Expanding to a Second Location:

The Financial Readiness Checklist

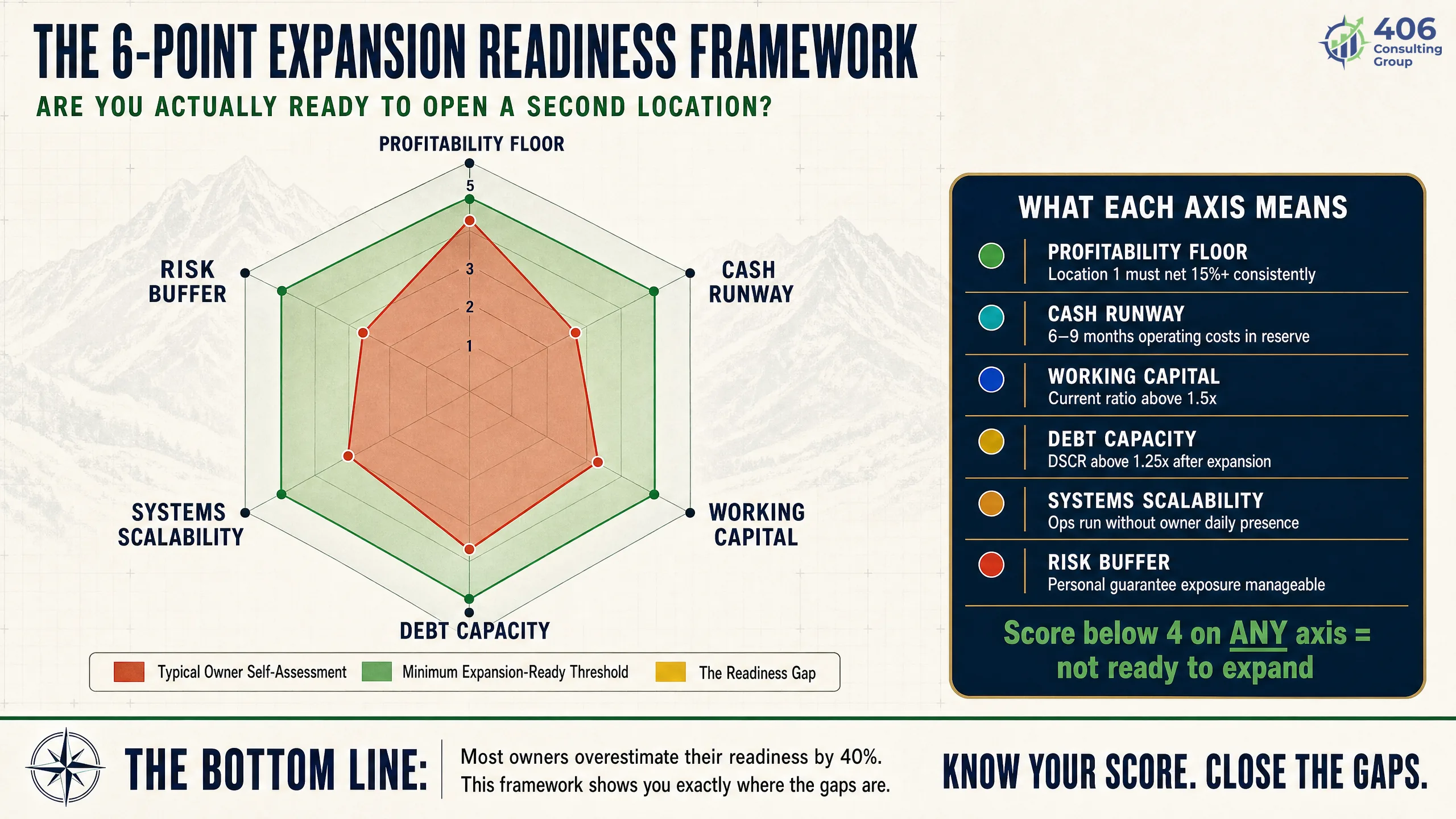

Most businesses that fail at a second location had the customers. What they didn't have was the financial infrastructure to survive the ramp. Six conditions must be green before you sign anything.

Most businesses that fail at a second location had the customers. They had the brand, the demand, and the confidence. What they didn't have was the financial infrastructure to survive the ramp — the cash runway, the working capital, the systems, and the margin floor at location one that would have told them the timing was wrong. Expanding to a second location is not a reward for being busy. It's a financial decision that requires six specific conditions to be met simultaneously before you sign anything.

This checklist covers the 6-Point Expansion Readiness Framework that 406 Consulting Group uses to evaluate whether a business is financially ready to expand — not just operationally ambitious. It covers what a second location actually costs (most owners are off by 40–60%), how lenders evaluate expansion financing, what to negotiate in a lease before you sign, Montana-specific multi-location considerations, and what the first 90 days look like financially if you do it right — and what they look like when you don't.

Table of Contents

The Go/No-Go Question: When a Second Location Makes Financial Sense

The short answer: a second location makes financial sense when all six conditions in the Expansion Readiness Framework are green at the same time. Not five of six. Not "mostly there." All six — because each one represents a failure mode that has killed real businesses that had everything else going for them.

40–60%

How much owners underestimate startup costs

The gap between what business owners budget and what a second location actually costs in the first 12 months.

Month 6–9

Typical second-location break-even

Most second locations don't generate positive cash flow until month 6 at the earliest — often closer to month 9 or beyond.

1 in 3

Second locations that underperform year one

Not failures — but cash negative longer than projected, creating strain on the first location that funded the expansion.

The distinction that matters most: operational readiness and financial readiness are different questions. A business can be operationally ready to run two locations — great systems, good management, replicable product — and still be financially unready. Financial readiness is about whether the balance sheet, the cash position, and the first location's profit margins can absorb the ramp period of the second location without putting everything at risk.

The Question Most Owners Ask vs. The Question That Matters

Most owners ask: "Can I run two locations?" The question that actually predicts success: "Can location one's cash flow support location two for nine months if location two ramps slower than projected?" If the honest answer is no — the timing isn't right, regardless of how strong the market opportunity looks.

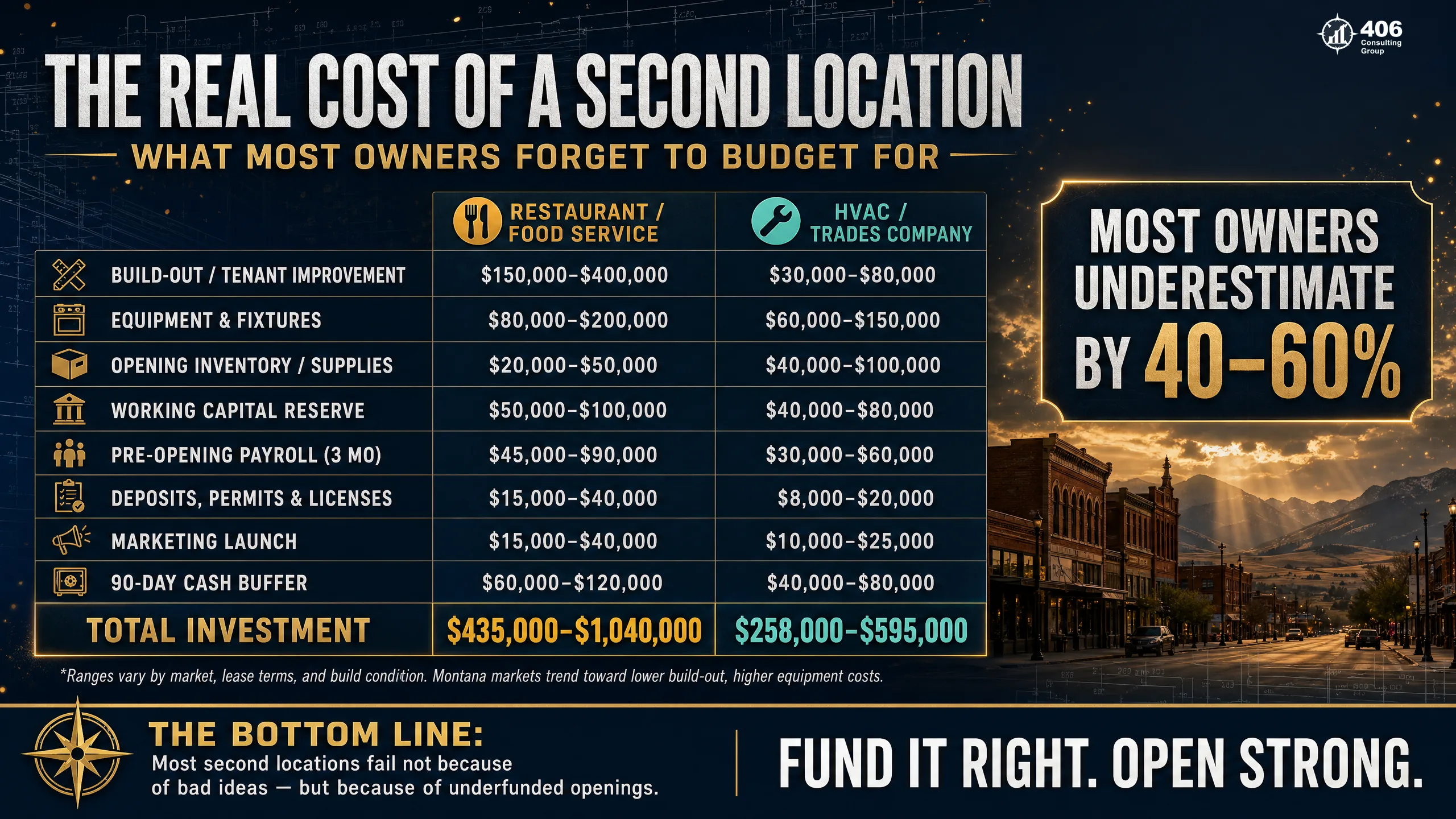

What a Second Location Actually Costs

Owners who have been through one location buildout consistently underestimate the second. The reasons: they forget the one-time costs they absorbed years ago, they undercount pre-opening payroll, and they build their model around best-case ramp assumptions instead of median-case. Here's the real cost breakdown.

| Cost Category | Low | Typical | High | Notes |

|---|---|---|---|---|

| Build-Out / Tenant Improvement | $15K | $60K | $200K+ | Highly variable — landlord TI allowance can offset $20K–$80K |

| Equipment & Fixtures | $8K | $35K | $120K+ | Industry-specific; often financed separately via equipment loan |

| Opening Inventory | $10K | $30K | $80K+ | Product businesses only; must be funded before first sale |

| Working Capital Reserve | $20K | $60K | $150K+ | 3–6 months operating costs; this is the number most owners skip |

| Pre-Opening Payroll | $8K | $25K | $60K+ | 4–8 weeks of staff training before revenue starts |

| Deposits & Permits | $3K | $12K | $30K+ | Security deposit, utility deposits, licensing, health permits |

| Marketing Launch | $3K | $10K | $40K+ | Grand opening, digital ads, local PR — often underbudgeted |

| Contingency / Overrun Buffer | $5K | $20K | $50K+ | Build-outs always run over; budget 15–20% contingency on construction |

| Total Range | $72K | $252K | $730K+ | Before financing costs |

The Number Most Owners Leave Out

Working capital reserve is the line item that kills second locations. Owners budget the build-out and the equipment but don't separately fund the cash cushion that covers 3–6 months of operating costs while the new location ramps. They assume revenue will cover it. In month one, it won't. In month three, it might. In month six, it usually does. The question is whether you have the bridge.

The 6-Point Expansion Readiness Framework

406 Consulting Group evaluates second-location readiness across six financial dimensions. Each one is a necessary condition — not just a nice-to-have. A business that scores green on five of six and red on one has a structural risk that the other five strengths won't protect it from. Use this framework before you talk to a landlord, before you call a lender, and before you tell your team about the expansion plan.

Profitability Floor

Location 1 must demonstrate sustainable net profit margins that prove the model works — not just that it's surviving.

Cash Runway

You need 6–9 months of projected location 2 operating costs in liquid reserve before opening day.

Working Capital

Separate from cash runway — the float needed to cover inventory, bridge payroll, and absorb AR timing gaps.

Debt Capacity

Your DSCR must support the new debt load at location 2's projected (not hoped) revenue, with a safety margin.

Systems Scalability

Bookkeeping, payroll, and reporting must work across two locations before you open the second one — not after.

Risk Buffer

A documented financial plan for what happens if location 2 takes 18 months to break even instead of 9.

Point 1: Profitability Floor — Location 1 Must Prove the Model

A second location replicates your model — including its weaknesses. If location one is generating thin margins because of structural cost issues, an inefficient pricing model, or owner labor that isn't priced into the P&L, location two will replicate those problems at double the overhead. The profitability floor check confirms that location one is genuinely profitable, not just busy.

| Industry | Minimum Net Margin for Expansion | Red Flag Below |

|---|---|---|

| Restaurant / Food Service | 12–18% | Under 10% — cover costs won't survive a slow ramp |

| Retail | 8–12% | Under 6% — no cushion for location 2 drain |

| Professional Services | 20–30% | Under 15% — owner compensation likely not properly reflected |

| Construction / Trades | 10–15% | Under 8% — job costing issues that scale badly |

| Healthcare-Adjacent | 15–22% | Under 12% — billing cycle gaps amplified at second location |

| Fitness / Wellness | 18–25% | Under 14% — high fixed cost base makes ramp period brutal |

Case Study: The Hidden Margin Problem

A Bozeman fitness studio was generating $380K in annual revenue with what looked like a 22% net margin. They came to us ready to sign a Missoula lease. When we rebuilt their P&L properly — replacing the owner's $28K "draw" with a market-rate salary of $65K for the management role she was filling — the real margin dropped to 14%. Still expansion-ready by our threshold, but the conversation about the second location changed completely. They budgeted for a general manager at the new location from day one instead of assuming the owner could cover both. That single adjustment saved them from a staffing crisis in month four.

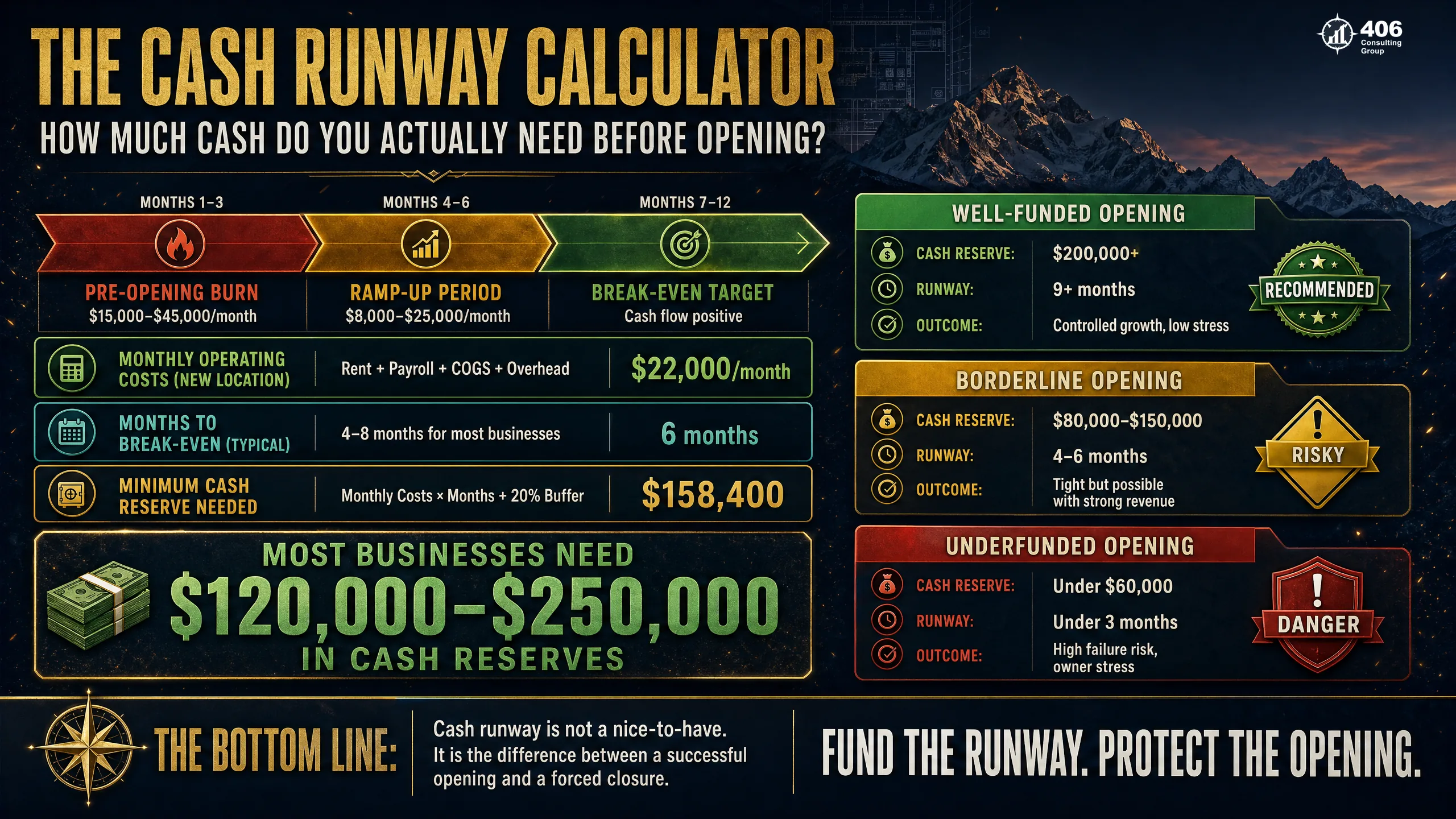

Point 2: Cash Runway — 6 Months of Operating Costs Before Day One

Cash runway is the number of months you can operate location two at full cost with zero revenue before you run out of money. The minimum viable runway before opening is six months. Nine months is safer. Anything under four months and you're betting that the ramp goes exactly as planned — which it almost never does.

How to Calculate Your Runway

Projected monthly operating costs

Rent, payroll, COGS, utilities, insurance — full run-rate at location 2, not partial

Multiply by 6 (minimum) or 9 (preferred)

This is your runway reserve — liquid cash, not available credit

Subtract from current liquid assets

Cash + money market + available line of credit = liquid position

If the result is negative, you're not ready

You need to build cash, reduce costs, or find additional financing before proceeding

Runway Scenario: $25K/Month Opex

Point 3: Working Capital — Inventory, Payroll Bridge, and AR Gap

Working capital and cash runway are related but different. Cash runway is how long you can operate with zero revenue. Working capital is the capital needed to fund operations even when revenue is flowing — because revenue and expenses don't arrive at the same time. A business can be generating strong sales and still run out of cash because inventory is purchased before it's sold, payroll is due before invoices are collected, and suppliers require payment terms that don't match your receivables cycle.

Inventory Float

Product businesses must fund location 2's opening inventory before the first sale. At 45-day inventory turns on $30K of stock, you're carrying $30K continuously before the cash cycle closes.

Payroll Bridge

Staff are hired 4–8 weeks before opening. That payroll is funded entirely from reserves — no revenue offset. For a 10-person team at $18/hr average, that's $28K–$56K before day one.

AR Gap

B2B businesses billing net-30 or net-60 have a gap between earning revenue and collecting it. At $60K/month in sales on net-45 terms, you're carrying $90K in receivables that aren't in your bank.

The Working Capital Rule of Thumb

For most businesses, maintain working capital of at least 15–20% of projected location 2 annual revenue before opening. A location projecting $500K in year-one revenue needs $75K–$100K in accessible working capital — separate from the cash runway reserve — to absorb timing gaps without cash crisis moments.

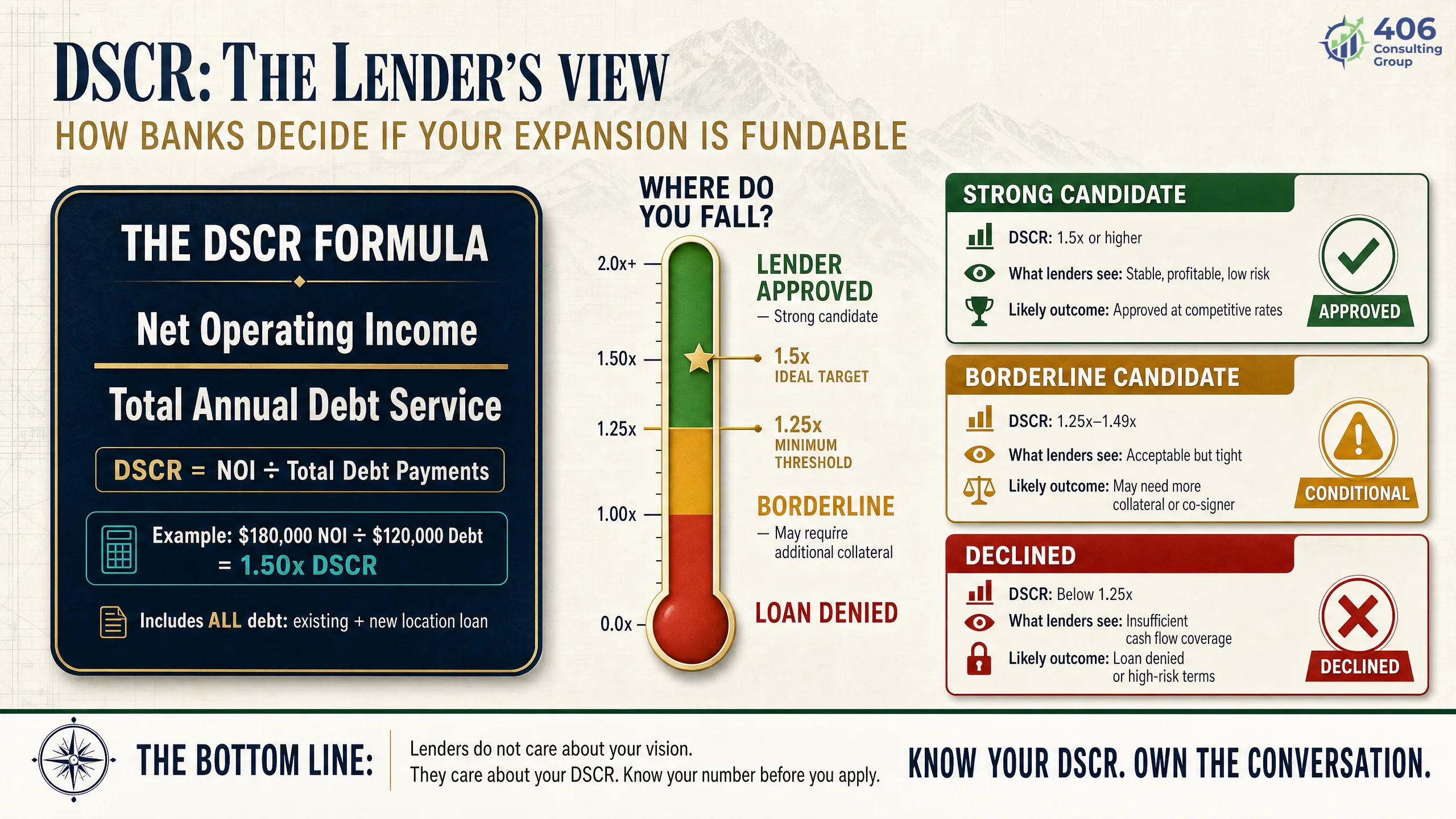

Point 4: Debt Capacity — What Your DSCR Tells a Lender (and You)

DSCR — debt service coverage ratio — is the single most important number in any expansion financing conversation. It measures whether your business generates enough net operating income to cover its debt payments, with room to spare. Lenders require a minimum of 1.25×. The question isn't just whether you can get the loan — it's whether your DSCR at location 2's realistic (not optimistic) revenue projection leaves you with enough margin to absorb a slower ramp.

DSCR Calculation

Net Operating Income

Revenue minus operating expenses (before debt service)

Total Annual Debt Service

All loan principal + interest payments per year

DSCR

Must be 1.25× minimum; 1.5× preferred

| DSCR | Lender View | Your Risk Assessment |

|---|---|---|

| Below 1.0× | Decline — income doesn't cover debt | Cannot service the debt even at projected revenue |

| 1.0×–1.25× | Borderline — some lenders may approve with strong collateral | Zero margin for slower ramp or unexpected costs |

| 1.25×–1.5× | Approvable — meets standard underwriting threshold | Minimal buffer; proceed only if runway is strong |

| 1.5×–2.0× | Strong — preferred by most commercial lenders | Adequate cushion for ramp variance |

| Above 2.0× | Excellent — lender competition for the deal | Comfortable — focus on lease terms and timing |

Use our Loan Qualification tool to model your DSCR before approaching a lender. Run it at three scenarios: your projected revenue, 75% of projected, and 50% of projected. If the DSCR falls below 1.25× at 75% of projection, the expansion financing is too thin.

Point 5: Systems Scalability — Bookkeeping and Payroll Across Two Locations

The financial systems that work fine for one location routinely fail at two. The failure mode isn't technical — it's structural. A single QuickBooks file with no location-level class tracking, a payroll system that processes everyone under one entity, and a monthly close that takes six weeks are manageable at one location. At two, they create financial blind spots that cost real money.

Single-Location System at Two Locations

- ✗Revenue and expenses mixed — can't see which location is profitable

- ✗Payroll split manually each period — error-prone and slow

- ✗Inventory tracked in spreadsheets — no real COGS by location

- ✗Month-end close takes 6+ weeks — decisions made on stale data

- ✗No location-level P&L — owner manages by feel, not numbers

- ✗Tax reporting requires manual allocation at year-end

Scalable System Before You Expand

- ✓Class tracking by location in QBO — P&L by location in real time

- ✓Payroll platform (Gusto, ADP) with multi-location cost allocation

- ✓COGS tracked by location — gross margin visible per location

- ✓15-day monthly close discipline — management package by the 15th

- ✓Location-level KPI dashboard — revenue, margin, labor % per location

- ✓Entity structure confirmed before opening — tax reporting is clean

Build these systems at location one before you open location two — not after. The cost of retrofitting a broken multi-location accounting setup is far higher than building it right the first time. Our bookkeeping services include multi-location chart of accounts setup and the class tracking configuration that makes location-level reporting automatic.

Point 6: Risk Buffer — Plan for 18 Months if You're Projecting 9

The risk buffer is the honest answer to this question: if location two takes twice as long to break even as you're projecting, what happens to the business? If the answer is "we'd be in serious trouble," you don't have a risk buffer — you have a bet. A risk buffer is a documented financial contingency plan, not an optimistic projection and a hope.

| Scenario | Break-Even at Month | Cash Required Beyond Runway | Risk Buffer Needed |

|---|---|---|---|

| Base case (projected) | Month 7 | $0 beyond reserve | Covered by runway |

| Slow ramp (–25% revenue) | Month 10 | $18K–$35K additional | Line of credit or additional reserve |

| Very slow ramp (–40% revenue) | Month 14 | $50K–$80K additional | Committed credit facility required |

| Near-failure scenario (–60% revenue) | Month 18+ | $100K–$150K+ additional | Location 1 must fund — assess survivability |

What a Real Risk Buffer Looks Like

An unused line of credit with $75K–$150K available, confirmed before opening — not applied for after you need it. A signed commitment from location one's cash flow (with the math to back it up) to fund a defined monthly shortfall. A decision threshold: "If location two is below X revenue at month six, we initiate this action plan." Risk buffers are pre-made decisions, not improvised responses.

Financing a Second Location: SBA, Bank Lines, and What Actually Gets Approved

Most second-location financing is a combination of sources — rarely one clean loan that covers everything. Understanding what each financing type is designed for and what it requires helps you approach lenders with the right ask and the right documentation. Carrie Anderson's commercial underwriting background informs this section: here's what actually gets approved and why.

| Financing Type | Best For | Typical Terms | Key Requirement |

|---|---|---|---|

| SBA 7(a) Loan | Working capital, equipment, build-out costs | Up to $5M / 10-year term / 9–11% current rate | 2+ years in business, 680+ credit, 1.25× DSCR |

| SBA 504 Loan | Real estate purchase or major equipment (over $150K) | Up to $5.5M / 20–25 year / ~6–7% fixed debenture / 10% down | Owner-occupied RE, net worth under $15M, job creation |

| Conventional Bank Term Loan | Lower amounts with strong collateral | $50K–$500K / 5–7 year term / prime +1–3% | Strong personal credit, collateral, 3 years financials |

| Business Line of Credit | Working capital float and risk buffer | $25K–$500K revolving / prime + 1–4% / annual renewal | Profitability, clean credit, typically asset-based |

| Equipment Financing | Specific equipment at location 2 | 100% of equipment value / 3–7 year / equipment as collateral | Equipment must have resale value; quick approval |

| Landlord / Seller Carry | TI allowance or purchase price carry | Negotiated — often 0% TI amortized into rent | Strong lease credit; leverage when market is soft |

For a deeper look at what lenders actually review in a commercial loan application, see our guide on what banks look at for a commercial loan.

What Actually Gets Declined — From an Underwriter's Desk

The most common reason a second-location loan gets declined isn't bad credit or no collateral — it's financials that don't support the projected revenue. An owner projects $600K at location two because location one does $600K. The underwriter looks at location one's ramp history, the new market's demographics, and the owner's management bandwidth and adjusts the projection. If the loan doesn't cash flow at the adjusted projection, it doesn't get approved. Bring lender-ready financials from location one, a realistic 3-year pro forma for location two, and a clear plan for management coverage — and come in at a 1.5× DSCR on your conservative projection, not your optimistic one.

The Lease Financial Analysis — What to Negotiate Before You Sign

The lease is the largest long-term financial commitment in a second-location expansion — often 5–10 years of fixed costs that survive even if the location doesn't. Most business owners negotiate price (base rent) and miss the clauses that have far larger financial impact over the term.

Negotiate Hard On These

- ✓Tenant Improvement (TI) Allowance: Ask for $30–$80/sq ft depending on market. Landlords expect to negotiate. Get it in writing before signing.

- ✓Rent Abatement Period: 3–6 months of free or half-rent during build-out and ramp. Standard in most commercial markets — just ask.

- ✓CAM Cap: Common area maintenance charges can escalate 8–12% annually without a cap. Negotiate 3–5% annual cap in writing.

- ✓Personal Guarantee Scope: Try to limit to 1–2 years instead of full term. A 10-year personal guarantee is a 10-year personal liability.

- ✓Renewal Option with Rate Cap: Lock in the right to renew at a defined rate (CPI + 3% max) — protects you from rent shock at renewal.

Red Flags — Walk Away or Renegotiate

- !Unlimited personal guarantee: Full lease term personal guarantee means the landlord can come after personal assets for 10 years if the business fails.

- !No TI allowance in a soft market: In most Montana markets, landlords provide TI. A landlord who won't negotiate TI in a vacancy-heavy market is a red flag.

- !Uncapped CAM charges: We've seen CAM charges double over a 5-year term. Uncapped CAM is a hidden rent increase that compounds annually.

- !No co-tenancy or go-dark clause: If the anchor tenant in your strip center leaves, your traffic disappears. A co-tenancy clause lets you renegotiate or exit.

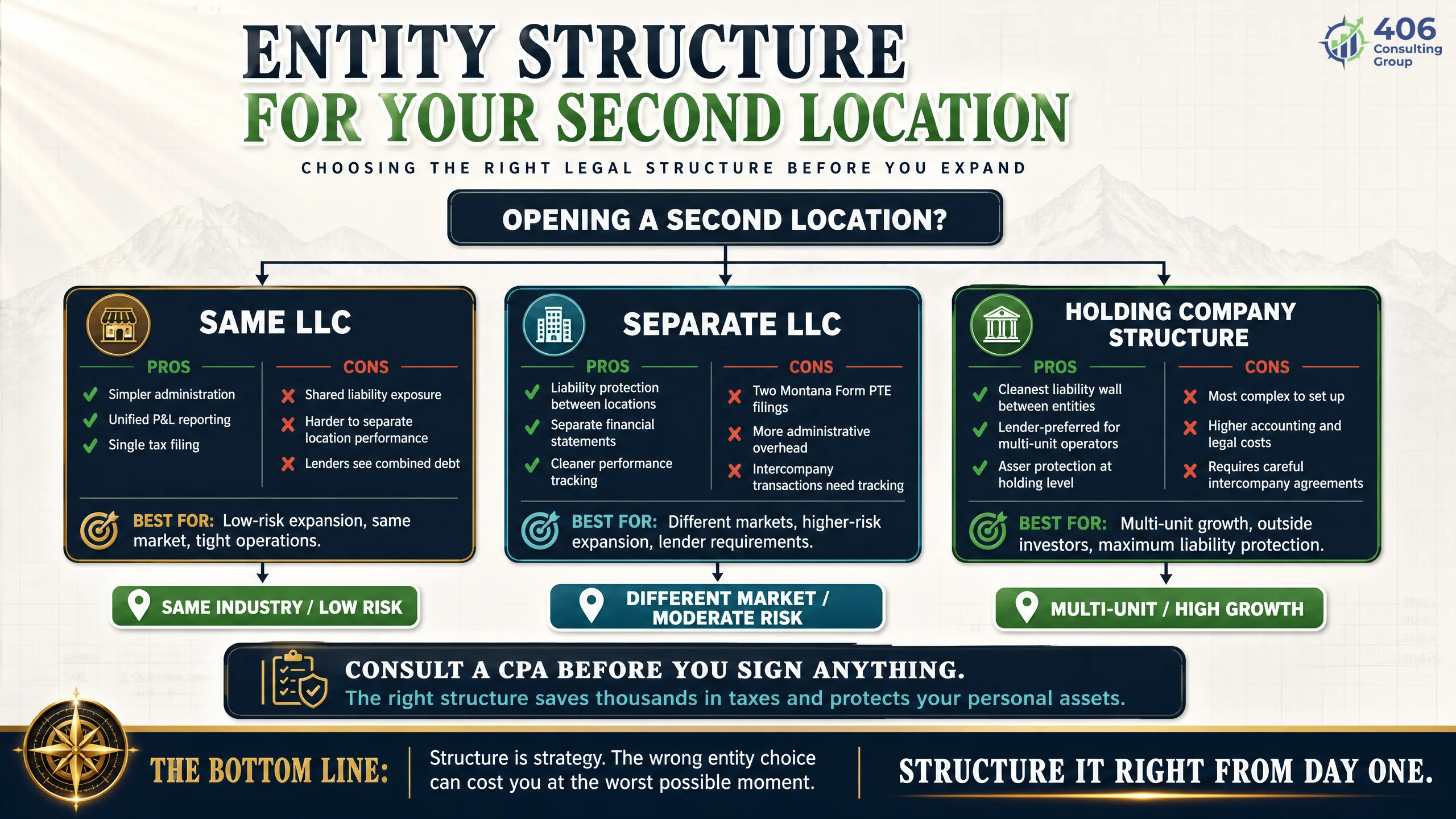

Montana Multi-Location Considerations

Montana businesses expanding to a second location have state-specific financial and tax decisions that national resources don't address. The biggest one: whether the second location should operate under the same entity or a separate LLC. This is both a tax question and a liability question, and the right answer depends on your specific situation.

| Structure | Financial Pros | Financial Cons | Best For |

|---|---|---|---|

| Same LLC (both locations) | Simpler bookkeeping, one Form PTE, losses from Location 2 offset Location 1 profits | No liability wall between locations, commingled financials require class tracking discipline | Lower-risk businesses, tight owner management bandwidth |

| Separate LLC per location | Clean liability separation, independent financials for each location, easier to sell one location | Two Form PTEs, two payroll entities, more complex bookkeeping | Higher liability exposure (food service, healthcare), lender preference for larger deals |

| Holding Company + Operating LLCs | Maximum liability protection, lender-preferred for multi-unit operations, cleanest exit structure | Most complex, highest accounting cost, management fee structure between entities required | 3+ locations, franchise models, investor-backed expansion |

Montana Form PTE — Multi-Entity Impact

Each Montana LLC or S-Corp files its own Form PTE by March 15. Two separate entities means two PTE returns, two sets of estimated payments (Form EST), and two sets of payroll filings (MW-1, MW-3). Factor this compliance complexity into your bookkeeping cost when choosing entity structure.

UI Wage Base Across Locations

Montana's UI taxable wage base is $47,300 per employee (2026). If both locations are under one entity, the base applies per employee across both — employees who hit the base early stop generating UI tax regardless of which location they work. Under separate entities, the base resets — employees may hit it twice.

Multi-location expansion is typically the inflection point where a bookkeeper alone isn't enough. Our CFO services include entity structure planning, inter-company accounting setup, and the consolidated financial reporting that two-location businesses need to make informed decisions and satisfy lenders. Use our Business Maturity Assessment to see where your financial systems stand relative to what a second location demands.

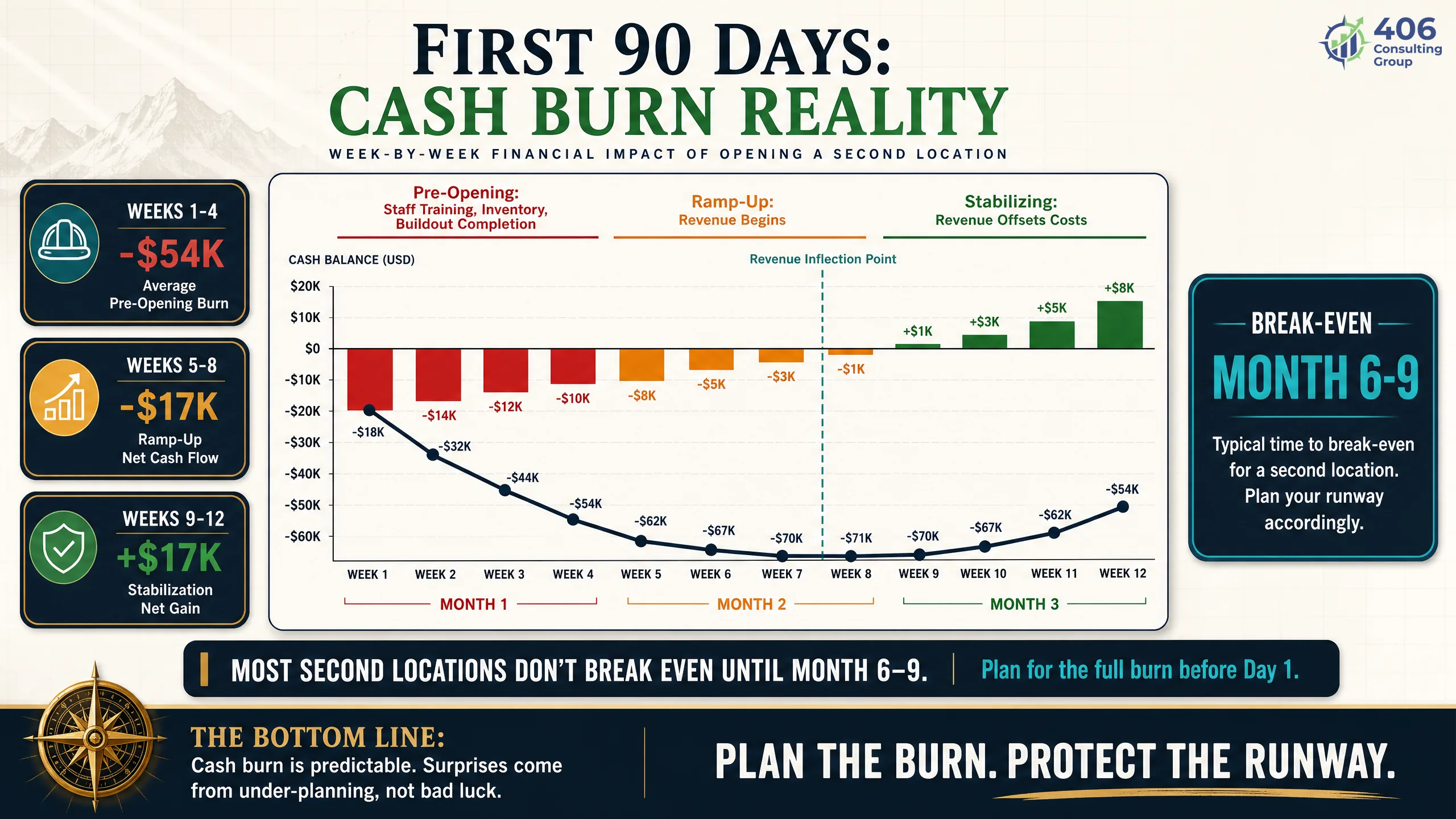

The First 90 Days: Cash Burn, Break-Even, and Warning Signs

The first 90 days are the highest-risk period of any second location. Costs are at full run-rate from day one. Revenue ramps slowly. The cash burn rate in this window determines whether your runway was adequate — and whether you need to activate your risk buffer plan early.

- ›All fixed costs active: rent, payroll, insurance, utilities — from day one

- ›Revenue at 20–40% of run-rate in most retail and service businesses

- ›Net weekly cash burn typically $5K–$25K depending on location size

- ›Owner focus: staffing issues, operational problems — financial monitoring critical

- ›Action: weekly cash position report; compare actual burn to model

- ›Revenue typically at 40–70% of projected run-rate by week 8

- ›Variable costs (COGS, hourly labor) scaling with revenue — burn rate declining

- ›First month-end close: actual vs. projected P&L by location

- ›Determine if ramp trajectory matches model — adjust risk buffer if behind

- ›Action: activate line of credit if cash position drops below 3-month operating costs

- ›Break-even typically reached by week 12–16 for service businesses; week 20–30 for restaurant/retail

- ›First full-quarter close: performance vs. projection by location

- ›Payroll calibration: adjust staffing to actual revenue level, not projected

- ›Lender reporting if covenants require quarterly financials

- ›Action: if still cash-negative at week 13, activate the documented contingency plan — do not improvise

| Industry | Typical Break-Even | Conservative Estimate |

|---|---|---|

| Professional Services / Consulting | Month 3–5 | Month 6–8 |

| Construction / Trades | Month 3–6 | Month 7–10 |

| Retail | Month 6–9 | Month 9–14 |

| Healthcare-Adjacent | Month 4–7 | Month 8–12 |

| Restaurant / Food Service | Month 7–12 | Month 12–18 |

| Fitness / Wellness | Month 6–10 | Month 10–16 |

Frequently Asked Questions

How much working capital do I need before opening a second location?

As a rule of thumb, maintain working capital of at least 15–20% of projected year-one revenue at location two, separate from your cash runway reserve. For a location projecting $500K in year-one revenue, that's $75K–$100K in accessible working capital to cover inventory float, payroll bridges, and AR timing gaps. This is in addition to — not instead of — your 6–9 month operating cost cash runway.

Should my second location be a separate LLC or under the same entity?

For most Montana businesses, a separate LLC for each location is the recommended structure. It provides liability separation between locations, cleaner P&L visibility per location, and is preferred by commercial lenders for larger expansion deals. The trade-off is additional Montana Form PTE filings and slightly more complex bookkeeping. A holding company structure (HoldCo owns both operating LLCs) is ideal for three or more locations or investor-backed expansion. Consult with a Montana tax advisor before deciding — the right answer depends on your specific liability exposure and tax situation.

What does a bank look at when financing a second business location?

Commercial lenders evaluate: (1) DSCR — net operating income vs. total debt service, minimum 1.25×; (2) two to three years of location one financials; (3) a realistic pro forma for location two with documented assumptions; (4) personal credit score (typically 680+ for SBA); (5) collateral — personal guarantee is common for small business expansion loans; (6) management capacity — who runs location one when you're at location two. Come with lender-ready financials, a conservative 3-year projection, and a clear answer to the management question.

How long does it typically take a second location to break even?

Break-even timelines vary significantly by industry. Professional services and construction typically break even in months 3–6. Retail and healthcare-adjacent businesses typically take months 6–9. Restaurants and food service typically take months 7–12, sometimes longer. Use the conservative estimate when building your cash runway — budget for the longer timeline and be pleasantly surprised if it comes sooner. Never build your financing model around the optimistic break-even.

What financial systems do I need before expanding to a second location?

Before opening a second location you need: (1) cloud-based accounting with location-level class tracking (QuickBooks Online or Xero); (2) a payroll platform that handles multi-location cost allocation; (3) a monthly close discipline producing location-level P&L by the 15th; (4) accounts receivable aging by location; (5) a management reporting package that shows both locations on one dashboard. These systems must be running and tested at location one before location two opens — not built after the fact.

What are the most common financial mistakes businesses make when opening a second location?

The six most common: (1) Opening with under 60 days of cash runway — cash crisis by month three. (2) Replicating a barely-profitable location one — doubling the volume doubles the problem. (3) No location-level bookkeeping — can't see which location is bleeding. (4) Signing a full-term personal guarantee without scope limits. (5) Hiring for location two before it opens without modeling the pre-revenue payroll burn. (6) No systems before scaling — accounting chaos across two locations that requires expensive cleanup.

Expansion Planning

Ready to Run the Numbers on a Second Location?

406 Consulting Group builds the financial model, evaluates the six readiness conditions, and tells you the honest answer — before you sign a lease or commit to a lender. We've seen what works and what doesn't across Montana multi-location businesses.

6-Point Expansion Readiness Framework

All 6 must be green before you sign

Profitability Floor

Location 1 net margin proves the model

Cash Runway

6–9 months of Location 2 operating costs

Working Capital

Inventory float, payroll bridge, AR gap

Debt Capacity

DSCR 1.25× minimum at conservative revenue

Systems Scalability

Multi-location bookkeeping before Day 1

Risk Buffer

Plan for 18 months if projecting 9

Break-Even by Industry

Plan for the conservative timeline

Related Guides