SBA Loan Application:

What Lenders Actually Want to See

Most SBA loan content is written from the borrower's side. This guide is written from inside the bank — by someone who has reviewed 300+ commercial loan applications including SBA 7(a), SBA 504, and USDA Business & Industry loans in Montana.

There is no shortage of content about how to apply for an SBA loan. Checklists, guides, bank landing pages, YouTube walkthroughs — all of it written from the borrower's perspective, telling you what documents to gather and what boxes to check. Almost none of it tells you what actually happens on the other side of the desk.

This guide is written from the underwriter's side. Carrie Anderson spent years as a contracted commercial loan analyst for a Montana community bank — reviewing, packaging, and supporting the underwriting of over 300 loan applications, including SBA 7(a), SBA 504, and USDA Business & Industry loans. Her work was reviewed in FDIC examination environments and assessed in KPMG and Wipfli review contexts. She has seen what passes and what doesn't — not in theory, but in the actual files.

What follows is what she would tell you before you submit your application — not after.

By Carrie Anderson — Co-Founder & Principal Analyst, 406 Consulting Group. Former contracted commercial loan analyst, 300+ Montana loan applications reviewed including SBA 7(a), SBA 504, and USDA B&I programs.

Quick Answer: What Do SBA Lenders Actually Look For?

- →Cash flow first: Your Debt Service Coverage Ratio (DSCR) must clear 1.25x at minimum — most community lenders prefer 1.35x or higher. This is calculated from your actual financial statements, not your tax return.

- →Clean books are non-negotiable: Mixed personal/business accounts, inconsistent records, and undocumented owner draws raise underwriting flags that delay or kill approvals.

- →Documents must be lender-ready: There is a difference between having the documents and having them organized, labeled, and formatted the way underwriters expect. The gap costs weeks.

- →Montana rural businesses often qualify for USDA B&I: This program is underutilized and frequently offers better terms with less competition than SBA 7(a) for businesses outside metro areas.

Table of Contents

Why Most SBA Loan Content Gets It Backwards

The typical SBA loan guide starts with the application and works forward. It tells you what forms to fill out, what documents to attach, and what credit score to aim for. That framing is backwards — and it's why so many borrowers show up to the underwriting process unprepared.

An underwriter doesn't read your application the way you wrote it. They work backward from a conclusion they need to defend: can this business service this debt, reliably, over the full term of the loan? Every document in the file exists to answer that question. Every gap in the file creates doubt. Every inconsistency requires an explanation — and explanations slow down approvals.

Here is the mental model that changes how you prepare: the underwriter is not your advocate. They are the person who has to defend the credit decision to a loan committee, to examiners, and potentially to the SBA or USDA guarantee agency during an audit. If your file doesn't give them what they need to make that case, they will ask for more — or they will decline.

How borrowers think about applications

- ✗"I have 3 years of tax returns" → compliance mindset

- ✗"My credit score is 720" → personal approval signal

- ✗"The business has been around 8 years" → longevity = safety

- ✗"I own real estate for collateral" → security = approval

- ✗"My accountant said we're profitable" → profitability = capacity

How underwriters read the same signals

- ✓"Do the tax returns match the P&L, and if not, why?"

- ✓"Is 720 personal credit consistent with the business financial picture?"

- ✓"Does 8 years of revenue show stable trends or a declining trajectory?"

- ✓"Is collateral sufficient to recover loss exposure if the business fails?"

- ✓"What is the documented DSCR from the actual financial statements?"

The Carrie Anderson Perspective

When I reviewed commercial loan files, the applications that moved through underwriting fastest were almost never the ones from the most profitable businesses. They were the ones where the financial picture was clear — where the numbers told a consistent story, where the documents were organized, and where there were no unexplained gaps. A business earning $180,000 per year with clean books, a documented DSCR of 1.45x, and a straightforward three-year revenue trend is a faster approval than a business earning $350,000 with messy financials, owner draws commingled with payroll, and a tax return that doesn't match the bank statements.

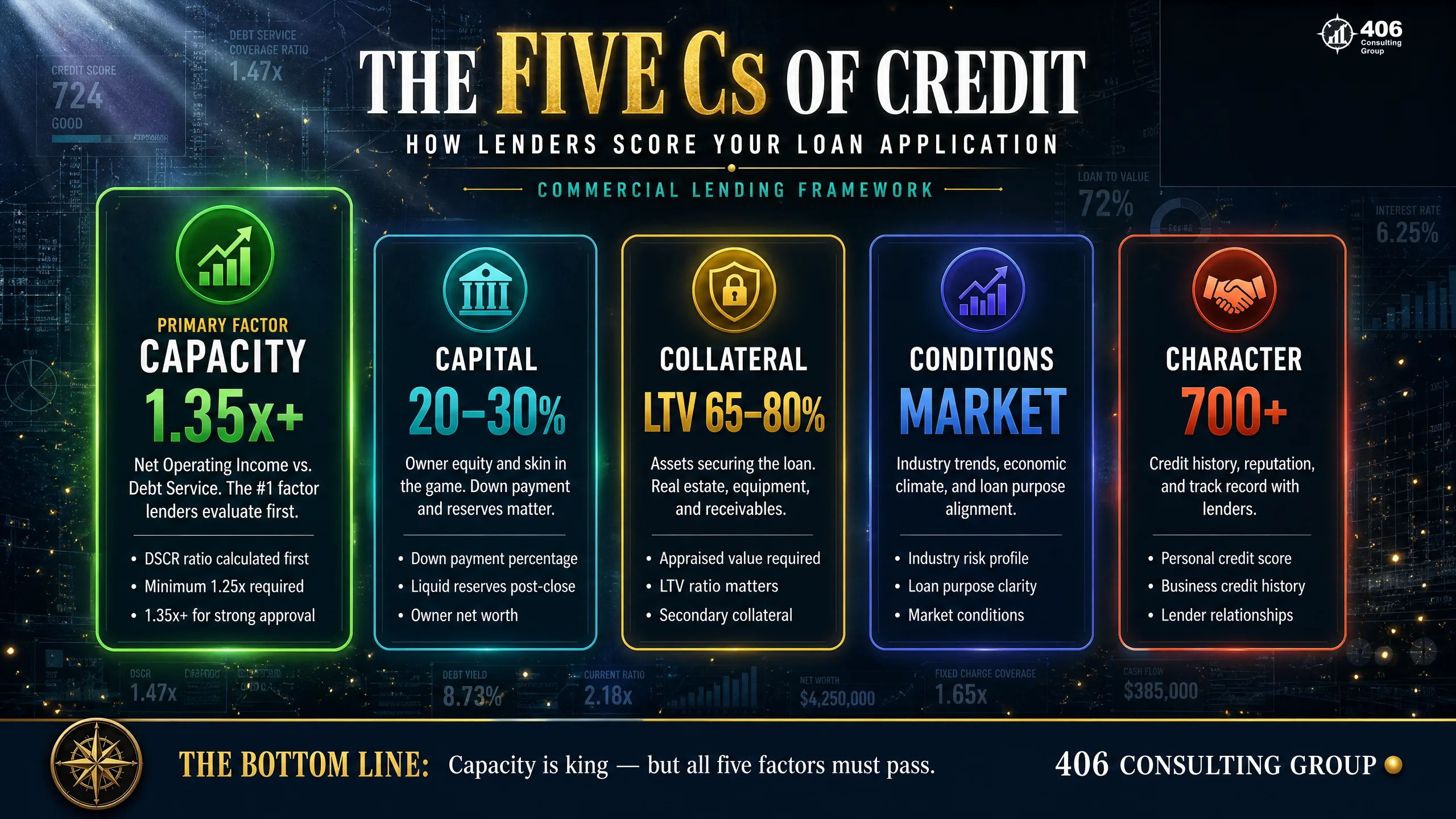

The Five Cs of Credit — From Inside the Bank

The Five Cs of Credit — Capacity, Capital, Collateral, Conditions, Character — appear in every intro banking course and on every bank's website. What those resources don't tell you is which one underwriters weigh most heavily for SBA loans, and what they actually look for in your documents for each one.

Capacity

Primary — 40%+ of the decision

Can your business generate enough cash flow to cover the new debt payment with room to spare? This is the DSCR calculation. It is the most important C and the one borrowers are least prepared to support with documentation.

Capital

Significant — equity injection and owner investment

How much of your own money is in this business? SBA loans typically require 10–30% equity injection from the borrower for acquisition or startup situations. For existing businesses, capital is demonstrated through the balance sheet — positive net worth, reasonable debt-to-equity ratio.

Collateral

Supporting — rarely the deciding factor

The SBA does not require full collateral coverage for 7(a) loans — if the business cash flow supports the loan, a lender cannot decline solely for insufficient collateral. That said, most lenders will take available collateral (business assets, real estate, personal assets) to secure the loan. Collateral is the recovery plan, not the approval rationale.

Conditions

Contextual — industry, purpose, economic environment

Why does your business need this loan, and does the business environment support repayment? Loan purpose must be clearly stated and eligible under SBA program rules. Industry conditions (seasonal, cyclical, or declining industries) affect how conservatively the underwriter models future cash flow.

Character

Baseline — must clear, not a differentiator

Do you have a history of meeting financial obligations? This is the credit check — personal and business credit history, any prior defaults, bankruptcies, tax liens, or judgments. Character problems can disqualify an otherwise strong application. Strong character alone doesn't approve a weak application.

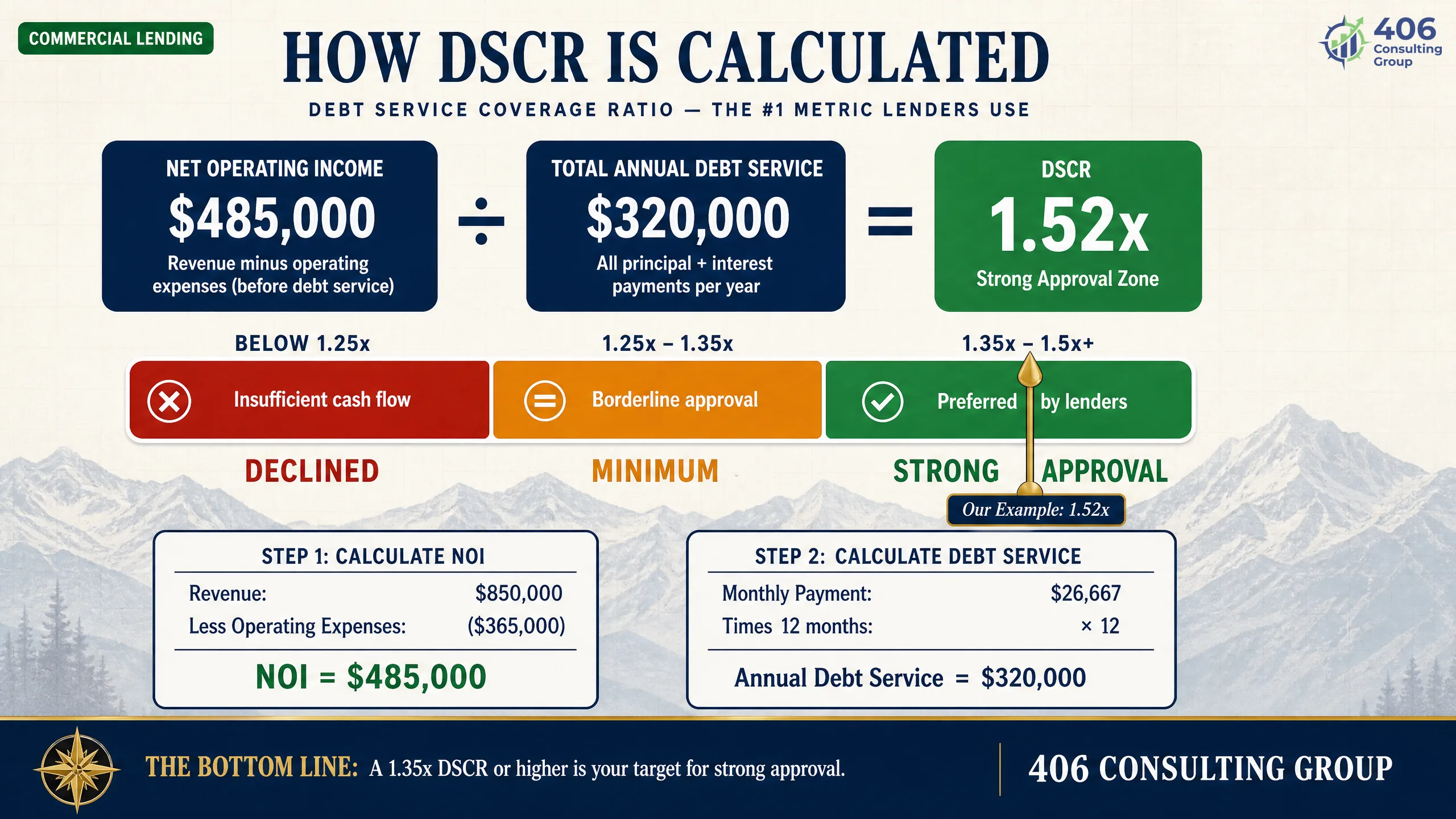

DSCR: The Number That Gates Everything

Debt Service Coverage Ratio is the single most important number in your loan file. Everything else in the application — the collateral, the credit score, the business plan — is context for this number. If your DSCR doesn't clear the threshold, the loan doesn't close. Full stop.

DSCR = Net Operating Income ÷ Total Annual Debt Service

SBA minimum: 1.25x | Community bank preferred: 1.35x+ | Strong: 1.5x+

| Scenario | Net Operating Income | Annual Debt Service | DSCR | Result |

|---|---|---|---|---|

| Clean books, documented add-backs | $142,000 | $87,600 | 1.62x | Strong approval |

| Messy books — same business, undocumented draws | $94,000 | $87,600 | 1.07x | Below threshold — declined |

| Documented add-backs accepted by underwriter | $125,000 | $87,600 | 1.43x | Approved with conditions |

| Seasonal business — 3-yr average used | $108,000 avg | $72,000 | 1.50x | Approved — seasonal narrative required |

The second and third rows above are the same business. The only difference is whether the books supported a clean NOI calculation. This is the most common reason applications that should be approved are declined or delayed: the financial records can't support the DSCR the business is actually generating.

The Add-Back Issue

Add-backs are legitimate — depreciation, owner compensation above reasonable salary, one-time non-recurring expenses — but they must be documented and defensible. An underwriter can accept an owner add-back if: (1) the owner's reasonable market salary is already reflected elsewhere in expenses, and (2) the add-back is labeled, sourced to a specific line item, and consistent across years. A handwritten note in the margin of a P&L is not documentation. A formal add-back schedule prepared by a CPA or financial advisor is.

What “Clean Books” Actually Means to an Underwriter

“Clean books” is one of the most commonly used and least understood terms in small business finance. Business owners hear it as a vague instruction to be organized. Underwriters mean something very specific by it — and the gap between those two interpretations is where applications stall.

Monthly close completeness

Every month has a reconciled P&L, a reconciled balance sheet, and bank statements that match. Not some months — all months. If the books were closed six months ago and you've been estimating since, the underwriter will request updated statements and the process resets.

Account separation

Business income flows into business accounts. Business expenses are paid from business accounts. Owner compensation is documented as either payroll or an owner draw with a clear line item. Personal expenses charged to the business — insurance, car payments, personal purchases — are flagged separately. Commingling is one of the most common underwriting red flags in small business files.

Consistent chart of accounts

The income and expense categories on your P&L should be consistent year over year. If ‘subcontractor expense’ was a line item in 2023, it should be the same line item in 2024 and 2025 — not reclassified to ‘labor’ or split across three categories. Inconsistency forces the underwriter to manually reconcile three years of financials, which takes time and creates doubt.

AR and AP aging

A current Accounts Receivable aging report shows who owes you money and how long it has been outstanding. Underwriters use it to assess receivable quality — heavily concentrated in one customer, or with significant balances over 90 days past due, signals fragility in cash flow that may not appear on the P&L.

Entity and account alignment

The entity on the bank account must match the entity on the tax return must match the entity on the loan application. Out-of-state LLCs that haven't completed Montana foreign qualification, recent entity conversions (LLC to S-Corp), or accounts held in an individual's name instead of the business entity all require additional documentation and explanation.

See our CFO Services Scorecard for a full 84-point assessment of your financial infrastructure — including the bookkeeping and reporting categories most likely to affect lender-readiness.

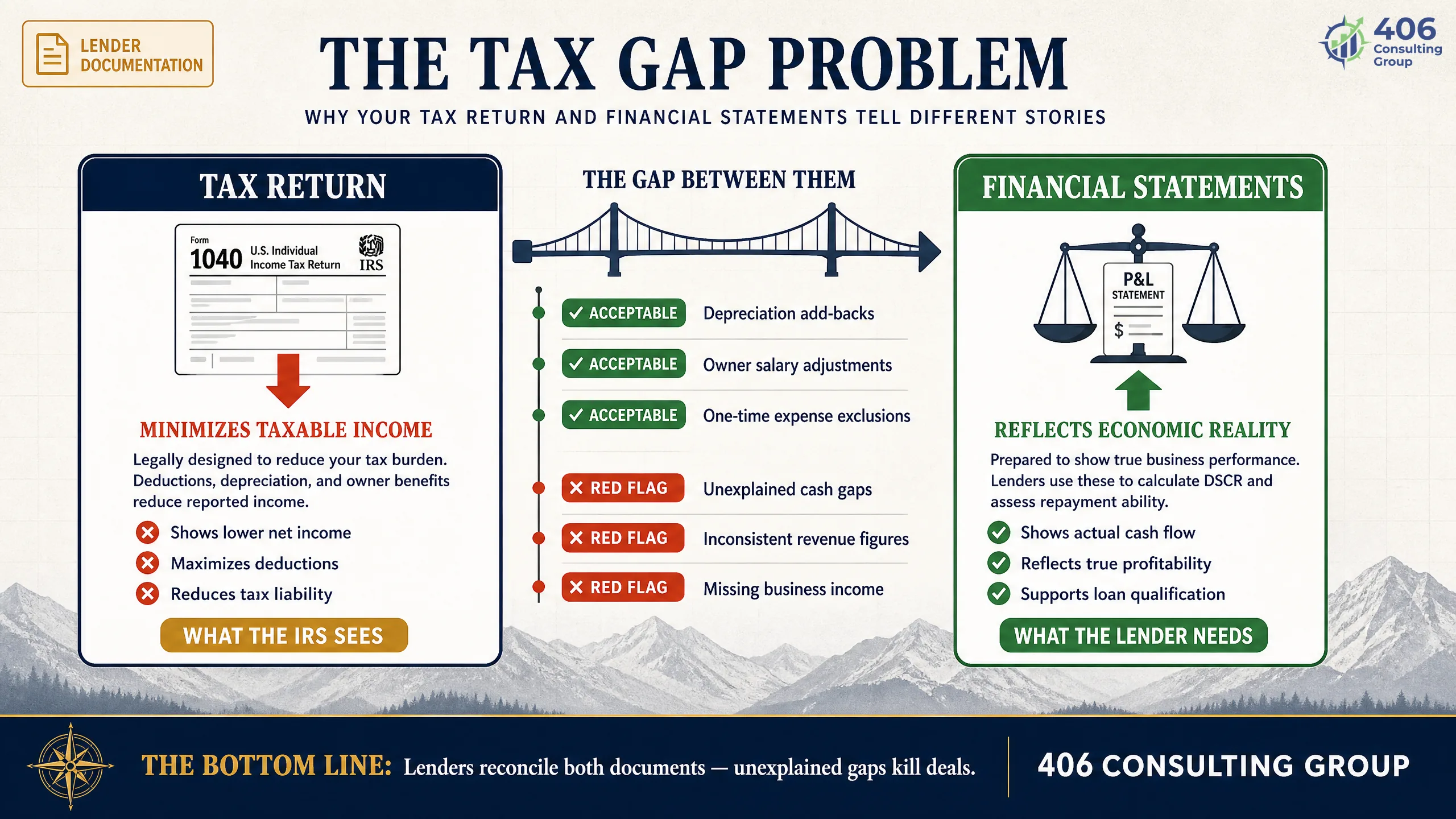

Tax Returns vs. Financial Statements: The Gap That Kills Loans

Here is something most borrowers don't know: an underwriter will always request both your tax returns and your financial statements — and then they will compare them line by line. The gap between what your tax return shows and what your financial statements show is one of the most scrutinized elements in the file.

Tax returns are optimized to minimize taxable income. Financial statements should reflect economic reality. The legitimate differences — depreciation, bonus depreciation, timing of income recognition — are fine and expected. What causes problems is when the gap is large, unexplained, and inconsistent across years.

Acceptable gaps — explain and document

- ✓Depreciation and bonus depreciation (Section 179) — high in tax return, lower or zero in financial statements

- ✓Owner compensation above reasonable salary — documented as add-back

- ✓One-time non-recurring expenses (legal fees, equipment write-off, litigation settlement)

- ✓Timing differences in income recognition (accrual vs. cash basis)

- ✓S-Corp shareholder health insurance and retirement contributions

Problematic gaps — require explanation

- ✗Large undocumented cash revenue not on tax return (triggers IRS and lender concern)

- ✗Revenue on tax return that doesn't appear in bank deposits

- ✗Expenses on financial statements not on tax return without documented rationale

- ✗Inconsistent treatment of owner draws year to year

- ✗S-Corp distributions taken but reasonable salary not reflected in expenses

The S-Corp Election and Loan Applications

An S-Corp election is excellent tax strategy, but it changes how underwriters read your compensation. If you elected S-Corp status, your reasonable owner salary appears as a W-2 expense in the business. Your remaining profit flows through as distributions. An underwriter will identify your W-2 salary from the tax return and may add back any compensation above what they consider a “reasonable market salary” for your role. What they will not give you credit for is S-Corp distributions taken outside of a documented payroll structure — those look like owner draws, not compensation, and get treated differently in the DSCR calculation. The fix is simple: document your salary election, your reasonable compensation rationale, and the payroll history clearly in the file.

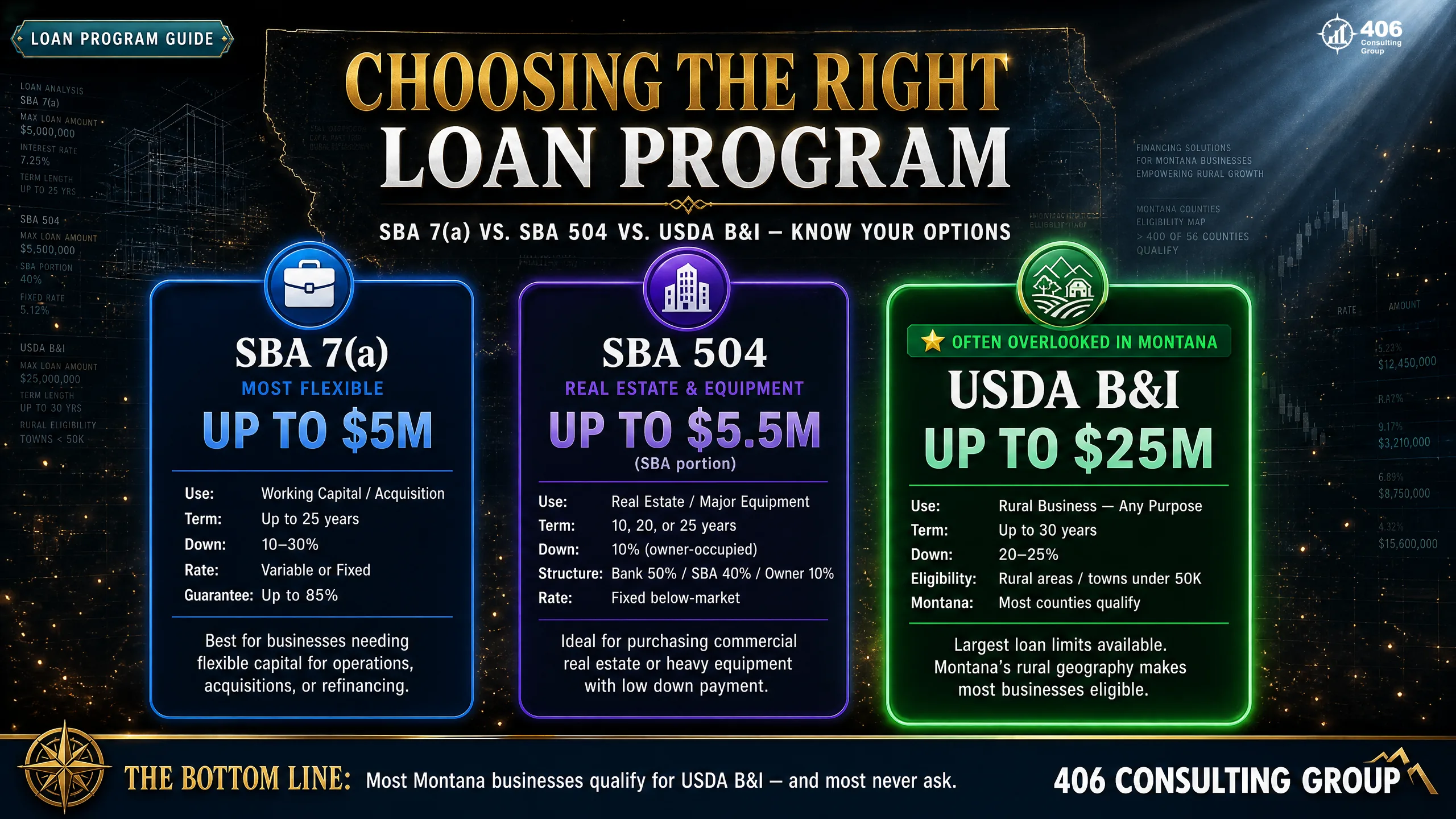

SBA 7(a) vs. SBA 504 vs. USDA B&I: Which One You Actually Need

Most small business owners know about SBA loans. Far fewer know that “SBA loan” covers two very different programs with different structures, different use cases, and different approval considerations. And almost no one outside of rural Montana banking circles knows about the USDA Business & Industry loan — which is frequently the better option for businesses in smaller Montana communities.

SBA 7(a) — The Most Common

Maximum loan

Up to $5 million

Best for

Working capital, business acquisitions, debt refinancing, equipment, tenant improvements

How it works

SBA guarantees 75–85% of the loan. Lender holds the remainder. Interest rate typically Prime + 2.75–4.75% (as of mid-2026, effective rates in the 11–13%+ range). Terms up to 10 years (working capital) or 25 years (real estate).

SBA 504 — Real Estate and Heavy Equipment

Maximum loan

Up to $5.5 million (SBA portion); total project can be much larger

Best for

Commercial real estate purchase, major equipment acquisition, leasehold improvements over $1M

How it works

Three-party structure: 50% conventional lender, 40% Certified Development Company (CDC) backed by SBA debenture, 10% borrower equity injection. The CDC portion carries a fixed rate tied to 10-year Treasury. Lower overall cost than 7(a) for real estate.

USDA Business & Industry (B&I) — Montana's Underused Option

Often overlooked in MontanaMaximum loan

Up to $25 million (guarantee); no hard loan cap from lender

Best for

Rural area businesses — any Montana community outside a metro area of 50,000+ population qualifies. Acquisition, working capital, real estate, equipment.

How it works

USDA guarantees 60–80% of the loan depending on size. Lender sets rate (typically competitive with 7(a)). Key difference: rural eligibility is determined by location, not business type. Most Montana businesses outside Billings, Missoula, and Great Falls qualify.

Why Montana Businesses Should Always Ask About USDA B&I

Most online SBA content is written from a national perspective and ignores rural-specific programs. The USDA B&I program is specifically designed for rural economic development — and Montana's geography means the majority of businesses in the state qualify. Any community outside a metro area of 50,000+ population is eligible; that covers most of Montana outside Billings, Missoula, and Great Falls.

The application runs through participating lenders — community banks and credit unions — rather than directly through the SBA. The USDA Rural Development State Office in Helena administers the program for Montana businesses. Rural lenders who work with this program regularly often have faster, more relationship-driven processes than metro SBA lenders. Fewer borrowers apply, which means fewer competing files and more lender attention per application.

Ask your banker two questions: (1) Does our location qualify for USDA B&I eligibility? (2) Does your institution participate in the program? The answer is often yes on both counts — and if your lender doesn't participate, the Montana USDA Rural Development office can direct you to one that does.

The Personal Financial Statement (SBA Form 413): What It Actually Reveals

Every principal with 20% or more ownership in the business must complete SBA Form 413 — the Personal Financial Statement. Most applicants treat it as a formality and rush through it. Underwriters read it carefully, and not just for the numbers.

Form 413 is a snapshot of your personal financial position: assets, liabilities, income, and contingent liabilities. Here is what underwriters are looking for — and what they notice when something is off.

Personal assets and net worth

Underwriters want to see personal liquidity — not to drain it, but to confirm the owner has some financial cushion if the business hits a rough period. All owners personally guaranteeing the loan should show positive net worth. Negative personal net worth on Form 413 is a significant red flag.

Personal debt obligations

Every personal loan, mortgage, vehicle payment, and credit card minimum is listed. Underwriters use this to assess your total personal debt load. They are looking for whether your personal obligations are sustainable on the income you'll draw from the business — and whether existing personal debt constrains how much equity you can actually inject.

Contingent liabilities

Guarantees on other loans, pending lawsuits, lease obligations. Underwriters look for undisclosed exposure. If you've personally guaranteed a business partner's loan, or you're co-signed on a family member's debt, those must appear on Form 413. Omissions discovered during underwriting or post-closing are treated as misrepresentation.

Income section

The income listed on Form 413 must be reconcilable with your personal tax returns. If you report $180,000 in personal income on Form 413 but your personal tax return shows $120,000, the underwriter will ask. If the business is the source, document it. If there's a legitimate explanation, write it.

Personal Guarantees — What They Actually Mean

SBA loans require personal guarantees from all principals with 20%+ ownership. This means the lender can pursue your personal assets — home equity, personal savings, investment accounts — if the business defaults and collateral recovery is insufficient. This is not a technicality. It is a real obligation. Understand it before signing. That said, it is standard for SBA lending — it is not a reason to decline applying. It is a reason to ensure the loan amount, the business cash flow, and the overall financial plan are sound before committing.

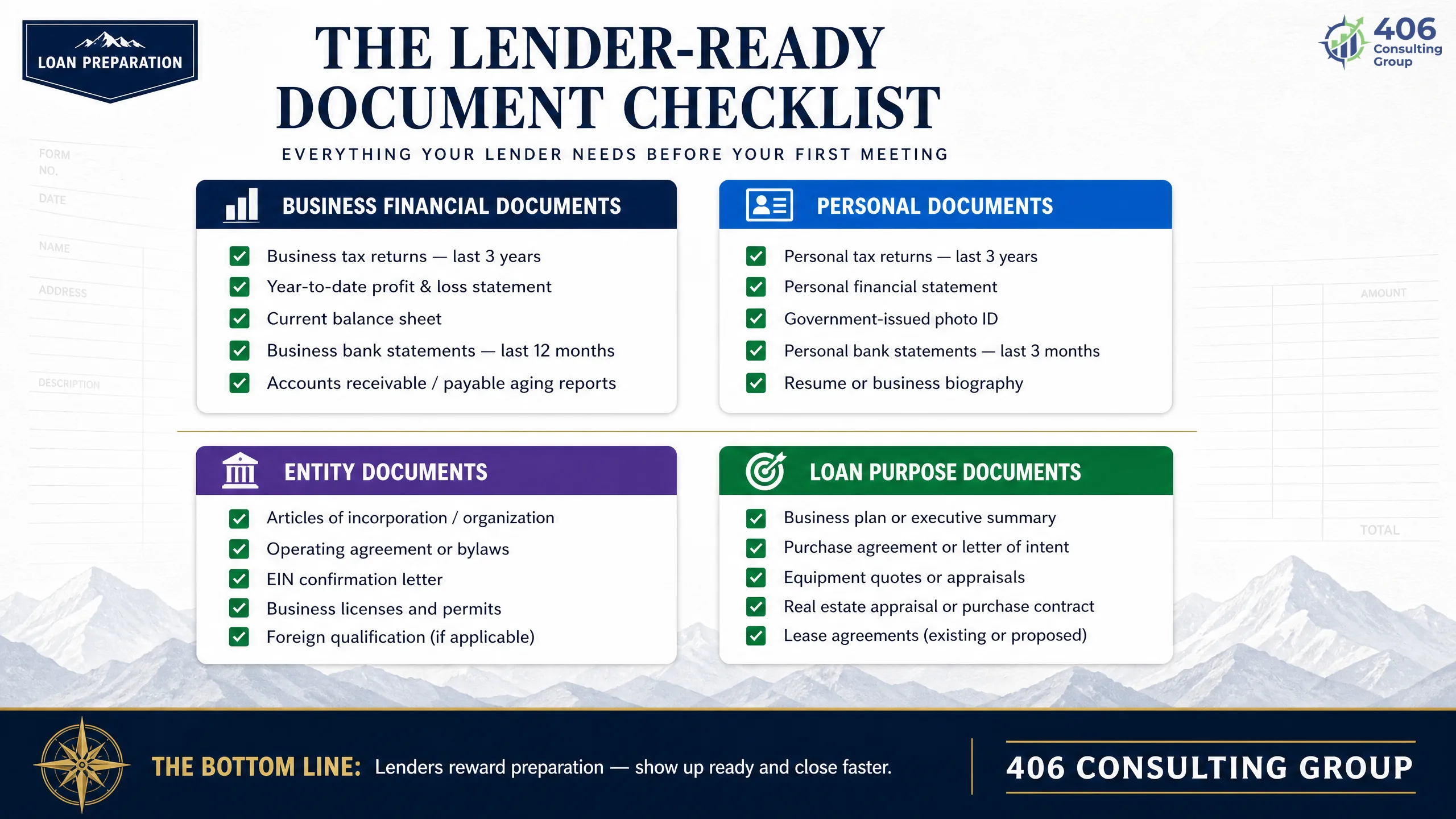

The SBA Loan Document Checklist: Lender-Ready vs. “I Have These”

There is a meaningful difference between having the required documents and having lender-ready documents. The difference is not what you have — it's how it's organized, labeled, and formatted. A disorganized file creates friction at every stage of underwriting. A well-organized file with a clear document index, consistent naming, and logical structure signals professionalism and reduces back-and-forth by weeks.

Business Financial Documents

3 years business federal tax returns (all schedules)

Must match entity on application; S-Corp: Form 1120-S with all K-1s; Partnership: 1065 with K-1s

3 years compiled or reviewed P&L statements

CPA-prepared preferred; must tie to tax returns with documented reconciliation if material differences exist

3 years balance sheets

Year-end; must be internally consistent year-over-year

YTD P&L (current year through last month)

Dated, signed or certified by owner; must be current within 90 days of application

Current balance sheet (within 90 days)

Dated; must reconcile with YTD P&L

Current AR and AP aging reports

Aged; shows concentration risk and collection quality

Existing debt schedule

All current business debt: lender name, original balance, current balance, rate, payment, maturity

Personal Documents (per principal with 20%+ ownership)

3 years personal federal tax returns (all schedules)

Must match income on Form 413; include all K-1s received

Completed SBA Form 413 — Personal Financial Statement

Signed and dated within 90 days; must be internally consistent

Government-issued ID

Driver's license or passport

Personal credit authorization (signed)

Lender pulls credit; don't self-pull and submit — lenders want a fresh tri-merge

Business Entity Documents

Articles of Organization or Incorporation

State-issued; current and matching the entity on the application

Operating Agreement or Bylaws

Signed; current; confirms ownership percentages matching application

Foreign qualification certificate (if applicable)

Required if entity formed outside Montana but operating in Montana. See our guide on Wyoming LLC vs. Montana LLC for foreign qualification costs and what it means for your loan file.

EIN confirmation letter (IRS CP-575 or 147c)

Confirms tax ID matches the entity

S-Corp election confirmation (IRS CP261) if applicable

Confirms S-Corp status and effective date

Loan Purpose Documents

Use of proceeds narrative (1–2 pages)

Specific, detailed, tied to the loan amount. 'Working capital' alone is insufficient — explain the working capital gap and what the funds will address

Business plan or executive summary (for startups or acquisitions)

Not required for established businesses with strong history, but helps for 7(a) acquisitions and 504 real estate

Purchase agreement (if acquisition)

Signed LOI or purchase agreement; list of assets being acquired with valuations

Real estate appraisal (if 504 or real estate 7(a))

SBA-approved appraisal; may be ordered by lender after application — don't order independently

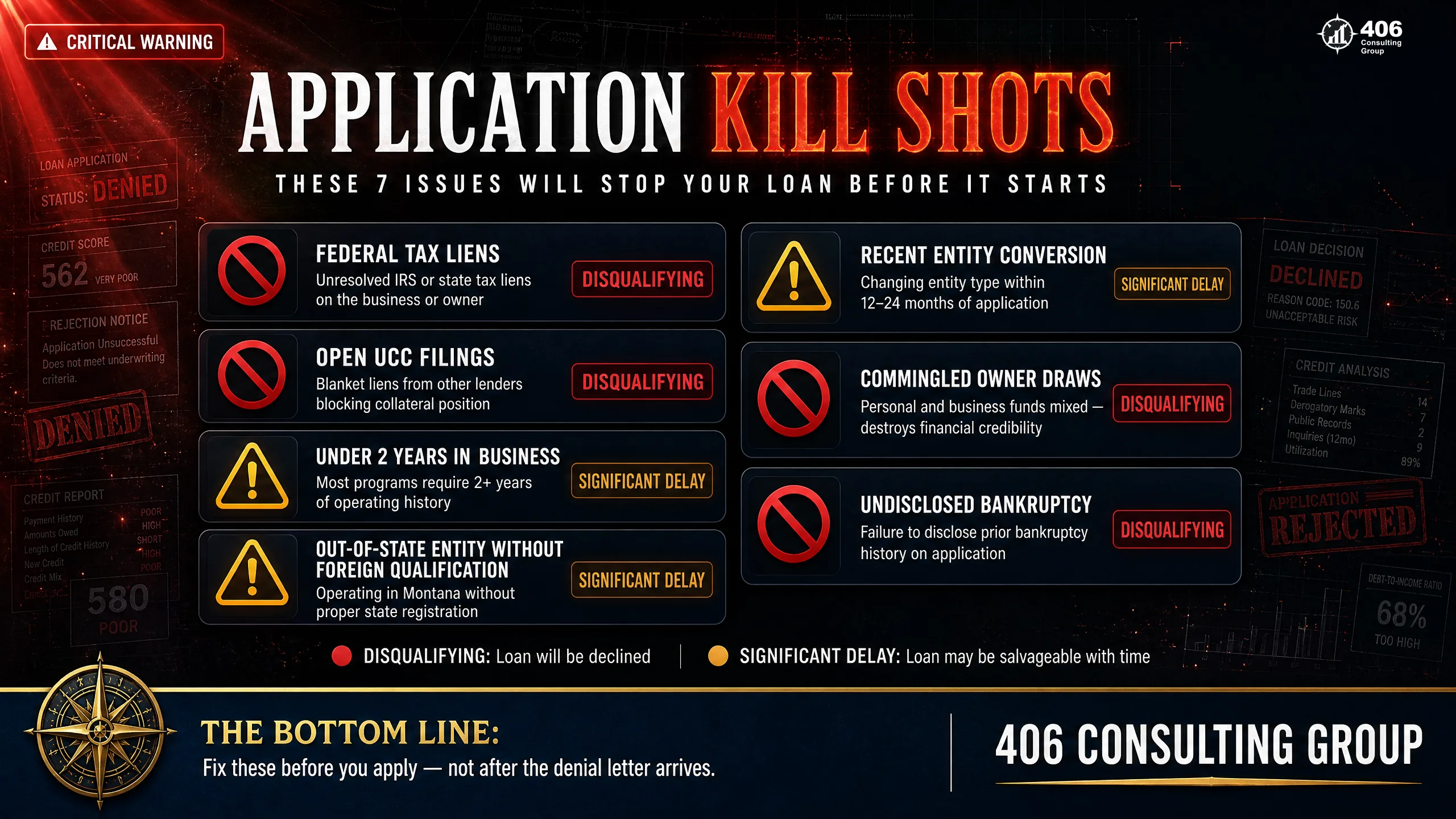

The Kill Shots: What Disqualifies Montana SBA Loan Applications Before Review Starts

There are items that stop a loan file before it reaches substantive underwriting. These are not issues that can be explained away or mitigated with a strong DSCR. They are disqualifying — or at minimum, cause for significant delay and remediation before the application can proceed.

Federal tax liens and delinquencies

Open federal tax liens are visible in UCC searches and credit pulls. SBA loans cannot close with open federal tax liens — the IRS has priority over SBA guarantees and lenders know it. Montana Department of Revenue state tax liens are similarly problematic. The fix is to resolve the delinquency and obtain a lien release certificate before applying, or to work with the IRS on an installment plan (which must be current at the time of application). Don't assume this won't be discovered — lenders specifically check.

Open UCC filings from prior lenders

If a prior lender filed a UCC-1 financing statement against your business assets and you've paid off the loan but the lender never filed a UCC-3 termination, the original filing still appears in searches and complicates new collateral pledging. Audit your UCC filings at the Montana Secretary of State before applying and clear any stale filings.

Business under 2 years old (startup classification)

The SBA defines startups as businesses with less than 2 years of operating history. Startup SBA loans are available but require a detailed business plan, projections, and often a higher equity injection (as much as 30%). Lenders are more conservative. If you are approaching the 2-year mark, waiting 6 months for the classification to change can meaningfully improve your application outcome.

Out-of-state entity without Montana foreign qualification

A Wyoming LLC, Nevada LLC, or Delaware entity operating in Montana without completing foreign qualification with the Montana Secretary of State lacks legal standing to conduct business here. A lender making a Montana business loan to an entity without legal standing in Montana faces guarantee complications. Resolve this before applying — the Montana foreign qualification process takes days and costs $70.

Recent entity conversion or formation (under 12 months)

If you converted from a sole proprietorship to an LLC, or from an LLC to an S-Corp, within the last 12 months, underwriters will want continuity documentation showing the business operated under prior structure and the conversion was properly executed. Newly formed entities with no operating history face startup classification regardless of how long the underlying business operated informally.

Owner draws commingled with payroll — undocumented

If your compensation as an owner is a mixture of payroll, sporadic draws, business expense reimbursements, and personal charges to the business card — with no consistent documentation — the underwriter will have difficulty computing a clean DSCR. They will discount what they can't document, which means your DSCR will be lower than your actual cash flow supports. The fix is to run a clean separation for at least 6 months before applying.

Bankruptcy within 3–7 years (depending on lender)

Prior personal or business bankruptcy is not automatically disqualifying for SBA loans, but must be disclosed on the application. Undisclosed bankruptcy discovered during underwriting is treated as misrepresentation, which is far worse. Lenders have different seasoning requirements — generally 3 years minimum, 7 years preferred. Apply with a lender who has experience with post-bankruptcy applicants and document the cause, resolution, and subsequent financial history clearly.

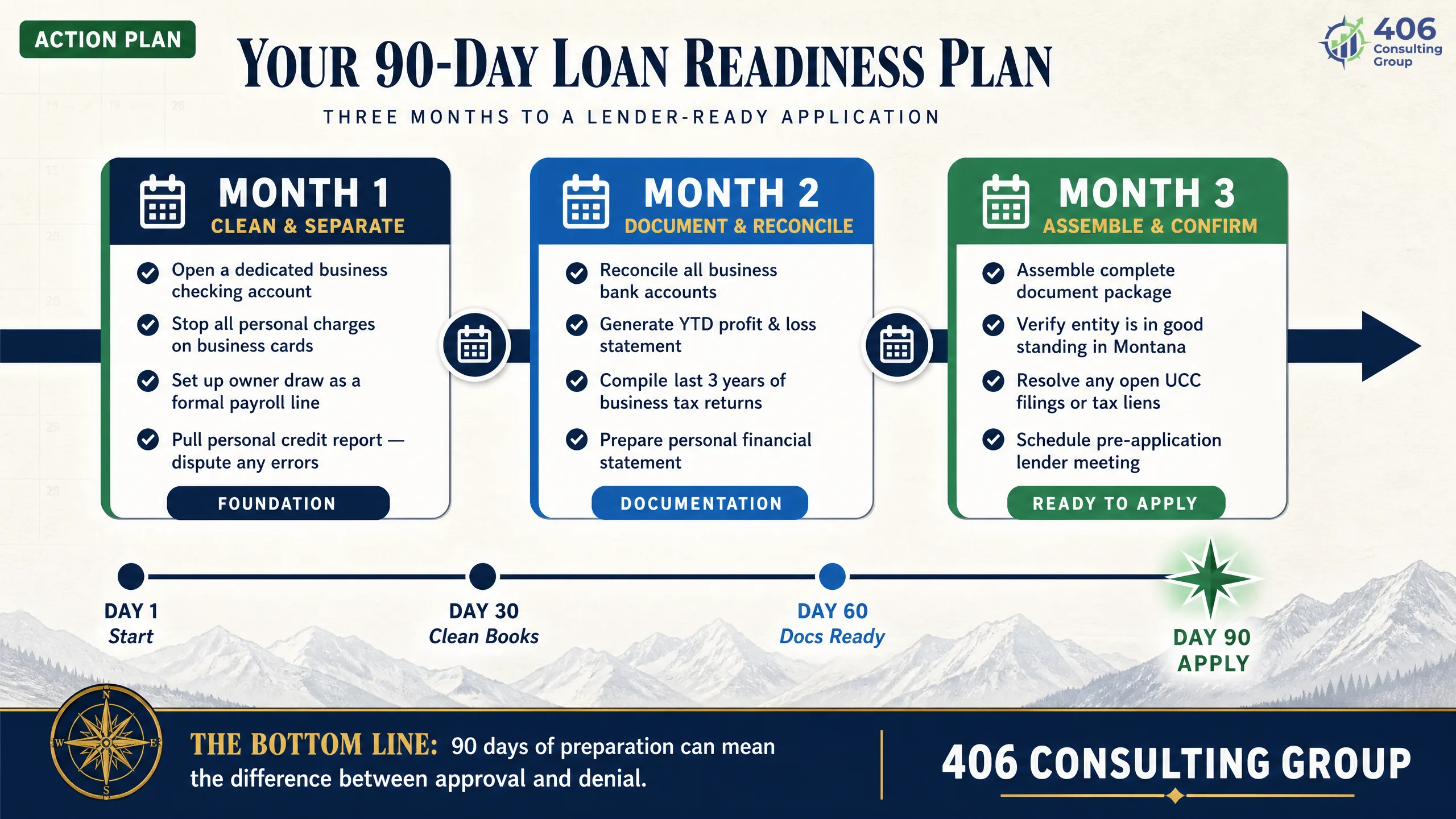

The 90-Day Prep Timeline: What to Fix Before You Apply

The single most impactful thing a business owner can do to improve their SBA loan outcome is not to find the right lender or optimize their application — it is to spend 90 days before applying getting their financial house in order. Three months of clean, documented, reconciled financial operations materially changes what an underwriter can calculate.

Month 1 — Clean and Separate

Month 2 — Document and Reconcile

Month 3 — Assemble and Confirm

Use the Loan Qualification Tool — Before You Apply

406 Consulting Group has built a Loan Qualification Assessment tool that walks you through the key underwriting criteria — DSCR, debt load, financial statement quality, entity structure — and gives you a directional read on where your application stands before you sit down with a lender. Run it before your 90-day prep begins so you know what to prioritize.

Run the Loan Qualification AssessmentIf your financials need significant work before an application is realistic, a conversation with 406 Consulting will give you a direct assessment of what needs to change and in what order — including whether a controller engagement or CFO advisory makes sense as preparation for a capital raise.

Frequently Asked Questions: SBA Loans for Montana Businesses

What credit score do you need for an SBA loan?

The SBA does not publish a minimum credit score requirement, but most lenders look for a personal credit score of 650 or higher for SBA 7(a) applications. Community lenders participating in USDA B&I programs may have slightly more flexibility. More important than the score itself is the story behind it — a 680 with a documented period of difficulty and a consistent 3-year recovery trend is a different file than a 680 with recent delinquencies. Pull your credit report before applying and be prepared to explain any derogatory marks proactively.

Can I get an SBA loan if my business is less than 2 years old?

Yes, but you will be classified as a startup and the requirements are more demanding. Startups typically need a detailed business plan with financial projections, a higher equity injection (up to 30% for some loan types), and a stronger personal financial picture to compensate for the lack of operating history. If you are within 6 months of the 2-year mark, consider whether waiting is worth the improved positioning. If you must apply now, have your business plan and personal financial statement tightly documented.

Do SBA loans require collateral?

The SBA's position is that lenders should not decline a loan solely for insufficient collateral if cash flow supports the debt. In practice, lenders will take all available collateral — business assets, equipment, real estate — to secure the loan. If business collateral is insufficient, lenders may require personal real estate as additional collateral on loans above $350,000. Collateral supports the recovery scenario if the business fails; it is not the primary approval driver. A strong DSCR with limited collateral is a better file than strong collateral with a weak DSCR.

How long does SBA loan approval take?

SBA 7(a) loans processed through preferred lenders (PLP status) can close in 30–60 days from a complete application. Non-preferred lenders submit to the SBA for direct approval, which adds 15–30 days. SBA 504 loans typically take 60–90 days due to the CDC involvement. USDA B&I loans can take 60–120 days depending on USDA processing volume. These timelines assume a complete, clean application. Incomplete files, missing documents, and unexplained financial inconsistencies add weeks at every stage. The 90-day preparation period described above exists specifically to avoid delays caused by document gaps.

What kills an SBA loan application during underwriting?

The most common underwriting killers are: a DSCR below 1.25x when properly calculated (not self-reported), open federal tax liens or state tax delinquencies, undisclosed bankruptcy or judgment history discovered during the process, an entity without legal standing in Montana (out-of-state LLC without foreign qualification), and financial statements that cannot be reconciled to tax returns. The kill shots that occur before underwriting even begins are federal tax liens and bankruptcy — these are visible in the first searches run on any application.

Does my entity type affect SBA loan eligibility?

Entity type affects the documentation required more than eligibility itself. Sole proprietors, LLCs, S-Corps, and C-Corps all qualify for SBA loans. What changes is how compensation is documented, how the DSCR is calculated, and which forms are required. S-Corps need Form 1120-S and all K-1s. Partnerships need Form 1065 and K-1s. Sole proprietors use Schedule C. The key is that the entity on the application matches the entity on all financial documents and bank accounts — any mismatch requires resolution before the file can move forward.

SBA Loan Quick Reference

Key numbers for Montana borrowers

Which Loan Is Right for You?

SBA 7(a)

Working capital, acquisition, refinancing

SBA 504

Real estate, heavy equipment (10%+ equity required)

USDA B&I

Rural MT businesses — often overlooked, often better terms

Prepare Before You Apply

Know where you stand before the lender does.

Related Services

About the Author

Carrie Anderson

Co-Founder & Principal Analyst, 406 Consulting Group

Former Corporate Controller who served as a contracted commercial loan analyst for a Montana community bank — reviewing and packaging over 300 loan applications including SBA 7(a), SBA 504, and USDA B&I programs. Her work was reviewed in FDIC examination environments and assessed in KPMG and Wipfli review contexts. She has seen firsthand what passes and what doesn't.

Read the Full Story