Small Business Tax Preparation

in Butte, Montana

Dan owns Summit Electric in Butte and pays his taxes every April — always with a check he didn't plan for. This guide covers Montana's tax landscape, Butte-Silver Bow local requirements, the S-Corp election most trade businesses haven't made, and the strategies that turn tax prep into tax planning.

Dan owns Summit Electric, a four-person electrical contracting business in Butte. He has been in business for seven years, does about $680,000 in revenue, and pays his taxes every year — usually in April, usually with a check he didn't plan for, and always with a vague sense that he probably should have done something differently the year before.

Last year, Dan's CPA told him he owed $14,400 in self-employment tax. Dan paid it. The year before, same story — different number, same surprise. He has been in business seven years. He has paid that bill seven times. Nobody has ever told him there is a way to cut it nearly in half.

Dan also missed his Butte-Silver Bow personal property report deadline in 2023. The penalty was $800. He didn't know the filing existed until he got the notice.

This is not a story about a bad business owner. Dan runs a tight operation. His crews show up. His customers pay. This is a story about what happens when small business tax preparation in Butte gets treated as a once-a-year event instead of a year-round function — and what it costs when nobody tells you about the deadlines, the strategies, or the elections you can make before the year is over.

By Carrie Anderson — Co-Founder, 406 Consulting Group. Background includes 300+ commercial loan reviews, small business financial advisory, and Montana tax compliance. Based in Montana.

Quick Answer: What Butte Business Owners Need to Know

- →Montana has no sales tax, but it does have a 5.9% income tax on pass-through earnings — dropping to 5.65% in 2026.

- →Butte-Silver Bow business licenses renew in January only. Miss it and the fee doubles.

- →Personal property report is due March 1 every year. Most owners don't know it exists until they get a penalty notice.

- →S-Corp election is the single biggest tax lever for most Butte small businesses — and most haven't made it.

- →The 20% pass-through deduction is now permanent and 100% bonus depreciation is back — two strategies worth real money if you plan for them.

Table of Contents

What Butte Business Owners Get Wrong About Tax Prep

Most small business owners in Butte think about taxes once a year — usually sometime in February when their bookkeeper asks for documents, or in April when the CPA calls. That's not tax preparation. That's tax recording. You're describing what already happened, not managing what's going to happen.

The distinction that costs most business owners real money:

What most owners do

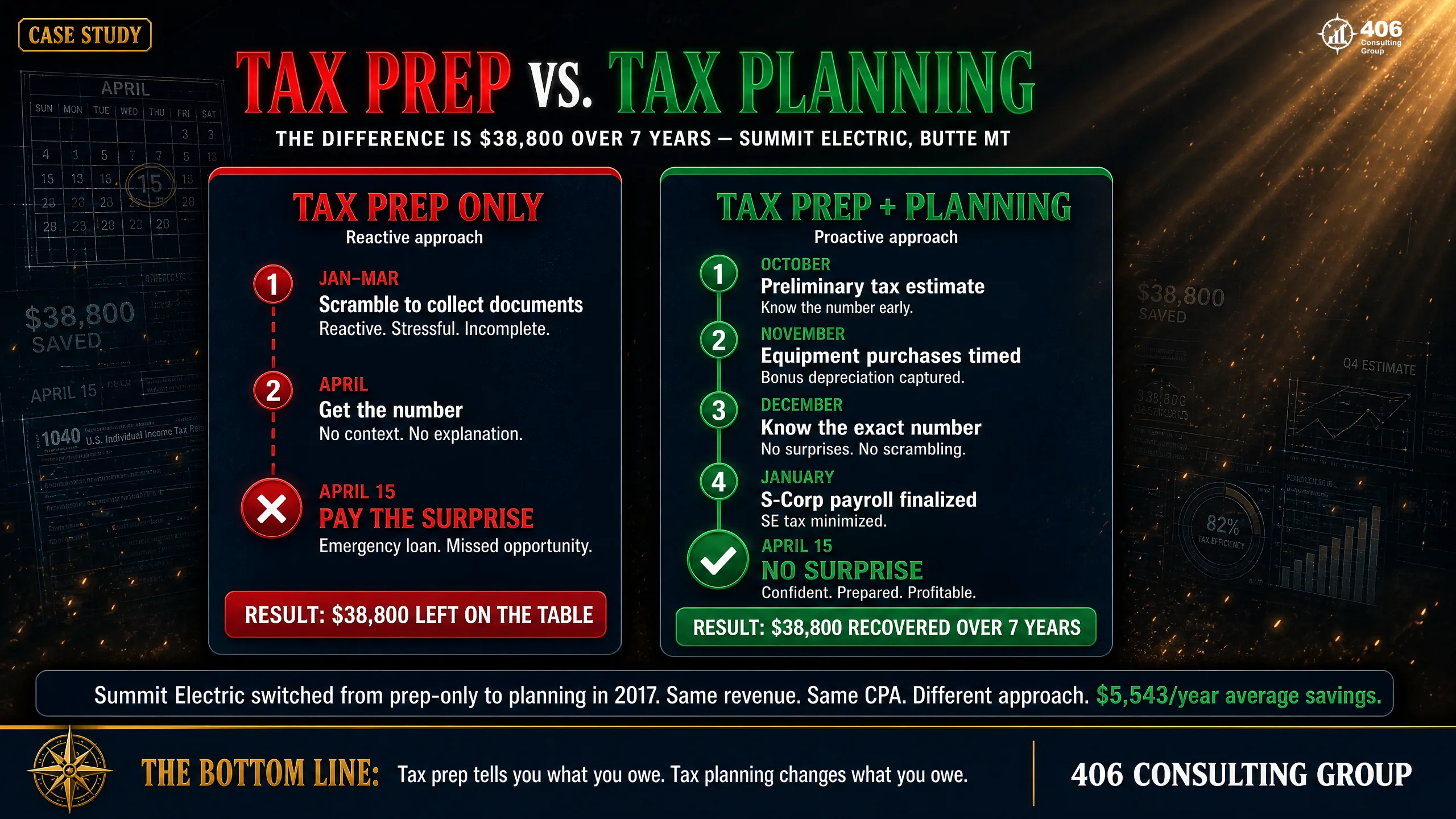

Run the business all year. Hand documents to the CPA in March. Get a number in April. Pay it. Repeat.

What a well-prepared owner does

Gets a tax estimate in October. Makes strategic purchases in November. Knows the number in December. Pays quarterly. No surprises in April.

The most expensive tax mistakes Butte business owners make aren't filing errors. They're timing errors — buying equipment in January when they should have bought it in December, taking a distribution in December when they should have taken it in January, not making the S-Corp election until year six when it would have saved $40,000 over years one through five.

Summit Electric — Dan's Timeline

Dan gets a call from his CPA in late March: "You owe $14,400." He pays it. Two weeks later, he buys a new service van — the same van he needed in December, when the purchase would have reduced his taxable income. Nobody told him the timing mattered. His CPA was busy filing returns through April 15 and didn't have a conversation with Dan until it was too late to act. That's not a bad CPA. That's a tax prep relationship instead of a tax planning relationship.

Montana's Tax Landscape: What's Different Here

Montana is genuinely one of the better states to run a small business from a tax perspective. But "better" doesn't mean "simple" — and there are Montana-specific rules that catch business owners off guard every year.

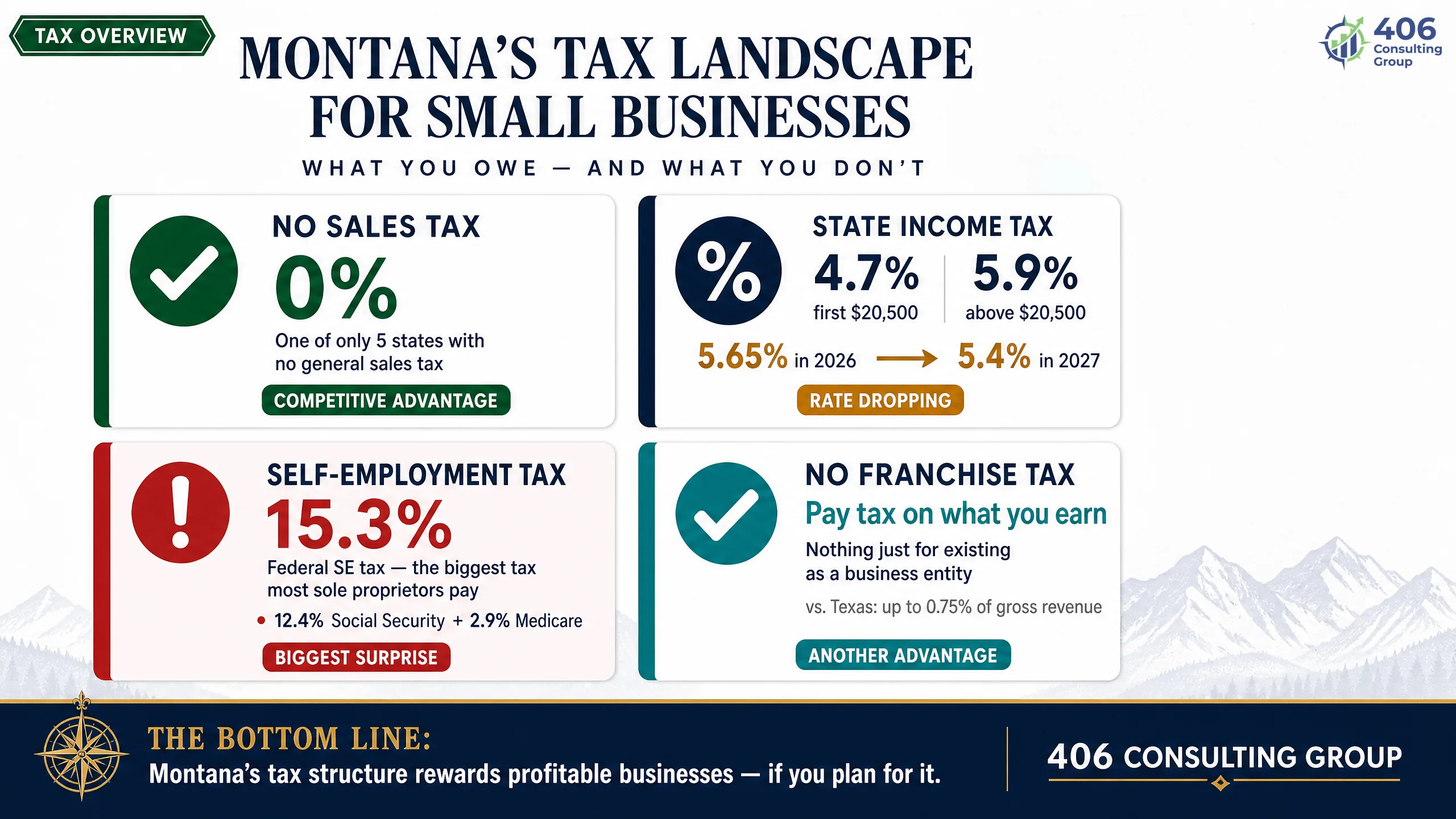

No sales tax — and that's real money

Montana is one of five states with no general sales tax. For a Butte retailer or service business, that means no sales tax registration, no quarterly sales tax filing, no nexus calculations, and no compliance overhead that eats 4–6 hours per month in other states. It's a genuine advantage. The trade-off: Montana makes up some of that revenue through income tax.

Montana income tax: 4.7% and 5.9%

Montana has two tax brackets. Income up to $20,500 is taxed at 4.7%. Income above $20,500 is taxed at 5.9%. For a pass-through business like an LLC or S-Corp, this applies to the owner's share of business income on their personal return. Important: pass-through entities filing a composite return (covering nonresident owners) are taxed at the flat rate of 5.9% on all income.

Rates are dropping — and the timing matters

Montana passed HB 337, which reduces the top income tax rate from 5.9% to 5.65% in 2026 and 5.4% in 2027. This is significant for a business owner who is planning major events — selling the business, taking a large distribution, converting entity types. Doing those things in 2027 at 5.4% instead of 2024 at 5.9% is real savings, and it's worth factoring into multi-year planning.

No franchise or privilege tax

Some states charge a franchise tax just for the privilege of doing business — regardless of income. Montana does not. You pay income tax on what you earn. If you have a bad year, your state tax bill reflects it.

| Tax Type | Montana Rule | What It Means for Your Business |

|---|---|---|

| Sales Tax | None | No filing, no compliance, no nexus issues for in-state sales |

| Income Tax | 4.7% / 5.9% | Pass-through income taxed at owner's rate; top rate dropping to 5.4% by 2027 |

| Corporate Tax | 6.75% | Applies to C-Corps only; most small businesses avoid via LLC or S-Corp |

| Self-Employment Tax | Federal — 15.3% | Not a Montana tax, but the biggest tax most sole proprietors pay |

| Personal Property Tax | Montana DOR | Annual report due March 1; applies to business equipment, furniture, and fixtures |

| Payroll Tax | Federal + Montana UI | Montana unemployment insurance (UI) rate varies by industry and claims history |

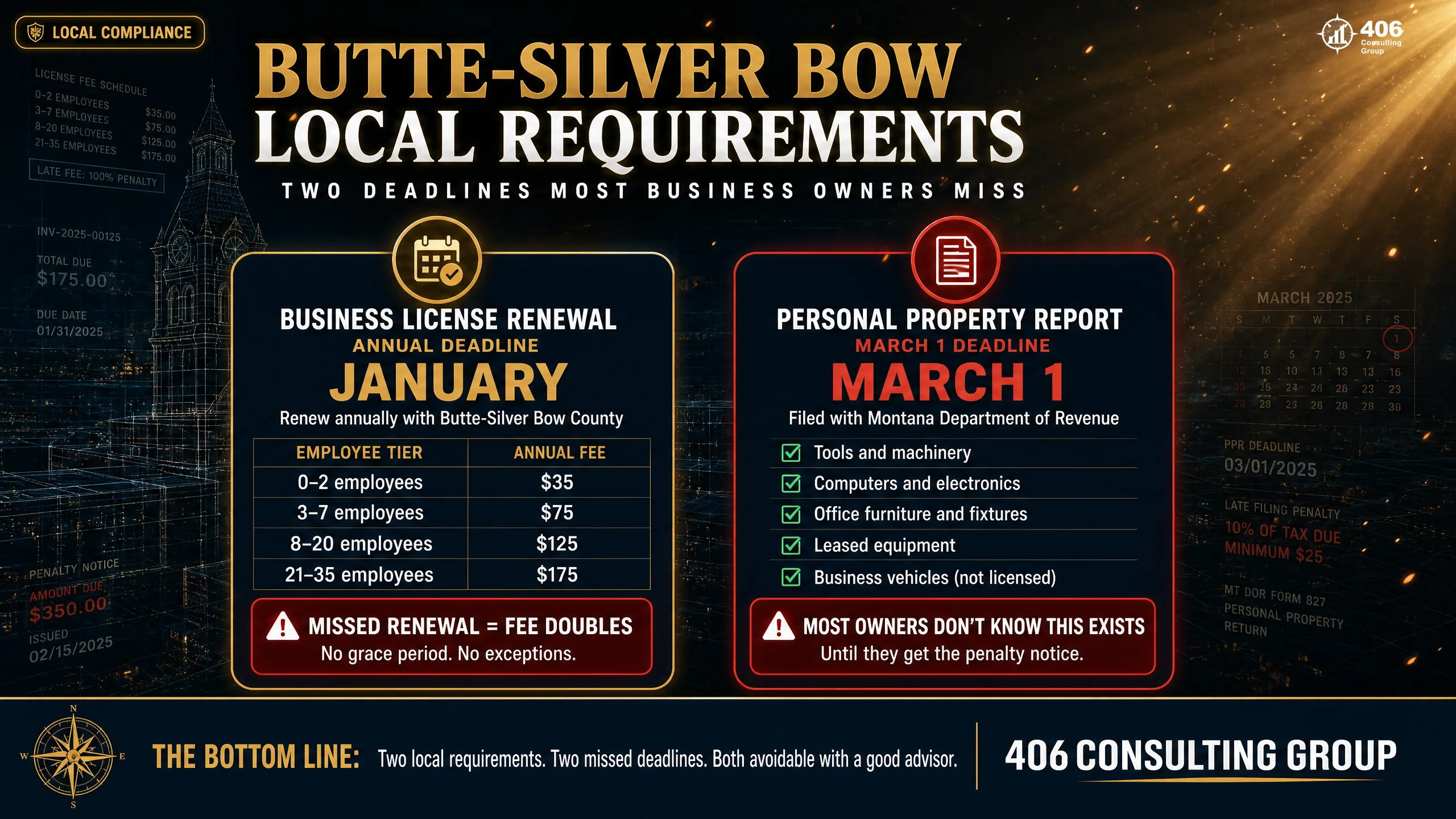

Butte-Silver Bow Local Requirements Most Business Owners Miss

Montana state taxes get all the attention. What gets less attention — and what trips up more Butte business owners — are the local Butte-Silver Bow requirements that run on their own deadlines, separate from your federal and state filings.

Butte-Silver Bow Business License

Renewal: January only — no exceptions

Every business operating in Butte-Silver Bow must hold a current business license. The fee scales by employee count:

0–2 employees

$35

3–7 employees

$75

8–20 employees

$125

21–35 employees

$175

The rule that catches everyone: missed renewals double the fee.

Renewals are accepted in January only. If you miss January — even by one day in February — you are considered delinquent and the fee doubles. There is no grace period. New businesses must file when they open; renewals are annual from that point forward.

Personal Property Report — Montana DOR

Due: March 1, every year

If your business owns equipment, furniture, computers, fixtures, or any other tangible personal property, you are required to file a personal property reporting form with the Montana Department of Revenue by March 1 each year. This is separate from your income tax return and separate from your business license. Most business owners don't learn it exists until they get a penalty notice.

What counts as personal property

Tools, machinery, equipment, computers, office furniture, vehicles not registered in the business name, display cases, signage, manufacturing equipment

What doesn't count

Real property (buildings and land — that's a different assessment), inventory held for sale, licensed motor vehicles

What happens if you miss it

The county assessor estimates your property value — typically higher than actual — and you're assessed taxes plus a penalty. Dan's 2023 penalty: $800.

Who has to file

Any business that owns tangible personal property with a total value above the de minimis threshold. If you have business equipment, assume you have to file.

Summit Electric — Dan's Missed Deadline

Dan has owned three service vehicles, two fully equipped work vans, specialty electrical tools, and a trailer full of conduit equipment for years. None of that was on his radar as "property tax." He filed income taxes. He paid sales tax (until he learned Montana doesn't have one). He never filed a personal property report. In 2023 he got a notice: estimated personal property assessment, late filing penalty — $800. He called his CPA, who apologized and said it had slipped through. Dan paid the $800 and filed within the week. Now it's in his calendar.

Documents You Need Before Tax Season

Getting this list together before your CPA asks for it — not after — is the single easiest way to cut your tax prep bill and avoid the "we need one more thing" loop that drags filings into September. Here is what your tax preparer needs and why each piece matters.

Financial Records

Year-end P&L statement

Shows total income and expenses by category. Must be reconciled — not just a QuickBooks export.

Balance sheet as of December 31

Shows assets, liabilities, and owner equity. Your CPA needs this to check for balance sheet issues before filing.

Bank statements — all accounts, all 12 months

Used to verify income and catch any transactions not recorded in your books.

Credit card statements — all business cards

Same purpose as bank statements — your CPA should reconcile these against your books.

Payroll & People

W-2s for all employees

Required to file business return and verify payroll tax deposits match.

1099-NECs for contractors paid $600+

Must be filed with the IRS by January 31. If you haven't sent them, do it before your CPA appointment.

Payroll tax deposit records

Confirms all payroll taxes were paid on time. Late deposits trigger penalties.

Health insurance premiums paid for owner

Self-employed health insurance is deductible on your personal return — often missed.

Assets & Equipment

Asset list — everything purchased during the year

Your CPA needs to know what you bought and when to apply the correct depreciation method.

Receipts or invoices for major purchases ($500+)

Documents the asset cost and placed-in-service date for depreciation records.

Vehicle mileage log

The IRS requires a contemporaneous log — not a year-end estimate. If you don't have one, this deduction is at risk.

Section 179 and bonus depreciation elections from prior years

Affects how remaining basis is calculated on existing assets.

Income Verification

1099-Ks from payment processors (Square, Stripe, PayPal)

These go directly to the IRS. Your income must match or your CPA must reconcile the difference.

Loan documents for any new debt

Interest is deductible; principal is not. Your CPA needs to separate the two.

Prior year tax return

Used to carry forward losses, check depreciation schedules, and verify basis.

Personal property report (filed March 1)

Separate filing from your income return — confirm this was done before your CPA appointment.

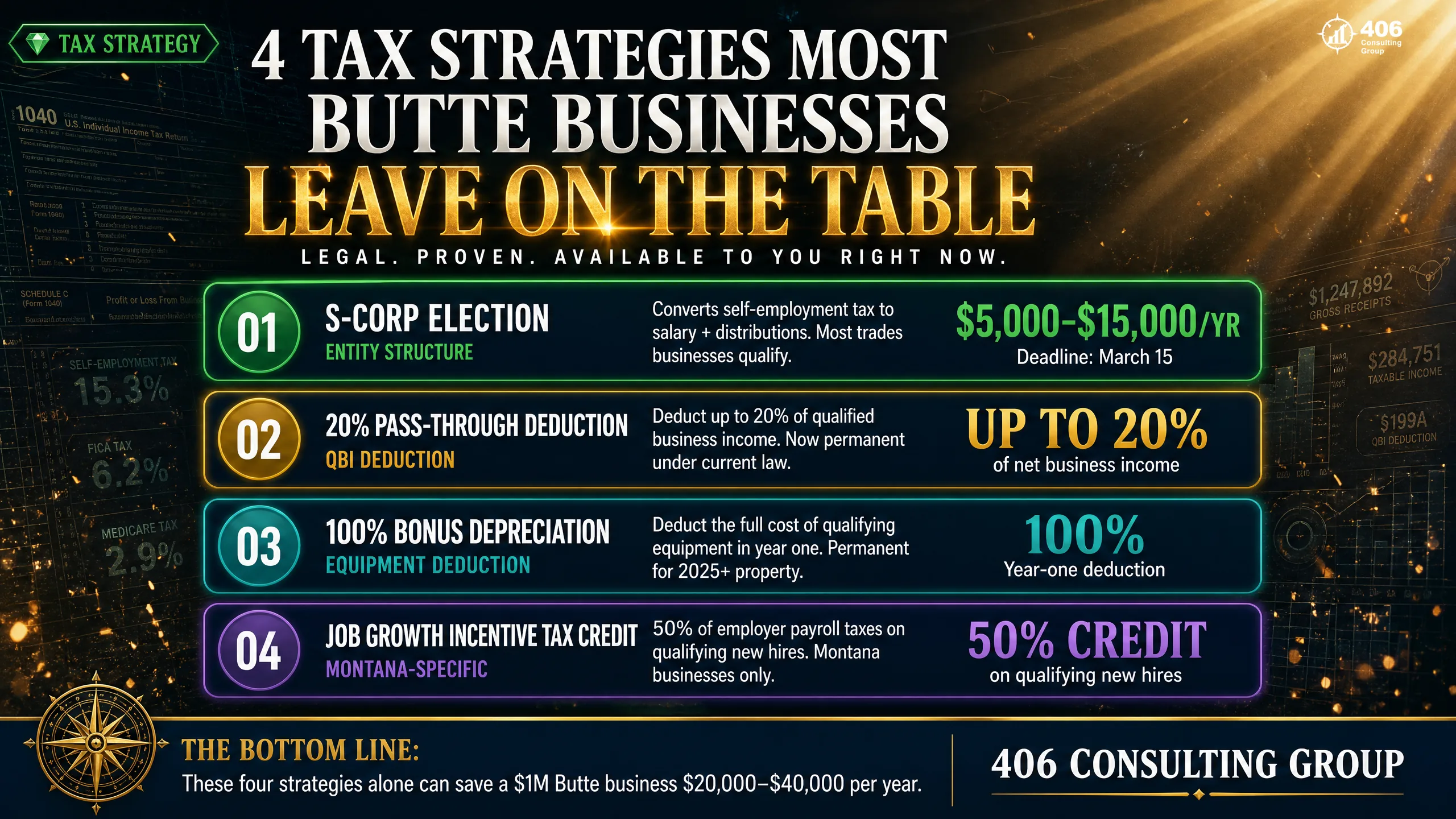

4 Tax Strategies Butte Small Businesses Miss — Including the Montana S-Corp Election

These are not loopholes. They are legal elections and deductions that Congress specifically created for small business owners. Most Butte business owners qualify for all four. Most are using zero of them effectively.

S-Corp Election — The Biggest Single Lever for Most Business Owners

If you are operating as a sole proprietor or single-member LLC and your net profit is above $50,000, you are almost certainly paying more self-employment tax than you need to. The S-Corp election changes how your income is classified — and that classification makes a large dollar difference.

Summit Electric — Dan's S-Corp math

Without S-Corp election

With S-Corp election

Dan has been in business 7 years. At $5,500/year in savings, that's $38,500 he could have kept over that period — net of any incremental accounting cost to run payroll.

Important: the S-Corp election has a deadline.

To elect S-Corp status for the current tax year, you must file Form 2553 by March 15 (for calendar year businesses). Miss that date and the election takes effect the following year. This is a decision to make before the year starts — not in April. See our S-Corp Calculator to run your numbers.

20% Pass-Through Deduction — Now Permanent

The qualified business income (QBI) deduction allows eligible pass-through business owners to deduct up to 20% of their qualified business income on their personal return. As of July 2025, this deduction was made permanent — it no longer expires at the end of 2025 as originally scheduled.

For Dan at Summit Electric: if his net profit is $102,000, the QBI deduction could eliminate tax on up to $20,400 of that income. At Montana's 5.9% rate plus his federal rate, that's a meaningful number — typically $5,000–$8,000 in combined federal and state tax savings for a business in Dan's range.

Most trade and service businesses in Butte qualify. The deduction phases out at higher income levels and has limitations for certain specified service trades, but for contractors, retail, healthcare support, and most local businesses — it applies. Your CPA should be calculating this automatically. If they're not, ask why.

100% Bonus Depreciation — Back and Permanent

For business property placed in service after January 19, 2025, 100% bonus depreciation is back and has been made permanent. This means if Summit Electric buys a $45,000 service truck, Dan can deduct the full $45,000 in year one — instead of depreciating it over five years.

This matters enormously for timing. A piece of equipment placed in service on December 31 qualifies for the full deduction in that tax year. The same equipment placed in service on January 2 pushes the deduction to the following year. For a business that is having a high-income year, that timing difference can mean $5,000–$15,000 in deferred taxes.

The planning implication:

If you know in October that you are having a strong year, that's the right time to accelerate planned equipment purchases into December. Talk to your tax advisor before the purchase — not after. The deduction is worth planning around, not just capturing after the fact.

Montana Job Growth Incentive Tax Credit

If you have hired new employees in Montana, you may qualify for the Job Growth Incentive Tax Credit — a Montana-specific credit equal to 50% of employer-paid payroll taxes on qualifying new hires for up to one year. This is a credit, not a deduction, which means it reduces your actual tax bill dollar-for-dollar.

Most Butte business owners have never heard of it. If Dan hires a new electrician at $55,000 per year, the employer's share of payroll taxes on that hire is approximately $4,208. The Job Growth Incentive Tax Credit could return $2,104 of that as a direct credit against his Montana income tax liability.

The credit requires pre-approval from Montana Department of Labor & Industry. You cannot claim it retroactively — the application must be submitted before or shortly after the new hire. This is another case where year-round planning captures value that annual tax prep misses entirely.

Industry-Specific Tax Issues in Butte

Butte's economy runs on trades, healthcare, retail, and food service. Each of those sectors has its own tax wrinkles — deductions, elections, and compliance requirements that don't apply to every business. Here is what matters by industry.

Trades & Construction (Electrical, Plumbing, HVAC, Roofing)

Equipment depreciation

Heavy tool and equipment purchases are your biggest deduction lever. 100% bonus depreciation makes timing critical — buy before December 31, not January 2.

Job costing and deductible costs

Materials, subcontractor costs, and direct labor are all deductible — but they need to be tracked by job to defend the deduction if questioned.

Vehicle deductions

You can deduct actual expenses or the standard mileage rate (67 cents/mile for 2024). For a truck used heavily for work, actual expenses plus depreciation usually wins — but requires records.

Workers' comp and liability insurance

Both are deductible. Montana workers' comp rates for electrical work are significant — make sure premiums are on your books.

Retail (Hardware, Auto Parts, Specialty Stores)

Inventory method election

FIFO (first in, first out) or LIFO (last in, first out) affects your taxable income in inflationary periods. LIFO can defer taxes when costs are rising. The election is locked in once made — get advice before choosing.

Cost of goods sold accuracy

COGS must reflect actual inventory used in sales. A year-end physical inventory count is the foundation of accurate COGS — and a common audit trigger when it's missing.

Section 263A (UNICAP rules)

Retailers with over $30M in gross receipts must capitalize certain indirect costs into inventory. Below that threshold, the simplified method applies — but you still need to know which method you're using.

Shrinkage and obsolescence

Write-offs for inventory that was stolen, damaged, or became unsellable are legitimate — but require documentation. A year-end inventory reconciliation is the starting point.

Healthcare (Dental, Optometry, Physical Therapy, Medical Offices)

Self-employed health insurance deduction

If you pay your own health insurance premiums, those are deductible on your personal return — even if you don't itemize. This is frequently missed by solo practitioners.

Retirement plan deductions

A SEP-IRA allows contributions of up to 25% of net self-employment income, up to $69,000 (2024 limit). A solo 401(k) allows even higher contributions for owner-only practices. Either one is a significant deduction and a tax-deferred savings vehicle.

Equipment and technology depreciation

Diagnostic equipment, imaging systems, and practice management software all qualify for Section 179 or bonus depreciation. These are typically high-dollar purchases where timing matters.

HIPAA compliance costs

Costs for HIPAA-compliant software, training, and compliance consulting are deductible as ordinary business expenses.

Food Service & Hospitality (Restaurants, Bars, Catering)

Tip reporting (Form 8027)

Restaurants with more than 10 employees must file Form 8027 annually, reporting total tips received by employees. Tip income must be reported by employees on Form 4137 when actual tips are less than the allocated amount.

FICA Tip Credit

Employers pay the employer share of FICA (7.65%) on employee tips above the federal minimum wage. The FICA Tip Credit (Form 8846) allows you to claim a tax credit for those payments — directly reducing your tax bill. This is one of the most underused credits in food service.

Montana lodging tax (applies to some)

Montana levies a 4% lodging tax on accommodations. If your business includes short-term lodging (B&Bs, vacation rentals, inn), this is a separate filing requirement from income tax.

Food cost and inventory

Food and beverage inventory is fully deductible when consumed in the production of sales. Accurate tracking through a POS system is the baseline — without it, COGS becomes an estimate, which is a red flag in an audit.

Tax Prep vs. Tax Planning: The Difference That Costs You Real Money

Small business tax preparation in Butte, Montana means filing an accurate return for what already happened. Tax planning means making decisions during the year so that what happens is better than what would have happened without it. They are not the same service, and most Butte small businesses are only buying one of them.

| Factor | Tax Prep Only | Tax Prep + Planning |

|---|---|---|

| When you know your tax number | In March or April, when the return is drafted | In October or November, with enough time to act |

| Equipment purchase timing | Whenever it's convenient — January counts the same as December | Timed to maximize the deduction in the highest-income year |

| S-Corp election | Made after the fact — usually year 6 when someone finally asks | Evaluated in year 1, implemented in year 2 when it makes sense |

| Owner distributions | Taken when cash is available; tax consequences managed later | Timed by tax year to optimize between salary, distribution, and retirement |

| Estimated tax payments | Paid (or not) without a clear forecast of what's owed | Calculated quarterly based on actual year-to-date income |

| Annual surprise | Yes — the CPA calls with a number in March | No — you know the number by December and have cash set aside |

The cost of prep-only for Dan

In seven years of business, Dan paid approximately $100,800 in self-employment taxes. With a year-one S-Corp election and proper planning, a reasonable estimate of what he would have paid is $62,000 — a difference of $38,800 over the same period. The cost of adding tax planning to his engagement: roughly $1,500–$2,500 per year. The cost of not having it: over $5,500 per year. That math doesn't favor waiting.

DIY vs. Professional: When It Stops Being Worth It

TurboTax and similar software work well for simple situations. A sole proprietor with one income stream, no employees, no equipment, and no entity elections can often file accurately with software. As soon as the complexity increases — employees, depreciation schedules, entity elections, multiple owners — the cost of the software meets the cost of the mistakes.

Sole proprietor, under $150K revenue, no employees

DIY may workSchedule C on your personal return. Software handles this well. Risk: you're not getting the S-Corp conversation, and you may be missing deductions you don't know to ask about.

$150K–$500K revenue, sole proprietor or single-member LLC

Professional advisableYou're likely in the S-Corp conversation zone. You may have employees, equipment, and deductions that require professional judgment. The cost of a CPA (typically $800–$2,500 at this level) is usually recovered in optimized deductions alone.

Above $500K, or any business with employees

Professional requiredPayroll tax returns, depreciation schedules, entity-level returns, W-2/1099 compliance, and Montana-specific requirements are not software territory. The penalty exposure from a DIY mistake at this level is higher than the cost of professional help.

Any business with an S-Corp election or multi-member LLC

Professional requiredS-Corps file a separate business return (Form 1120-S) in addition to the owner's personal return. Multi-member LLCs file Form 1065. These require professional preparation — the cost of a mistake on a business return is measured in penalties and back taxes, not just the cost of amended returns.

What to Look for in a Butte Tax Preparer

Not every tax preparer handling small business tax preparation in Butte, Montana is the same. Virtually anyone in Montana can prepare a return — there is no state licensing requirement beyond the IRS's Preparer Tax Identification Number (PTIN). Here is how to tell the difference between someone who files your return and someone who actually manages your tax position.

Credentials — what they mean

CPA (Certified Public Accountant)

Licensed by the Montana Board of Public Accountants. Passed a rigorous national exam. Bound by continuing education requirements. Can represent you before the IRS in an audit.

Enrolled Agent (EA)

Federally licensed by the IRS. Specifically tested on tax law. Can represent you before the IRS in all matters. Often specializes in tax preparation exclusively.

PTIN Holder (no other credential)

Can legally prepare returns but has no credential beyond registration. No exam, no continuing education requirement, no representation rights in an audit.

Red flags to watch for

- ✗Charges fees based on the size of your refund — this incentivizes inflation

- ✗Only available January through April — no year-round advisory relationship

- ✗Has never heard of the Job Growth Incentive Tax Credit

- ✗Doesn't ask about your entity structure or whether you've evaluated S-Corp

- ✗Doesn't ask about your equipment purchases and their placed-in-service dates

- ✗Can't explain the difference between your Montana state return and your federal return

- ✗Doesn't mention the personal property report when you describe your business

The One Question to Ask Any Tax Preparer Before You Hire Them

“How will you communicate with me between now and next April — and what specifically will that communication look like?”

A preparer who only contacts you when they need documents or to deliver a return is a filing service, not a tax advisor. A tax advisor who contacts you in October with a preliminary tax estimate, tells you what elections are still available, flags upcoming deadlines, and recommends year-end moves — that's a relationship worth paying for. If they can't answer the question specifically, keep looking.

Frequently Asked Questions: Small Business Taxes in Butte, Montana

When should I make the S-Corp election?

To elect S-Corp status for the current calendar year, Form 2553 must be filed by March 15. For a brand-new business, you have 75 days from the date of formation to make the election effective from day one. If you miss the deadline, the election takes effect the following year — which is why the S-Corp conversation should happen in your first year of business, not your sixth. The general rule of thumb: if your net profit from self-employment is consistently above $50,000–$60,000 per year, the math usually favors the S-Corp election.

What are Montana's estimated tax payment deadlines?

Montana follows federal estimated tax payment schedule: April 15, June 15, September 15, and January 15 of the following year. If you expect to owe $500 or more in Montana income tax and are not having taxes withheld at the source, you are required to make quarterly estimated payments. Missing or underpaying estimated taxes results in an underpayment penalty — currently calculated at the federal underpayment rate. The safest approach is to work with your CPA in October to calculate where you stand and adjust Q3 or Q4 payments accordingly.

What is the Butte-Silver Bow personal property report and who has to file it?

Any business operating in Silver Bow County that owns tangible personal property — equipment, tools, machinery, furniture, computers, fixtures — is required to file an annual personal property reporting form with the Montana Department of Revenue by March 1. This is separate from your income tax return and separate from your business license renewal. The assessor uses the reported values to calculate your personal property tax obligation. Missing the deadline results in an estimated assessment (typically higher than actual) plus a late filing penalty. If you're unsure whether you need to file, assume you do and confirm with your CPA.

Does it make sense to change my entity structure?

Entity structure changes are worth reviewing when your income crosses $50,000 in net profit (sole proprietor to S-Corp), when you bring in a partner (single-member LLC to multi-member LLC or corporation), or when you are planning a liquidity event (sale of the business). In Montana, the rate drops coming in 2026 and 2027 also make this a period worth re-evaluating — some structures perform better at different rate levels. A change in entity type has tax, legal, and operational implications; it should never be made based on a single factor. See our article on <Link href='/articles/when-to-change-business-entity-structure' className='text-[#4CAF50] underline font-semibold'>when to change your business entity structure</Link> for a full breakdown.

What triggers an audit for a small business in Montana?

Common federal audit triggers for small businesses include: a large Schedule C loss filed against other income for multiple consecutive years, home office deductions that are disproportionate to total income, vehicle deduction claimed at 100% business use (the IRS is skeptical), significant discrepancies between reported income and 1099s or payment processor reports, and cash-heavy businesses that show unusually low income relative to industry norms. Montana DOR audits often follow federal audits — if the IRS adjusts your federal return, Montana typically reassesses your state return as well. The best defense against an audit is clean records: contemporaneous mileage logs, receipts for business expenses, and books that reconcile to bank statements.

Can I deduct my home office if I run a business in Butte?

Yes — if you meet the IRS requirements. The home office deduction requires that the space be used regularly and exclusively for business. 'Exclusively' is the word that eliminates most claims: a desk in the corner of a guest bedroom doesn't qualify. A dedicated room used only for business work does. If you qualify, you can deduct either a simplified rate ($5 per square foot, up to 300 sq ft = $1,500 max) or actual expenses — a proportional share of mortgage interest or rent, utilities, insurance, and repairs based on the percentage of your home used for business. The actual expense method produces a larger deduction in most cases but requires documentation. Note: the home office deduction is not available to S-Corp employees who work from home — the structure of the deduction changes once you make the S-Corp election.

Related Tools & Resources

Butte, Montana Tax Advisory

Done Paying Taxes You Didn't Plan For?

406 Consulting Group works with Butte small businesses year-round — not just in April. We handle the S-Corp election conversation, the Butte-Silver Bow deadlines, the quarterly tax estimates, and the strategic moves that turn tax prep into tax savings. Let's run the numbers for your business.

Butte Tax Quick Reference

Key numbers and deadlines

Annual Deadline Calendar

January

→ BSB business license renewal (only window)

→ Send W-2s and 1099-NECs to recipients

Jan 31

→ W-2s and 1099-NECs filed with IRS/SSA

March 1

→ Personal property report — Montana DOR

March 15

→ S-Corp and partnership tax returns due

→ S-Corp election deadline for current year

April 15

→ Personal/business tax return due

→ Q1 estimated tax payment due

June 15

→ Q2 estimated tax payment due

September 15

→ Q3 estimated tax payment due

→ Extended S-Corp/partnership returns due

October

→ Year-end tax planning — act before December

January 15

→ Q4 estimated tax payment due

Butte Business? Talk to 406.

Montana-based. Year-round tax advisory.

406 Tax Services

About the Author

Carrie Anderson

Co-Founder, 406 Consulting Group

Background includes 300+ commercial loan reviews, small business financial advisory, and Montana-specific tax compliance. Carrie has worked with trade contractors, retail businesses, healthcare practices, and food service operations across Montana — and has seen every tax mistake in this article in real client files.

Read the Full Story