Trump Accounts for Kids:

What Montana Families & Business Owners Need to Know

Ryan owns Glacier Electric in Kalispell — and just found a benefit that beats a raise. Trump Accounts give kids a $1,000 head start, and let business owners contribute $2,500 tax-free per employee. Here's exactly how they work in 2026.

Ryan owns Glacier Electric in Kalispell — 14 employees, about $2.4 million in revenue, and a reputation for treating his crew well. Last month one of his best foremen, a guy with a new baby, told Ryan he was thinking about taking a job with a bigger outfit down in the valley for an extra $2 an hour. Ryan didn't have a benefit to counter with. He does now, and it's called a Trump Account — one of the most useful and least understood pieces of the 2025 tax law for Montana families and business owners alike.

Starting July 4, 2026, Ryan can put up to $2,500 a year into a Trump Account for that foreman's child — tax-free to the employee, deductible to Glacier Electric. It costs Ryan less than a $2/hour raise, it's worth more to a new parent, and almost none of his competitors know it exists yet. That's the part of the Trump Account conversation that most articles skip: this isn't only a savings account for your own kids. For a business owner, it's a recruiting and retention tool hiding inside a tax law.

Trump Accounts were created by the One Big Beautiful Bill Act — officially the Working Families Tax Cuts — signed into law on July 4, 2025. Every eligible American child born from 2025 through 2028 gets a one-time $1,000 deposit from the federal government. Families can add up to $5,000 a year. The money is invested in the stock market and grows for decades. As of mid-2026, roughly 4 million children have already been signed up and about 1 million have claimed the $1,000.

This guide covers what a Trump Account actually is, who gets the free $1,000, the employer contribution move that most Montana business owners are missing, how the money is taxed (it is not a 529 — that trips people up), and where it fits alongside a 529 plan and a Roth IRA. We'll use Ryan and Glacier Electric throughout so you can see exactly where you fit.

By Carrie Anderson — Co-Founder, 406 Consulting Group. Background in commercial banking and underwriting (300+ loan reviews) plus small business tax and financial strategy across Montana.

Quick Answer: Trump Accounts in One Box

- →Free $1,000: A one-time federal deposit for U.S. citizen children born Jan 1, 2025 – Dec 31, 2028. You have to claim it (Form 4547 or TrumpAccounts.gov).

- →$5,000/year limit: Parents, family, and employers can add up to $5,000 total per child, per year. Contributions can't start before July 4, 2026.

- →Business owner move: An employer can contribute up to $2,500 per employee per year — tax-free to the employee, deductible to the business.

- →Invested in the market: Money must go into a low-cost fund tracking a U.S. stock index (think S&P 500) and grows tax-deferred.

- →Taxed like a traditional IRA, not a 529: No withdrawals until the year the child turns 18, then it becomes a traditional IRA. Withdrawals are taxed as ordinary income.

Table of Contents

What Is a Trump Account? (The 30-Second Answer)

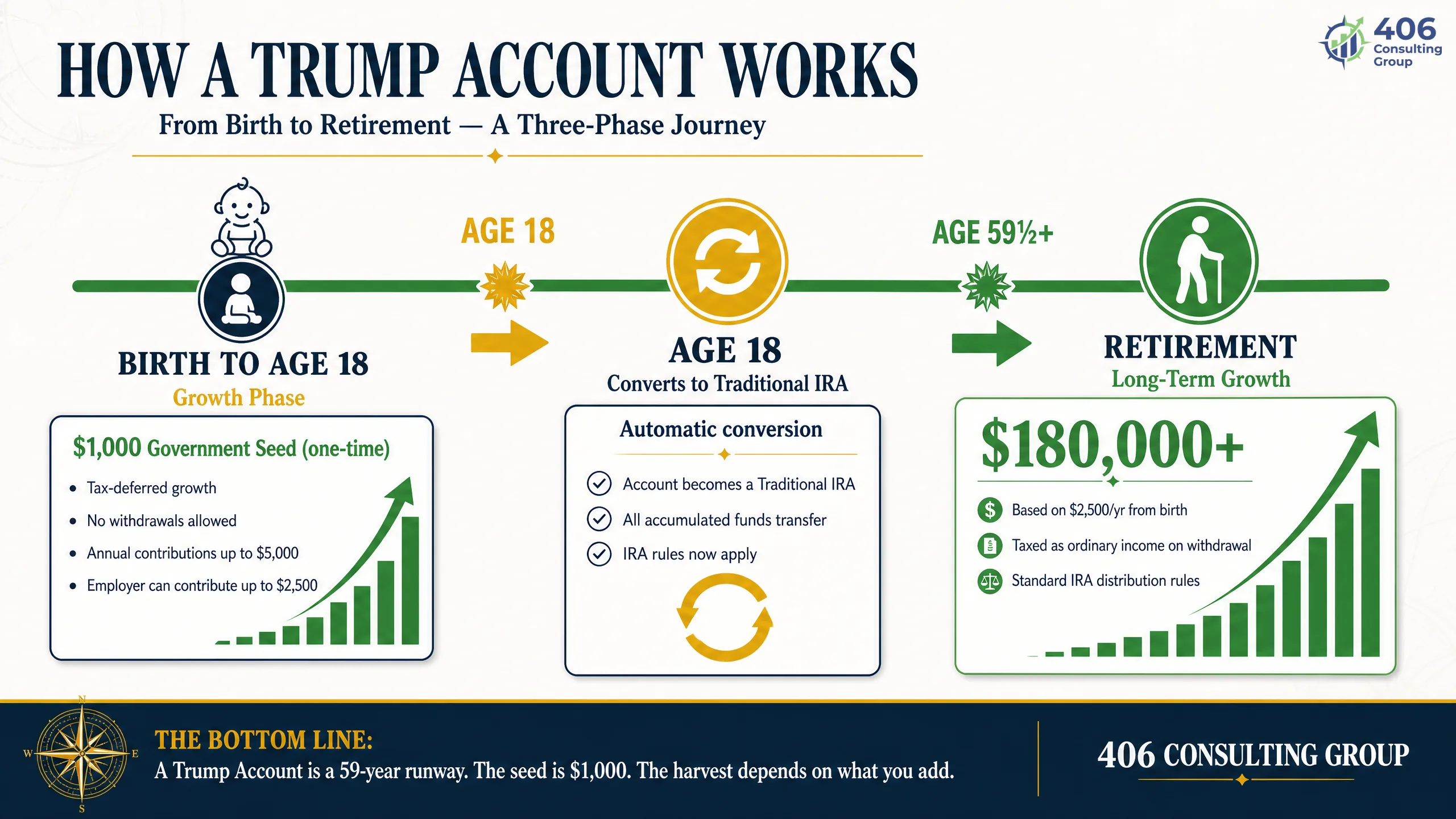

The short answer: a Trump Account is a tax-deferred investment account for a child, seeded with a one-time $1,000 from the federal government, that grows in the stock market until the child turns 18 and then converts into a traditional IRA. Think of it as a retirement account that starts at birth instead of at your first job.

Here is the plain-English version. When Ryan's daughter was born in early 2026, the government set aside $1,000 in an account with her name on it — once Ryan claims it. That money gets invested in a fund that tracks the U.S. stock market. Ryan, his parents, or anyone else can add to it, up to $5,000 a year. Nobody touches the money until the year she turns 18. From that point forward, it behaves exactly like a traditional IRA — it keeps growing tax-deferred, and when she eventually pulls money out, she pays ordinary income tax on the growth.

Define it once: "tax-deferred"

Tax-deferred means the account grows every year without you paying tax on the gains along the way — the tax bill comes later, when the money is withdrawn. That is different from "tax-free" (a Roth or a 529 used for college), where qualified withdrawals are never taxed. This single distinction is the most important thing to understand about a Trump Account, and it's the one most people get wrong. We cover the tax treatment in full in Section 6.

Who Qualifies — and Who Gets the Free $1,000

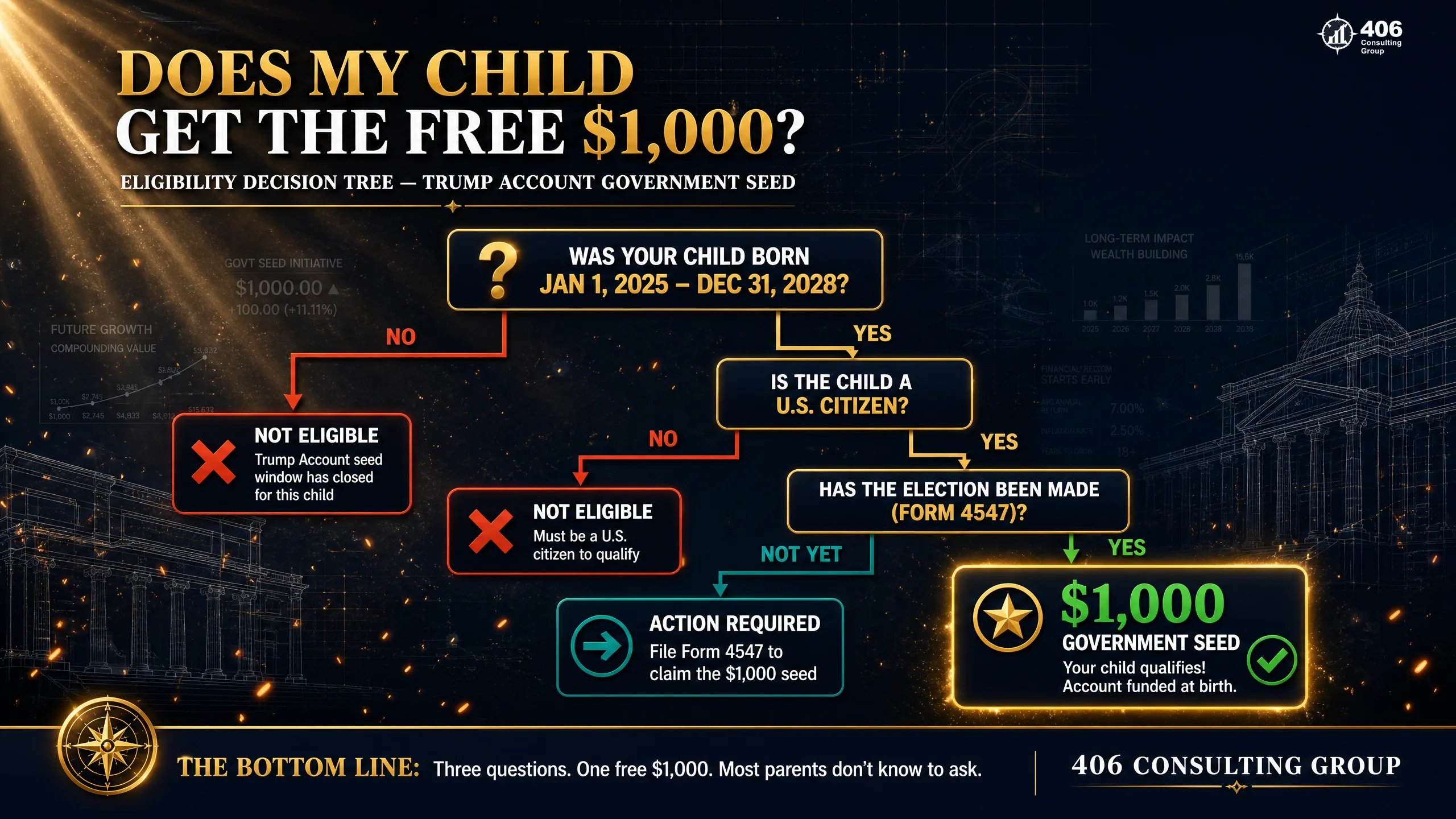

The short answer: any child under 18 can have a Trump Account, but the free $1,000 government deposit only goes to U.S. citizen children born between January 1, 2025 and December 31, 2028. Miss that birth window and you can still open and fund an account — you just don't get the seed money.

To get the free $1,000 seed

- Child is a U.S. citizen at birth

- Child is born Jan 1, 2025 – Dec 31, 2028

- Child has a Social Security number

- Parents have work-eligible Social Security numbers

- An election is made for the child (Form 4547 or the online portal)

To open an account (no seed)

- Any child under age 18 with a Social Security number

- Born before 2025 or after 2028 — still eligible to open and grow the account

- Family, others, and employers can still contribute up to $5,000/year

- You simply won't receive the one-time $1,000 federal deposit

Don't leave $1,000 on the table

The $1,000 is not automatic — you have to make the election. As of mid-2026, about 4 million children had been signed up but only around 1 million had actually claimed the $1,000 pilot contribution. That gap is families who qualify and haven't filed. If you had a baby in 2025 or 2026, this is a form worth filing this week. Glacier Electric's foreman qualified for his newborn and had no idea until Ryan mentioned it.

The Business Owner's Edge: $2,500 Tax-Free Per Employee

The short answer: yes, your business can contribute to your employees' Trump Accounts — up to $2,500 per employee per year — and that contribution is tax-free to the employee and deductible to the business. It's one of the few benefits in the tax code that costs a small business relatively little and lands as real money in an employee's family.

Here's why it matters for a Montana employer. A $2,500 raise isn't really $2,500 to your employee — after federal income tax, Montana income tax, and the employee's share of payroll taxes, a $2,500 raise might net them $1,700 in their pocket. And it costs you more than $2,500, because you owe the employer share of payroll taxes on top. A $2,500 Trump Account contribution flips both sides: the employee keeps the full $2,500 (no income tax, and it's not treated as wages), and you deduct it without the payroll-tax add-on.

Glacier Electric — Raise vs. Trump Account Contribution

A $2,500 raise

Cost to Glacier Electric: ~$2,691 (raise + 7.65% payroll tax)

Employee income + payroll tax: ~$800 lost

What the family actually keeps: ~$1,700

A $2,500 Trump Account contribution

Cost to Glacier Electric: $2,500 (fully deductible)

Employee income + payroll tax: $0

What the family actually keeps: $2,500 — invested for the child

Same rough cost to the business. The Trump Account version delivers roughly 47% more value to the employee's family — and it goes into an investment account with that child's name on it, which is a very different thing to talk about at a job interview than "we match a little on the 401(k)."

The rules on employer contributions — in plain English

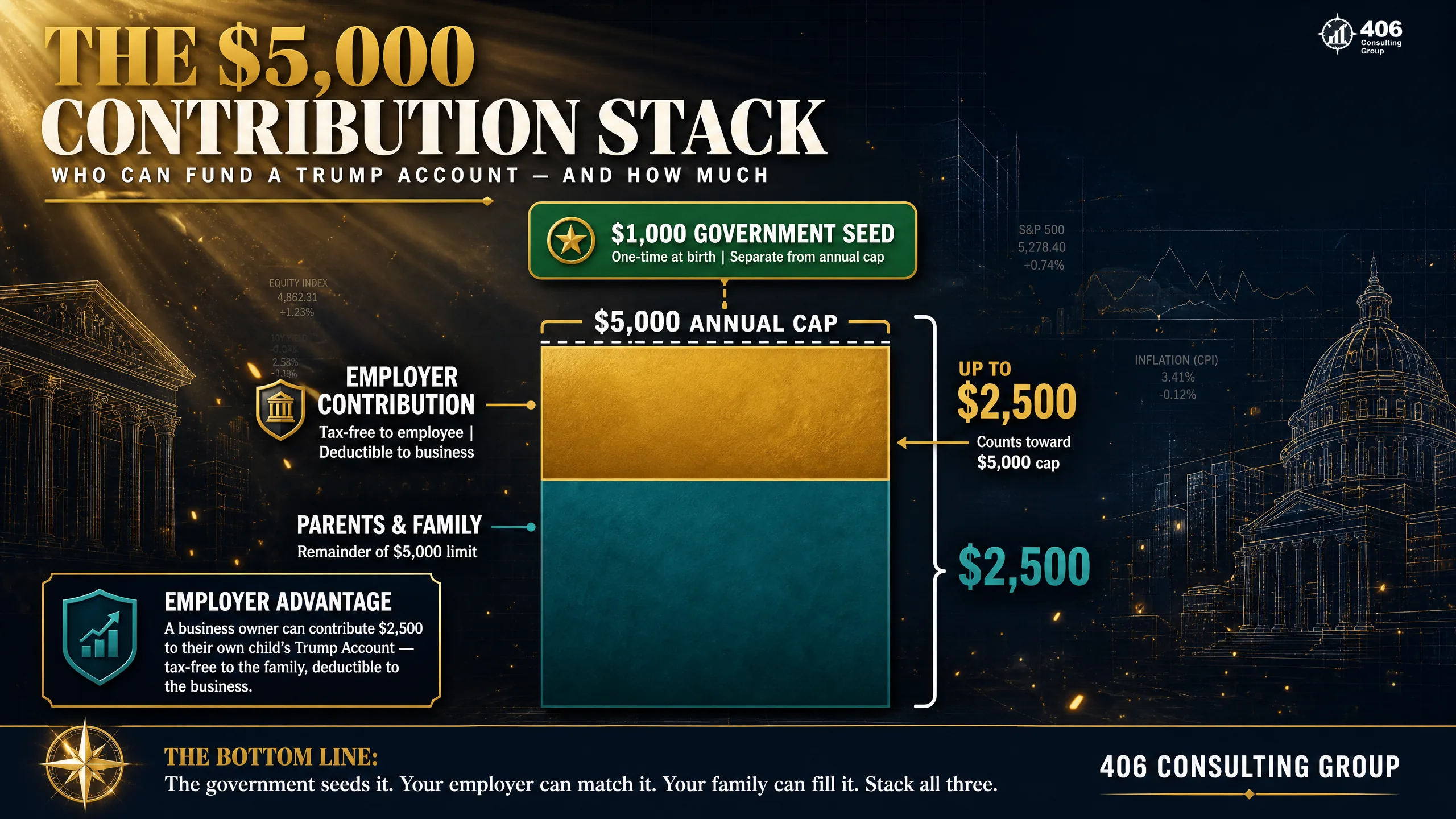

Up to $2,500 per employee, per year

The limit is per employee — not per child. If an employee has three kids with Trump Accounts, the $2,500 is split across them; it does not become $7,500.

It counts toward the $5,000 annual cap

The employer's $2,500 is part of the $5,000 total, not on top of it. If you contribute $2,500, the family can add up to $2,500 more that year.

Tax-free to the employee

The contribution is excluded from the employee's taxable wages — it doesn't show up as income on their W-2.

Deductible to the business

You deduct it as a compensation/benefit expense, like other fringe benefits.

Can cover an employee's child or a young employee

The contribution can go to the Trump Account of an employee's dependent child — or of a minor/young employee themselves.

How to Set Up an Employer Trump Account Program

A Trump Account contribution program runs through the same part of your business that handles payroll and benefits. You don't need to become a benefits expert — you need a written program, a consistent rule for who gets what, and a bookkeeper or payroll partner who codes it correctly so the deduction and the tax-free treatment both hold up.

Decide who's eligible and how much

Ryan chose a simple rule for Glacier Electric: any full-time employee past 90 days with a child who has a Trump Account gets $1,500 a year, and anyone past three years gets the full $2,500. A clear, written rule keeps it fair and keeps it defensible if the IRS ever asks.

Put the program in writing

The contribution has to be made under an employer Trump Account contribution program — meaning a documented plan, not a one-off gift to a favorite employee. This is the step business owners skip, and it's the one that protects the tax treatment.

Confirm which employees have accounts open

You can only contribute to an account that exists. Part of rolling this out is helping employees open Trump Accounts for their kids (Form 4547 or TrumpAccounts.gov) so the contributions have somewhere to land.

Run it through payroll correctly

The contribution is excluded from the employee's taxable wages and deducted by the business — but only if it's recorded that way. Coded as a regular bonus, it becomes taxable wages and you lose the entire advantage. This is a bookkeeping-setup question, not a guess.

Communicate it as a benefit

The whole point is retention and recruiting. If your crew doesn't understand what they're getting, you've spent the money without getting the loyalty. Put it in the offer letter and the annual benefits summary.

Glacier Electric's math across the crew

Ryan has 9 employees with young kids who'll open accounts. At an average of about $2,000 each, that's roughly $18,000 a year — fully deductible, so the after-tax cost to the business is closer to $13,500 once you account for the deduction. For a $2.4M contractor fighting to keep skilled tradespeople, $13,500 to hand every young parent on the crew a growing investment account for their child is one of the cheapest retention tools he's ever found. We help owners size this against their payroll through our payroll services and tax planning.

The Rules That Actually Matter: Limits, Timing, and Investments

There are three rules that determine what you can actually do with a Trump Account: how much you can put in, when you can start, and how the money has to be invested. Get these three right and everything else follows.

Rule 1 — The $5,000 annual contribution limit

Parents, grandparents, other family, and employers can add up to $5,000 combined per child, per year during the growth phase (birth to 18). The limit is indexed to inflation starting after 2027. The one-time $1,000 government seed does not count against this limit, and neither do certain qualified rollovers. The employer's $2,500 does count toward the $5,000. For comparison, that $5,000 is actually below the traditional IRA limit ($7,000 in 2026) — but a Trump Account can be funded from birth, decades before a child ever earns a paycheck.

Rule 2 — Contributions can't start before July 4, 2026

This is the timing catch. The accounts and the $1,000 seed exist now, but no family or employer contributions could be made before July 4, 2026. That date has just passed — which is exactly why this is the moment to set up your plan. You can make the eligibility election and claim the $1,000 before you're able to add your own money.

Rule 3 — The money must be invested in a U.S. stock index fund

You don't get to pick individual stocks or park it in bonds. Trump Account money must be invested in a low-cost mutual fund or ETF that tracks the S&P 500 or a similar broad U.S. equity index. For a long time horizon — 18 years or more — a low-fee stock index fund is exactly what most advisors would recommend anyway, so this restriction is less limiting than it sounds. It also keeps fees low, which matters enormously over 18 years of compounding.

| The number | What it is |

|---|---|

| $1,000 | One-time federal seed for U.S. citizen kids born 2025–2028 (doesn't count toward the annual limit) |

| $5,000 | Annual contribution limit from all sources combined, indexed after 2027 |

| $2,500 | Maximum tax-free employer contribution per employee per year (counts toward the $5,000) |

| July 4, 2026 | First date family and employer contributions are allowed |

| Age 18 | First year money can be withdrawn; account converts to a traditional IRA |

| Form 4547 | The IRS form to elect a Trump Account (or use TrumpAccounts.gov) |

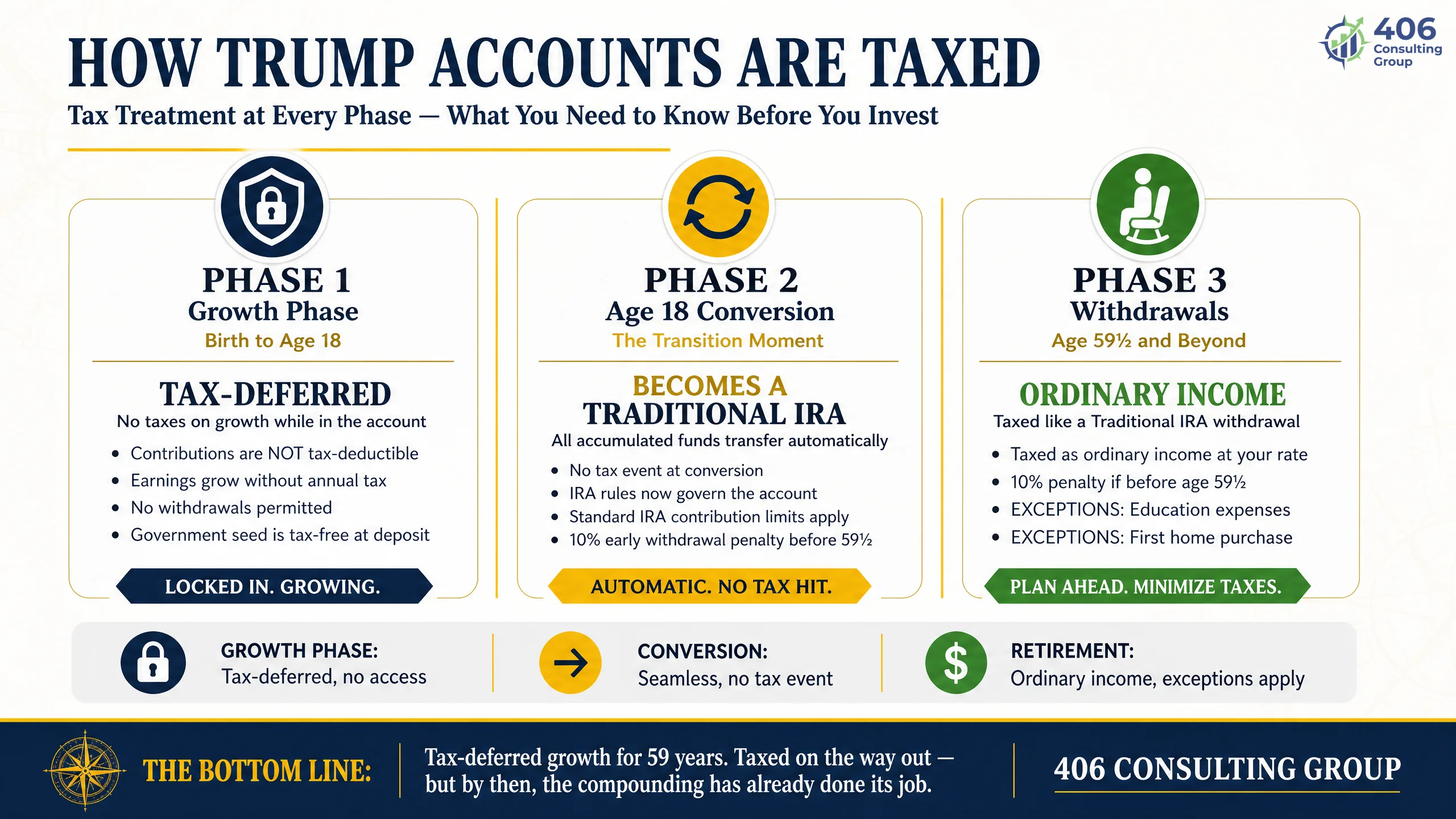

How Trump Accounts Are Taxed

The short answer: a Trump Account grows tax-deferred, and once the child turns 18 it becomes a traditional IRA — so withdrawals of the growth are taxed as ordinary income, with a 10% penalty if money comes out before age 59½ unless an exception applies. This is the single biggest misunderstanding about Trump Accounts. It is not a 529, and it is not a Roth. Treating it like tax-free college money is a costly mistake.

Phase 1 — Growth (birth to 18)

The money is invested and grows tax-deferred. No tax is due on the gains year to year, and no withdrawals are allowed (except in narrow cases like the death of the beneficiary). This is the compounding engine — 18 years of untaxed growth.

Phase 2 — Conversion at 18

Starting January 1 of the year the child turns 18, the account is treated as a traditional IRA and follows traditional IRA rules from there. The child now controls it.

Phase 3 — Withdrawals

Because it's now a traditional IRA, withdrawing the growth is taxed as ordinary income. Take money out before age 59½ and you generally add a 10% early-withdrawal penalty — unless it fits an exception like qualified higher-education expenses or up to $10,000 for a first home. The portion representing after-tax contributions comes back out tax-free; the growth and any pre-tax dollars (the seed, employer contributions) are taxed.

Why "it's not a 529" matters in real dollars

Say Ryan's daughter has $60,000 in her Trump Account at 18 and uses it for college. Unlike a 529 — where qualified education withdrawals are completely tax-free — pulling from the Trump Account is a traditional-IRA distribution. The higher-education exception spares her the 10% penalty, but the growth is still taxed as ordinary income in the year she withdraws it. That's the difference between a Trump Account and a 529, and it's why the two tools do different jobs. We line them up side by side in the next section.

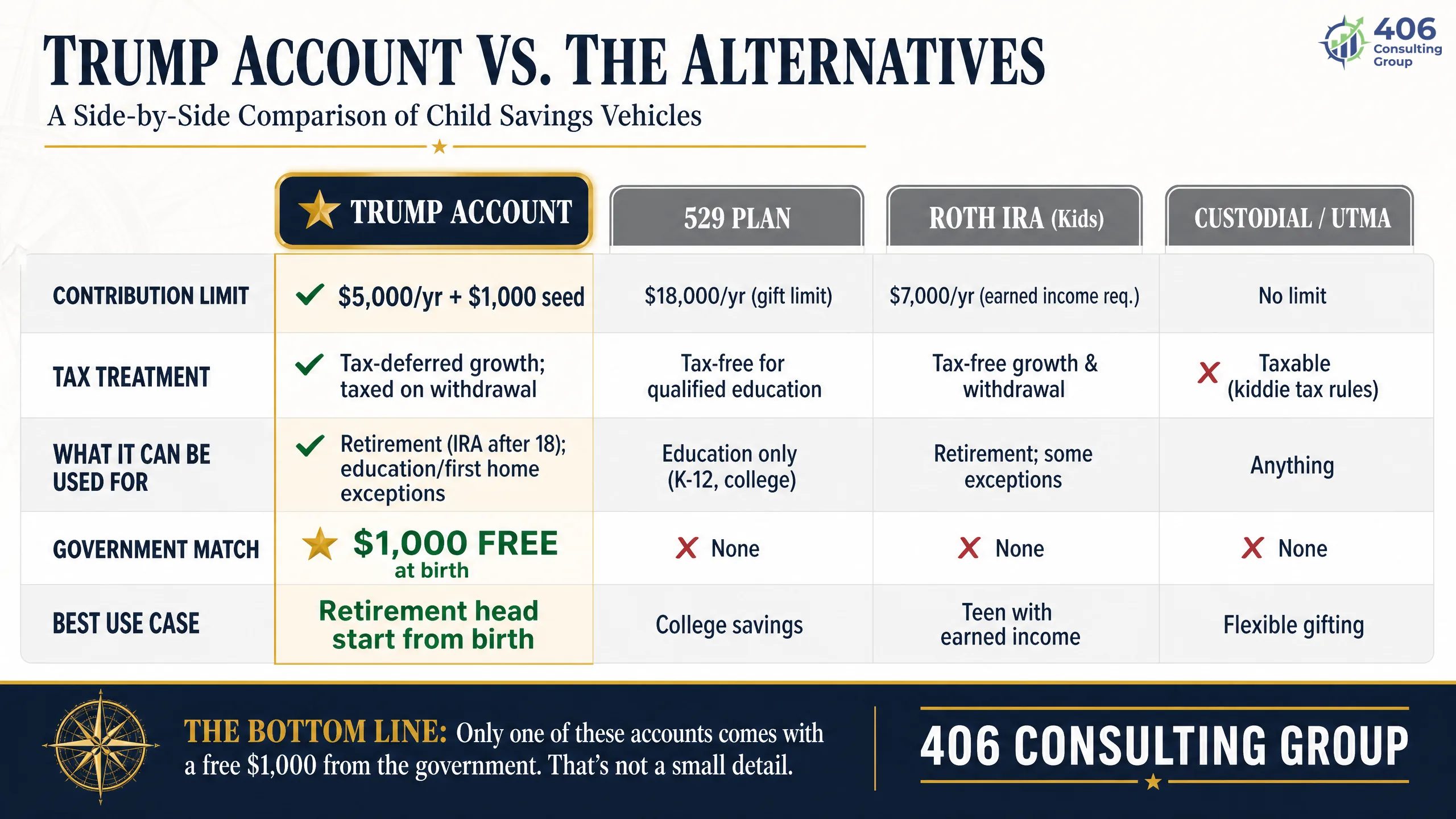

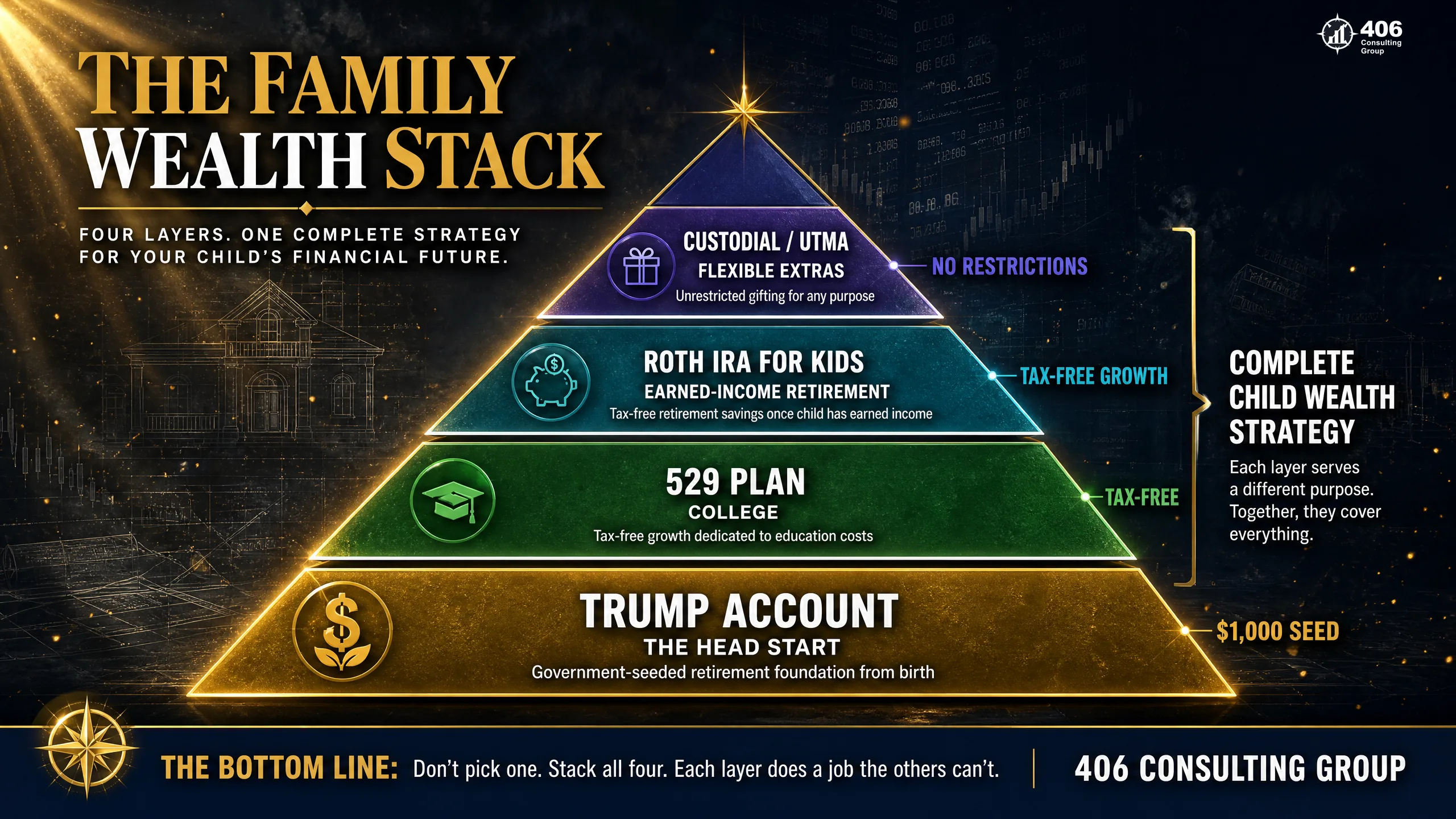

Trump Account vs. 529 vs. Roth vs. Custodial — The Family Wealth Stack

The short answer: a Trump Account is not a replacement for a 529 or a Roth IRA — it's a new layer that sits alongside them. Each account does a specific job. We call the way they fit together the Family Wealth Stack: the Trump Account is the head-start base, the 529 handles college, a Roth handles earned-income retirement savings, and a custodial account covers flexible extras. Stop asking "which one?" and start asking "which one for which goal?"

| Feature | Trump Account | 529 Plan | Roth IRA (kids) | Custodial (UTMA) |

|---|---|---|---|---|

| Annual limit | $5,000 | Very high (gift-tax limits) | $7,000 (2026) or earned income | No limit (gift-tax limits) |

| Government match | $1,000 seed (2025–2028) | None (state deduction may apply) | None | None |

| How growth is taxed | Tax-deferred | Tax-free | Tax-free | Taxable (kiddie tax) |

| Withdrawals taxed? | Ordinary income (like IRA) | Tax-free for education | Tax-free in retirement | Capital gains as incurred |

| What it's for | Long-term / retirement head start | College & K–12 tuition | Retirement (needs a job) | Anything for the child |

| Needs earned income? | No | No | Yes | No |

| Investment choice | U.S. stock index only | Plan menu | Wide open | Wide open |

The Family Wealth Stack — which account for which job

Base — Trump Account

Claim the free $1,000 and let it compound. This is the retirement head start you fund first because part of it is free money.

Layer 2 — 529 Plan

This is your college vehicle. Tax-free for tuition, and in Montana you get a state income tax deduction for contributing (a Trump Account gives you no such deduction).

Layer 3 — Roth IRA for the child

The moment your kid has real earned income — a summer job, working in your business — a Roth turns those wages into tax-free retirement dollars.

Top — Custodial / UTMA

Maximum flexibility for anything else: a car, a first apartment, a business idea. No restrictions on use, but no tax advantages either.

Most Montana families won't max all four. The Stack is about sequence: claim the free $1,000 first, then fund the layer that matches your biggest goal.

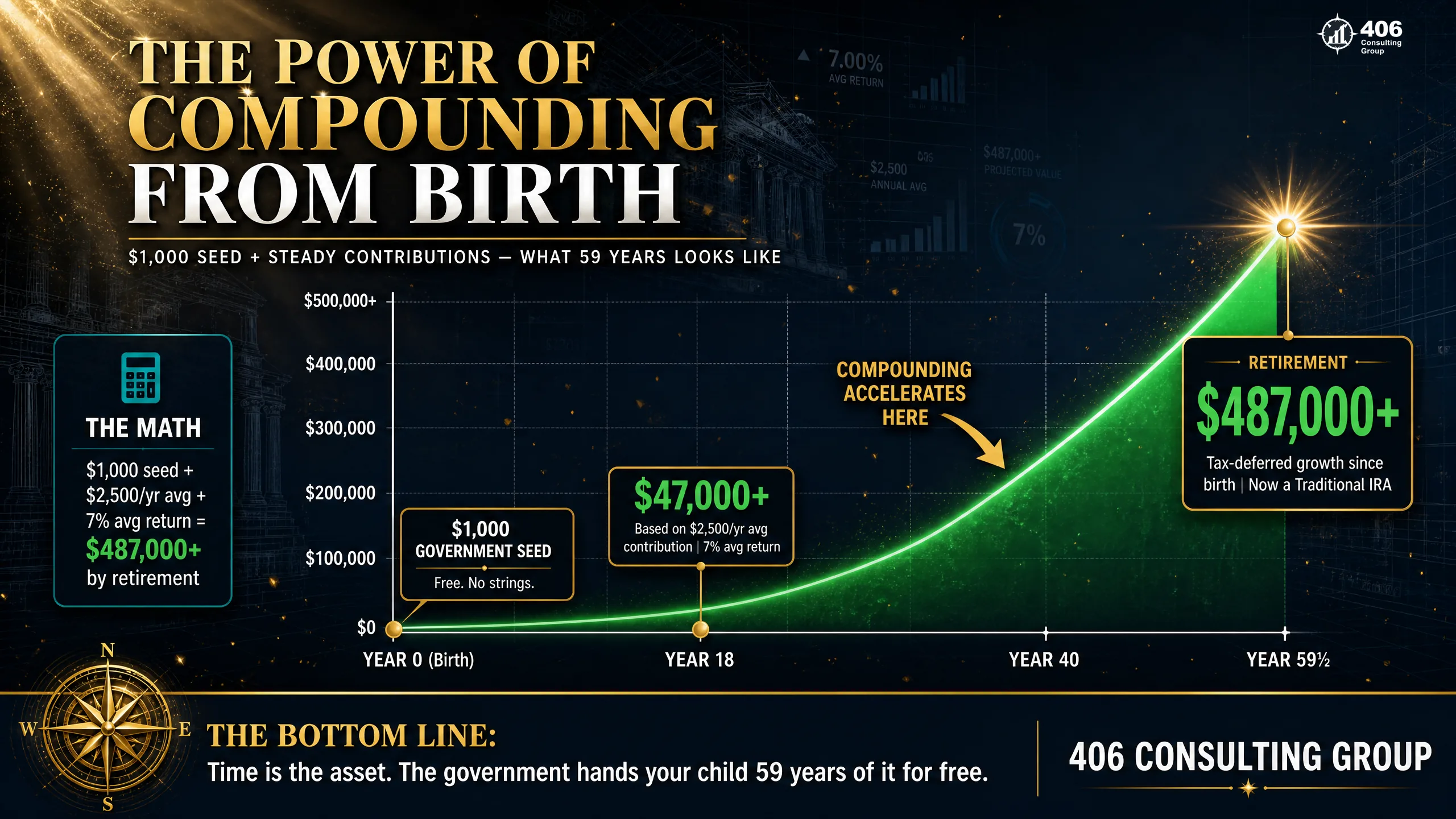

Running the Numbers: What It Actually Grows To

The short answer: the power of a Trump Account isn't the $1,000 — it's 18 years of compounding on top of it, and then decades more once it becomes an IRA. Here's what different contribution levels turn into by age 18, and why the number gets genuinely large if the money is left alone.

| Yearly contribution | Total you put in by 18 | Balance at 18 (~7%/yr) |

|---|---|---|

| $0 (just the $1,000 seed) | $1,000 | ~$3,400 |

| $1,000/year | $19,000 | ~$37,000 |

| $2,500/year (employer-funded) | $46,000 | ~$88,000 |

| $5,000/year (the max) | $91,000 | ~$173,000 |

Illustrative only, assuming a 7% average annual return on a U.S. stock index over 18 years. Actual returns vary and markets can lose money in any given year.

The "even if you never add a dollar" point

Here's the line that should get every eligible parent to file the form: if you claim the $1,000, add nothing else, and simply leave it alone, that single deposit could grow to roughly $81,000 by the time your child is 65 — from money you didn't put in. Claiming the seed is the highest-return five minutes of paperwork you'll do this year.

What This Means for Montana Families and Employers

Trump Accounts are a federal program, so the core rules are the same in Kalispell as they are anywhere else. But a few Montana-specific realities change how the accounts fit into a family's or a business owner's plan.

Montana's income tax still applies later

Montana taxes pass-through income at rates topping out around 5.9%, dropping to 5.65% in 2026. Because Trump Account withdrawals are taxed as ordinary income at the federal level, your child will likely owe Montana income tax on that growth too when they withdraw it as an adult. That's another reason a Trump Account is a long-term, low-touch account — not a short-term college fund.

The 529 keeps a Montana-only edge

Montana gives residents a state income tax deduction for contributing to a 529 (Achieve Montana) — generally up to $3,000 per taxpayer, or $6,000 for a married couple. A Trump Account gives you no state deduction. So for college dollars specifically, the 529 is still the more tax-efficient layer for a Montana family.

No state sales tax doesn't change this

Montana having no general sales tax is great for your day-to-day, but it's irrelevant to Trump Accounts — this is an income-tax-and-investment question. Don't let the lack of sales tax lull you into skipping the income-tax planning on the back end.

A rare edge for small Montana employers

Montana's economy runs on small businesses — contractors, trades, ranches, main-street shops. The $2,500 tax-free employer contribution is a benefit a 12-person Kalispell contractor can actually afford, and it competes with what big out-of-state employers offer. Confirm Montana's income-tax treatment of the employer contribution with your advisor, since state conformity to new federal exclusions can lag.

Glacier Electric's takeaway

Ryan does two things: he claims the $1,000 for his own daughter and layers a 529 on top for her college (for the Montana deduction), and he rolls out a Trump Account contribution program for his crew as a retention benefit. Same law, two different plays — one for his family, one for his business. That's how most Montana owners should think about it.

5 Mistakes That Cost Families Money

Not claiming the free $1,000

About 3 in 4 signed-up kids hadn't claimed the $1,000 as of mid-2026. If your child was born 2025–2028 and you haven't filed the election, you're leaving free money — money that could be ~$81,000 by retirement — on the table.

Treating it like a tax-free 529

Trump Account withdrawals are taxed as ordinary income, like a traditional IRA. Families who assume it's tax-free college money get an unpleasant surprise when the growth is taxed. Use a 529 for college; use the Trump Account for the long game.

Business owners ignoring the $2,500 contribution

This is the biggest miss on the employer side. Owners hand out taxable bonuses when a $2,500 tax-free Trump Account contribution delivers more value to the employee at a similar cost to the business — and buys real loyalty.

Blowing past the $5,000 cap

The employer's $2,500 counts toward the $5,000 limit. If your employer contributes $2,500 and you also add $5,000, you've over-contributed. Coordinate the family and employer pieces so the total lands at or under $5,000.

Skipping the written employer program

An employer contribution only gets tax-free treatment if it's made under a documented Trump Account contribution program and coded correctly in payroll. A casual gift to one employee, recorded as a bonus, is just taxable wages with extra steps.

The 406 Trump Account Playbook

Here's the step-by-step we walk Montana families and business owners through. Follow it in order — the sequence matters, because the free money and the tax-free money come first.

Claim the $1,000 (if you qualify)

If your child was born 2025–2028 and is a U.S. citizen with an SSN, make the election through Form 4547 or TrumpAccounts.gov. This is the free-money step and it's the one most families haven't done.

Decide your annual number

Pick a realistic yearly contribution up to $5,000. Even $50/month ($600/year) started at birth compounds meaningfully over 18 years. You don't have to max it to make it worthwhile.

If you own a business, set up the employer program

Put a written $2,500-per-employee contribution program in place and code it correctly in payroll. This is the highest-leverage move for owners — tax-deductible for you, tax-free for your crew.

Layer it in the Family Wealth Stack

Add a 529 for college (and the Montana deduction), and a Roth once your child has earned income. The Trump Account is the base, not the whole plan.

Review it once a year

Contribution limits index after 2027, IRS regulations are still being finalized, and your income and goals change. A quick annual review keeps the whole stack coordinated and compliant.

The rules here are new and the IRS has said more regulations are coming. If you're a business owner deciding how to structure a contribution program, or a family trying to fit a Trump Account into a bigger plan, this is worth a conversation with someone who does tax planning and advisory work for a living — not a one-size-fits-all download. Run your own S-Corp and payroll numbers first with our S-Corp Calculator.

Frequently Asked Questions: Trump Accounts

What is a Trump Account?

A Trump Account is a tax-deferred investment account for a child, created by the One Big Beautiful Bill Act (the Working Families Tax Cuts) signed July 4, 2025. Eligible children born 2025–2028 receive a one-time $1,000 federal deposit. The money is invested in a low-cost fund tracking a U.S. stock index and grows tax-deferred until the child turns 18, at which point the account is treated as a traditional IRA. Families and employers can contribute up to $5,000 per child per year.

Who is eligible for the $1,000 Trump Account contribution?

The one-time $1,000 federal seed goes to children who are U.S. citizens at birth, born between January 1, 2025 and December 31, 2028, who have a Social Security number and whose parents have work-eligible Social Security numbers. An election must be made for the child (via IRS Form 4547 or TrumpAccounts.gov) — the $1,000 is not deposited automatically. Children outside that birth window can still have a Trump Account opened and funded; they just don't receive the seed.

How much can you contribute to a Trump Account each year?

Up to $5,000 per child per year from all sources combined — parents, family, others, and employers — during the growth phase from birth to age 18. This limit is indexed to inflation starting after 2027. The one-time $1,000 government seed and certain qualified rollovers do not count toward the $5,000. Contributions could not be made before July 4, 2026.

Can my business contribute to my employees' Trump Accounts?

Yes. An employer can contribute up to $2,500 per employee per year to the Trump Account of the employee's dependent child (or a young employee). The contribution is excluded from the employee's taxable income and is deductible to the business. The $2,500 limit is per employee, not per child — it does not multiply by the number of kids — and it counts toward the overall $5,000 annual limit. To preserve the tax treatment, the contribution must be made under a documented employer Trump Account contribution program and recorded correctly in payroll.

How are Trump Account withdrawals taxed?

Once the child turns 18, the account is treated as a traditional IRA. Withdrawals of the account's growth (and of pre-tax amounts like the seed and employer contributions) are taxed as ordinary income, and a 10% early-withdrawal penalty applies before age 59½ unless an exception applies — such as qualified higher-education expenses or up to $10,000 for a first-time home purchase. After-tax contributions come back out tax-free. This is different from a 529, where qualified education withdrawals are entirely tax-free.

Trump Account vs. 529 plan — which is better?

They do different jobs, so most families use both. A 529 is the better vehicle for college: withdrawals for qualified education are tax-free, and Montana residents get a state income tax deduction (through Achieve Montana) for contributing. A Trump Account is a long-term, retirement-style head start — it offers the free $1,000 seed and decades of tax-deferred growth, but withdrawals are taxed as ordinary income like a traditional IRA. Claim the Trump Account's free $1,000 first, then use a 529 for college savings.

When can I start contributing to a Trump Account?

Family and employer contributions could not be made before July 4, 2026. As of mid-2026 that date has passed, so contributions can now be made up to the $5,000 annual limit. You can make the eligibility election and claim the $1,000 seed independently of making contributions.

How do I open a Trump Account?

A parent or guardian opens a Trump Account for an eligible child using IRS Form 4547 (Trump Account Election(s)) or the online portal at TrumpAccounts.gov. You'll need the child's Social Security number. If your child qualifies for the $1,000 seed, making the election is what triggers that deposit — so filing promptly matters.

Official Sources

Related Tools & Resources

Tax Planning & Advisory

A New Benefit for Your Family — and a Recruiting Edge for Your Business.

406 Consulting Group helps Montana families claim what they're owed and helps business owners build a Trump Account contribution program that's structured, deductible, and actually competes for talent. Let's figure out the right play for your situation.

Trump Account Quick Reference

The numbers that matter

Own a Business?

$2,500 tax-free per employee is a real retention tool.

The Family Wealth Stack

Which account for which goal

Trump Account

Free $1,000 + long-term head start

529 Plan

College (Montana state deduction)

Roth IRA (kids)

Retirement, once they earn income

Custodial / UTMA

Flexible, anything for the child

About the Author

Carrie Anderson

Co-Founder, 406 Consulting Group

Background in commercial banking and underwriting — 300+ loan reviews — plus small business tax strategy and financial advisory across Montana. Carrie helps Montana families and owners turn new tax law into concrete, dollars-and-cents plans.

Read the Full Story