Bookkeeping for Trucking Companies:

What You Need to Know

Terry owns Highline Hauling in Billings — 4 trucks, $1.2M in freight revenue — and got a $1,200 IFTA penalty because his bookkeeper didn't do IFTA. This guide covers what makes carrier bookkeeping different: IFTA, Form 2290, per diem, factoring, cost per mile, and the chart of accounts general bookkeepers miss.

Terry owns Highline Hauling in Billings. Four trucks, three company drivers, running dry van freight on the I-90 and I-15 corridors. He does about $1.2 million in revenue a year, and he has a bookkeeper who keeps the accounts clean and the payroll running on time.

What Terry doesn't have: a clear picture of which lanes are actually making him money. His best lane — Billings to Seattle — looks profitable because the revenue is good. His Billings to Spokane lane looks fine on paper too. What neither number shows is that the Spokane lane, once you factor in fuel cost, the deadhead miles back, and the lower rate he's been accepting from that broker, is running at $2.58 per mile in cost against $2.60 in revenue. He's hauling freight for $80 per trip.

Terry also got a $1,200 penalty from the state of Idaho last year because his IFTA mileage records for Q3 didn't match his fuel receipts. His bookkeeper doesn't do IFTA — he didn't know that until the notice arrived. And one of his trucks is still operating on a 2290 that expired in August because nobody flagged the renewal.

Terry's real problem isn't bad bookkeeping — it's that bookkeeping for trucking companies is a different discipline, and his bookkeeper never learned it. Carrier accounting in Montana and across the West requires IFTA records, 2290 compliance, per diem programs, and cost-per-mile tracking that general-purpose bookkeeping doesn't cover. This guide covers what's different, what's required, and how to set up the financial function that gives you the numbers to actually run the business.

By Jason Anderson — Co-Founder, 406 Consulting Group. Background in large-scale operational finance at BP, where fuel cost tracking, fleet accounting, and compliance reporting were core functions at scale.

Quick Answer: What Makes Trucking Bookkeeping Different

- →IFTA: Quarterly fuel tax filing required for interstate carriers. Requires mileage-by-state records every trip.

- →Form 2290: Annual heavy vehicle use tax, due August 31. Proof of payment required to register vehicles in most states.

- →Per diem: $69/day for DOT-regulated drivers away from home. Must be tracked correctly or it becomes taxable wages.

- →Cost per mile: The number that tells you whether a lane or load is actually profitable — not available from standard bookkeeping.

- →Factoring: Selling invoices at 2–4% discount for immediate cash. Recorded differently than standard revenue — most bookkeepers get this wrong.

Table of Contents

Why Trucking Bookkeeping Is Different from General Small Business Accounting

A general bookkeeper can handle a retail store, a restaurant, or a service business with standard QuickBooks knowledge. A trucking operation — even a small one — has seven things a standard setup doesn't cover. Miss any of them and you're either out of compliance, paying more tax than you owe, or running lanes blind.

IFTA filing — quarterly, per state, per vehicle

Interstate carriers must file a fuel tax return every quarter, allocating fuel taxes across every state they operated in. This requires trip-level mileage records and fuel receipts organized by state. A general bookkeeper who doesn't know IFTA exists won't be maintaining the records you need to file it.

Form 2290 (Heavy Vehicle Use Tax)

Every vehicle over 55,000 lbs used on public highways owes annual federal excise tax. It's due August 31. Most new carriers find out about it when they try to renew their plates and the DMV asks for the stamped Schedule 1 as proof of payment.

Revenue tracking by load, not by period

A trucking company's revenue is generated load by load, lane by lane. Standard revenue reporting tells you what came in this month. Carrier-level reporting tells you what you made on the Billings-to-Seattle lane versus the Billings-to-Spokane lane — which is the number you actually need to manage the business.

Fuel as a cost-of-revenue item, not overhead

In most businesses, fuel is a small overhead expense. In trucking, fuel is typically 20–25% of revenue — the single largest cost. It needs to be tracked by trip and by vehicle, not dumped into a generic 'fuel' expense account, to be usable for IFTA and cost-per-mile analysis.

Per diem for DOT-regulated drivers

Drivers away from home for work qualify for a $69/day per diem deduction. Paid correctly, it's tax-free to the driver and deductible to the carrier. Paid wrong — or not tracked at all — it either becomes taxable wages or disappears as a missed deduction.

Equipment depreciation cycles

A semi-truck costs $150,000–$200,000 and has a 5-year MACRS depreciation schedule. Bonus depreciation allows full expensing in year one. A 4-truck fleet's depreciation decisions can swing taxable income by $300,000+ depending on when trucks are purchased and what elections are made.

Factoring receivables

Many carriers factor their invoices — selling them to a third party at a 2–4% discount for immediate payment. This is not a revenue reduction. It's a financing cost. Booked wrong, it understates revenue and creates reconciliation problems every quarter.

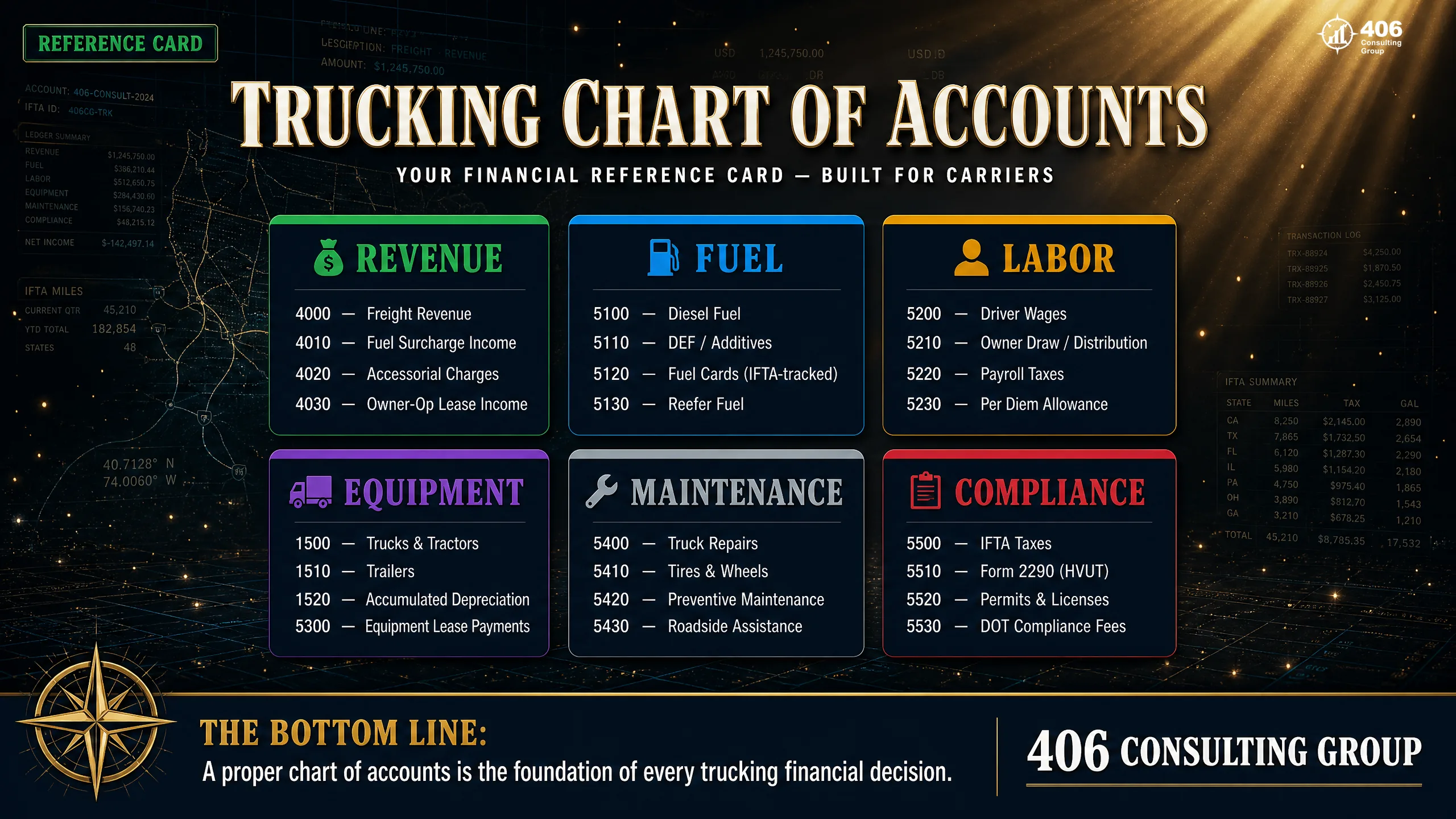

The Chart of Accounts a Trucking Company Actually Needs

The default QuickBooks chart of accounts is built for a generic small business. For a carrier, it's missing most of the accounts you need and lumps together costs that should be separated. Here is the structure Highline Hauling runs — four trucks, about $1.2M in freight revenue.

Revenue Accounts

Freight Revenue — Company Trucks

Primary load revenue from owner-operated equipment

Freight Revenue — Brokered Loads

Revenue from loads dispatched through brokers

Fuel Surcharge Revenue

Surcharges billed to customers — must match surcharge expense

Accessorial Charges

Detention, layover, lumper reimbursement, TONU fees

Operating Expenses — Fuel

Diesel Fuel — Truck 1

Per-vehicle fuel tracking for IFTA and cost-per-mile

Diesel Fuel — Truck 2/3/4

Separate accounts or classes per vehicle

DEF (Diesel Exhaust Fluid)

Often forgotten — required for modern emissions systems

Reefer Fuel

If applicable — separate from tractor fuel

Operating Expenses — Labor

Driver Wages

W-2 wages; separate from owner's draw

Driver Per Diem

Tax-free per diem paid to drivers — $69/day DOT rate

Owner Compensation

Separate line — critical for S-Corp payroll tracking

Payroll Taxes — Employer Share

Separate from gross wages for true labor cost

Operating Expenses — Equipment

Equipment Loan Payments — Principal

Balance sheet only — not an expense

Equipment Loan — Interest

This is the expense; principal reduces the liability

Depreciation — Trucks

MACRS or bonus depreciation; separate from trailers

Depreciation — Trailers

Different depreciation life than tractors

Operating Expenses — Maintenance

Preventive Maintenance

Oil changes, filters, scheduled service — by vehicle

Repairs — Mechanical

Unscheduled repairs; track by vehicle for fleet analysis

Tires

High-cost item; track separately for cost-per-mile

Parts and Supplies

Driver supplies, straps, load bars, tarps

Compliance and Permits

IFTA Taxes Paid

Net payment to states after credits — quarterly

Form 2290 (HVUT)

Annual federal excise tax — $100–$550 per vehicle

UCR Registration

Unified Carrier Registration — annual, by fleet size

Operating Authority / Permits

MC number fees, state permits, oversize/overweight

Highline Hauling — Why Classes Matter as Much as Accounts

Terry uses QuickBooks with a class for each truck (Truck 1 through Truck 4) and a class for each lane (Billings-Seattle, Billings-Spokane, Billings-Denver). Every expense is coded to both the account and the class. This means at the end of the month he can run a profit and loss by class — and see exactly what Truck 3 cost to operate and what the Billings-Spokane lane returned. Without classes, he'd have accounts but no visibility into the performance that matters.

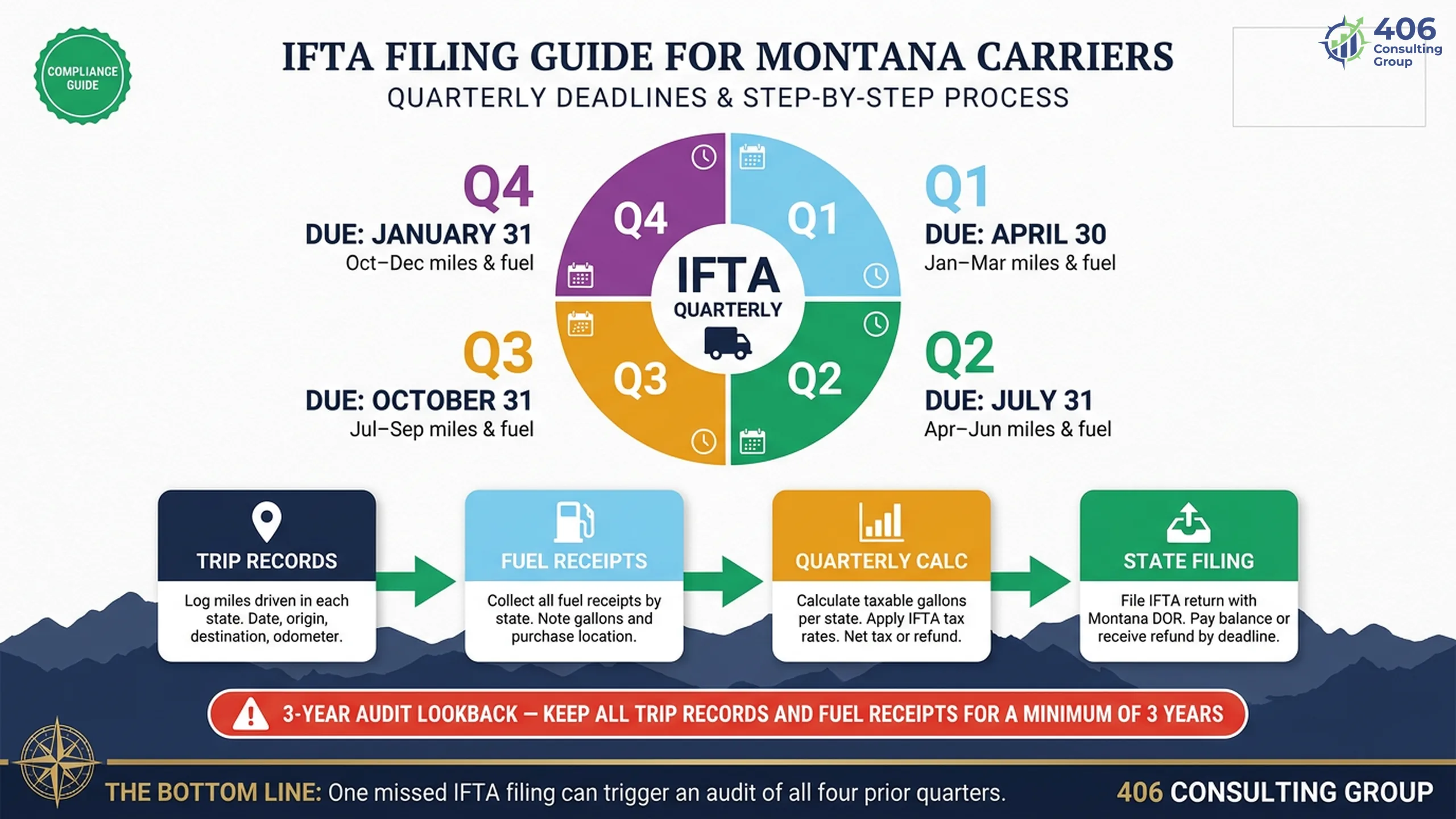

IFTA — What It Is and What Happens If You Miss It

IFTA stands for the International Fuel Tax Agreement. It exists because carriers cross state lines constantly, buying fuel in some states and consuming it in others. Without IFTA, every state would require separate fuel tax accounts and filings. IFTA consolidates all of that into one quarterly return filed in your base state — which then settles with the other states on your behalf.

If your truck has three or more axles, or has a gross vehicle weight over 26,000 lbs, and you operate in two or more IFTA jurisdictions, you are required to be registered for IFTA. For Highline Hauling, every truck qualifies. For a single owner-operator running across state lines, every load qualifies.

What IFTA Actually Requires

Trip records for every trip

Date, origin, destination, route, total miles, miles by state. Every trip. Without exception. These are the records an IFTA audit examines first.

Fuel receipts for every fill-up

Date, location, gallons purchased, vehicle. The receipt must show the state where fuel was purchased. Credit card statements are acceptable if they show the purchase location.

Quarterly reconciliation

Miles driven in each state ÷ fleet MPG = fuel consumed in each state. Fuel purchased in each state. The difference is either a tax owed (you consumed more than you bought in a state) or a refund (you bought more than you consumed).

Quarterly filing deadlines

Q1 (January–March): due April 30. Q2 (April–June): due July 31. Q3 (July–September): due October 31. Q4 (October–December): due January 31. Montana is an IFTA member — file with Montana DOT.

Penalties — And Why Idaho Sent Terry a $1,200 Notice

The standard IFTA penalty for late filing or non-filing is the greater of $50 or 10% of the net tax due. For an underpayment or a records failure, the penalty applies per jurisdiction — meaning if an auditor finds your mileage records don't support your Q3 filing across four states, you can face four separate assessments.

Terry's Q3 problem: his bookkeeper logged fuel receipts but didn't maintain the trip-level mileage-by-state records. When Idaho audited the Q3 filing, the mileage numbers couldn't be substantiated. Result: Idaho assessed estimated miles (higher than actual), calculated a tax due, and added a 10% penalty plus interest. Total: $1,200 — and that was one state, one quarter.

IFTA audits have a three-year lookback. An auditor can examine every quarter for the past three years. Clean trip records from day one are not optional — they are the only protection you have in an IFTA audit.

| IFTA Record | Required? | Acceptable Format |

|---|---|---|

| Trip report (miles by state) | Yes — every trip | Driver log, ELD data, GPS report, or paper trip sheet |

| Fuel receipts | Yes — every purchase | Receipt showing state, date, gallons, vehicle; credit card statement with location |

| Beginning/ending odometer | Yes — each quarter | Logged in dispatch system or driver log |

| Fleet MPG documentation | Yes — for calculation | Quarterly MPG derived from fuel purchases and miles driven |

| Repair records affecting mileage | Recommended | Service records if vehicle was out of service for extended period |

Form 2290 — The Heavy Vehicle Use Tax Most New Carriers Miss

Form 2290 is the federal Heavy Vehicle Use Tax (HVUT). Any vehicle with a gross vehicle weight of 55,000 lbs or more that is used on public highways owes this tax annually. The filing period runs July 1 through June 30. For vehicles in use during July, the return and payment are due by August 31.

This is not an obscure filing. It's a federal excise tax that's been on the books for decades. Most experienced carriers know it cold. Most new carriers find out about it the wrong way — when they try to renew their vehicle registration and the DMV requires a stamped Schedule 1 (the IRS-stamped proof of 2290 payment) before they'll issue plates.

2290 Tax Rates (2024–2025)

Key Deadlines and Rules

Annual filing period

July 1 – June 30 (federal highway use year)

Due date for July vehicles

August 31 — file and pay for any vehicle used in July

New vehicles mid-year

Due by the last day of the month following first use

Proof required for plates

Stamped Schedule 1 from IRS — digital filing generates this within minutes

Penalty for non-filing

4.5% of total tax per month, plus 0.5% for late payment, up to 25% max

VIN correction

Free VIN correction allowed once — typos on original return require amendment

Highline Hauling — Truck 3's Expired 2290

Terry's Truck 3 was due for 2290 renewal on August 31. Nobody had it in their calendar. The truck kept running. In November, a DOT inspection in Idaho flagged the expired cab card — the Schedule 1 stamped by the IRS, which functions as proof of 2290 payment. The officer issued a citation and placed the truck out of service until Terry could produce a valid Schedule 1. Terry filed electronically that afternoon, got his stamped Schedule 1 within the hour, and the truck was back on the road by evening — but the citation, the lost day, and the scramble cost more than the $550 tax would have.

Per Diem for Truck Drivers: Rules, Rates, and Tracking

The per diem deduction for truck drivers is one of the most valuable — and most frequently mishandled — items in carrier accounting. When done correctly, it reduces the driver's taxable income, lowers payroll taxes, and is fully deductible to the carrier. When done wrong, it creates IRS exposure for both the carrier and the driver.

The DOT Per Diem Rate

Standard per diem rate (2024)

$69/day

Deductible percentage (owner-operators)

80% of $69 = $55.20/day

Days away from home required

Overnight, away from tax home

For company drivers: the carrier can pay up to $69/day as a non-taxable reimbursement — it doesn't appear as wages on the W-2, isn't subject to payroll taxes, and is deductible to the carrier. Amounts above $69/day are taxable wages. For owner-operators on Schedule C: 80% of $69 ($55.20) per day away from home is deductible.

Highline Hauling — The Per Diem Math for 3 Company Drivers

Each of Terry's three company drivers is on the road approximately 200 nights per year. At $69/day, that's $13,800 per driver in non-taxable per diem — paid separately from wages and not subject to federal or state payroll taxes.

Without per diem program

Driver compensation: $70,000/year (wages only)

Payroll taxes on $70,000: ~$5,355 (employer share)

Driver's income tax: on full $70,000

With per diem program

Wages: $56,200 | Per diem: $13,800

Payroll taxes on $56,200: ~$4,299 (employer share)

Savings per driver: ~$1,056/year in payroll taxes

Across 3 drivers: ~$3,168/year in payroll tax savings for Highline Hauling — plus the tax benefit to each driver.

What Makes a Per Diem Payment Taxable (and Causes IRS Problems)

- ✗Paying per diem without documenting that the driver was away from their tax home overnight

- ✗Paying the same per diem rate to local drivers who return home each night (it's fully taxable for them)

- ✗Paying per diem above $69/day without adding the excess to W-2 wages

- ✗No records of which days the driver was on the road — the IRS requires substantiation

- ✗Including per diem in the driver's hourly or mileage rate without separating it on payroll

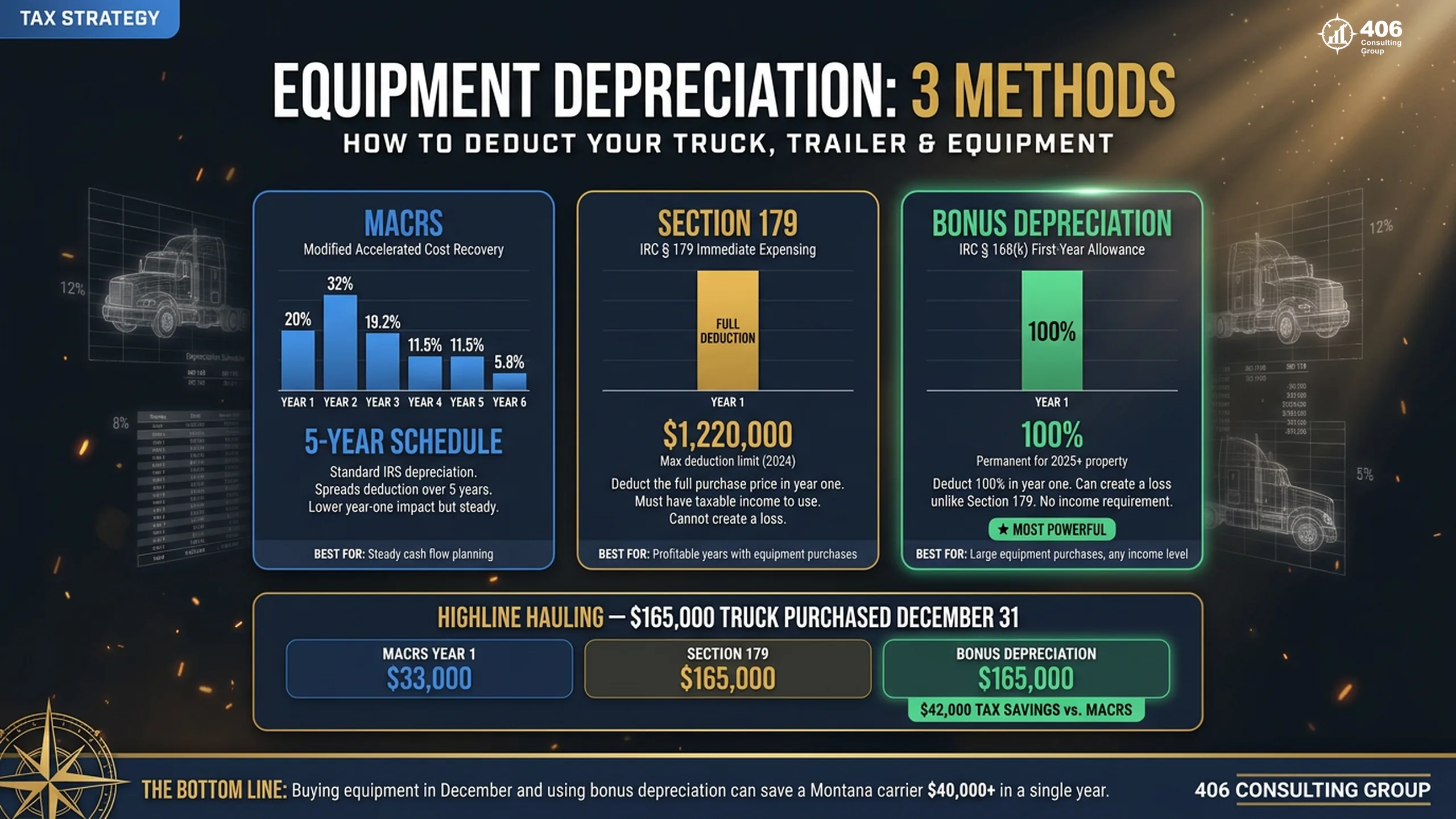

Equipment Depreciation: Section 179, Bonus Depreciation, and the Timing Game

Equipment is the largest capital investment in a trucking operation. A single semi-truck costs $150,000–$200,000. A trailer runs $50,000–$80,000. How and when you depreciate that equipment determines your taxable income — and for a carrier with multiple trucks, the decision swings five and six figures.

MACRS (standard depreciation)

How it works: Semi-trucks depreciate over 5 years using the Modified Accelerated Cost Recovery System. Year 1: 20%, Year 2: 32%, Year 3: 19.2%, Year 4: 11.52%, Years 5–6: remaining balance. On a $160,000 truck, Year 1 depreciation is $32,000.

Best for: Spreading deductions over time when income is expected to grow — higher future rates make the later deductions more valuable.

Section 179 expensing

How it works: Elect to deduct the full cost of qualifying equipment in the year placed in service, up to $1,220,000 (2024 limit). The deduction is limited to your business taxable income — you can't create a loss with Section 179 alone.

Best for: High-income years where you want to reduce taxable income immediately. A $160,000 truck deducted in full in year one saves you from carrying the depreciation over five years.

Bonus depreciation (100%, now permanent)

How it works: For property placed in service after January 19, 2025, 100% bonus depreciation is permanent. Unlike Section 179, bonus depreciation can create a loss. A carrier with $120,000 of net income before depreciation who buys a $160,000 truck in December can show a $40,000 loss — which offsets other income.

Best for: Maximum immediate tax reduction in high-revenue years. The timing of the placed-in-service date is critical — December 31 vs. January 2 is a full year of deduction difference.

Highline Hauling — Terry's Truck 4 Decision

Terry is planning to add a fourth truck in Q4 at $165,000. His net income before the purchase is tracking to $190,000. With 100% bonus depreciation, buying Truck 4 before December 31 reduces his taxable income to $25,000 — saving roughly $42,000 in combined federal and Montana income tax. If he buys it on January 3 instead, that deduction moves to next year. The timing decision alone is worth $42,000.

This is the kind of conversation that happens in October with a tax advisor — not in April with a tax preparer. The decision is already made by the time the return is filed.

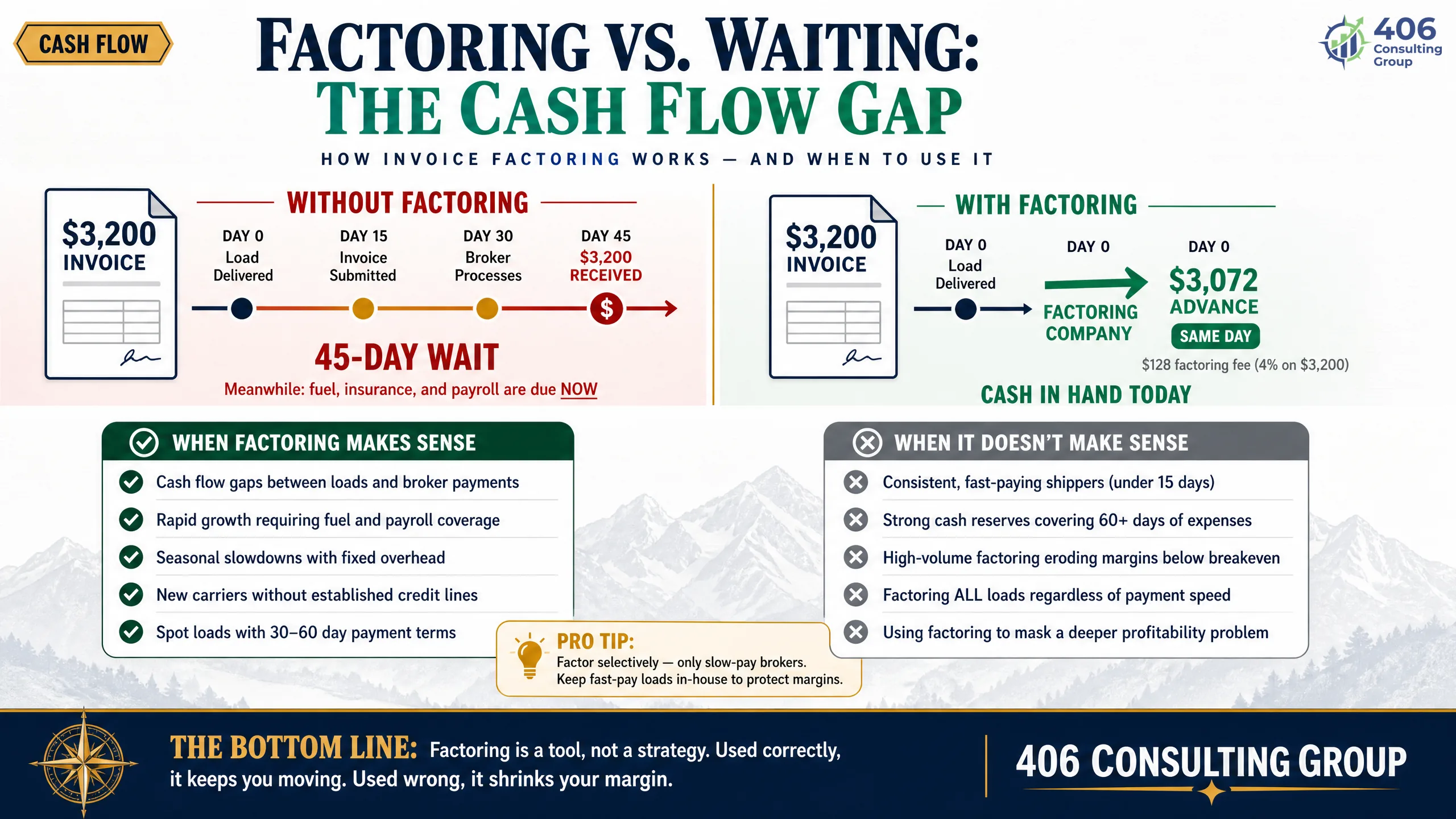

Factoring vs. Waiting: Cash Flow Management for Trucking Companies

The typical broker payment cycle is 30–45 days. Some brokers pay in 15 days. Some take 60. When you're paying drivers weekly, diesel every few days, and truck payments monthly, waiting 45 days to get paid for a load you delivered last week creates a structural cash flow problem — especially for carriers growing faster than their cash reserve.

How Factoring Works

You deliver a load. You have a $3,200 invoice from the broker, due in 45 days. Instead of waiting, you sell that invoice to a factoring company. The factor advances you 95–97% of the invoice immediately ($3,040–$3,104). When the broker pays the invoice in 45 days, the factor keeps the remaining 3–5% ($96–$160) as their fee.

Typical factoring fee

2%–4% of invoice

Advance rate

95%–98% same day

Recourse vs. non-recourse

Recourse = cheaper; non-recourse = factor absorbs bad debt

When factoring makes sense

- You're growing fast and cash can't keep up with payroll

- You have high-quality brokers but long payment terms

- Your credit line is maxed or you don't have one

- You're a newer carrier without established broker relationships

- The cost of factoring is less than the cost of turning down loads for lack of cash

When factoring doesn't make sense

- —You have a cash reserve that covers 60 days of operating costs

- —Your brokers pay in 15–20 days consistently

- —You're running direct shipper accounts with faster payment

- —The factoring fee (3%) on $1.2M revenue = $36,000/year — that's significant overhead

- —You can qualify for a revolving line of credit at lower effective cost

How Factoring Appears in the Books (and Where Bookkeepers Get It Wrong)

The factoring fee is a financing expense, not a reduction in revenue. When you factor a $3,200 invoice and receive $3,072 (96%), the correct accounting is: record the full $3,200 as revenue, record the $128 fee as a financing cost (account: Factoring Fees or Financing Charges). Do not record $3,072 as revenue — this understates revenue, distorts your cost-per-mile calculation, and creates problems when your gross revenue doesn't match the 1099s your brokers issue.

Highline Hauling factors about $400,000 in invoices per year at 3.2% — roughly $12,800 in annual factoring fees. Booked correctly, Terry sees $1.2M in revenue and $12,800 in financing costs. Booked wrong, he sees $1,187,200 in revenue and wonders why his per-mile numbers don't add up.

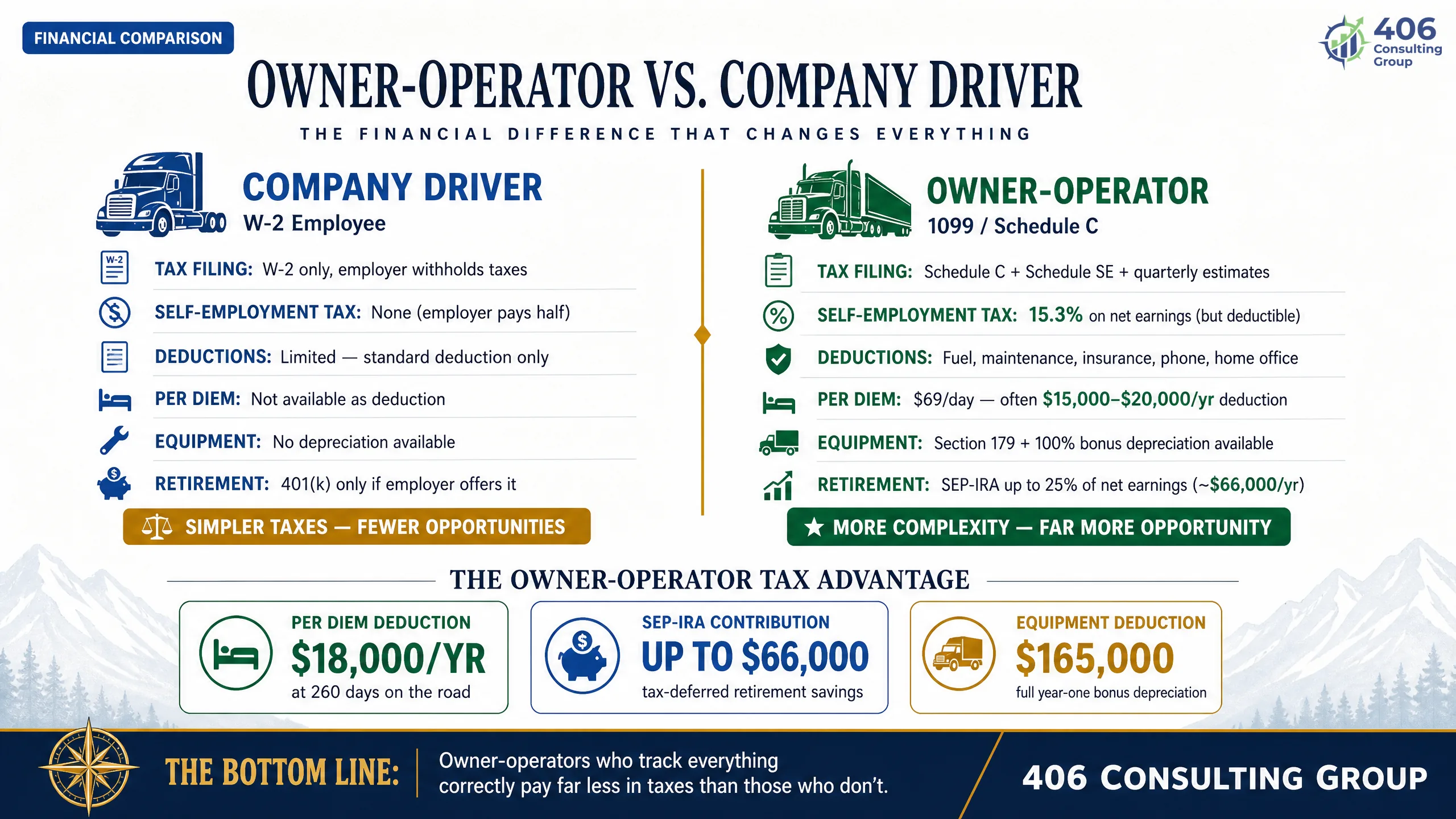

Owner-Operator vs. Company Driver: How Owner-Operator Bookkeeping Changes Everything

The owner-operator vs. company driver distinction is one of the most consequential decisions in carrier accounting. It affects payroll, IFTA responsibility, equipment ownership, insurance, and tax structure — and getting it wrong creates IRS exposure under worker misclassification rules.

| Factor | Company Driver (W-2) | Owner-Operator (1099) |

|---|---|---|

| Payroll taxes | Carrier pays 7.65% employer share; withholds employee share | Driver pays full 15.3% SE tax (offset by deductions) |

| Equipment | Carrier owns and depreciates the truck; driver has no ownership | Driver owns or leases their truck; depreciates on their return |

| Fuel | Carrier pays fuel; deducts and tracks for IFTA | Driver pays fuel; deducts and files their own IFTA (if applicable) |

| IFTA responsibility | Carrier files IFTA for company trucks | Owner-operator may have their own IFTA account under their own authority |

| Insurance | Carrier provides liability; driver may need occupational accident | Driver carries their own commercial truck insurance — typically higher |

| Per diem | Carrier can pay $69/day non-taxable; deductible to carrier | Driver deducts 80% of $69/day on their own Schedule C |

| 1099 vs. W-2 | W-2 at year end — payroll records throughout the year | 1099-NEC by January 31 — if paid $600+ in the year |

| Lease-on agreements | N/A | Leasing onto carrier authority — carrier may supply fuel, dispatch; driver uses their equipment |

Worker Misclassification — The IRS and DOL Test

Paying a driver as a 1099 contractor when they meet the legal definition of an employee is one of the most expensive mistakes a carrier can make. The IRS uses a multi-factor test: Does the carrier control when, where, and how the driver works? Does the carrier provide the equipment? Is this the driver's primary income source? If the answers are yes, the IRS may reclassify the relationship — and the carrier owes back payroll taxes, penalties, and interest for every year of the misclassification. Genuine owner-operators who own their own equipment, set their own schedules, and operate under their own authority are properly classified as contractors. Drivers who use your truck, run your loads, and follow your dispatch are employees — regardless of what the contract says.

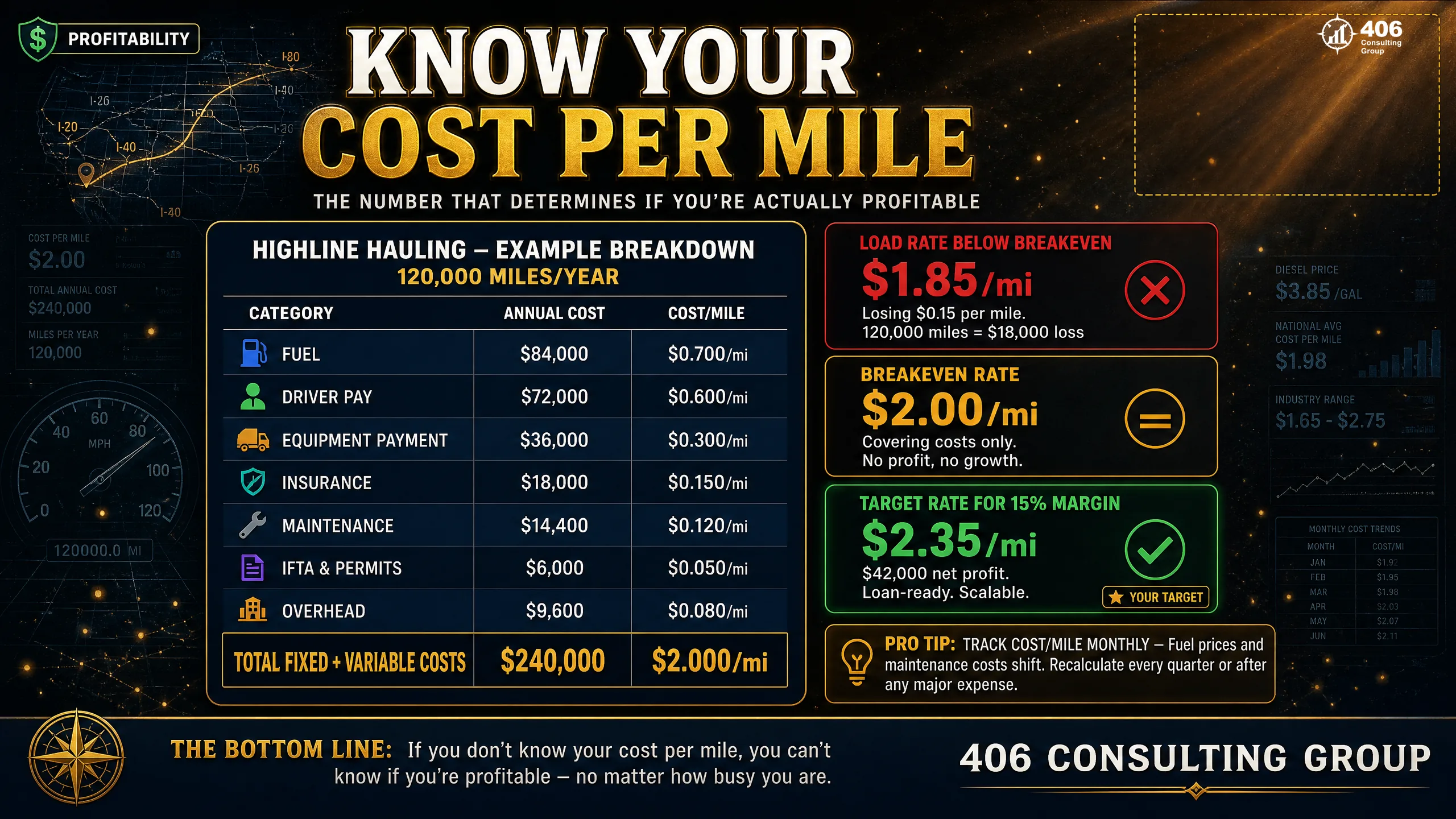

Cost Per Mile: The Number That Tells You If You're Actually Making Money

Cost per mile is the most important operational metric in trucking. It tells you what it costs you to move a truck one mile — and when compared against your revenue per mile on any given lane, it tells you whether you're making money or losing it. A carrier without cost-per-mile visibility is pricing loads by gut feel and finding out the result in April.

Highline Hauling — Cost Per Mile Breakdown (4 Trucks, ~400,000 Miles/Year)

Variable Costs (per mile)

Fixed Costs (per mile)

Total cost per mile

$2.02

Revenue per mile (avg)

$3.00

Net per mile

$0.98

Why the fleet average hides the real story:

Billings → Seattle

Billings → Denver

Billings → Spokane (w/ deadhead)

The Billings-to-Spokane lane looks fine — it's technically profitable. But at $0.13/mile net on loads that average 350 miles, Terry is making $45.50 per trip before accounting for the deadhead miles back. Once deadhead is factored in, he's often running that lane for less than $20 in net contribution. The Seattle lane makes $483 per trip. Terry can't see this without cost-per-mile tracking by lane — which requires the bookkeeping structure to support it.

Frequently Asked Questions: Trucking Company Bookkeeping

What triggers an IFTA audit?

Common IFTA audit triggers include: significant discrepancies between reported miles and GPS or ELD data, fuel purchases that don't align with reported miles (implying unreported miles or mileage inflation), consistently reporting unusually high or low MPG for your equipment class, and failing to file on time more than once. States share IFTA data with each other and with the IRS. Montana participates in coordinated audit programs with other IFTA member jurisdictions. The best protection is trip-level records — not reconstructed estimates — maintained in real time.

What is UCR registration and is it separate from IFTA?

The Unified Carrier Registration (UCR) is a separate annual registration requirement for interstate motor carriers, freight brokers, and leasing companies. It is not the same as IFTA. UCR fees are based on fleet size: 1–2 vehicles ($76), 3–5 ($228), 6–20 ($380), 21–100 ($1,000+). Registration opens October 1 each year for the following calendar year. Operating without UCR registration is a federal violation — DOT officers check it during roadside inspections. It's a small fee that carriers miss because it's not tied to any other filing they already do.

What bookkeeping software works best for trucking companies?

QuickBooks Online or Desktop handles trucking bookkeeping well when set up correctly — specifically with vehicle classes, lane classes, and the right chart of accounts. Some carriers use trucking-specific software like TruckingOffice, Axon, or Rose Rocket for dispatch and load management, then integrate or import into QuickBooks for accounting. The software matters less than the setup — a generic QuickBooks with a generic chart of accounts won't give you the cost-per-mile or lane-level visibility you need regardless of what platform you're on.

Should a trucking company make the S-Corp election?

For an owner-operator running under their own authority with net profit consistently above $60,000–$80,000, the S-Corp election math usually works. Self-employment tax is 15.3% on all net profit for a sole proprietor. With an S-Corp, you pay yourself a reasonable salary (subject to payroll taxes) and take the remainder as a distribution (not subject to SE tax). For an owner-operator netting $120,000, the savings can be $6,000–$10,000 per year. The election requires running payroll, filing a separate S-Corp return, and maintaining proper documentation of owner compensation — there's an administrative cost, but it's typically well below the tax savings. Use our <Link href='/tools/scorp-calculator' className='text-[#4CAF50] underline font-semibold'>S-Corp Calculator</Link> to run your numbers.

Do I need a bookkeeper who specializes in trucking, or can a general bookkeeper handle it?

A general bookkeeper can handle trucking if they're willing to learn the industry-specific requirements — IFTA, Form 2290, per diem rules, factoring accounting, and the chart of accounts structure a carrier needs. The risk is a general bookkeeper who doesn't know what they don't know: they'll keep the accounts clean, but they may not flag that your IFTA records aren't sufficient for an audit, or that your per diem payments are structured incorrectly. Ask any bookkeeper you're evaluating: 'How do you handle IFTA?' and 'How do you record factoring transactions?' Their answers will tell you what you need to know.

What are the most common bookkeeping mistakes trucking companies make?

The most common: (1) No trip-level mileage records for IFTA — reconstructed estimates won't survive an audit. (2) Recording the full invoice as revenue when factoring instead of booking the factoring fee separately. (3) Missing Form 2290 renewals in August. (4) Paying per diem as part of the mileage rate without separating it on payroll — it becomes fully taxable wages when bundled. (5) No cost-per-mile tracking by vehicle or lane — the carrier is making or losing money on specific lanes but can't see it. (6) Misclassifying owner-operators as employees or employees as independent contractors.

Related Tools & Resources

Trucking & Carrier Accounting

Know Your Cost Per Mile. Know Your Lane Margins. Know Your Numbers.

406 Consulting Group sets up and manages bookkeeping for carriers who need more than clean accounts — IFTA-ready records, cost-per-mile tracking, per diem programs, and the financial visibility to make real decisions about loads, lanes, and equipment. Let's build the right setup for your fleet.

Trucking Quick Reference

Key numbers and deadlines

Carrier Compliance Calendar

January 31

→ Q4 IFTA return due

→ 1099-NECs to contractors

April 30

→ Q1 IFTA return due

July 31

→ Q2 IFTA return due

August 31

→ Form 2290 (HVUT) due for all qualifying vehicles

October 1

→ UCR registration opens for following year

October 31

→ Q3 IFTA return due

December 31

→ Equipment placed in service for current-year depreciation

→ Year-end tax planning moves

Running a Fleet?

Get IFTA-ready, cost-per-mile-ready books.

About the Author

Jason Anderson

Co-Founder, 406 Consulting Group

Background in large-scale operational finance at BP — including fuel cost tracking, fleet accounting, and compliance reporting at pipeline scale. That discipline applied to Montana carrier operations means the same rigor on cost-per-mile, fuel allocation, and equipment depreciation that moves $75M in inventory uses at scale.

Read the Full Story