The business broker (if used) finds buyers. But none of these professionals is responsible for the overall financial picture — for modeling the scenarios, coordinating the advisors, preparing the financial package, and making sure the deal structure the attorney is documenting produces the tax outcome the CPA is expecting. That is the fractional CFO's role.

Financial Package Preparation

The fractional CFO prepares the complete financial package: 3 years of normalized financial statements, EBITDA bridge, cash flow analysis, working capital assessment, and business narrative. This is the document that goes to the bank, the SBA lender, and the business appraiser. Its quality determines whether financing is approved and at what terms.

Scenario Modeling

Before the letter of intent is signed, the CFO models the financial outcomes under each deal structure scenario: asset vs. stock sale, different installment periods, different seller note interest rates, earnout provisions. The analysis shows which structure maximizes the seller's after-tax proceeds while remaining financeable for the buyer.

Advisor Coordination

The fractional CFO sits at the center of the advisory team — coordinating between the CPA on tax strategy, the attorney on deal documents, the banker on loan qualification, and the business appraiser on valuation. Without a coordinator, advisors work in silos and the deal often falls apart at the point where their work intersects.

Post-Transfer Financial Setup

After the transfer, the CFO helps the successor build financial management infrastructure: new banking relationships, updated financial reporting, management dashboards, and the operational systems the successor needs to run the business at the level assumed in the purchase price. This is Stage 5 of the Roadmap — and almost always skipped without CFO engagement.

When to engage a fractional CFO: Ideally 2–3 years before the intended transfer — early enough to clean up the books (Stage 1), build a defensible valuation (Stage 2), and begin the tax strategy work that requires lead time. Engaging at Stage 3 (deal structure) is still valuable. Engaging after the letter of intent is signed is expensive — the most important decisions are already made. See what a fractional CFO costs and what ROI to expect.

Case Study: Montana Family Contracting Business — 3-Generation Transfer

Anonymized — Montana

Commercial Contracting Business — Third-Generation Family Transfer

When We Were Engaged

- Business valued informally at $2.2M — no formal appraisal

- Books prepared by the owner on QuickBooks — inconsistent method, personal expenses mixed in

- No buy-sell agreement — founder wanted to transfer to grandson

- Founder (age 68) wanted to complete transfer within 18 months

- No tax strategy in place — asset sale assumed, gain fully taxable in year one

- Grandson had strong operational capability but no financing qualification or business financial management experience

Outcome at Transfer (26 months later)

- Formal valuation established at $2.8M — higher than informal estimate due to normalized EBITDA

- 18 months of restated financials — CPA-compiled, accrual basis, personal expenses removed

- Buy-sell agreement drafted and funded with cross-purchase life insurance

- Transfer structured as installment sale over 8 years — gain deferred across payment period

- Deal structure optimized from lump-sum asset sale (ordinary income treatment assumed) to stock sale with installment treatment — $380K in projected tax savings on founder's gain

- Grandson qualified for $800K SBA 7(a) loan; seller note for remaining $2M financed the balance

$380K

Projected tax savings vs. original asset sale structure

$2.8M

Defensible valuation vs. $2.2M informal estimate

8 yrs

Installment period — gain deferred, cash flow managed

The critical insight: The founder had informally valued the business at $2.2M because that is what he thought it was worth. The formal valuation — using normalized EBITDA (after removing $140K in personal expenses from the books) multiplied by an industry-appropriate multiple — came in at $2.8M. The founder was leaving $600K on the table by not cleaning up the books before valuing the business. Combined with the tax strategy optimization, the two-year preparation period recovered far more value than its cost.

Frequently Asked Questions: Family Business Succession Planning

What is the financial side of succession planning for a family business?

The financial side covers six areas: business valuation (what the business is worth), operational financial readiness (getting the books clean enough to support a transaction), deal structure (asset vs. stock sale, installment vs. lump sum), tax strategy (minimizing what the government takes), financing (how the successor pays for it), and estate planning (how the transfer intersects with personal wealth transfer). Most family businesses plan the operational succession — who runs what — without adequately addressing any of these six financial dimensions.

How do you value a family business for succession?

A defensible business valuation uses at least two of three approaches: the income approach (normalized EBITDA × industry multiple), the asset approach (fair market value of assets minus liabilities), and the market approach (comparable private company transactions). For most operating businesses, the income approach is primary. Normalized EBITDA — earnings adjusted to remove personal expenses and one-time items, with owner compensation adjusted to market rate — is the key input. The multiple applied to EBITDA depends on industry, growth rate, customer concentration, and owner dependence. For gift or estate purposes, minority interest discounts may apply, reducing the taxable value by 30–50%.

What is a buy-sell agreement and why does every family business need one?

A buy-sell agreement is a legal contract establishing how ownership transfers when specific events occur — death, disability, retirement, divorce, bankruptcy, or voluntary exit. It specifies the valuation mechanism (how the price is set), the funding mechanism (how the buyer pays), and the structure (cross-purchase vs. entity redemption). Every business with more than one owner needs one. Without it, an owner's death or departure can leave the surviving owners in business with the deceased's heirs — or create a forced liquidation. An unfunded buy-sell agreement — one without insurance or a sinking fund to cover the buyout — is almost as dangerous as no agreement.

What are the tax strategies for transferring a family business?

Key strategies include: (1) Installment sale (Section 453) — spread gain recognition across the payment period rather than recognizing all in year one; (2) Asset vs. stock sale structure — sellers prefer stock sales (lower capital gains rates), buyers prefer asset sales (stepped-up basis); (3) Annual gifting — the $19,000/year annual exclusion (2025–2026) allows gradual equity transfer with no gift tax; (4) Lifetime exemption utilization — the $15M per person permanent exemption (established by the OBBBA, July 2025) allows substantial business interest transfers without estate or gift tax; (5) Step-up in basis planning — ownership held until death eliminates all capital gains from the decedent's lifetime; (6) GRAT and trust strategies — transfer appreciation to heirs at low gift tax cost. Most of these strategies require 2–5 years of lead time to execute properly.

How can a family member finance a buyout of the business?

The four primary financing structures for a family business buyout are: seller financing (the selling owner holds a promissory note paid from business cash flow over 5–10 years — most common in family transfers), SBA 7(a) loans (up to $5M, guaranteed by the Small Business Administration, allows financing up to 90% of the purchase price), conventional bank financing (faster but requires stronger buyer financials and lower loan-to-value), and earnout structures (part of the price is contingent on future business performance). Most family transfers use a combination — typically a seller note plus an SBA or bank loan, with potentially a gifted equity component. The successor must personally qualify for any bank financing, which requires 3 years of personal tax returns, strong credit, and sufficient personal equity contribution.

When should a family business owner start succession planning financially?

The answer is almost always earlier than you think. The Business Succession Financial Roadmap has five stages: Foundation (clean books — 3–5 years before transfer), Valuation (2–3 years), Structure (1–2 years), Transfer (transaction year), and Optimization (post-transfer). Stage 1 alone — getting 3 years of CPA-quality, accrual-basis, normalized financial statements — takes 3 years to produce properly. Tax strategies like GRAT trusts or gifting programs require years to build meaningful equity transfers. A business owner who wants to exit in 3 years and has not started financially is already behind. Five years of preparation produces materially better financial outcomes than 18 months.

Does 406 Consulting Group help with family business succession planning?

Yes. 406 Consulting Group provides fractional CFO services, controller services, and financial preparation support for family business succession planning across Montana, Idaho, and the Intermountain West. We prepare businesses for transfer — cleaning up the books, building the valuation support, modeling the deal structure scenarios, and preparing the financial package for bank and SBA financing. Carrie Anderson's background in commercial banking provides direct insight into what lenders require for business acquisition financing. Contact us to discuss what financial preparation for your specific succession situation looks like.

External Resources

Montana & Intermountain West

Financial Preparation for Your Family Business Succession

406 Consulting Group helps family businesses across Montana and the Intermountain West prepare financially for succession — from cleaning up the books to modeling the deal structure to preparing the lender package. Start 3–5 years before your intended exit and your options are wide open.

Business Succession Financial Roadmap

Which stage is your business in?

Foundation

3–5 yrs out — clean books, normalize earnings

Valuation

2–3 yrs out — formal appraisal, value drivers

Structure

1–2 yrs out — deal terms, tax strategy, financing

Transfer

Transaction year — execute and close

Optimization

Post-transfer — seller tax plan, successor setup

Key Numbers to Know

Related Reading

Planning a family business transfer?

Talk to 406 Consulting Group about the financial preparation your succession needs. The earlier you start, the more options you have.

Schedule a Consultation