When to Change Your Business Entity:

5 Signs You've Outgrown Your Current Structure

Most Montana business owners pick an entity at formation and never revisit it. The Entity Fit Framework tells you when the structure is costing more than it saves — and what to do about it.

Most business owners choose their entity structure once — at formation — based on what their accountant or attorney recommended at the time, or what was cheapest to set up. Then they grow. Revenue doubles. They hire employees. They take on contracts with real liability exposure. They start thinking about selling in five years. And the entity they chose when they were a one-person shop billing $90,000 a year is quietly costing them tens of thousands of dollars annually in taxes they don't have to pay.

The wrong entity structure is rarely a sudden crisis — it's a slow, compounding leak. This guide uses the Entity Fit Framework to diagnose whether your current structure still fits where your business actually is today, and identifies the five specific signs that tell you the answer is no. If three or more apply to your business, the conversation about changing your structure is overdue.

Table of Contents

The Entity Decision Most Business Owners Delay Too Long

The structure that was right at $80,000 in annual revenue is almost never right at $400,000. The business has changed — the entity hasn't. This gap is where excess tax liability lives, where liability exposure grows unchecked, and where exit value gets quietly eroded by the wrong ownership structure for what a buyer will actually want to purchase.

$18K–$24K

Excess SE tax paid over 3 years

What a business owner at $200K net profit pays by staying in an LLC past the S-Corp crossover point for three years.

March 15

S-Corp election deadline

The IRS deadline to elect S-Corp status for the current tax year. Miss it and you wait another year — or apply for a late election.

5 signs

Any 3 of 5 means act now

The Entity Fit Framework checks five dimensions. Three or more red flags in the same business is a clear signal the structure review is overdue.

Why Business Owners Don't Make the Change

Jason Anderson has worked through Montana entity structure transitions with businesses ranging from $80K sole proprietors to multi-entity S-Corp operations — and the same three reasons come up every time. (1) "My accountant hasn't brought it up" — many accountants file what you have rather than proactively redesigning what you should have. (2) "It seems complicated" — an LLC-to-S-Corp election is a single IRS form and a payroll setup. It's three weeks of work, not three months. (3) "I'm not sure it's worth it" — at $150K net profit, the math is almost always clearly yes. Run the numbers before deciding it's not worth the effort.

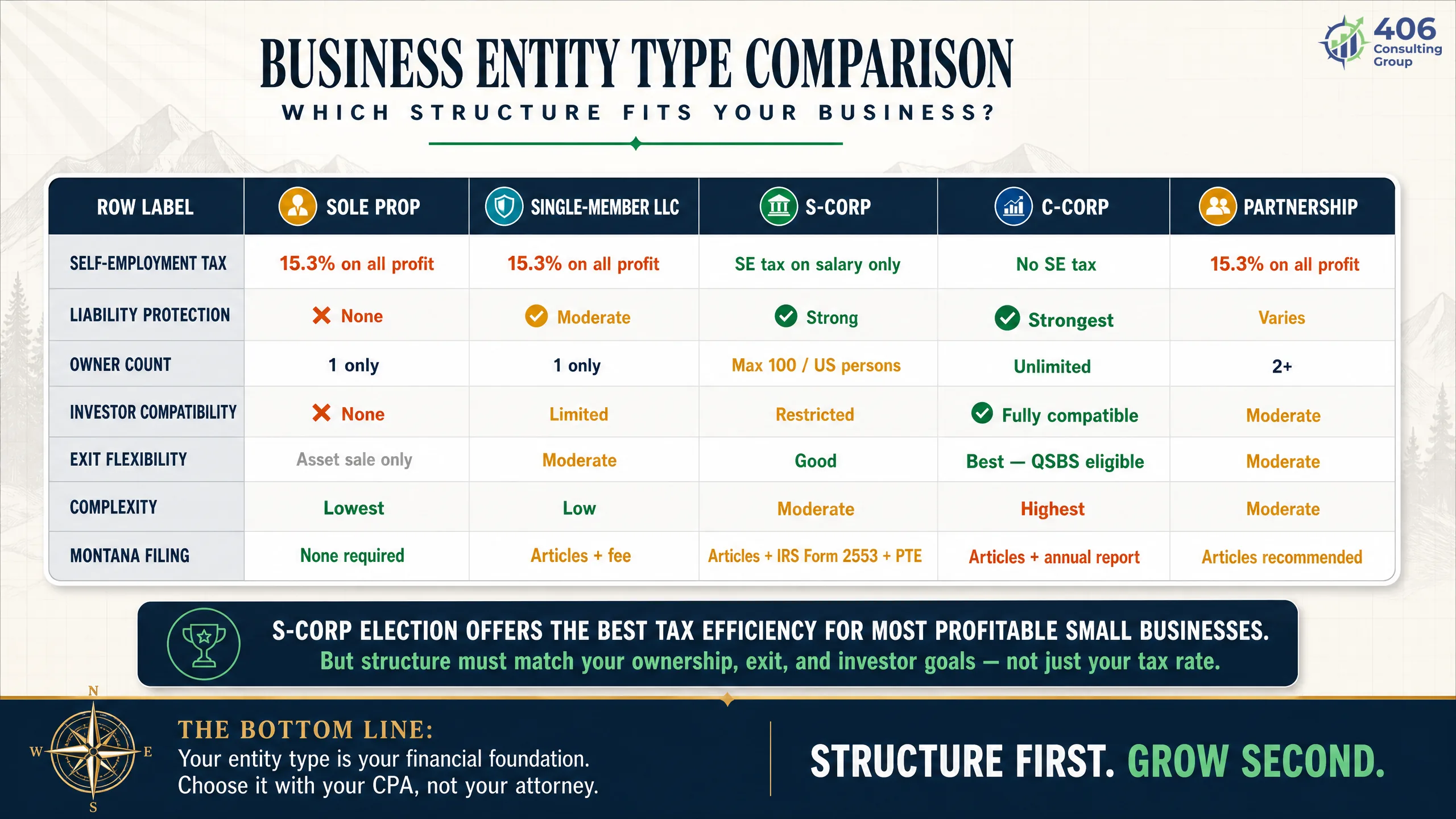

How Business Entity Types Actually Work

Before diagnosing whether your structure fits, a clear-eyed look at what each structure actually delivers — not textbook definitions, but what the differences mean financially.

| Entity Type | SE Tax | Liability Shield | Owner Limit | Best For |

|---|---|---|---|---|

| Sole Proprietor | All net income (15.3% / 2.9%) | None | 1 (you) | Testing an idea — not scaling one |

| Single-Member LLC | All net income (same as sole prop) | Charging order protection | 1 | Early stage; low revenue; low liability exposure |

| Multi-Member LLC | Active members pay SE on share | Charging order protection | Unlimited, flexible | Partners who want flexibility over formality |

| S-Corporation | W-2 salary only (not distributions) | Corporate veil | Max 100; US persons; one class of stock | $60K+ net profit; owner doing W-2-able work |

| C-Corporation | W-2 salary only | Corporate veil (strongest) | Unlimited; foreign; preferred stock OK | Venture-backed; QSBS strategy; institutional capital |

| Partnership | General partners pay SE on share | None for general partners | 2+ required | Professional firms; real estate; limited structures |

The Tax Classification Distinction That Confuses Most Owners

An LLC is a legal entity — it describes your liability structure. An S-Corp is a tax election — it describes how the IRS taxes your income. You can have an LLC that is taxed as an S-Corp. That's the most common transition for growing Montana businesses: keep the LLC legal structure, elect S-Corp tax treatment via IRS Form 2553. You don't need to form a new corporation to get S-Corp tax benefits.

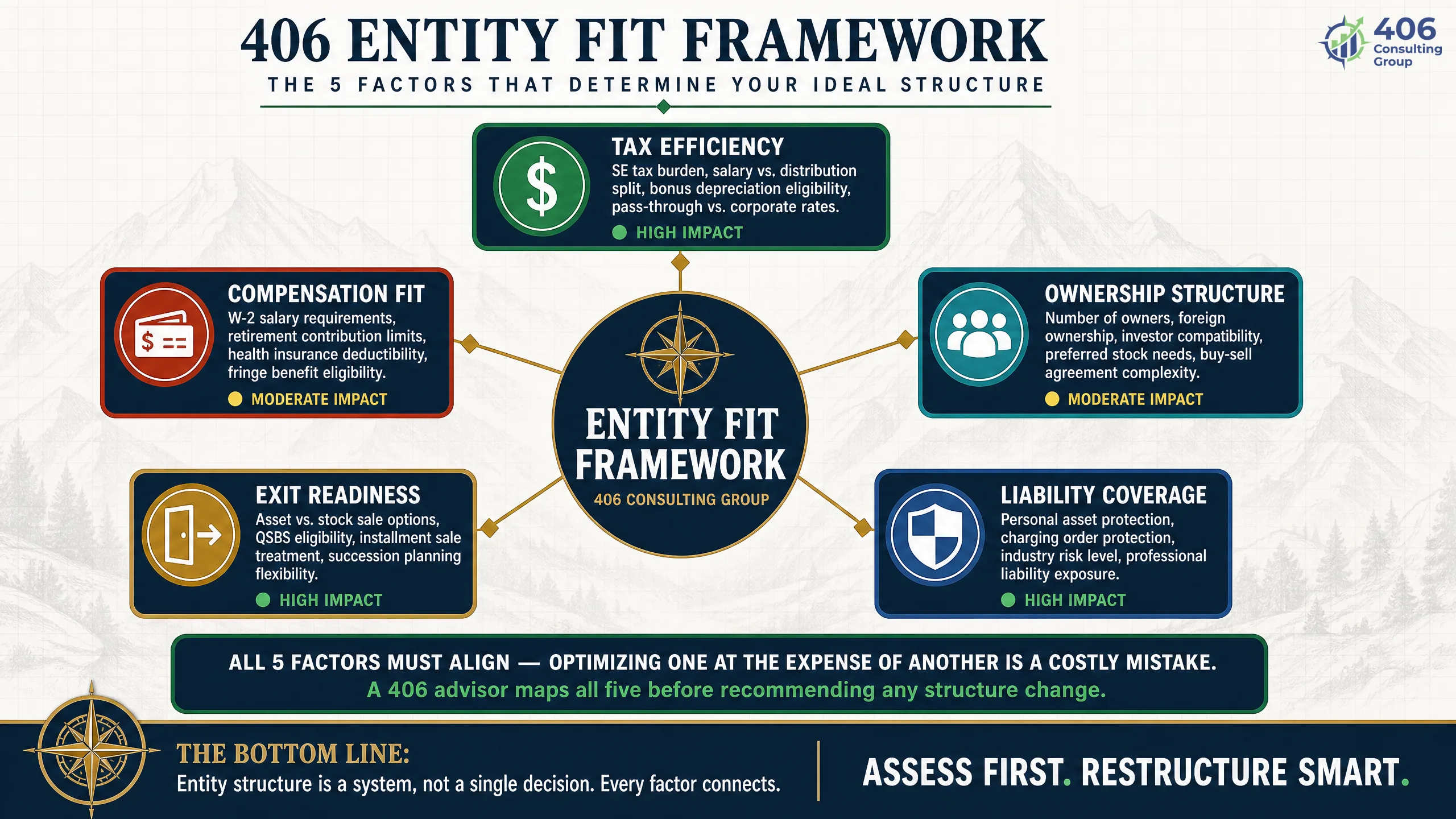

The Entity Fit Framework

The Entity Fit Framework evaluates your current structure across five dimensions. It's not a "which entity is best" exercise — it's a diagnostic. Green means your current structure works in this dimension. Yellow means it's becoming a constraint. Red means it's actively costing you money or creating risk. Three or more yellows or reds in the same business means the structure review is overdue.

Tax Efficiency

Is your current structure minimizing SE tax and maximizing deductions at your current income level?

Ownership Structure

Does your entity accommodate your current and planned ownership — partners, investors, equity compensation?

Liability Coverage

Does your entity provide adequate personal liability protection for your current revenue, headcount, and contract exposure?

Exit Readiness

Is your entity structured in a way that maximizes after-tax exit proceeds for the sale you may want in 3–10 years?

Compensation Fit

Does your entity allow you to structure owner compensation in a way that minimizes SE tax and maximizes retirement contributions?

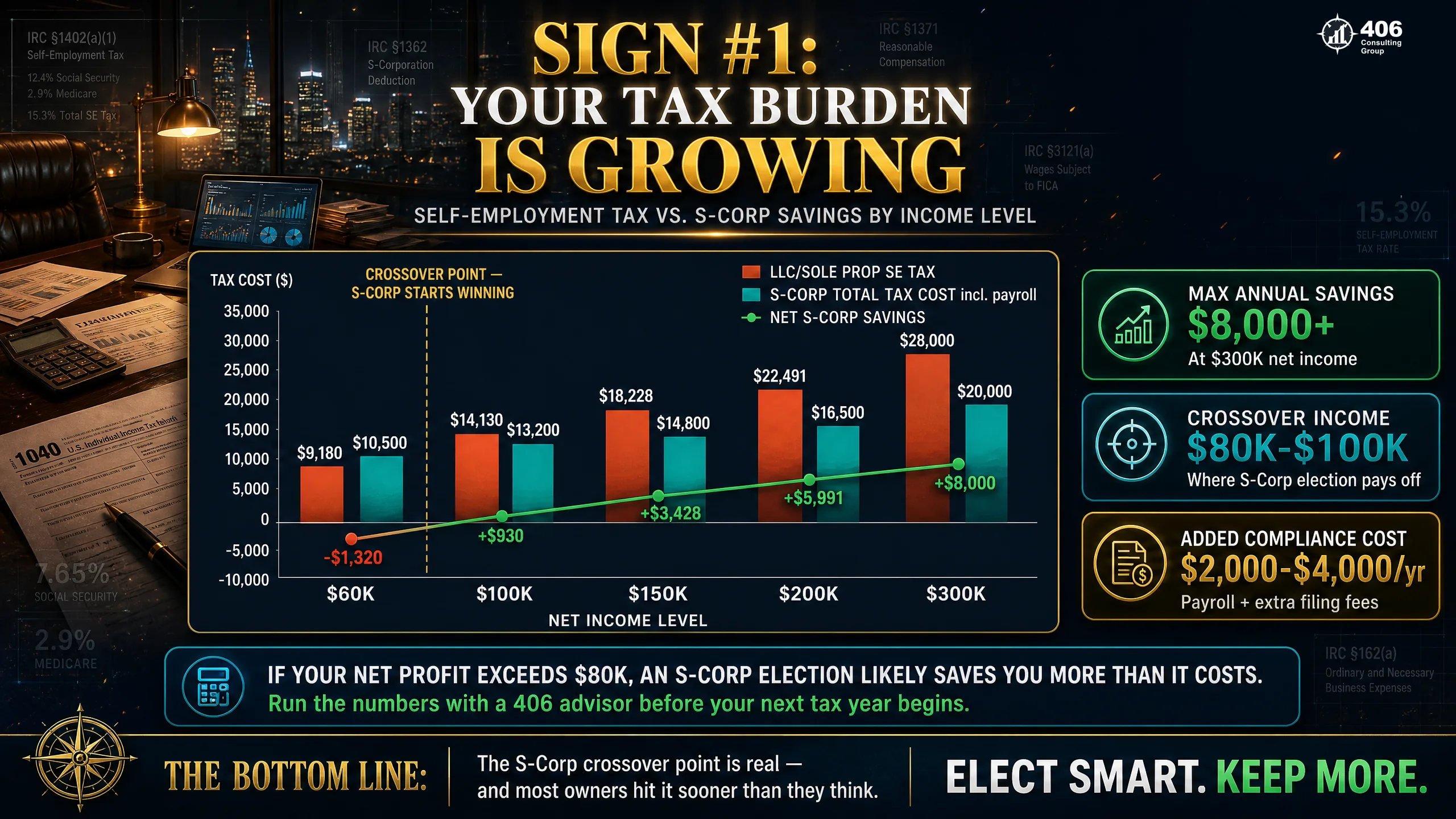

Sign 1: Your Tax Bill Is Growing Faster Than Your Revenue

Self-employment tax is the most expensive tax most LLC owners pay, and the least visible — because it comes packaged with the Schedule SE that most owners don't read carefully. As a sole proprietor or single-member LLC taxed as a disregarded entity, 100% of your net business income is subject to SE tax: 15.3% on the first approximately $176,100 (2025 Social Security wage base; adjusts annually), plus 2.9% Medicare on everything above. At $200,000 net profit, that's roughly $27,000 in SE tax alone — before a single dollar of income tax.

| Net Business Profit | LLC SE Tax (est.) | S-Corp: Salary + Distribution | S-Corp SE Tax (est.) | Annual Savings |

|---|---|---|---|---|

| $60,000 | $8,478 | $45K salary / $15K dist. | $6,358 | $2,120 |

| $100,000 | $14,130 | $60K salary / $40K dist. | $8,478 | $5,652 |

| $150,000 | $21,195 | $75K salary / $75K dist. | $10,598 | $10,597 |

| $200,000 | $27,050 | $90K salary / $110K dist. | $12,713 | $14,337 |

| $300,000 | $32,130 | $110K salary / $190K dist. | $15,533 | $16,597 |

The S-Corp election allows you to split income into two buckets: a W-2 salary (subject to SE tax) and a distribution (not subject to SE tax). The IRS requires the salary to be "reasonable" — meaning it must reflect what you'd pay someone else to do the work you do. An owner doing $200,000 of work can't pay themselves a $20,000 salary and take $180,000 as a distribution. But a reasonable $85,000–$95,000 salary with the remainder as distribution is defensible and produces real tax savings.

The S-Corp Crossover Point

Running S-Corp payroll adds cost: payroll processing ($50–$150/month), additional tax filings, and accounting complexity. Net these costs against the SE tax savings and the S-Corp typically becomes worthwhile at $60,000–$80,000 in net business profit for most Montana businesses. Below that threshold, the savings often don't justify the added compliance cost. Use our S-Corp Savings Calculator to find your specific crossover point.

For a deeper dive on S-Corp tax benefits in Montana, including the Montana-specific pass-through considerations, see our guide on S-Corp tax benefits for Montana businesses.

Sign 2: You're Taking on Investors or Bringing in Partners

The entity structure that works for a solo owner frequently breaks when a second owner enters the picture — and shatters when outside investors come in. S-Corps have strict ownership rules that catch many growing businesses off guard. If you're planning any ownership change, the structure conversation has to happen before the handshake, not after.

S-Corporation

- ›Maximum 100 shareholders

- ›All owners must be US citizens or permanent residents

- ›Only one class of stock — no preferred shares

- ›No corporate or partnership shareholders

- ›IRAs can be shareholders; trusts require specific qualification

Breaks when: foreign investors, institutional investors, preferred equity rounds, or more than 100 owners.

Multi-Member LLC

- ›Unlimited members, any nationality

- ›Flexible economic arrangements (unequal profit/loss splits)

- ›No stock classes — but operating agreement can replicate economics

- ›SE tax exposure for active members

- ›Requires a solid operating agreement

Works for: partners and early investors who can accept SE tax exposure and operating agreement flexibility.

C-Corporation

- ›Unlimited shareholders, any nationality or entity type

- ›Multiple classes of stock (common, preferred)

- ›Stock options and warrants (ISOs, NSOs)

- ›Institutional investor compatible

- ›Required for most venture capital deals

Required when: foreign investors, institutional/PE capital, preferred equity rounds, or QSBS planning.

The S-Corp That Accidentally Terminated Its Election

One of the most expensive entity mistakes we see: a business with S-Corp status that transferred shares to a foreign national, a corporation, or an ineligible trust — immediately and retroactively terminating the S-Corp election. The IRS doesn't give you a warning. The election terminates on the date of the ineligible transfer, and you're suddenly a C-Corp from that date forward, with all the tax implications that come with it. Before any ownership transfer, confirm eligibility with a tax advisor.

Sign 3: Your Liability Exposure Has Outgrown Your Current Protection

The liability question is simple in principle: are your personal assets exposed if something goes wrong in the business? The answer depends on both your entity structure and how well you maintain it. A sole proprietor has zero separation between business and personal — one judgment can reach everything you own. An LLC provides meaningful protection if maintained correctly. An S-Corp or C-Corp provides additional protection through corporate formality requirements that, when followed, create a stronger legal barrier.

| Entity | Personal Liability Shield | Montana-Specific Strength | Key Risk |

|---|---|---|---|

| Sole Proprietor | None | N/A | All personal assets exposed to any business claim |

| Single-Member LLC | Charging order protection | Strong — Montana LLC Act is favorable | Some courts have pierced single-member LLCs more readily than multi-member |

| Multi-Member LLC | Charging order protection | Strong — harder for creditors to reach | Still requires corporate formality maintenance to avoid piercing |

| S-Corporation | Corporate veil | Strong when formalities maintained | Veil can be pierced for commingling funds, failing to follow corporate formalities |

| C-Corporation | Corporate veil (strongest) | Strong | Same piercing risk as S-Corp; personal guarantees on loans bypass it entirely |

The liability trigger for reviewing your structure: when your annual revenue, contract values, or headcount crosses a threshold where a single lawsuit or liability event could be financially catastrophic. For most Montana businesses, that conversation happens around $500,000 in revenue or 5+ employees — not because those are magic numbers, but because that's when the exposure typically becomes real enough to justify the structure.

The Formality Requirement Most LLC Owners Skip

A liability shield only holds if you maintain it. Commingling personal and business funds, failing to keep a separate business bank account, signing contracts personally instead of in the entity's name, and failing to maintain basic corporate records are all grounds for a court to pierce the veil and hold you personally liable. The entity structure is only as strong as the discipline you apply to maintaining it.

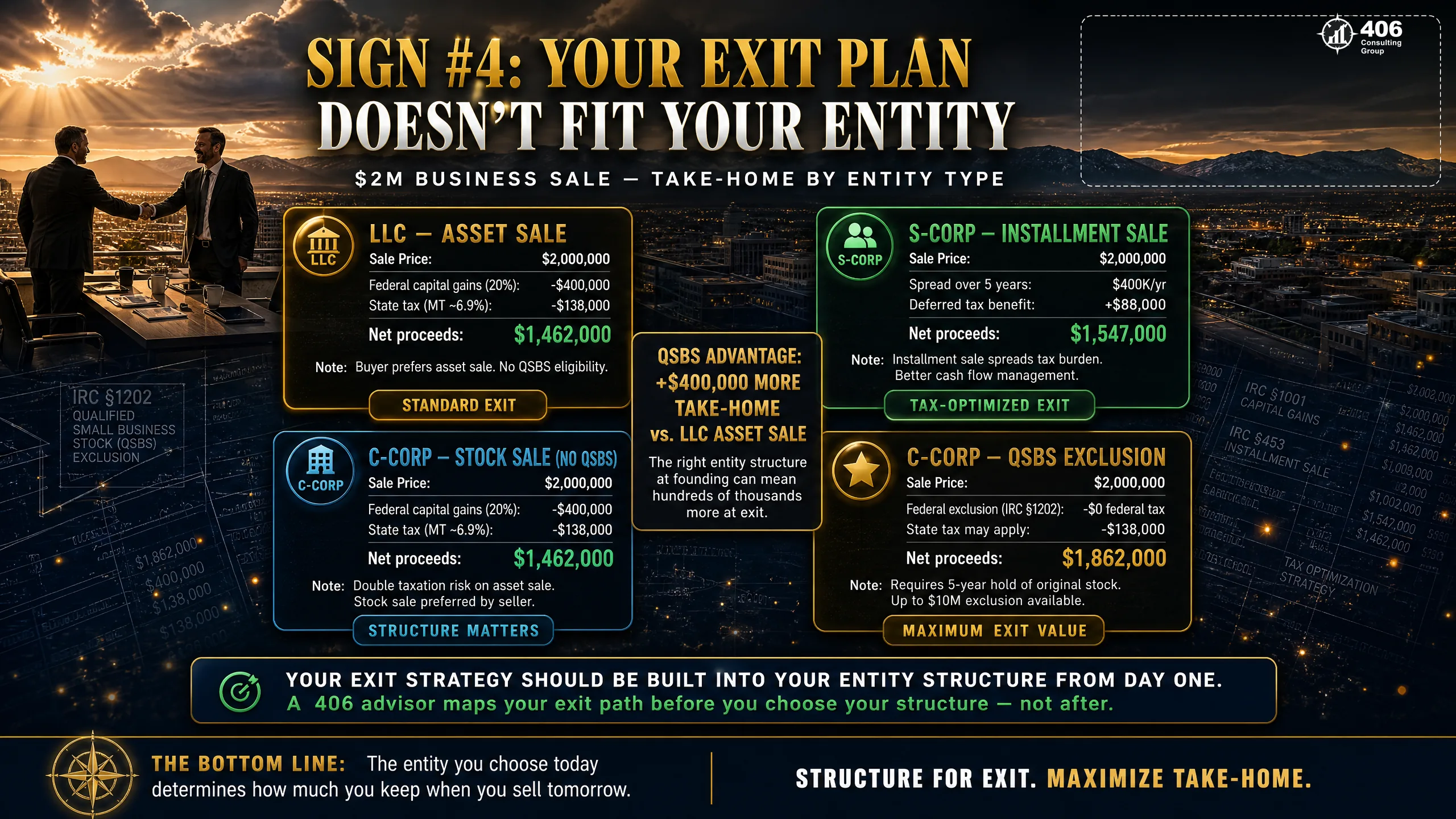

Sign 4: You're Preparing to Sell or Bring in Outside Capital

Entity structure has a direct, quantifiable impact on what you take home when you sell — and on whether institutional buyers will look at your deal at all. The tax treatment of a business sale differs materially by entity type, and the QSBS exclusion available only to C-Corp shareholders can represent millions of dollars in tax-free gain for the right business at the right stage.

Asset Sale vs. Stock Sale — Why It Matters

Most small business sales are structured as asset sales (buyer acquires assets, not the entity). For the seller, this typically means ordinary income tax on equipment and inventory (Section 1245 recapture) and capital gains on goodwill. For an S-Corp or LLC, this income passes through to the owner's personal return. For a C-Corp, the corporation pays tax on the asset sale — then the owner pays again on the distribution. This double taxation is the primary reason most small businesses should avoid C-Corp status unless QSBS or venture capital requires it.

Qualified Small Business Stock (QSBS) — C-Corp Only

IRC Section 1202 allows shareholders of qualifying C-Corps to exclude up to $10 million (or 10× adjusted basis, whichever is greater) in capital gains from federal tax when selling stock held for 5+ years. This is one of the most powerful tax incentives in the code — but it's available only to C-Corp shareholders. An LLC or S-Corp owner cannot access QSBS. For businesses that could plausibly sell for $5M–$30M and are in their early stages, the QSBS strategy alone can justify C-Corp structure.

Institutional and PE Buyer Requirements

Private equity firms and institutional buyers overwhelmingly prefer to acquire C-Corps or to convert the target to a C-Corp before close. S-Corp stock has restrictions on who can own it — which eliminates most institutional buyers by definition. If your exit strategy includes PE or a strategic acquirer with a C-Corp structure, the entity conversion conversation should happen 3–5 years before the anticipated sale, not during the letter-of-intent stage.

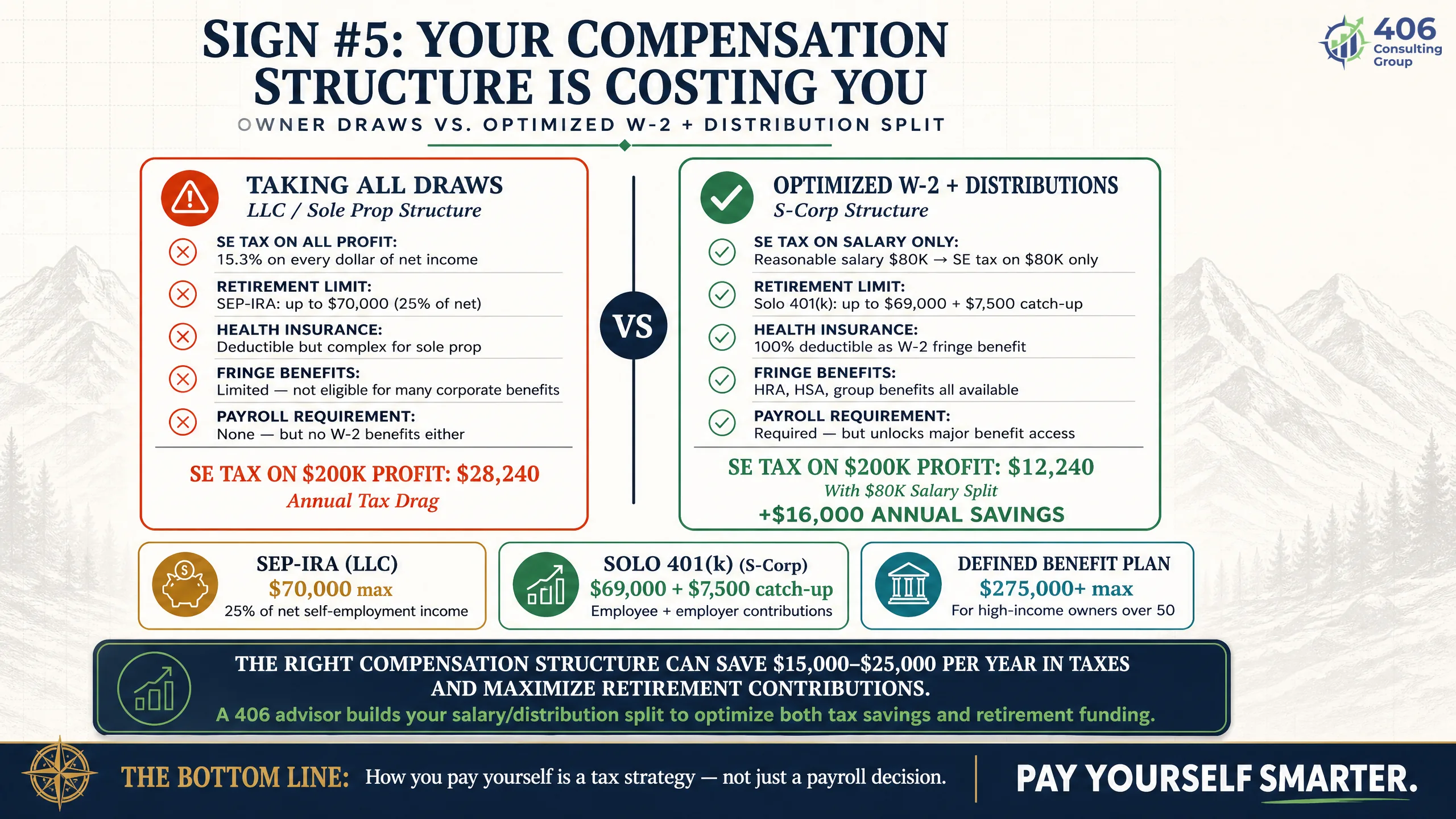

Sign 5: Your Compensation Structure No Longer Makes Sense

How you pay yourself as a business owner is both a tax question and a retirement planning question — and both answers change significantly when you move from a disregarded-entity LLC to an S-Corp. The most common sign that compensation structure has become a problem: an owner doing $150,000 worth of work who is taking all profit as a draw, paying SE tax on every dollar, and making minimal retirement contributions because the structure doesn't support better options.

Single-Member LLC — All Draws

S-Corp — W-2 + Distribution

The Retirement Contribution Multiplier

S-Corp owners can contribute to a Solo 401(k) as both employee ($23,500 in 2026; $31,000 if 50+) and employer (up to 25% of W-2 salary) — for a potential combined contribution of $69,000+ annually. A single-member LLC owner's SEP-IRA contribution is capped at 20% of net self-employment income. On $85,000 in W-2 salary, the S-Corp owner can contribute significantly more to tax-deferred retirement accounts — an advantage that compounds dramatically over a 15–20 year accumulation period.

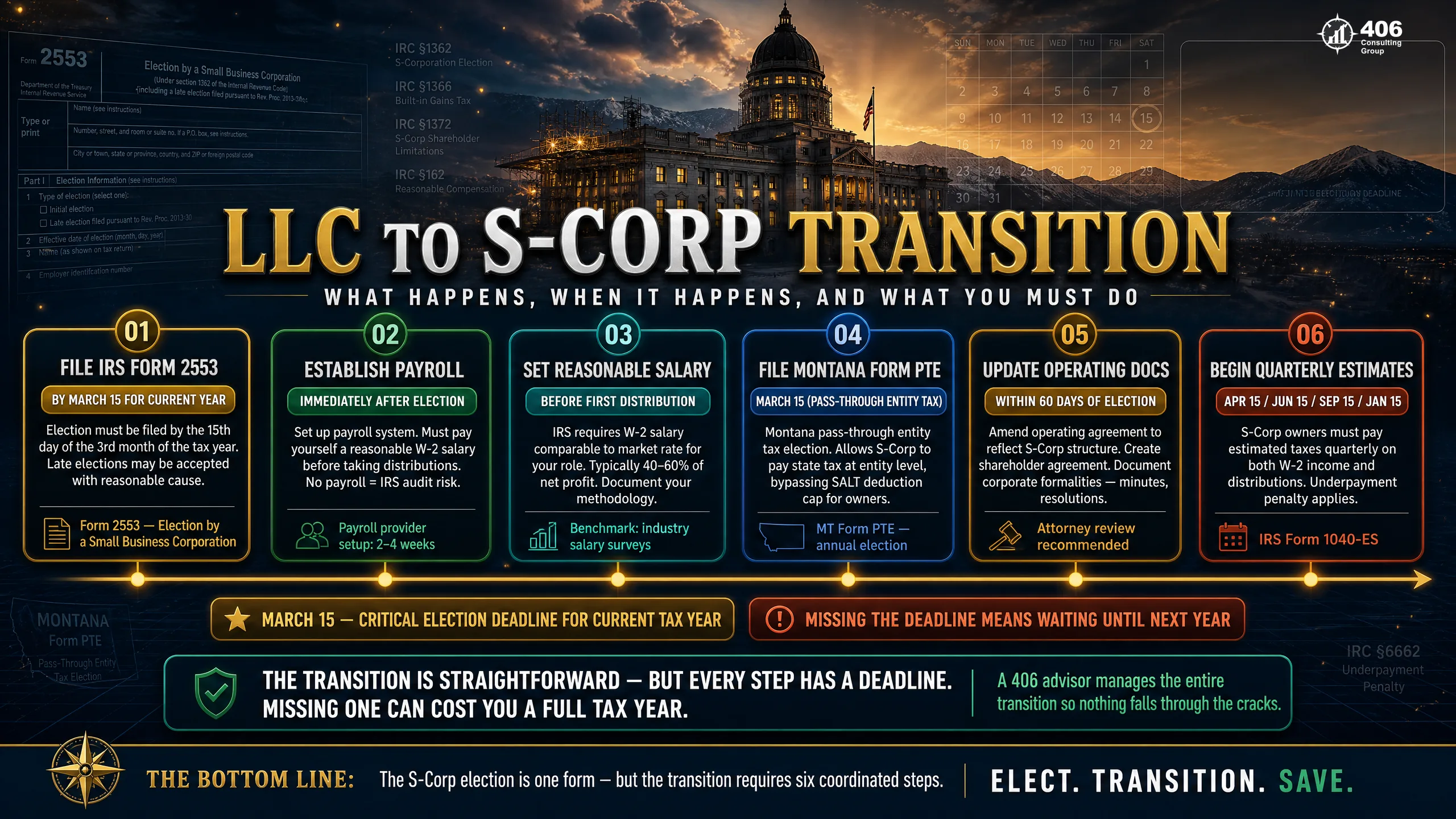

The Most Common Transition: LLC to S-Corp

The LLC-to-S-Corp election is the most common entity structure change for growing Montana businesses — and it's significantly less complicated than most owners expect. You don't form a new corporation, reopen bank accounts, or renegotiate contracts. You file IRS Form 2553, establish payroll, and set a reasonable salary. The legal entity stays the same; the tax treatment changes.

File IRS Form 2553

The S-Corp election form — available at IRS.gov/form2553. Must be filed by March 15 for the election to apply to the current tax year (or within 75 days of the start of the tax year). Late elections are possible with reasonable cause — but require additional IRS approval.

Establish Payroll

As an S-Corp owner-employee, you must be on payroll. Set up payroll processing (Gusto, ADP, or similar), establish your EIN for payroll purposes, and begin running a W-2 salary. This is the most operationally significant change.

Set Reasonable Salary

Work with your tax advisor to document what a reasonable salary is for your role. The IRS scrutinizes unusually low salaries. Bureau of Labor Statistics data, industry benchmarks, and the complexity of your work are all inputs. The salary doesn't need to be high — it needs to be defensible.

Update Montana Form PTE

Montana S-Corps file Form PTE (pass-through entity return) due March 15. You'll also need to make estimated tax payments via Montana Form EST. Update your Montana business registration to reflect the S-Corp tax treatment.

Update Accounting and Bookkeeping

Your chart of accounts needs to separate owner W-2 payroll from distributions. QuickBooks or Xero must be configured to track payroll taxes, employer contributions, and distributions separately. This is where clean books become critical — not optional.

File Two Returns in Year One (Sometimes)

If your election is mid-year, you may need to file a short-period return for the pre-election period and a standard S-Corp return for the post-election period. Your tax advisor will determine whether a calendar-year election avoids this complexity.

Cost to Make the Transition

Professional help to set up the S-Corp election, establish payroll, and reconfigure accounting typically runs $500–$2,000 depending on complexity. Ongoing additional cost: payroll processing ($50–$150/month) and the additional tax return (Form 1120S, ~$500–$1,500/year more than a Schedule C). Against annual SE tax savings of $8,000–$20,000+ for most businesses at the crossover point, the economics are clear. Our tax planning services include S-Corp election setup and the first-year transition support that most businesses need.

When C-Corp Makes Sense — and When It Doesn't

C-Corp status is the right answer for a specific set of businesses. It's the wrong answer for most Montana small businesses — and converting to a C-Corp for the wrong reasons creates tax complexity that is expensive and slow to unwind.

C-Corp Makes Sense When:

- ✓QSBS strategy is part of the exit plan — you expect a $5M+ exit and want the Section 1202 exclusion

- ✓Venture capital or institutional PE investment requires C-Corp structure

- ✓You need preferred stock or multiple stock classes for equity compensation or investor terms

- ✓International shareholders or corporate shareholders need to own equity

- ✓Employee stock option programs (ISOs) are part of the compensation strategy

- ✓You plan to retain significant earnings in the business at the 21% federal corporate rate vs. passing through at individual rates

C-Corp Is Wrong When:

- ✗You intend to take profits out of the business annually — double taxation on dividends makes this expensive

- ✗You're a profitable services business with no institutional capital plans

- ✗Your exit is a simple sale to an individual or small strategic buyer — asset sale structure makes C-Corp status irrelevant or harmful

- ✗You want to pass losses through to your personal return — C-Corp losses cannot offset personal income

- ✗Your accountant/attorney isn't experienced with C-Corp compliance — the added complexity is real

Montana-Specific Entity Considerations

Montana has entity-specific rules and tax rates that differ from the national picture. These don't change the fundamental analysis but are essential inputs for Montana business owners comparing structures.

Montana LLC Act — Charging Order Protection

Montana's LLC statutes provide strong charging order protection — a creditor who wins a judgment against an LLC member can only obtain a charging order against that member's distributions, not seize the member's LLC interest or force a liquidation. This is meaningfully stronger protection than some states. Multi-member LLCs in Montana have historically received even stronger protection than single-member LLCs.

Montana Form PTE and Estimated Tax

S-Corps and multi-member LLCs file Montana Form PTE (pass-through entity return) due March 15 (with extensions to September 15). Estimated tax payments are required quarterly via Form EST. When you convert an LLC to S-Corp tax treatment, you gain the PTE filing obligation if you didn't already have it. Budget for this in your professional services costs.

Montana Tax Rates by Entity

Montana individual income tax: maximum rate 5.9% on income above approximately $20,500. Montana corporate income tax: 6.75% flat rate on net income. For an S-Corp owner in the highest Montana bracket, all business income passes through at the individual rate (5.9%). A C-Corp pays 6.75% at the entity level — then the owner pays again on distributions. This reinforces the case against C-Corp for Montana businesses that intend to distribute profits.

Annual Report and Registration

Montana LLCs owe a $20 annual report filed with the Secretary of State. Montana corporations owe $15. Each entity must maintain a registered agent in Montana. If you operate under a separate entity per location, multiply these requirements by the number of entities. See MTrevenue.gov for Montana business filing details.

The Cost of Waiting Too Long

Delaying the entity structure review isn't neutral — it's expensive. The costs compound annually, and some consequences (like missed QSBS qualification periods or retroactively terminated S-Corp elections) can't be unwound after the fact. Here's what the delay actually costs in concrete terms.

| Scenario | Annual Cost of Delay | 3-Year Cost | Recoverable? |

|---|---|---|---|

| LLC at $150K net — SE tax over S-Corp | $10,597 | $31,791 | No — tax paid is gone |

| LLC at $200K net — SE tax over S-Corp | $14,337 | $43,011 | No — tax paid is gone |

| Missing S-Corp election window | 1 full year of excess SE tax | Depends on income | Partial — late elections available with IRS approval |

| Missing QSBS 5-year hold window | N/A — one-time opportunity | Up to $10M exclusion lost | No — hold period must begin before the clock starts |

| Ineligible S-Corp shareholder terminating election | Retroactive C-Corp treatment | Full back taxes + penalties | IRS relief available but costly and not guaranteed |

Timing the Switch: When in the Year to Make the Change

The cleanest time to change entity structure is January 1 — the start of a new tax year. This avoids a split-year return and gives you a clean slate for payroll, bookkeeping, and tax reporting. In practice, most businesses don't discover the need mid-year and the March 15 deadline matters more than the calendar year.

Cleanest option. File Form 2553 in December or early January. Full year under the new structure. No split-year return complexity. Preferred for most transitions.

S-Corp election deadline for the current tax year. File Form 2553 by March 15 and the election applies retroactively to January 1 of that year. This is the effective deadline for the current year.

If you miss March 15, you can elect S-Corp treatment starting mid-year with a short period return. Or apply for late-election relief (Revenue Procedure 2013-30) which the IRS often approves for reasonable cause.

If the entity structure review is happening now and it's past March 15, don't wait until next January — get the analysis done, make the decision, and implement the transition for the beginning of the next tax year with a clean plan. Our CFO advisory services include entity structure analysis and the transition planning that ensures the switch happens cleanly, on schedule, and with the right professional support. Use our LLC vs. S-Corp comparison tool to model the numbers for your specific situation.

Frequently Asked Questions

At what income level does an S-Corp election make sense for a Montana LLC?

For most Montana businesses, the S-Corp election becomes financially advantageous at $60,000–$80,000 in annual net business profit, after accounting for the added cost of payroll processing and the additional S-Corp tax return. Below that threshold, the SE tax savings are often smaller than the added compliance cost. Above $100,000 in net profit, the savings are nearly always significant — typically $8,000–$20,000 or more annually depending on what a reasonable salary is for your role.

Can I keep my LLC and still elect S-Corp tax treatment?

Yes — this is the most common approach for Montana small businesses. You keep your existing LLC legal structure (bank accounts, contracts, branding, and state registration stay the same) and file IRS Form 2553 to elect S-Corp taxation. The LLC remains the legal entity; the IRS simply taxes it under S-Corp rules. You don't need to form a separate corporation.

What is a reasonable salary for an S-Corp owner?

The IRS requires S-Corp owner-employees to pay themselves a salary that reflects what you'd pay a third party to do the same work. Factors: industry salary data (Bureau of Labor Statistics, industry surveys), the complexity of your role, and the total revenue of the business. As a practical guide: if the market salary for your role is $80,000–$120,000, your S-Corp salary should be in that range. Paying yourself $30,000 when you're doing $300,000 of revenue-generating work is the type of arrangement the IRS audits.

What happens if an ineligible person becomes an S-Corp shareholder?

The S-Corp election terminates immediately and retroactively on the date the ineligible shareholder acquired shares. This means the business is treated as a C-Corp from that date forward — which triggers corporate-level tax on income that was being passed through. The IRS does have relief provisions for inadvertent terminations, but they require prompt action, IRS approval, and corrective steps. Prevention is far cheaper than cure: verify eligibility before any ownership transfer.

How does Montana treat S-Corp income differently from the federal government?

Montana conforms to the federal S-Corp pass-through treatment — income passes through to shareholders and is taxed at the individual level. Montana S-Corps file Form PTE (pass-through entity return) due March 15, and shareholders make estimated tax payments via Form EST. Montana's individual income tax tops out at 5.9%, compared to the 6.75% corporate rate — which reinforces the pass-through advantage for Montana businesses that intend to distribute profits annually rather than accumulate them in the entity.

What's the deadline to elect S-Corp status for the current year?

March 15 is the IRS deadline to file Form 2553 for the election to apply retroactively to January 1 of the current tax year. If you miss this deadline, you can apply for a late election under Revenue Procedure 2013-30, which the IRS often approves when there's reasonable cause and the business has otherwise been filing as if it were an S-Corp. If the late election isn't approved, the election takes effect January 1 of the following year.

Entity Structure Review

Not Sure If Your Structure Still Fits?

406 Consulting Group runs the Entity Fit Framework analysis for Montana businesses at every stage — from the first S-Corp election conversation to multi-entity exit planning. We'll tell you what the change is worth in real dollars and handle the transition from election to payroll to updated bookkeeping.

Entity Fit Framework

3 or more red flags = act now

Tax bill growing faster than revenue

SE tax on all LLC profit — S-Corp election saves $8K–$20K+/yr

Taking on investors or partners

S-Corp restrictions break with institutional investors

Liability exposure outgrown structure

Revenue and headcount need stronger corporate protection

Preparing to sell or raise capital

Entity type affects exit proceeds and buyer compatibility

Compensation structure no longer works

All draws = excess SE tax + limited retirement options

Key Dates

Our Services

Related Guides