When to Upgrade from

Bookkeeping to a Controller

Your bookkeeper is doing everything right. So why did your tax bill blindside you? Why did you nearly miss payroll? Why can't you tell a banker which of your service lines is actually making money? This guide explains the infrastructure gap — and what it costs to stay in it.

The bookkeeper vs. controller question hits most Montana business owners somewhere around $1 million in revenue — and most get the wrong answer because nobody explains what a controller actually does.

Mike owns Cascade Mechanical, an HVAC and plumbing company in Kalispell. He's been in business nine years, has eight employees, and did $1.8 million in revenue last year. He has a bookkeeper — she's reliable, has been with him for four years, and he trusts her completely.

And yet, last March, his CPA called to tell him he owed $34,000 in taxes. He had no idea. Two months before that, he nearly missed payroll because $180,000 in receivables was sitting uncollected and nobody had flagged it. He's never been able to tell a banker — or himself — exactly which of his three service lines is actually making money.

Mike doesn't have a bookkeeping problem. He has an infrastructure problem. His bookkeeper is doing exactly what a bookkeeper is supposed to do. The issue is that his business has grown past what bookkeeping alone can manage — and nobody told him there was a next step.

This guide explains what that next step is, when you need it, and what it costs — with real numbers so you can decide whether Mike's situation sounds familiar.

By Jason Anderson — Co-Founder, 406 Consulting Group. Background in large-scale operational finance at BP before building financial infrastructure for Montana SMBs.

Quick Answer: Do You Need a Controller?

- →Under $1M revenue: A good bookkeeper is probably enough. Focus on clean records and a reliable CPA.

- →$1M–$3M revenue: You likely need a controller and may not know it yet. The 7 signs below will tell you.

- →Above $3M: You almost certainly need a controller. The question is fractional or full-time.

- →The cost of waiting: For a $1.8M business like Cascade Mechanical, the financial gaps a controller would close typically represent $50,000–$80,000 per year in recoverable value.

Table of Contents

Two Different Jobs That Sound Like the Same Job

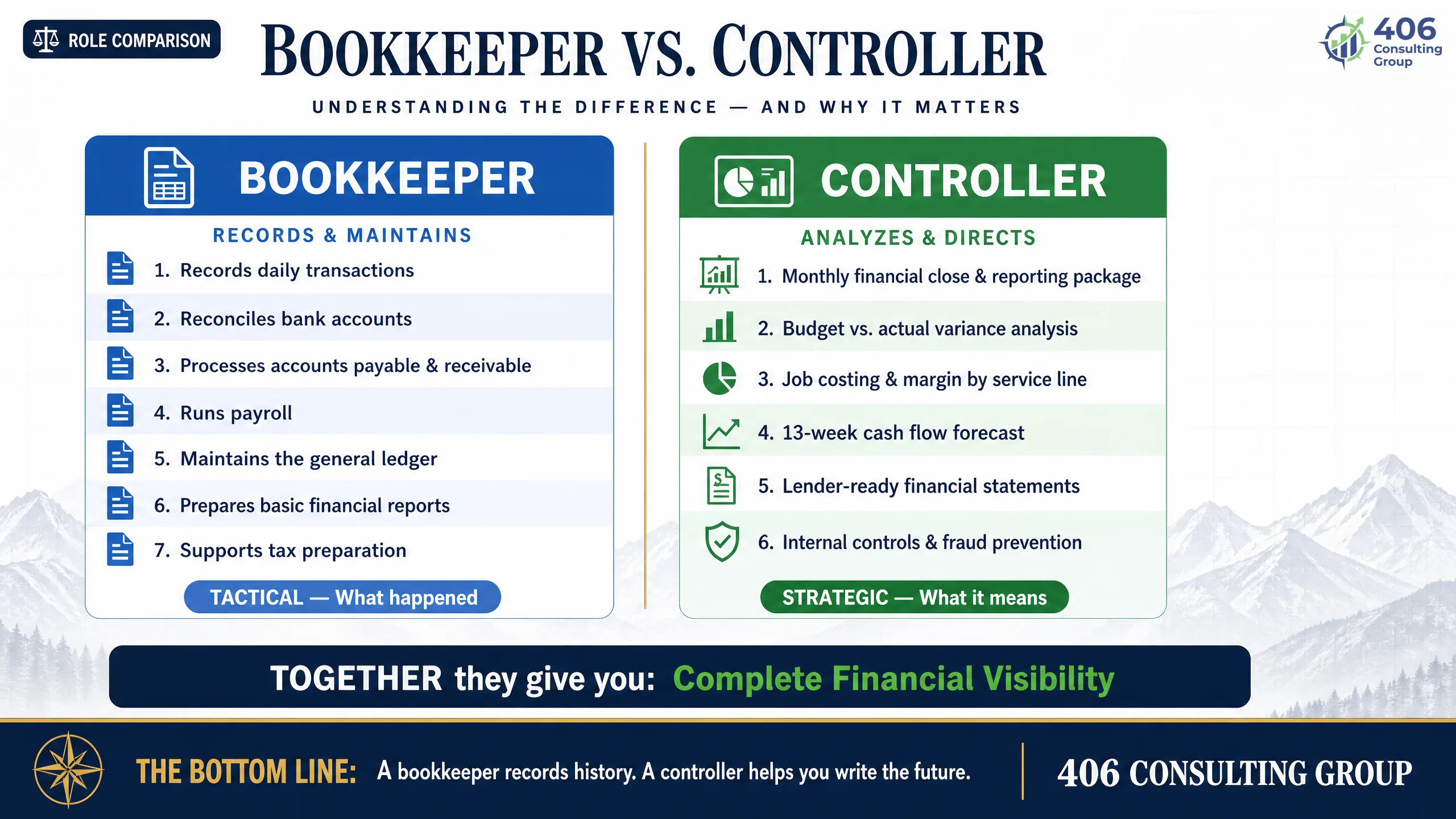

Here is the simplest way to understand the difference: a bookkeeper records what already happened. A controller manages what is happening and makes sure you can act on it.

Think of it like a restaurant. The bookkeeper is the person who records every meal that was sold, every ingredient that was purchased, and every server who was paid. At the end of the month, the records are accurate. But no one has told you that your food cost percentage jumped from 28% to 34% in October — and that if you don't fix it, you'll be in trouble by January. That's the controller's job.

The simplest version:

Bookkeeper

“Here's what happened to your money last month.”

Controller

“Here's what's happening, here's what it means, and here's what you need to do about it.”

Both roles are necessary. The bookkeeper vs. controller distinction isn't about one being better — it's about what a growing business needs at different stages. A bookkeeper is the right answer up to a point. A controller is the right answer after that. The mistake is not knowing where the line is.

This is not a criticism of your bookkeeper.

A skilled bookkeeper who is doing exactly their job is still not a controller. These are different roles with different training, different responsibilities, and different outcomes. Expecting a bookkeeper to do controller-level work is like expecting your office manager to also be your operations director. The skills don't overlap the way most people assume.

What a Bookkeeper Does (and Doesn't Do)

A bookkeeper's job is to keep accurate records of your financial transactions. In a well-run engagement, that means:

What a bookkeeper IS responsible for

- Recording all income and expense transactions

- Categorizing expenses to the correct accounts

- Reconciling bank and credit card accounts monthly

- Processing accounts payable (paying bills)

- Processing accounts receivable (invoicing customers)

- Running payroll or coordinating with a payroll service

- Providing your CPA with organized records at tax time

What a bookkeeper is NOT typically responsible for

- —Analyzing whether your margins are healthy or eroding

- —Telling you which jobs or service lines are profitable

- —Producing a monthly report you can actually make decisions from

- —Tracking budget vs. actual and explaining the variance

- —Forecasting your cash position 8–13 weeks out

- —Preparing lender-ready financial packages

- —Catching errors or fraud in the accounting system

- —Advising on tax strategy or entity structure

Cascade Mechanical — What Mike's Bookkeeper Does

Mike's bookkeeper processes all of Cascade Mechanical's transactions in QuickBooks. Every invoice goes in. Every bill gets paid. Payroll runs on time. Bank accounts reconcile every month. She is good at her job. What she doesn't do: tell Mike that his commercial service contracts are running a 6% margin while his residential HVAC installs are running 22% — and that if he knew that, he'd restructure how he quotes commercial work immediately. That analysis doesn't happen because it's not in her job description. It's not what she was hired for.

What a Controller Actually Does

A controller owns the financial function. Not just the records — the entire financial picture. Here is what that looks like in a real business like Cascade Mechanical:

Monthly close and financial package

By the 15th of every month, Mike gets a 4-page report: income statement with prior-month comparison, balance sheet, cash flow summary, and a one-page narrative explaining what changed and why. Not just numbers — context. 'Commercial service revenue was down $18,000 vs. last month due to two delayed contract starts. Residential installs were up 14%. Net effect: margin improved by 1.2 points despite lower top-line revenue.'

Budget vs. actual tracking

At the start of the year, Mike and his controller build a simple budget: what Cascade Mechanical expects to earn and spend each month. Every month, the controller compares actual results to the budget and flags anything over 10% off. Mike knows immediately if something is drifting — not in March when the CPA calls, but in November when there's still time to do something about it.

Job costing and margin analysis

Cascade Mechanical runs three service lines: residential HVAC, commercial HVAC, and plumbing. The controller tracks the margin on each one. When commercial contracts start running thin, it shows up in the monthly report — with the specific jobs that dragged the margin down and what the labor or materials issue was.

Cash flow forecasting

A 13-week rolling cash flow forecast shows Mike exactly what his bank account will look like week by week, based on invoices outstanding, bills due, and payroll schedule. The $180,000 receivables situation that almost caused a payroll crisis? A controller catches that 6 weeks out — not the day before payroll is due.

Lender-ready financials

When Mike is ready to buy a second service truck or expand his team, his controller maintains the financial package a lender needs: organized P&L, balance sheet, AR aging, and debt schedule — current, reconciled, and ready to hand to a banker on two days' notice.

Internal controls

A controller sets up basic checkpoints so the bookkeeper's work gets reviewed. Invoices are compared to purchase orders. Bank reconciliations are reviewed by someone other than the person who did them. No single person handles both the money and the records. For an 8-person business, this doesn't need to be complex — but it does need to exist.

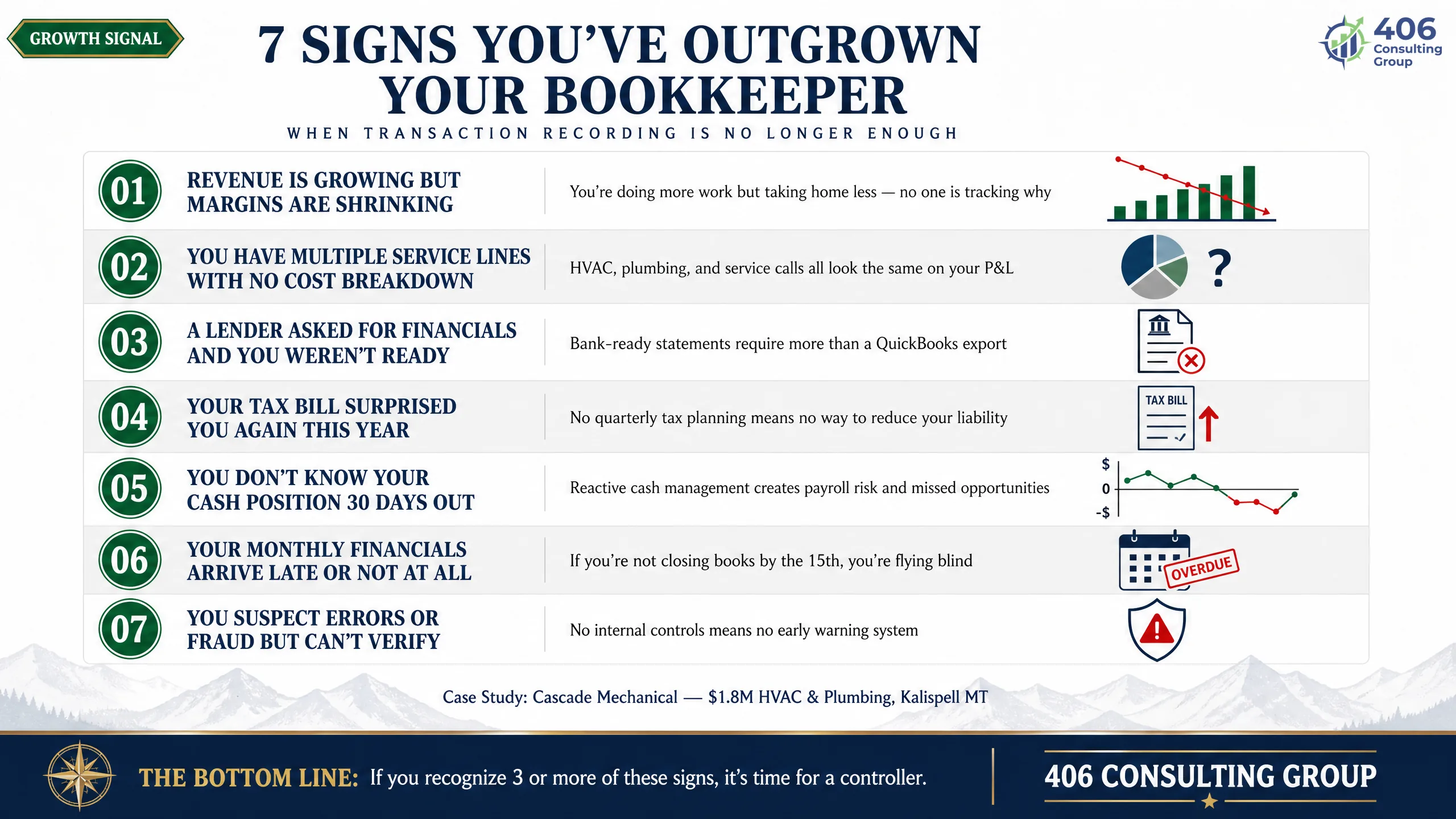

7 Signs When to Hire a Controller

Most business owners don't upgrade proactively — they upgrade after something goes wrong. The goal of this section is to help you recognize the signs before that happens. Read each one and ask honestly: does this sound like my business?

Your revenue crossed $1M–$1.5M and the financial picture is getting less clear, not more

Cascade Mechanical — Mike's situation

Cascade Mechanical at $800K was actually easier for Mike to understand than at $1.8M. Fewer jobs. Simpler cash flow. Now he has three service lines, eight employees, and equipment on two payment plans — and he feels less in control of the numbers than he did at half the size.

This is the most common sign — and the most overlooked. Growth adds complexity faster than most owners expect. A bookkeeper records the complexity. A controller helps you understand and manage it.

You have multiple revenue streams and you don't know which one is actually profitable

Cascade Mechanical — Mike's situation

Mike knows Cascade Mechanical made money last year. He does not know that his commercial HVAC contracts ran a 6% net margin while residential installs ran 22%. He's been bidding commercial work at the same markup as residential, which means he's been growing his lowest-margin line fastest.

If you can't tell your most profitable service, product line, or customer type — by specific dollar margin, not gut feel — you're flying without instruments. A controller builds the job costing structure that gives you this clarity.

You're planning a commercial loan and your books aren't lender-ready

Cascade Mechanical — Mike's situation

Mike wants to finance a second service truck — $65,000. His banker asked for a current P&L and balance sheet. Mike called his bookkeeper. She sent over a QuickBooks report three days later. It had five uncategorized transactions, two accounts that hadn't been reconciled since August, and no prior-year comparison. The banker asked for a resubmission.

Lenders don't read QuickBooks reports — they read organized, reconciled financial statements that tell a coherent story. A controller maintains those month by month so they're available on request. See our <Link href='/articles/sba-loan-application-what-lenders-want-to-see' className='text-emerald-700 underline font-semibold'>full guide on what lenders actually want to see</Link>.

Your tax return consistently surprises you

Cascade Mechanical — Mike's situation

Mike knew he had a good year. He did not know he owed $34,000 until his CPA called in March. At that point, all the money he would have put aside had already been spent — on equipment, on bonuses, on two trucks he bought in December thinking he had the cash.

A CPA's job is to file an accurate return, not to tell you month-by-month what you're on track to owe. A controller tracks your tax position throughout the year and gives you enough warning to plan around it — or to make smart purchases at the right time.

You've had a cash flow crisis you didn't see coming

Cascade Mechanical — Mike's situation

Mike has $180,000 in outstanding invoices right now. One large commercial customer is 67 days past due. He nearly missed payroll last week. His bookkeeper knows the invoices are outstanding — she sent the statements. But nobody flagged the risk six weeks ago when there was still time to push harder on collections or arrange a line of credit.

Cash crises almost always come with advance warning — if someone is watching the right numbers. A controller runs a 13-week cash forecast and escalates before the crisis, not during it.

You can't produce a current P&L or balance sheet on demand

Cascade Mechanical — Mike's situation

A banker, a potential business partner, or an equipment leasing company asks Mike for financials. He calls his bookkeeper. She needs two to three days to pull the report together and clean it up. Sometimes it's accurate. Sometimes there are issues she notices while preparing it that she needs to fix first.

A business with a functioning controller has lender-ready financials available within 24 hours at any point in the month. They're maintained as a byproduct of the monthly close process — not assembled on request.

You have employees but no real internal controls

Cascade Mechanical — Mike's situation

At Cascade Mechanical, Mike's bookkeeper processes vendor invoices, approves payments, and reconciles the bank account — all three. Nobody reviews her work before it's done. Mike trusts her completely, and she has earned that trust. But if she made an error — or if someone inside the business was inflating invoices from a fake vendor — nobody would catch it.

Internal controls aren't about distrust — they're about protection. A review layer protects the bookkeeper from errors, protects the business from fraud, and protects the owner from surprises. A controller builds and maintains that review layer.

The Real Cost of Staying at the Bookkeeping Level Too Long

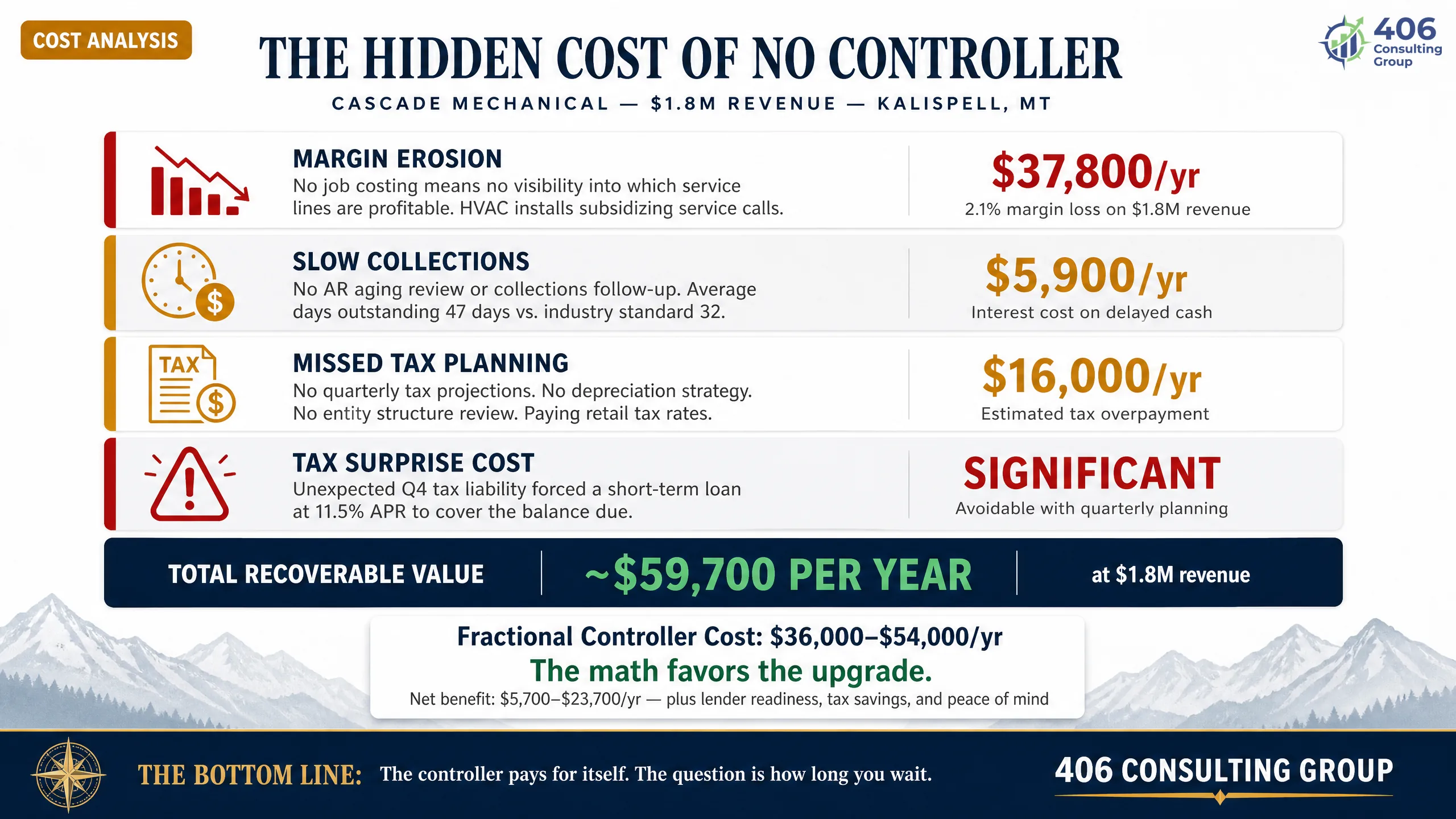

The cost of not having a controller isn't a line item on your P&L. It's invisible — which is exactly why so many business owners don't see it until after the fact. Here is what it actually costs Cascade Mechanical each year to operate without one.

Margin erosion from no job costing

$37,800/yearMike's commercial contracts run 6% margin. His residential work runs 22%. He doesn't know this, so he bids commercial work at the same rate. Last year, Cascade Mechanical did $420,000 in commercial revenue at 6% margin — that's $25,200 in profit. If that work had been priced to run 15% margin, it would have generated $63,000. The difference: $37,800 left on the table.

Cash flow cost — slow collections

$5,900/yearCascade Mechanical averages 52 days to collect on invoices. Industry standard for a trade contractor is closer to 35 days. On $1.8M in revenue, that 17-day gap means roughly $84,000 is trapped in receivables at any given time — money Mike has earned but can't use. At 7% cost of capital (line of credit rate), that's about $5,900 per year in financing cost for money that's already his.

Tax planning missed

$16,000/yearMike's net profit last year was $216,000. He doesn't have an S-Corp election — he's still taxed as a single-member LLC. Every dollar of that profit is subject to self-employment tax at 15.3% on the first portion. An S-Corp election with proper owner compensation would have saved him approximately $14,000–$18,000 in SE tax. His CPA could have flagged this anytime. Without a controller building that relationship between monthly results and tax strategy, nobody did.

The $34,000 tax surprise — cost of no quarterly planning

Hard to quantify — significantMike paid his $34,000 tax bill in March. If he had known by October that he was tracking toward a large liability, he could have purchased a new piece of equipment, accelerated some deductible expenses, or made a retirement contribution — all legitimate, all legal, all timing decisions that require advance notice. The cost of the surprise: not necessarily the tax bill itself, but the financial flexibility he lost by not knowing.

Cascade Mechanical's Recoverable Value

Add it up: $37,800 in margin, $5,900 in collection cost, $16,000 in tax savings. That's roughly $59,700 per year that Cascade Mechanical is leaving on the table — not from bad decisions, but from not having the visibility to make better ones. A fractional controller engagement for a business this size costs $3,000–$4,500 per month. At the low end, that's $36,000/year for a controller — to capture $59,700 in value. The math is not close.

Note: These are illustrative figures based on common patterns in businesses at Cascade Mechanical's revenue level. Actual results vary by business, industry, and existing financial practices.

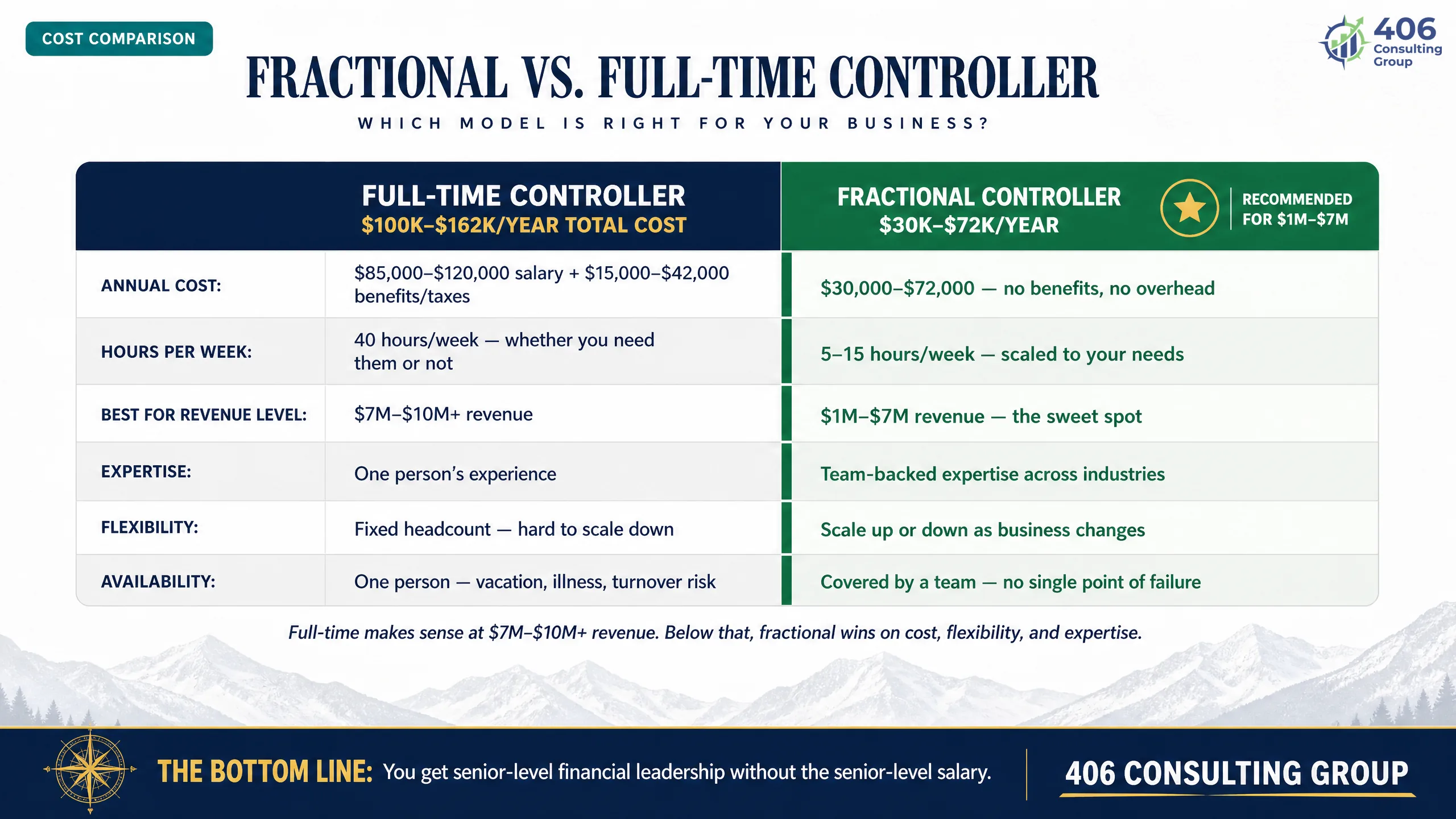

Fractional Controller vs. Full-Time: What Montana Businesses Need

When most business owners hear “controller,” they picture a full-time hire — a $90,000 salary, an office, benefits, the whole thing. For a $1.8M business, that picture is completely wrong. Here's what the numbers actually look like.

| Factor | Full-Time Controller | Fractional Controller |

|---|---|---|

| Annual cost | $80,000–$120,000 salary + 25–35% benefits = $100,000–$162,000 total | $2,500–$6,000/month = $30,000–$72,000/year |

| Hours per week | 40 hours/week — most of which a $1M–$3M business doesn't need | 8–20 hours/month — scaled to what the business actually requires |

| Right size for... | $8M+ in revenue where financial complexity justifies full-time oversight | $1M–$8M in revenue — the vast majority of Montana SMBs |

| Expertise level | One person's experience and knowledge | Senior-level expertise across multiple clients and industries |

| Flexibility | Fixed overhead — hard to scale down during slow periods | Scales with the business — more intensive during growth phases or loan prep |

| Availability | Dedicated — but also limited to one set of knowledge | Multiple senior-level practitioners; not dependent on one person's availability |

What Cascade Mechanical Actually Needs

Cascade Mechanical at $1.8M doesn't need a controller sitting in an office 40 hours a week. Mike needs: a monthly close done right, a reporting package he can read, job costing tracked by service line, a cash flow forecast updated weekly, and someone who can pull together a lender package when he needs it. That's 10–15 hours a month of senior-level work. At $3,500/month in a fractional engagement, Mike gets exactly what he needs without a six-figure salary commitment he'd be paying for regardless of how much work there was to do.

The Upgrade Path: Bookkeeper + Controller Working Together

The most important thing to understand: adding a controller doesn't mean replacing your bookkeeper. These roles work together — and when they're structured correctly, they make each other better.

Your bookkeeper

Records every transaction. Processes invoices and bills. Runs payroll. Reconciles accounts. Provides the raw data.

Your controller

Reviews the bookkeeper's work. Closes the books monthly. Produces the reporting package. Tracks budget vs. actual. Flags issues. Maintains lender-ready financials. Builds and enforces internal controls.

You

Read the monthly report. Make decisions based on real numbers. Know your cash position before a crisis. Walk into a bank with a clean file. Run the business instead of chasing the finances.

What This Looks Like at Cascade Mechanical

Mike's bookkeeper still processes every transaction. On the first of the month, she hands off the QuickBooks file for review. The controller reviews all entries, reconciles any discrepancies, adds the job costing analysis across the three service lines, prepares the 4-page monthly report, and updates the 13-week cash forecast. By the 15th, Mike has everything he needs to understand how last month went and what the next 13 weeks look like.

Mike doesn't get a tax surprise in March anymore. He gets a quarterly tax estimate in October so he can plan. And when his bank called about the truck financing, his controller had a complete financial package ready in two days.

Where Are You Now? The Financial Maturity Assessment

Before deciding to upgrade, it helps to know where you actually stand. Not where you think you stand — where the numbers say you are.

406 Consulting Group built a free Financial Maturity Assessment that takes about eight minutes to complete. It scores your business across five key dimensions — bookkeeping quality, reporting, cash flow visibility, internal controls, and tax readiness — and gives you a score between 1 and 5 in each area. A score below 2.5 in any dimension means you have a gap that is likely costing you money right now.

| Score | What It Means | Likely Next Step |

|---|---|---|

| 1.0–2.0 | Books are incomplete or unreliable. Basic bookkeeping is the priority before anything else. | Get bookkeeping cleaned up first. A controller engagement on top of messy books doesn't work. |

| 2.0–2.5 | Books are maintained but reporting is thin. You know what happened but not what it means. | Controller engagement is the right move. The bookkeeping foundation is there. |

| 2.5–3.5 | You have some reporting but it's inconsistent. You get good information some months, nothing useful others. | Controller to standardize reporting and add forecasting. You're close — the upgrade pays quickly. |

| 3.5–4.5 | Solid foundation. Monthly reporting exists. Some forecasting. The gaps are in analysis and strategy. | Consider fractional CFO advisory layer on top of your controller function. |

| 4.5–5.0 | You have strong financial infrastructure. Reporting, forecasting, and controls are working. | Focus on CFO-level strategic decisions: growth, capital, exit planning. |

Run the Assessment — Free, 8 Minutes

The Financial Maturity Assessment will tell you your score across all five dimensions and give you a prioritized list of what to address first. Most business owners are surprised by at least one of the scores — in both directions.

Take the Financial Maturity AssessmentWhat to Look for in a Controller Engagement

Once you've worked through the bookkeeper vs. controller question and decided the upgrade is right, the next question is what a good controller engagement actually looks like. Not all controller services are the same. Here is what to look for — and what to watch out for.

What a strong controller engagement looks like

- Monthly close completed by the 15th — every month, without being asked

- A reporting package you can actually read and understand (not just a QuickBooks export)

- Quarterly check-ins on tax position and year-end planning

- Cash flow forecast updated regularly — not just available on request

- Willingness to work with and review your existing bookkeeper

- Lender experience — they understand what a bank needs to see

- Clear deliverables and a defined scope of work from the start

Red flags to watch for

- ✗Produces reports but can't explain what changed or why

- ✗Refuses to work with your existing bookkeeper — wants to replace everything

- ✗No defined monthly deliverable — just 'available when you need me'

- ✗No experience with your industry or similar businesses

- ✗Can't give you a sample reporting package before you commit

- ✗No lender experience — hasn't worked with a bank on a client's behalf

- ✗Vague about scope and pricing — difficult to understand what you're getting

The Question to Ask Any Controller Before You Hire Them

“Walk me through what I will receive from you every month and when I will receive it.” If they can't answer that question specifically — a defined deliverable, a defined date, a defined format — keep looking. A controller who doesn't have a clear monthly process is a consultant you'll have to manage, not a financial function you can rely on. See also our CFO Services Scorecard for a full breakdown of what each financial function should deliver at each maturity level.

Frequently Asked Questions: Bookkeeping vs. Controller

What's the actual difference between a bookkeeper and a controller?

A bookkeeper records transactions — income, expenses, payroll, reconciliations. Their job is accurate records. A controller owns the financial function: they close the books, produce reporting you can make decisions from, track budget vs. actual, forecast cash flow, and maintain the internal controls that make your financial records reliable. Most businesses need both, working together. The bookkeeper feeds the data; the controller uses it to run the financial picture.

At what revenue level does a business need a controller?

The honest answer is: it depends more on complexity than revenue. A $1.5M business with multiple service lines, employees, job costing needs, and a commercial loan outstanding needs a controller. A $2M business with one product, one customer type, and simple cash flow might be fine with a strong bookkeeper for a while longer. That said, $1M–$1.5M is where the warning signs typically start showing up — and $2M+ is where operating without a controller starts becoming genuinely expensive.

Can I keep my bookkeeper if I hire a controller?

Yes — and in most cases you should. The bookkeeper and controller work together, not against each other. The bookkeeper handles day-to-day transaction processing. The controller reviews that work, closes the books, and produces the reporting layer on top of it. Replacing a reliable bookkeeper is usually the wrong move. Adding the controller function on top of what your bookkeeper already does is the right structure.

What does a fractional controller cost?

For a Montana business in the $1M–$5M revenue range, a fractional controller engagement typically runs $2,500–$6,000 per month depending on complexity, transaction volume, and scope. Cascade Mechanical at $1.8M with three service lines and a job costing component would be toward the middle of that range — around $3,000–$4,500/month. Compare that to a full-time controller at $85,000–$120,000 in salary (plus benefits), and fractional is significantly more cost-effective until a business reaches $7M–$10M where full-time volume justifies the investment.

How is a controller different from a CFO?

A controller manages the financial function — closing, reporting, controls, compliance. A CFO uses what the controller produces to make strategic decisions: capital structure, growth planning, financing strategy, M&A. For most businesses under $5M, a strong controller is what they need. A fractional CFO makes sense once the reporting and controls are solid and the owner wants forward-looking strategic guidance — not just historical reporting. You generally need the controller foundation before a CFO engagement adds its full value.

What does a controller actually deliver each month?

At minimum: a reconciled income statement with prior-period comparison, a balance sheet, a cash flow statement, and a brief narrative explaining material changes. In a well-structured engagement, you also get a budget vs. actual comparison with variance explanations, a 13-week cash flow forecast, an AR aging report, and quarterly tax position updates. The deliverable should be defined, dated, and consistent — not assembled on request when you need it.

Controller vs. Bookkeeper

At a glance

The 7 Signs — Quick Check

Know Where You Stand

Free assessment — 8 minutes

406 Financial Services

Controller Services

Monthly close, reporting, cash flow forecasting, internal controls

Bookkeeping

Clean, consistent transaction recording and reconciliation

CFO Advisory

Strategic layer — capital, growth, and financial decision-making

Tax Planning

Year-round tax positioning, S-Corp elections, entity strategy

About the Author

Jason Anderson

Co-Founder, 406 Consulting Group

Background in large-scale operational finance — managing $75M inventory at BP and overseeing large-scale pipeline operations. Built financial infrastructure for large systems before bringing that discipline to Montana SMBs. He knows what a functioning financial operation looks like at scale — and what it takes to build one at $1M–$5M.

Read the Full Story