New Equipment vs. Used Equipment:

Breaking Down the Numbers

The equipment decision most construction and trucking companies get wrong — because they stop at purchase price. The 5-factor ROI framework that reveals the real cost before you sign anything.

Every construction and trucking company eventually faces the same decision: new iron or used iron? The mistake most owners make isn't picking the wrong answer — it's using the wrong question. "Which one costs less to buy?" is not the same as "Which one costs less to own, operate, and eventually sell?" Those two questions produce different answers, and the gap between them is where profitable equipment decisions live and where bad ones quietly bleed cash.

This guide breaks down the full financial analysis using the 406 Equipment ROI Framework — five factors that together determine the true cost of a piece of equipment over its useful life in your operation. Carrie Anderson spent years as a commercial underwriter reviewing equipment loan files for Montana businesses, and the patterns in which purchases worked and which didn't are the foundation of this framework. It covers tax treatment under the OBBBA (100% bonus depreciation is now permanent), financing options and how lenders view new vs. used as collateral, downtime risk math, resale value curves, and Montana-specific considerations that national equipment guides ignore. The goal is a decision you can defend with numbers, not gut feel.

Table of Contents

The Equipment Decision Every Construction and Trucking Company Faces

The core tension is real: a new excavator at $280,000 feels like a stretch. A five-year-old excavator at $145,000 feels like a deal. But "feels like" is doing a lot of work in that sentence. The used machine's 8,000 hours mean more frequent hydraulic servicing, higher parts cost, and a non-zero probability of a $35,000 engine overhaul in year two. The new machine comes with a manufacturer warranty, better fuel efficiency, and zero deferred maintenance. Neither is automatically right — the answer depends on five financial variables that most owners don't fully model before signing.

30–60%

Higher maintenance cost per hour

Used equipment 8+ years old vs. new — the maintenance premium that rarely appears in the purchase price comparison.

20–30%

New equipment depreciation in year 1

The value a new piece of equipment loses in its first 12 months — which used equipment buyers avoid entirely.

$3K–$8K

Daily revenue lost to a breakdown

What one day of unplanned downtime costs a construction operation — the risk premium on older equipment.

The Question Most Owners Ask vs. The Question That Matters

"Which costs less to buy?" vs. "Which costs less to own, operate, and sell over the next five years after taxes?" When tax treatment closes the new-vs-used purchase price gap by $40,000 in year one, the conversation changes. Run the full analysis — not just the sticker price comparison.

The 406 Equipment ROI Framework

The 406 Equipment ROI Framework evaluates every equipment purchase across five dimensions simultaneously. Buying on Factor 1 alone — purchase price — without modeling Factors 3 and 4 (operating costs and downtime risk) is the most common way construction and trucking companies make expensive equipment decisions. All five factors interact. A used unit that scores well on price may score poorly on operating cost and downtime, and the combined verdict can flip entirely.

Purchase Price & Financing

The visible cost — but only the starting point. Includes down payment, financing rate, monthly payment, and true cash-out-of-pocket in year one after tax treatment.

Tax Treatment

Section 179 and 100% bonus depreciation can close the new-vs-used price gap by $30,000–$80,000 in year one alone. Both new and used equipment qualify — but the math differs.

Operating Cost Baseline

Maintenance, fuel, insurance, and tires per operating hour. Modeled over the projected ownership period — not just year one. The number most owners skip.

Downtime Risk

The probability-weighted cost of unplanned downtime. For critical-path equipment, one major breakdown can cost more than the purchase price gap between new and used.

Resale Value & Exit Strategy

What will this equipment be worth in 3–7 years? The exit value directly affects total cost of ownership — and determines whether you can trade up on favorable terms.

Factor 1: Purchase Price, Financing, and True Monthly Cost

Purchase price is the most visible factor — and the one most owners stop at. The fuller picture includes the down payment, the financing rate differential between new and used, and the monthly payment impact. For tax-paying businesses, the year-one effective cost also includes the depreciation benefit, which is covered in Factor 2. Here's what the financing side looks like in practice.

| Financing Variable | New Equipment | Used Equipment | Notes |

|---|---|---|---|

| Typical Rate Range | 5.5–7.5% | 7.5–11% | Captive lenders (Cat, Deere, Kenworth) offer best new rates; used goes to commercial lenders |

| Max LTV / Loan-to-Value | Up to 100% | 70–85% of appraised value | Lenders discount used equipment value; may require larger down payment |

| Typical Term | 48–84 months | 36–60 months | Shorter terms on used reduce lender risk; increases monthly payment |

| Warranty Factor | Full manufacturer | None (or extended for fee) | Warranty reduces lender risk perception — factors into rate |

| Appraisal Required | Rarely | Often (for older/higher-hour units) | Adds $500–$1,500 and 1–2 weeks to close |

| Down Payment Typical | 10–20% | 15–30% | Used requires more skin-in-the-game from borrower |

Side-by-Side Payment Comparison — $280K New vs. $145K Used Excavator

New — $280,000

Used — $145,000 (5 yr, 7,200 hrs)

Year-1 out-of-pocket gap: $26,116 — before tax treatment, operating cost differential, or downtime risk. Factor 2 will close this gap significantly.

For a deeper look at how commercial lenders underwrite equipment purchases alongside other business debt, see our guide on what banks look at for a commercial loan.

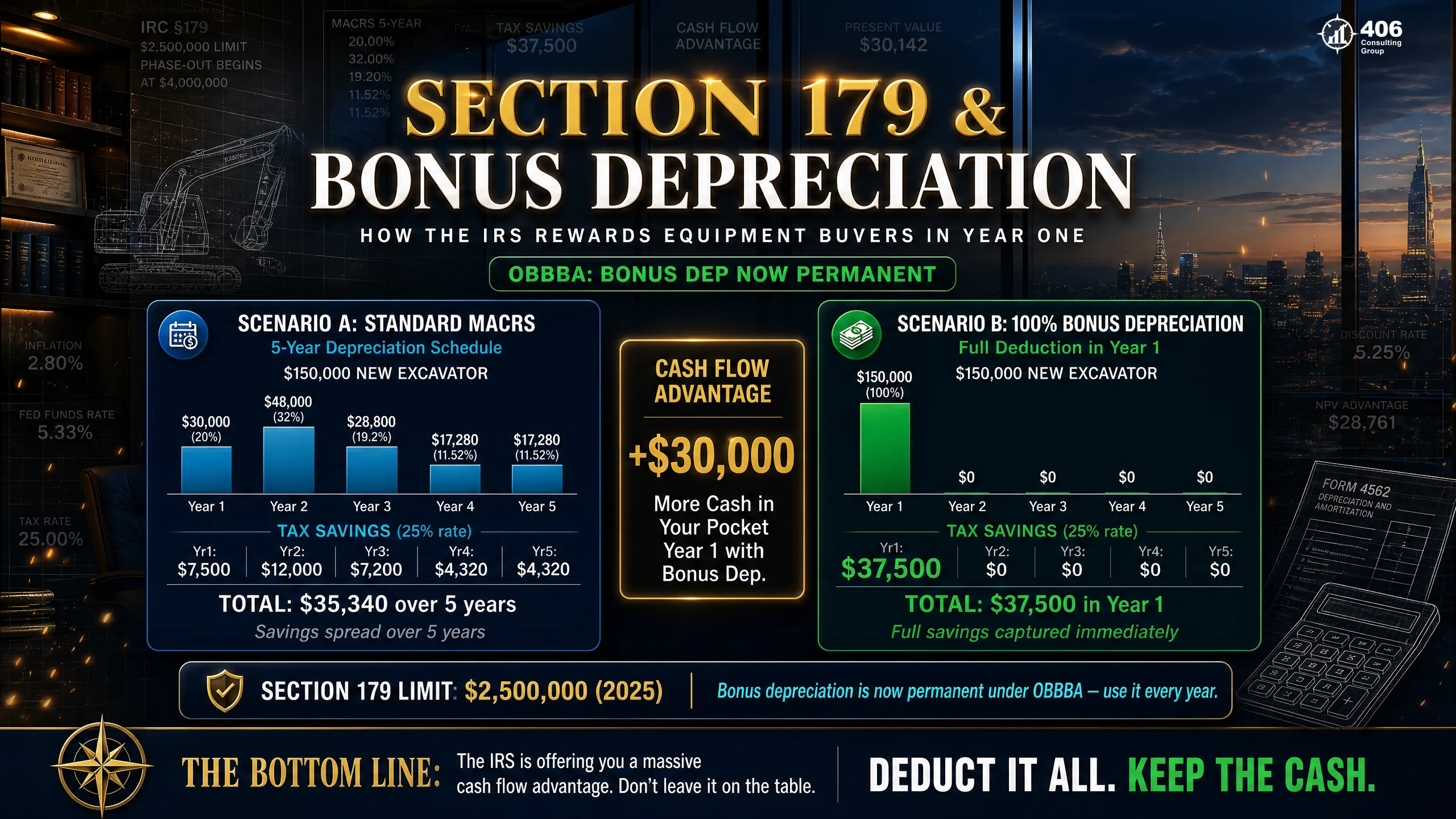

Factor 2: Tax Treatment — Section 179, Bonus Depreciation, and MACRS

Tax treatment is the most underutilized factor in the new vs. used equipment decision — and the one most likely to change the verdict. The One Big Beautiful Bill Act (OBBBA, signed July 4, 2025) made 100% first-year bonus depreciation permanent. Section 179 limits increased to $2.5 million for 2026. Critically: both new and used equipment qualify for bonus depreciation and Section 179 — but the tax impact differs because the starting asset values differ.

100% Bonus Depreciation

Permanent under OBBBA. Deduct the full purchase price in year one — no spreading across 5-year MACRS schedule. Applies to both new and used qualifying property.

Section 179 — $2.5M Limit

2026 limit: $2.5 million per entity. Phase-out begins at $4.05M in total property placed in service. Can be combined with bonus depreciation or used separately.

MACRS 5-Year Schedule

Standard depreciation if you don't elect bonus or Sec. 179. Most construction equipment depreciates over 5 years under MACRS — but the front-loaded schedule still produces significant year-1 deductions even without bonus.

| Scenario | Asset Value | Year-1 Deduction | Tax Savings (25% rate) | Effective Net Cost |

|---|---|---|---|---|

| New excavator — 100% bonus | $280,000 | $280,000 | $70,000 | $210,000 |

| Used excavator — 100% bonus | $145,000 | $145,000 | $36,250 | $108,750 |

| New excavator — MACRS only | $280,000 | $56,000 (20%) | $14,000 | $266,000 |

| Used excavator — MACRS only | $145,000 | $29,000 (20%) | $7,250 | $137,750 |

What This Does to the New vs. Used Decision

After 100% bonus depreciation, the effective net cost of the new excavator ($210,000) vs. the used ($108,750) is still a $101,250 gap — but it's now $101,250 vs. the pre-tax gap of $135,000. The tax benefit of the new unit ($70,000 in savings) is larger than the used unit's tax benefit ($36,250) in absolute terms. This is why high-margin businesses often favor new equipment — the larger deduction generates a larger tax shield. Lower-margin businesses may find the used unit's lower total capital deployment more attractive. Run it with your actual tax rate. See IRS.gov bonus depreciation rules.

Factor 3: Operating Cost Baseline — Maintenance, Fuel, and Insurance

Operating cost per hour is the number most equipment buyers never calculate before purchasing. It's also the number that most reliably determines whether the purchase was good or bad — because it compounds across every hour the machine runs. A used machine with 30% higher operating costs per hour running 1,200 hours annually generates $9,000–$18,000 in additional operating expense every year compared to new iron. Over a 5-year ownership period, that's $45,000–$90,000 in costs that were invisible at purchase time.

| Operating Cost Component | New Equipment (per hr) | Used 5–7 yrs (per hr) | Used 8–12 yrs (per hr) |

|---|---|---|---|

| Scheduled Maintenance (oil, filters, fluids) | $4–$7 | $6–$10 | $9–$15 |

| Unscheduled Repairs (avg annualized) | $2–$5 | $5–$12 | $12–$25 |

| Undercarriage / Wear Parts (tracked equip) | $8–$12 | $12–$18 | $18–$28 |

| Fuel (modern Tier 4 vs. older engines) | $22–$35 | $25–$38 | $28–$42 |

| Insurance (per hour estimate) | $2–$4 | $3–$5 | $4–$7 |

| Estimated Total Operating Cost/hr | $38–$63 | $51–$83 | $71–$117 |

How to Build Your Own Operating Cost Baseline

Before buying any piece of used equipment: (1) Get the last 12 months of maintenance records — actual parts and labor spend, not owner estimates. (2) Pull the hours meter and calculate cost per hour from records. (3) Call your dealer or an independent mechanic and ask what deferred maintenance this machine needs in the next 500 hours. (4) Budget that deferred maintenance as a day-one cost, not a future maybe. An owner who can't produce maintenance records is telling you something important about how this machine was treated.

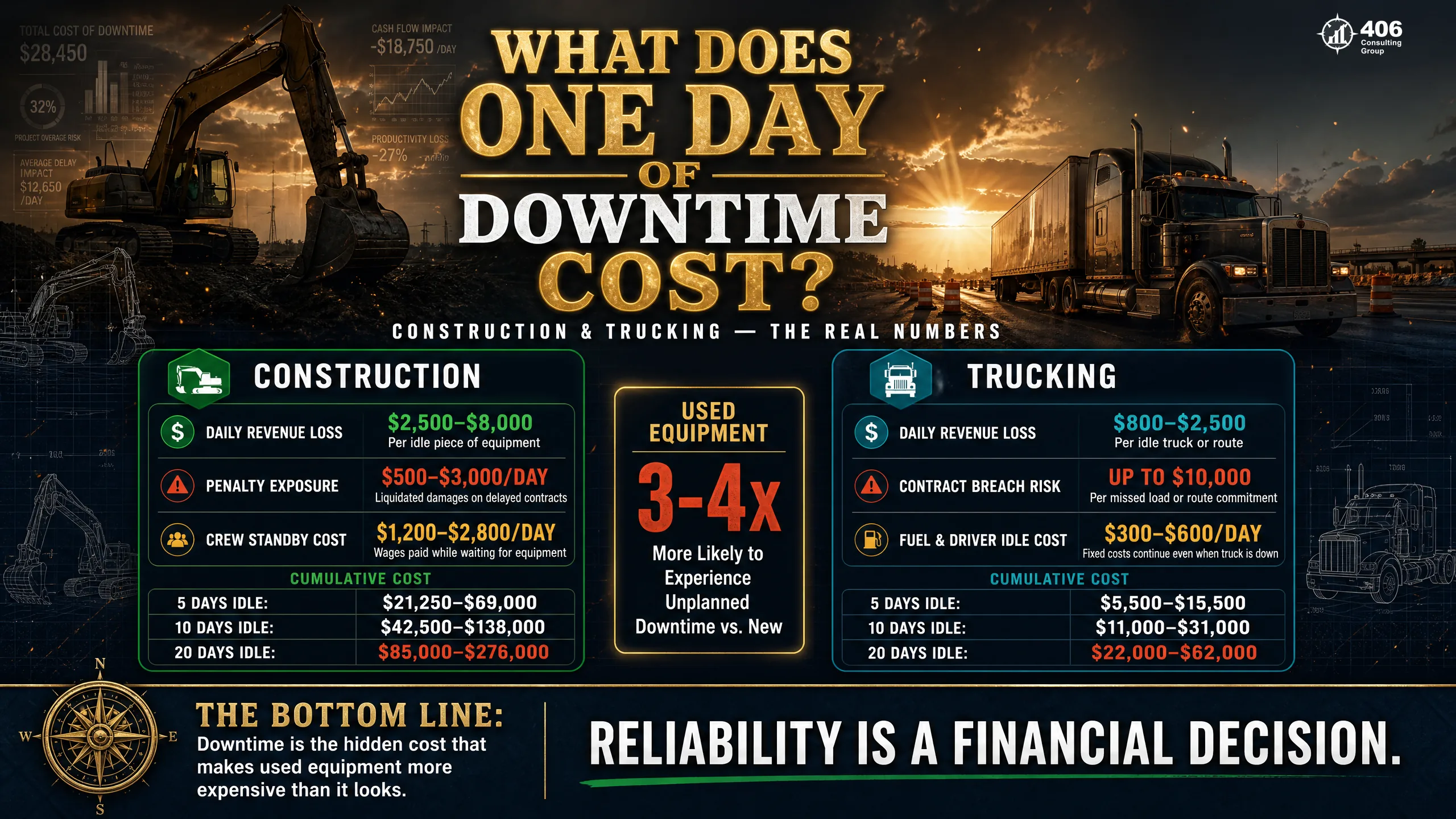

Factor 4: Downtime Risk and the Cost of Being Off the Job

Downtime risk is the factor most owners understand conceptually but fail to quantify. It's not just the repair bill — it's the cascade of costs that starts when a critical piece of equipment goes down mid-job. For construction operations, a single major breakdown at the wrong moment can cost more than the total purchase price gap between new and used equipment.

Construction Operation — One Day Down

Trucking Operation — One Day Down

How to Evaluate Downtime Risk Before Buying Used

- ›Hours: Under 5,000 on heavy iron is generally low-risk. 5,000–8,000 is the risk transition zone. Over 8,000 demands scrutiny on major components.

- ›Make/model reliability: Cat, Komatsu, Deere, Volvo have documented reliability records. Ask your dealer or an independent mechanic which specific model years and configurations to avoid.

- ›Service history documentation: No records = unknown risk. Documented dealer service = lower risk. Owner-maintained with receipts = medium risk.

- ›Pre-purchase inspection: $500–$1,500 from an independent mechanic is mandatory on any used equipment purchase over $50,000. Non-negotiable.

- ›Component remaining life: Ask specifically about engine, hydraulics, transmission, and undercarriage (tracked equipment). Get written estimates on remaining hours before major service.

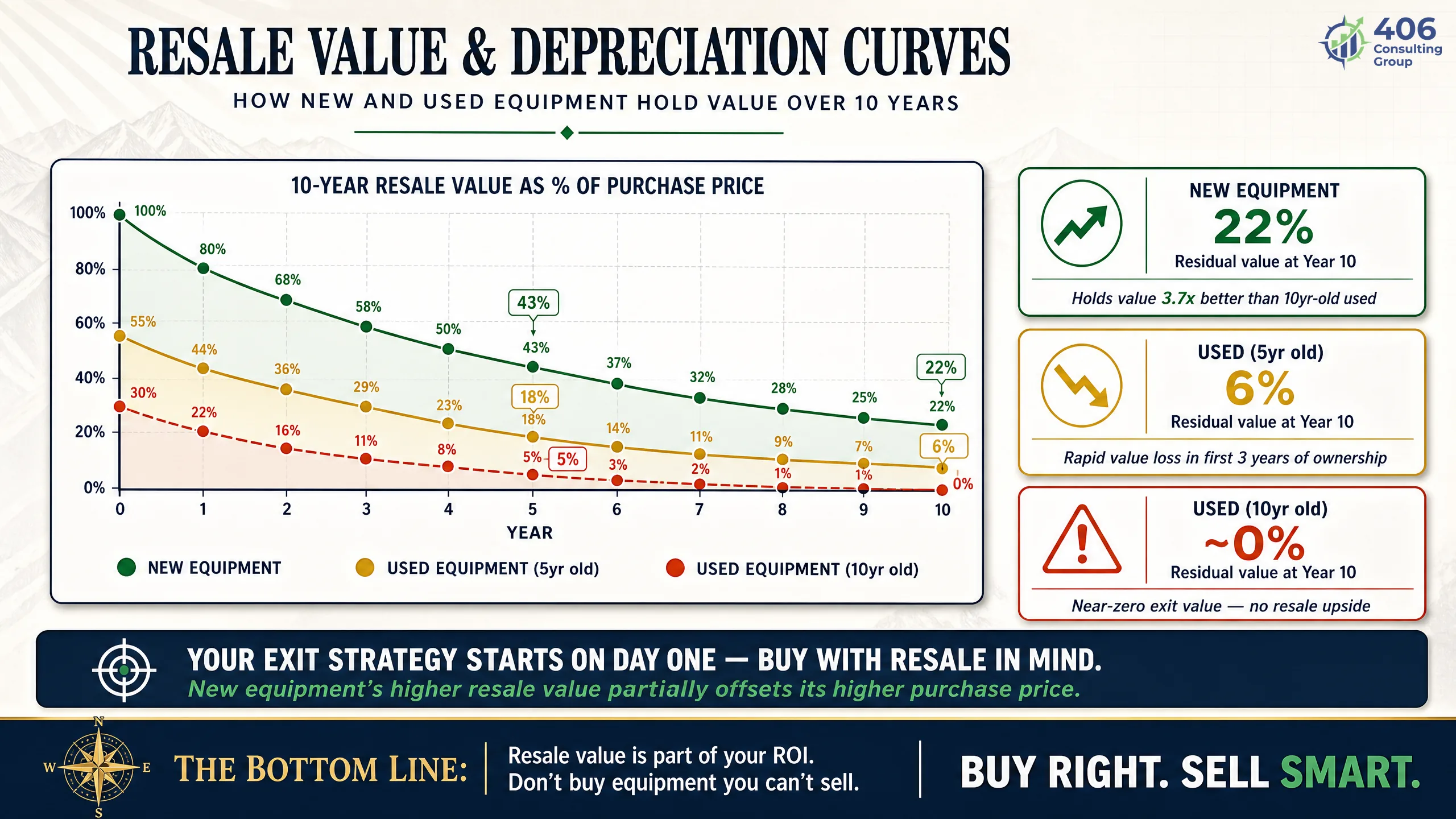

Factor 5: Resale Value and Exit Strategy

Resale value is the factor that makes the total cost of ownership real — because what you sell a piece of equipment for at the end of the ownership period directly affects what it actually cost you to own it. New equipment loses 20–30% in year one but then depreciates more gradually. Well-maintained used equipment with documented service history holds value better proportionally — because you absorbed the new-equipment depreciation cliff for the seller. Poorly maintained or high-hour equipment hits a resale cliff where it becomes expensive to operate and difficult to sell at any reasonable price.

New Equipment

Steep year-1 drop; then moderates. Strong resale if well-maintained.

Well-Maintained Used (3–5 yrs at purchase)

Avoids the new-equipment cliff. Best ROI scenario if maintained.

Deferred-Maintenance Used (8+ yrs)

Cliff risk: accelerating depreciation + high operating costs = ownership trap.

Dealer vs. Auction vs. Private Sale

Dealer trade-in: fastest, lowest price — typically 15–25% below market. Auction (Ritchie Bros., IronPlanet): broad market reach, 30–60 day timeline, 5–8% auction fees. Private sale: highest price but takes 30–120 days and requires active marketing. For exit strategy planning: dealer trade works when you're upgrading and the speed matters; auction works for older equipment or full fleet turnover; private sale works for recent low-hour units with broad market appeal.

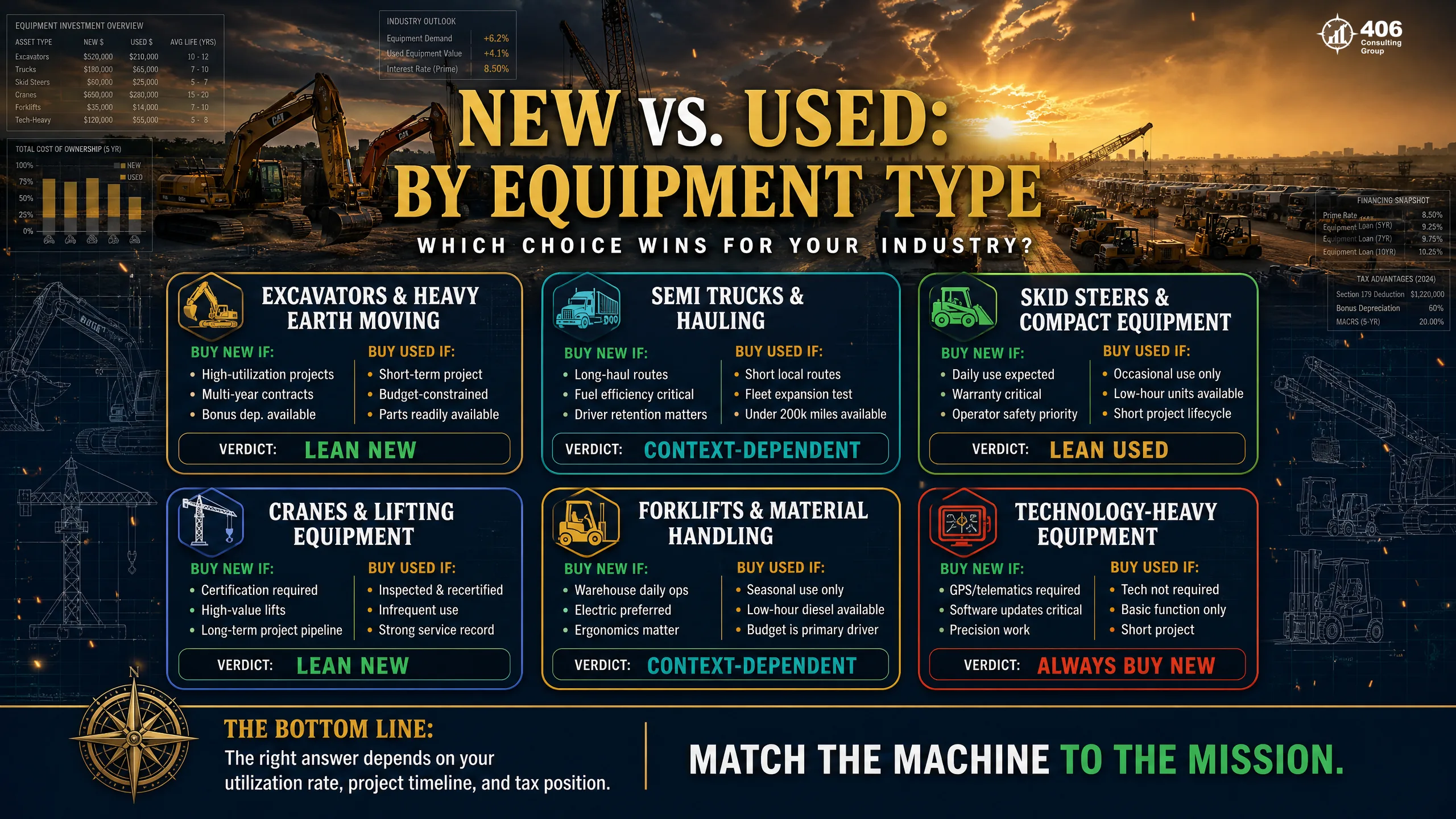

New vs. Used: Side-by-Side by Equipment Type

The new vs. used verdict is not uniform across equipment categories. The downtime risk profile of a skid steer is fundamentally different from a crane. A semi truck has a well-established used market with clear pricing. Here's how the framework applies by equipment type.

| Equipment | New Price Range | Used Price Range | Maint. Premium (used) | Verdict |

|---|---|---|---|---|

| Excavator (20–30 ton) | $280K–$400K | $80K–$190K | 35–55% higher at 8,000+ hrs | Used OK under 6,000 hrs w/ records; new for critical-path jobs |

| Semi Truck (Class 8) | $165K–$200K | $45K–$110K | 40–60% higher at 600K+ miles | Well-established used market; buy 2–4 yr old with certified rebuild |

| Skid Steer / CTL | $55K–$90K | $18K–$45K | 25–40% higher at 4,000+ hrs | Used widely available; low downtime risk; good value if under 3,000 hrs |

| Dump Truck (tri-axle) | $130K–$180K | $35K–$85K | 30–50% higher on older chassis | Used solid with inspection; avoid high-mileage older emissions-tier units |

| Concrete Mixer | $200K–$280K | $55K–$130K | High — drum wear and hydraulic complexity | New preferred for high-utilization fleets; used for lower-cycle operations |

| Tower / Mobile Crane | $400K–$2M+ | $120K–$600K+ | Certification and inspection costs are key variable | Used requires current certification; new preferred for long-term contract work |

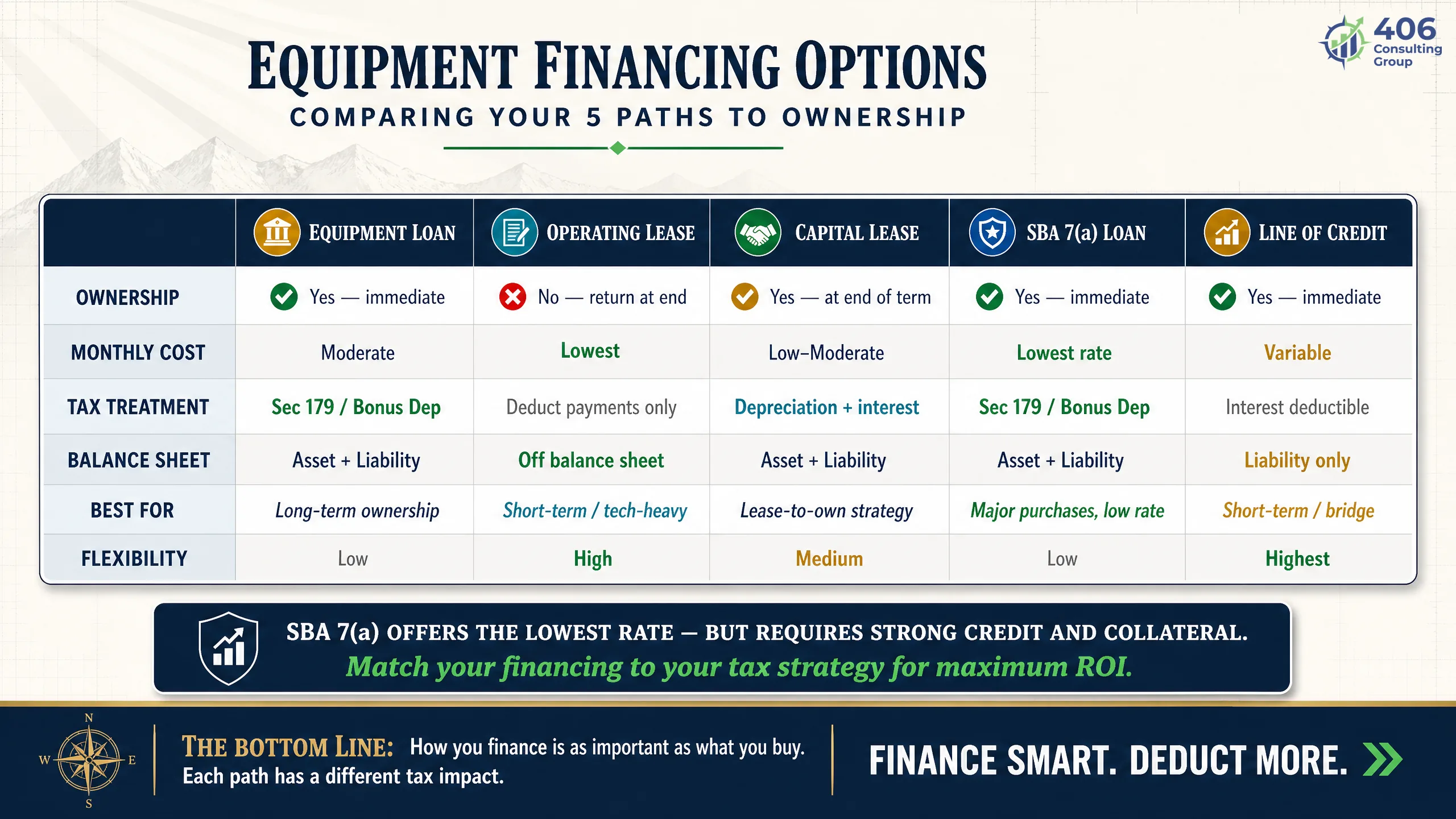

Equipment Financing Options

The financing structure you choose changes the cash flow profile, the tax treatment, and the balance sheet impact of any equipment purchase. Not all financing options work equally well for new vs. used, and some options that work well for new equipment aren't available for older or higher-hours used units. Here's how each option stacks up.

| Financing Type | Ownership | Tax Treatment | Best For | New vs. Used? |

|---|---|---|---|---|

| Equipment Loan | Yes — from day one | Depreciation (bonus / 179 / MACRS) | Long-term ownership; maximize depreciation benefit | Both — best rates on new |

| Operating Lease | No — return at end | Lease payments are operating expense | Lower monthly payment; equipment refresh every 3–5 yrs | New primarily — used lease availability limited |

| Capital / Finance Lease | Yes — at end or via buyout | Depreciation on asset; interest on liability | Ownership intent with lower upfront; balance sheet asset | Both — used eligible if lender approves collateral |

| SBA 7(a) Loan | Yes | Depreciation; longer terms reduce monthly | Longer repayment term; lower monthly payment | Both — used must meet SBA age/condition standards |

| Line of Credit | Yes (if used to purchase) | Depreciation on asset; interest deductible | Short-term bridge or lower-cost used equipment | Used primarily — not efficient for large new equipment |

| Manufacturer Captive | Yes (or lease) | Varies by structure | Lowest rates on new equipment from that manufacturer | New only — Cat, Deere, Kenworth, Volvo, etc. |

Use our Loan Qualification tool to model how an equipment loan affects your DSCR before approaching a lender. For larger purchases, our CFO advisory services include equipment financing structure analysis and lender presentation prep. For SBA equipment loan programs, see SBA.gov.

Montana Considerations

Montana's operating environment creates equipment-specific considerations that national guides don't address. If you're running heavy equipment or trucks in Montana, these factors belong in your new vs. used analysis.

Temperature Extremes and Equipment Wear

Montana winters push diesel equipment to its limits. Cold-start wear in sub-zero temperatures accelerates engine wear on older, pre-Tier 4 equipment without modern cold-weather systems. Hydraulic seals on used equipment with deferred maintenance fail faster in cold. Winter operating costs on older iron are meaningfully higher in Montana than in comparable-climate states — budget for it.

Spring Breakup Road Restrictions

Montana DOT spring road restrictions (typically March–May) limit gross vehicle weights significantly — sometimes down to 50% of normal posted limits. Trucking operations need to model revenue gaps during restriction periods. Equipment financing payments don't pause for breakup season. This affects cash flow planning for trucking fleets and should be part of any equipment purchase analysis.

No Montana Sales Tax Advantage

Montana has no state sales tax. When buying equipment from a dealer in a neighboring state (Idaho, Wyoming, North Dakota), confirm that the transaction can be structured to avoid that state's sales tax with Montana title and registration. On a $200K purchase, avoiding a 6% Idaho sales tax saves $12,000 — a real factor in where you purchase.

Montana Diesel Fuel Tax

Montana's motor fuel tax is 33 cents per gallon for diesel. Heavy equipment operations running high fuel volumes can apply for refund of fuel tax on off-highway use. For high-utilization operations, this refund can be meaningful — and is commonly missed. See MTrevenue.gov.

Short Construction Season

Montana's effective outdoor construction window runs roughly May through October in most of the state, shorter at elevation. This limits annual equipment utilization to 800–1,100 hours for many operations — vs. 1,500–2,000 hours in year-round markets. Lower utilization means the per-hour operating cost premium of used equipment compounds more slowly, which can shift the verdict toward used for seasonal operations.

Montana Equipment Markets

Primary equipment dealer markets: Billings (largest concentration, Cat/Deere/Komatsu/Kenworth/Peterbilt), Missoula (Volvo, Hitachi, Western Star), Great Falls (John Deere, Case). For used equipment, Billings hosts the most active secondary market. Ritchie Bros. runs regional auctions through the region. For auction market intel: IronPlanet.com tracks price history by model and region.

When Used Makes Sense — and When It Doesn't

There is no universal answer to new vs. used — but there are clear decision rules that make the answer obvious in most situations. Here's how to apply the framework to a go/no-go verdict.

Used Makes Sense When:

- ✓Unit is under 6,000 hours (heavy iron) or under 400K miles (trucking) with documented service history

- ✓Independent pre-purchase inspection confirms no major deferred maintenance

- ✓Equipment is not on the critical path of a penalty-clause contract

- ✓Montana seasonal utilization is low enough that per-hour maintenance premium doesn't compound quickly

- ✓Capital is limited and the used unit preserves cash for working capital

- ✓Tax bracket is low enough that the bonus depreciation delta between new and used is not a deciding factor

- ✓Well-established used market for this make/model with predictable resale at exit

New Makes More Sense When:

- ✗Equipment is on the critical path of a contract with liquidated damages clauses

- ✗Annual utilization is high (1,000+ hours) — operating cost premium on used compounds quickly

- ✗Business is in a high enough tax bracket that the larger bonus depreciation on new equipment creates a material year-1 cash advantage

- ✗Available used inventory in acceptable hours/condition is thin or overpriced

- ✗Manufacturer captive financing offers rates that make new competitive with used commercial financing

- ✗Warranty coverage is needed to satisfy bonding or contract insurance requirements

- ✗Long-term ownership (7+ years) planned — new delivers better cumulative operating economics over a full ownership cycle

The Decision Checklist Before You Sign Anything

Use this checklist before committing to any equipment purchase — new or used. Items marked with a star are non-negotiable for used equipment.

Financial Analysis

- Built a 5-year total cost of ownership model (not just sticker price)

- Modeled tax treatment: bonus depreciation or Section 179 impact at your actual tax rate

- Compared financing options from at least 3 sources (captive, bank, SBA)

- Calculated monthly payment impact on DSCR — confirmed lender covenant compliance

- Modeled downtime cost scenario: what does 10 days down cost this operation?

- Planned exit strategy: dealer trade, auction, or private at target resale date

Used Equipment Specific ★

- ★ Independent pre-purchase inspection completed by qualified mechanic ($500–$1,500)

- ★ Last 12 months maintenance records reviewed — actual parts/labor spend documented

- ★ Hours meter verified and cross-referenced with service records

- ★ Remaining component life estimated: engine, hydraulics, transmission, undercarriage

- ★ Financing confirmed — lender approved collateral value on this specific unit's age/hours

- Comparable market auction data pulled (IronPlanet, Ritchie Bros.) for this model/year/hours

For operations using job costing to track equipment profitability, our Job Costing tool and construction bookkeeping services include equipment cost allocation and operating cost per hour tracking — so you'll have real data for the next equipment decision instead of estimates.

Frequently Asked Questions

Does used equipment qualify for bonus depreciation and Section 179?

Yes — both new and used equipment qualify for 100% first-year bonus depreciation under the OBBBA, which made it permanent as of July 2025. Used equipment must be "new to you" (not previously owned by your entity or a related party) to qualify. Section 179 also applies to used equipment. The tax benefit is the same percentage — but because new equipment costs more, the absolute dollar value of the deduction is larger on a new purchase.

What hours on used heavy construction equipment are considered too high?

General benchmarks: under 5,000 hours on an excavator or dozer is typically low-risk with a clean service history. 5,000–8,000 hours is the transition zone — still buyable but warrants a full independent inspection and component-life assessment. Over 8,000 hours demands documented evidence of major component rebuilds (engine, hydraulics, final drives) or a significant price discount that accounts for near-term overhaul costs. For trucking, under 400,000 miles is broadly considered manageable; 400,000–700,000 with documented maintenance is in the risk zone; over 700,000 typically means major driveline costs are imminent.

Can I get an SBA loan to buy used construction equipment?

Yes. SBA 7(a) loans can finance used equipment purchases, but the equipment must meet SBA eligibility standards — the equipment generally cannot be older than 10–15 years at loan maturity (depending on lender). SBA also requires that the equipment be in good working condition. For higher-hours or older units, conventional equipment lenders or a business line of credit may be a better fit than SBA. The SBA 504 program is generally for real estate and large fixed assets, not used equipment.

Is it better to lease or buy construction equipment?

Operating leases make sense when: you want lower monthly payments, you prefer to refresh equipment every 3–5 years, or the equipment is not central to long-term business value. Purchasing (via loan) makes sense when: you want to own the asset and capture depreciation benefits, you plan to keep the equipment for 7+ years, or you want to build equity to use as collateral on future financing. For Montana construction operations with high seasonal utilization, ownership and bonus depreciation often produce better economics than leasing — but run both scenarios with your specific numbers.

How does Montana's spring road restriction affect equipment financing decisions?

Spring breakup restrictions (typically March through May in most of Montana) can reduce trucking revenue by 30–60% during that window — but financing payments continue. This creates a predictable seasonal cash flow trough that must be planned for. Before purchasing trucking equipment, model a cash flow projection that explicitly accounts for restricted-weight revenue during breakup season. Lenders who understand Montana operations will expect to see this in your projections. If the restricted-season cash flow doesn't cover debt service, you need a line of credit or operating reserve to bridge it.

What's the biggest financial mistake construction companies make when buying equipment?

Buying on purchase price alone and skipping the operating cost and downtime analysis. The second most common: not getting an independent pre-purchase inspection on used equipment. A $750 inspection fee that surfaces a $25,000 engine issue is the best equipment ROI you'll ever generate. The third: not running the tax treatment numbers — many construction companies buy used to save cash upfront and leave $30,000–$70,000 in bonus depreciation tax savings on the table because they didn't model the new equipment scenario.

Equipment Finance

Ready to Run the Numbers on Your Next Equipment Decision?

406 Consulting Group builds the full 5-factor ROI analysis for construction and trucking equipment purchases — tax treatment, financing structure, operating cost baseline, and the downtime risk math most owners skip. We've seen both sides of the decision from the underwriting desk.

406 Equipment ROI Framework

All 5 factors before you sign

Purchase Price & Financing

Down payment, rate, true monthly cost

Tax Treatment

Bonus depreciation, Section 179, MACRS

Operating Cost Baseline

Maintenance, fuel, insurance per hour

Downtime Risk

Probability-weighted breakdown cost

Resale Value & Exit

Projected value at ownership exit

Key Numbers

Free Tools

Our Services

Related Guides