Expert Virtual CFO Guidance

for Boise, ID Business Owners

Boise businesses between $1M and $10M in revenue need CFO-level financial leadership — cash flow forecasting, lender relationships, and strategic planning — without the cost of a full-time hire.

Boise is in a growth cycle that is creating a very specific financial problem for the businesses driving it. Revenue is up. Headcount is growing. Complexity — vendors, payroll, financing, taxes, multiple entities — is compounding. But the financial infrastructure most of these businesses have is the same one they built when they were a fraction of their current size: a bookkeeper, a seasonal CPA, and a spreadsheet. That gap — between the financial complexity of a growing business and the financial leadership available to manage it — is exactly what a virtual CFO fills.

A virtual CFO is not a bookkeeper who does more. It is not a CPA who gives year-end advice. It is CFO-level strategic financial leadership — cash flow forecasting, financial modeling, lender relationships, KPI management, tax strategy coordination, and financial planning — delivered on a fractional basis at a cost that works for a growing Boise business that is not yet ready for a $200,000 full-time CFO hire.

Carrie Anderson co-founded 406 Consulting Group after years in commercial banking, where she reviewed and financed business growth across Montana and the Pacific Northwest. Her background is the CFO's most valuable context: she knows what lenders actually look at, what financial statements need to look like to open capital doors, and what the gap between a good-looking business and a bankable one actually costs in real dollars.

Table of Contents

Why Boise Businesses Need CFO-Level Financial Guidance

Boise has grown faster than almost any metropolitan area in the country over the past decade — and the businesses that have grown with it face a financial infrastructure problem that most do not recognize until it becomes expensive. The problem is not bad accounting. It is the gap between what a bookkeeper and seasonal CPA can provide and what a business at $1M–$10M in revenue actually needs.

$1M–$5M

The revenue range where most Boise businesses outgrow their bookkeeper but have not yet hired CFO-level leadership

72%

Of businesses that fail cite cash flow problems as a contributing factor — almost all of which are preventable with proper forecasting

3–6 months

Typical lag between when a business needs CFO guidance and when it acts — the gap where the most costly decisions are made without it

You are making major financial decisions without a model

Equipment purchases, new hires, office space expansions, pricing changes — these are financial decisions that should be modeled before they are made. If you are making them based on gut feel and a bank balance, you are operating without CFO-level guidance and the decisions reflect it.

Your bookkeeper cannot answer forward-looking financial questions

Bookkeepers record what happened. A CFO tells you what is going to happen — cash position in 90 days, margin impact of a new product line, what the business is worth if you needed to sell it today. If your financial team cannot answer these questions, you do not have CFO coverage.

Banks have declined a loan or offered worse terms than expected

A lender's decision reflects the quality of the financial information in front of them. Businesses with CFO-prepared financial packages — clean statements, a defensible narrative, DSCR and working capital clearly presented — borrow on materially better terms than businesses that show up with QuickBooks reports and optimism.

Tax surprises are a recurring event

A business with CFO-level oversight does not have surprise tax bills in April. Quarterly estimated payments, year-end planning, entity election optimization, and tax strategy coordination with the CPA are standard CFO functions. Surprise tax bills are a symptom of no one doing this work.

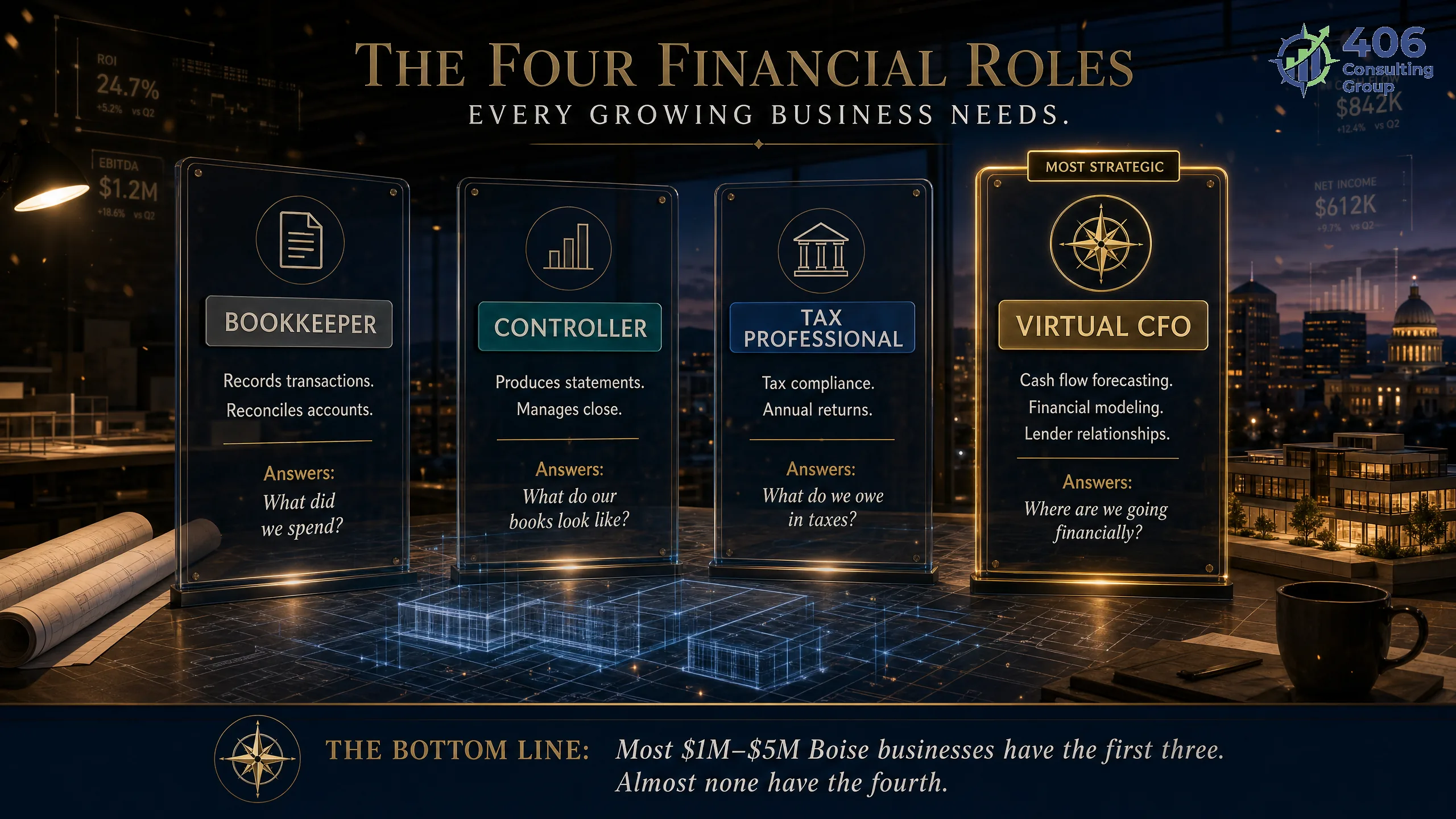

What a Virtual CFO Actually Does

The most common confusion in financial services for small businesses is what each role actually does. Bookkeeper, controller, CPA, and CFO — each fills a distinct function, and growth businesses routinely have one or two of these when they need all four. Here is how they differ, and what the CFO layer specifically adds.

| Role | Primary Function | Time Orientation | Typical Cost (Boise) | Answers |

|---|---|---|---|---|

| Bookkeeper | Records transactions, reconciles accounts, maintains the general ledger | Backward-looking | $500–$2,000/mo | "What did we spend?" |

| Controller | Produces accurate financial statements, manages close process, ensures accounting accuracy | Current-state | $2,000–$5,000/mo | "What do our financials look like right now?" |

| CPA | Tax compliance, tax return preparation, IRS representation | Annual / backward-looking | $1,500–$5,000/yr (returns only) | "What do we owe in taxes?" |

| Virtual CFO | Cash flow forecasting, financial strategy, lender relationships, KPI management, tax strategy coordination, financial modeling | Forward-looking | $2,500–$8,000/mo | "Where are we going financially — and how do we get there?" |

Cash Flow Forecasting

A 13-week rolling cash flow forecast updated weekly — the single most valuable financial tool for a growing business. Shows where the cash crunch is coming 60 days before it arrives, when to draw on a line of credit, and when cash position is strong enough to make an investment.

Financial Modeling and Scenario Planning

What does the P&L look like if we hire two engineers? What if revenue drops 20%? What if we raise prices 15%? A CFO builds the models that let you evaluate decisions before you make them — not discover their consequences six months later.

Lender Relationship Management

Knowing what a banker looks at — DSCR, working capital ratio, debt-to-equity, trend in revenue and EBITDA — and presenting your financials in a way that answers those questions before they are asked. A CFO with a banking background (like Carrie's) has sat on the other side of that table.

KPI Dashboard and Reporting

Monthly management reporting that gives you the 8–12 numbers that actually indicate business health: gross margin by product line, revenue per employee, cash conversion cycle, customer acquisition cost, lifetime value. Not a dump of QuickBooks data — a curated view of what matters.

Tax Strategy Coordination

The CFO coordinates with the CPA so that entity elections, quarterly payments, year-end deductions, and financial structure decisions are made proactively — not discovered at filing. The CFO does not replace the CPA; they make the CPA's work more effective.

Strategic Financial Planning

Annual budget, quarterly reforecasts, 3-year financial projections. A plan the business is actually managed against — with variance analysis each month that shows where you are ahead, where you are behind, and why. The difference between managing a business and reacting to one.

The Boise Business Financial Command Framework

The Boise Business Financial Command Framework organizes a virtual CFO engagement into four sequential phases. Each phase has a specific objective, a set of deliverables, and a clear indicator that the business is ready to move to the next phase. Most businesses engaging a CFO for the first time start in Phase 1 — regardless of revenue — because financial visibility is the prerequisite for everything that follows.

Phase 1: Visibility

Establish a clear, accurate picture of the business's financial reality — where money comes from, where it goes, and what the business is actually worth.

- Baseline financial assessment — current P&L, balance sheet, cash position

- Identification of accounting gaps, personal expenses in books, inconsistent categorization

- First 13-week cash flow forecast

- Chart of accounts cleanup and financial reporting structure

- Owner compensation analysis — market rate vs. current draw

Phase complete when: You can answer: What is our gross margin? What is our cash position in 60 days? What was our EBITDA last year? — without having to call your bookkeeper.

Phase 2: Control

Establish financial processes, controls, and reporting systems that produce reliable information on time — every month, without heroic effort.

- Monthly financial close process established (by the 10th of each month)

- KPI dashboard live — 8–12 metrics tracked monthly

- Accounts receivable and payable aging monitored

- Expense approval thresholds and controls implemented

- Quarterly estimated tax payments calculated and calendared

Phase complete when: You receive a monthly financial package by the 10th. You know your key metrics without asking. Financial surprises are rare.

Phase 3: Strategy

Use clean, reliable financial information to make forward-looking decisions — budgets, pricing, hiring, capital, and growth planning.

- Annual budget built and approved

- Quarterly reforecast vs. budget variance analysis

- 3-year financial model for growth planning

- Pricing and margin analysis by product/service line

- Capital planning — when to borrow, how much, what for

Phase complete when: You make major business decisions with a financial model in front of you. You know what the business can afford and what it cannot.

Phase 4: Scale

Use financial infrastructure to actively support growth — bank financing, investor capital, acquisitions, succession, or geographic expansion.

- Lender-ready financial package for business financing

- Investor deck financial model and projections (if applicable)

- M&A or acquisition financial due diligence support

- Succession or exit financial preparation

- Multi-entity financial consolidation and management

Phase complete when: Your financial infrastructure is an asset — it opens capital, supports acquisitions, and creates options the business did not previously have.

Trigger Events — When Your Boise Business Needs a Virtual CFO

Most business owners wait too long to engage CFO-level guidance. The right time is before the problem — not after. Here are the specific trigger events that reliably indicate a business needs CFO-level oversight, with the cost of waiting at each.

Revenue crossed $1M and you still don't know where the money goes

Cost of waiting: Every month without a clear financial picture is a month of missed optimization. Businesses at $1M+ with no P&L visibility typically have $80K–$200K in margin improvement available.

Get a CFO baseline assessment before the next quarter.

A bank loan was declined or terms came back weaker than expected

Cost of waiting: A declined loan or a loan at a higher rate than a better-prepared competitor pays represents real cost. A business borrowing $500K at 9.5% instead of 7.5% pays $10K/year in excess interest — every year the loan is outstanding.

A CFO prepares the financial package that changes the conversation with lenders.

You have no idea what your cash position will be in 90 days

Cost of waiting: A cash crunch that arrives as a surprise costs significantly more to manage than one anticipated 60–90 days out. Emergency credit lines, missed vendor discounts, and reactive decisions under pressure all cost more than proactive planning.

A 13-week cash flow forecast is the first deliverable a CFO produces.

You are considering a major hire, acquisition, or capital investment

Cost of waiting: A hiring decision made without a financial model for its impact on margin and cash flow is a guess. An acquisition evaluated without proper due diligence and financial modeling is a risk. These are CFO-level decisions.

Engage a CFO before the decision — not after, when options are limited.

Tax surprises are recurring — large bills or large refunds in April

Cost of waiting: Large unexpected tax bills disrupt cash flow and signal that no one is managing quarterly estimated payments. Large refunds mean the business overpaid the government throughout the year — free loan to the IRS.

A CFO coordinates quarterly tax planning with your CPA — no April surprises.

Key employees are asking about equity or you are considering partners

Cost of waiting: Equity grants, partner buyins, and profit-sharing arrangements without a clear financial model for what they actually cost the business — and what they are worth to the recipient — routinely create disputes and unexpected costs.

A CFO models the financial impact of any equity or ownership change before it is offered.

You are planning to sell, raise outside capital, or exit in the next 3–5 years

Cost of waiting: Businesses that begin financial preparation for exit 3–5 years out sell for significantly more — and on better terms — than businesses that begin 12–18 months out. Clean books, normalized EBITDA, and a documented financial track record take years to build.

Start Phase 1 of the Financial Command Framework now, not when the conversation gets serious.

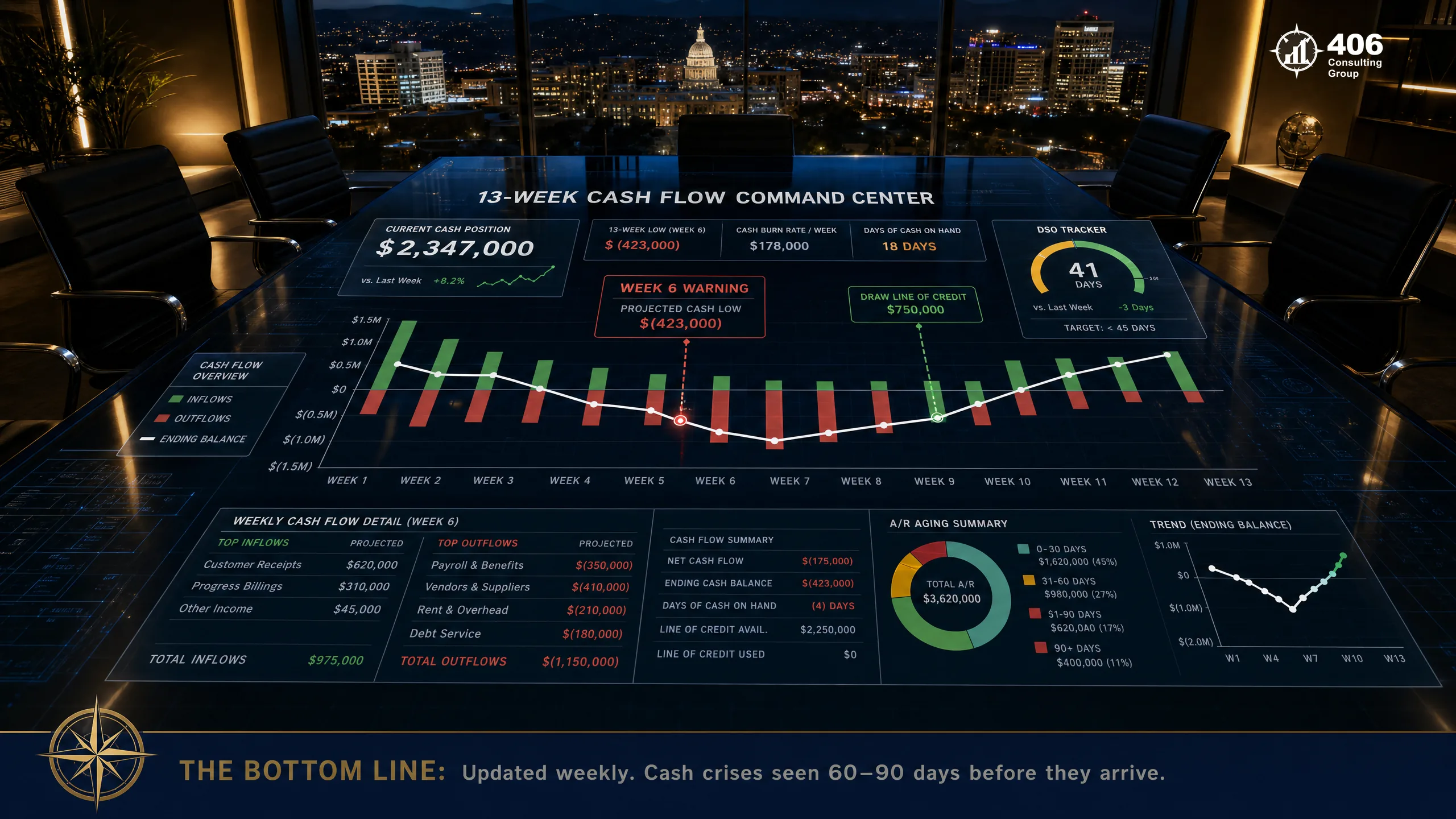

Cash Flow Forecasting and Management

Cash flow is not the same as profit. A profitable business can run out of cash — and many Boise businesses do, particularly those growing fast, carrying significant receivables, or managing seasonal demand. The CFO's primary operational tool for cash management is the 13-week rolling cash flow forecast.

The 13-Week Rolling Cash Flow Forecast

A weekly projection of cash receipts and disbursements for the next 13 weeks (one quarter), updated weekly. The forecast shows beginning cash balance, projected inflows (collections from customers, loan draws), projected outflows (payroll, rent, vendor payments, tax payments, debt service), and ending cash balance. The rolling structure means the forecast always looks 13 weeks forward — not just to quarter-end. Updated weekly against actuals so variances are visible and explainable before they become crises.

Receivables Management Integration

For businesses with significant accounts receivable — construction companies billing on draws, professional service firms invoicing monthly, technology companies with net-30 terms — the largest variable in cash flow is when customers actually pay. A CFO monitors DSO (days sales outstanding) monthly and actively manages the receivables cycle: when to invoice, when to follow up, when to tighten terms, and when to use a line of credit to bridge the gap.

Line of Credit Strategy

A revolving line of credit is the right working capital tool for most Boise businesses with receivables or inventory — but only if it is used strategically. The CFO determines the right line size (typically 10–15% of annual revenue), maintains the banking relationship, and manages draws against the cash flow forecast so the line is used when genuinely needed and paid down when cash position allows. A line drawn for operating expenses — not working capital timing — is a warning sign.

Seasonal Cash Flow Planning

Boise's construction, tourism, and agricultural-adjacent businesses have material seasonal cash flow patterns. A CFO builds the seasonal shape of the business into the cash flow model — planning for the trough periods (typically Q1 for many Boise industries) with cash reserves built in Q3/Q4. Businesses that run lean year-round often find themselves in cash emergencies in February and March that were entirely predictable in October.

Lender-Ready Financials and Banking Relationships

Carrie Anderson spent years in commercial banking reviewing business loan applications — which means she knows what the banker is actually looking for before the application is submitted. Most business owners prepare for a loan the way they would prepare for a job interview: they put their best foot forward and hope for the best. A CFO with a lending background prepares a financial package the way an underwriter reads it.

What Boise Lenders Actually Evaluate

| Metric | Lender Standard | What It Measures |

|---|---|---|

| Debt Service Coverage Ratio (DSCR) | ≥1.25× (most lenders) | Net operating income ÷ total debt service. Shows the business generates enough cash to cover its loan payments with a 25% buffer. |

| Working Capital Ratio | ≥1.2× (preferred ≥1.5×) | Current assets ÷ current liabilities. Shows the business can pay its short-term obligations. |

| Debt-to-Equity Ratio | ≤3:1 for most commercial loans | Total liabilities ÷ owner's equity. Higher ratios signal the business is heavily leveraged. |

| Revenue and EBITDA Trend | 3 years consistent or growing | Lenders want to see trajectory, not a single year of strong performance. |

| Financial Statement Quality | CPA-compiled or reviewed preferred | Owner-prepared statements carry a risk discount. CPA involvement signals reliability. |

| Owner Personal Financial Statement | Strong personal credit (680+ FICO) | Personal guarantee is standard. Owner's personal financial health is part of the underwriting. |

The CFO's role in a loan process: A CFO prepares the complete loan package — normalized financial statements, EBITDA bridge, cash flow projections, business narrative, and a clear presentation of collateral and ownership. The CFO also selects the right lender (SBA vs. conventional vs. credit union vs. USDA for rural-adjacent Boise businesses) and presents the package in the format each lender expects. See what commercial lenders actually evaluate for the full breakdown.

Strategic Financial Planning for Boise's Growth Market

Boise's growth creates genuine strategic decisions that financial models should inform: when to open a second location, when the current team is the growth constraint vs. capital, whether to buy or lease equipment, what pricing actually needs to be to hit a profitability target. Strategic financial planning is the CFO function that translates business goals into financial models and financial models into decisions.

Annual Budget

Built from the ground up — revenue by product/service line, headcount and compensation planning, operating expense by category, capital expenditures, and debt service. The budget is the benchmark every month's actual performance is compared against.

Quarterly Reforecast

As the year progresses, the budget becomes less accurate. A quarterly reforecast updates projections based on actual performance — so year-end expectations are realistic and year-end planning decisions are made with current information.

3-Year Financial Model

Where is the business going over the next 3 years under conservative, base, and optimistic scenarios? The 3-year model drives capital planning, hiring planning, and the conversations with lenders and investors who want to understand the business's trajectory.

Pricing Strategy and Margin Analysis

Most Boise businesses do not know their gross margin by product or service line — they know the blended average. A CFO builds a margin analysis by line, identifies which services are subsidizing which, and models the P&L impact of pricing changes before they are implemented. A 5% price increase on 60% of revenue that the market will absorb is worth more than a year of cost-cutting.

Hiring Impact Modeling

Each incremental hire has a revenue break-even — the point at which the new employee generates enough additional revenue (or frees up enough owner time) to cover their fully loaded cost. A CFO models this before the hire decision, not after the offer is accepted.

Capital Expenditure Analysis

Buy vs. lease, financed vs. cash, now vs. next year — equipment and facility decisions for growing Boise businesses involve tax implications (Section 179, bonus depreciation), cash flow timing, and balance sheet impact. A CFO runs the numbers under each scenario and presents a recommendation.

KPIs and Financial Dashboard Management

A CFO does not give you every number in the financial statements — they give you the 8–12 numbers that actually indicate where the business is and where it is going. The right KPIs differ by business model, but most Boise businesses at the $1M–$10M range need to be tracking the following metrics monthly.

Profitability KPIs

Gross Margin %

(Revenue − COGS) ÷ RevenueThe most fundamental profitability metric. If gross margin is deteriorating, the business is working harder for less — before overhead.

EBITDA Margin %

EBITDA ÷ RevenueOperating profitability before financing and taxes. The metric lenders and acquirers use to value the business.

Net Profit Margin %

Net Income ÷ RevenueBottom-line profitability after all costs. Should be growing as revenue scales — if not, overhead is growing faster than revenue.

Cash and Liquidity KPIs

Days Sales Outstanding (DSO)

(AR Balance ÷ Revenue) × Days in PeriodHow long it takes to collect after invoicing. Every day of DSO above your target is cash sitting on someone else's balance sheet.

Operating Cash Flow

Cash from Operations (direct or indirect)The cash the business actually generates from operations — not accounting profit, not bank balance. The most important number on the cash flow statement.

Current Ratio

Current Assets ÷ Current LiabilitiesShort-term liquidity. Below 1.0 means current liabilities exceed current assets — a stress indicator that lenders see immediately.

Growth and Efficiency KPIs

Revenue per Employee

Total Revenue ÷ FTE HeadcountProductivity benchmark. Growing revenue without growing headcount proportionally means efficiency is improving. The inverse is a warning sign.

Customer Acquisition Cost (CAC)

Total Sales & Marketing Spend ÷ New CustomersWhat it costs to acquire one new customer. Should be declining as the business matures — rising CAC signals increasing competition or declining marketing efficiency.

Revenue Concentration

Top Customer Revenue ÷ Total RevenueA business where one customer represents 30%+ of revenue has material concentration risk — and lenders will discount the value of that revenue accordingly.

Operational KPIs (Business-Type Specific)

Backlog (Construction/Project)

Value of signed contracts not yet recognized as revenueForward revenue visibility. A 6+ month backlog is a strong lender and management indicator.

Utilization Rate (Services)

Billable Hours ÷ Available HoursThe core efficiency metric for professional service businesses. Below 65% typically means pricing or staffing needs adjustment.

Inventory Turnover (Product/Retail)

COGS ÷ Average InventoryHow fast inventory sells. Low turnover means capital tied up in slow-moving stock — a cash flow constraint.

Coordinating Tax Strategy with CFO-Level Oversight

The CFO is not the CPA — but in a well-run business, the CFO and CPA are working together throughout the year, not just at tax filing time. The CFO provides the forward-looking financial picture that allows the CPA to make proactive, not reactive, tax decisions. This coordination is where most of the tax savings actually come from.

Quarterly Estimated Payment Management

The CFO monitors actual income against the year's projection throughout the year and adjusts estimated tax payments accordingly. No more April surprises — and no more overpaying the IRS with large quarterly payments when income has fallen short of projections.

Entity Election Timing

S-Corp elections, accounting method changes, and entity restructuring all have specific filing deadlines. The CFO identifies when these decisions need to be made and coordinates with the CPA to ensure the window is not missed. An S-Corp election missed by a week costs a full year of excess SE tax.

Year-End Tax Planning

In Q4, the CFO produces a year-end tax projection: what is the estimated tax liability based on year-to-date income, what deductions are still available, what purchases should be made before December 31, and what income should be deferred to January. This is the planning session that changes the April tax bill.

Compensation Structure Optimization

For S-Corp owners, the split between W-2 salary and distributions determines self-employment tax exposure. The CFO models the optimal compensation structure throughout the year — not in April after the return is already filed. A $20K difference in salary-to-distribution ratio at $400K income is worth roughly $3,000 in annual tax savings.

For Boise business owners using virtual tax preparation services — the CFO engagement and the tax preparation engagement work best when coordinated. The CFO provides the financial context; the tax preparer applies it to the return. Bundling both with 406 Consulting Group ensures the two are never working from different information.

What to Expect from a Virtual CFO Engagement

A virtual CFO engagement is structured differently from a one-time project or a seasonal relationship. Here is what the cadence of a mature virtual CFO engagement looks like — what gets delivered, when, and in what format.

- Baseline financial assessment — review of prior 2–3 years of financials

- Accounting software access and chart of accounts review

- First 13-week cash flow forecast built

- KPI dashboard framework established

- Introduction to banking relationships and existing lenders

- Tax situation review — coordination with existing CPA or referral

- Monthly financial close support (by the 10th of each month)

- P&L, balance sheet, and cash flow statement review with management commentary

- KPI dashboard updated with prior month actuals

- Cash flow forecast updated (rolling 13-week)

- Budget vs. actual variance analysis with explanation

- Tax estimated payment reminders and updates

- 90-minute video call: quarterly financial review

- Budget reforecast for remaining quarters

- Q-specific tax planning update with CPA coordination

- Banking relationship update — covenant compliance, any financing needs on the horizon

- Strategic initiative financial update — are the key decisions of the quarter on track financially?

- Annual budget development for the coming year

- 3-year financial model update

- Year-end tax planning session with CPA

- Annual banking review — is the current credit structure optimal?

- CFO assessment — what changed in the business this year, what does the financial infrastructure need to look like next year?

Virtual CFO vs. Full-Time CFO — Cost Comparison

The fully loaded cost of a full-time CFO in Boise is typically $180,000–$280,000 per year when salary, benefits, payroll taxes, and equity are included. For a business between $1M and $10M in revenue, that hire often does not make financial sense — not because CFO-level work is not needed, but because it is not needed full time. A virtual CFO delivers 80–90% of the value at 20–30% of the cost.

| Factor | Virtual CFO | Full-Time CFO |

|---|---|---|

| Annual Cost | $30,000–$96,000/yr ($2,500–$8,000/mo) | $180,000–$280,000/yr (all-in) |

| Time to Productive | 2–4 weeks (experienced, no learning curve) | 3–6 months (hiring process + ramp-up) |

| Availability | Responsive year-round; scales with business needs | Full-time on-site or remote; fixed cost regardless of need |

| Expertise | Access to team with cross-industry experience; brings pattern recognition from multiple businesses | One person's experience; deep in one industry |

| Scalability | Scope adjusts as the business grows — start focused, expand to full CFO suite | Fixed salary; difficult to reduce scope if business hits a down period |

| Best For | $1M–$15M revenue; businesses that need CFO-level thinking but not full-time presence | $15M+ revenue or businesses with complex, daily CFO demands (M&A activity, investor board, rapid multi-location scaling) |

See the detailed breakdown in what a fractional CFO costs and what ROI to expect — including how to evaluate whether the engagement pays for itself and at what revenue level a full-time hire makes sense.

Industry-Specific CFO Services for Boise Businesses

The financial infrastructure a Boise technology company needs is materially different from what a construction firm or a healthcare practice needs. A CFO who specializes in your industry brings pattern recognition — the problems you are about to face, the metrics that actually matter, and the capital strategies that work in your specific business model.

Technology & Software Companies

- Runway management — how many months of cash at current burn rate?

- SaaS metrics — MRR, ARR, churn rate, LTV:CAC ratio

- R&D capitalization under Section 174 (post-2022 amortization requirement)

- Fundraising financial model — investor deck projections and scenario analysis

- Revenue recognition — particularly for multi-year contracts or milestone-based projects

Boise's technology sector is growing rapidly, and the most common CFO failure mode for tech companies is runway management. A CFO who tracks burn rate weekly and models the fundraising timeline prevents the cash crisis that kills otherwise viable companies.

Construction & Contractors

- WIP (work-in-progress) management and job costing accuracy

- Bonding capacity — maintaining the financial ratios that support larger bonding limits

- Equipment financing strategy — owned vs. leased, Section 179, depreciation timing

- Subcontractor payment management and lien waiver tracking

- Percentage-of-completion vs. completed contract accounting method election

Construction is the industry where the gap between accounting and CFO-level financial management is widest — and most costly. A contractor who wins the jobs but loses the margin has a CFO problem, not an estimating problem. Accurate job costing and WIP management are the difference.

Healthcare & Medical Practices

- EBITDA optimization for practice valuation (DSO-based practices have specific valuation multiples)

- Payer mix analysis — revenue by insurance carrier and reimbursement rate trends

- Physician compensation modeling — partnership track, relative value units, profit sharing

- Practice acquisition or expansion financial modeling

- Billing department efficiency — collections as a percentage of charges, denial rates

Healthcare practices are increasingly acquisition targets — and the acquirer's price is driven by EBITDA and clean financial records. A CFO who tracks the metrics that drive practice valuation (and cleans up the books that support it) creates tangible transaction value.

Professional Services

- Utilization rate management — billable hours as a percentage of available hours

- Pricing and rate modeling — when to raise rates and by how much

- Partner compensation modeling — equity buyouts, profit distribution structures

- Client concentration risk monitoring and management

- Overhead allocation and profit center reporting by practice area or team

Professional service firms live and die on utilization and billing rates. A CFO who tracks utilization monthly and models the revenue impact of rate increases against client retention gives partners the data they need to make confident decisions about both.

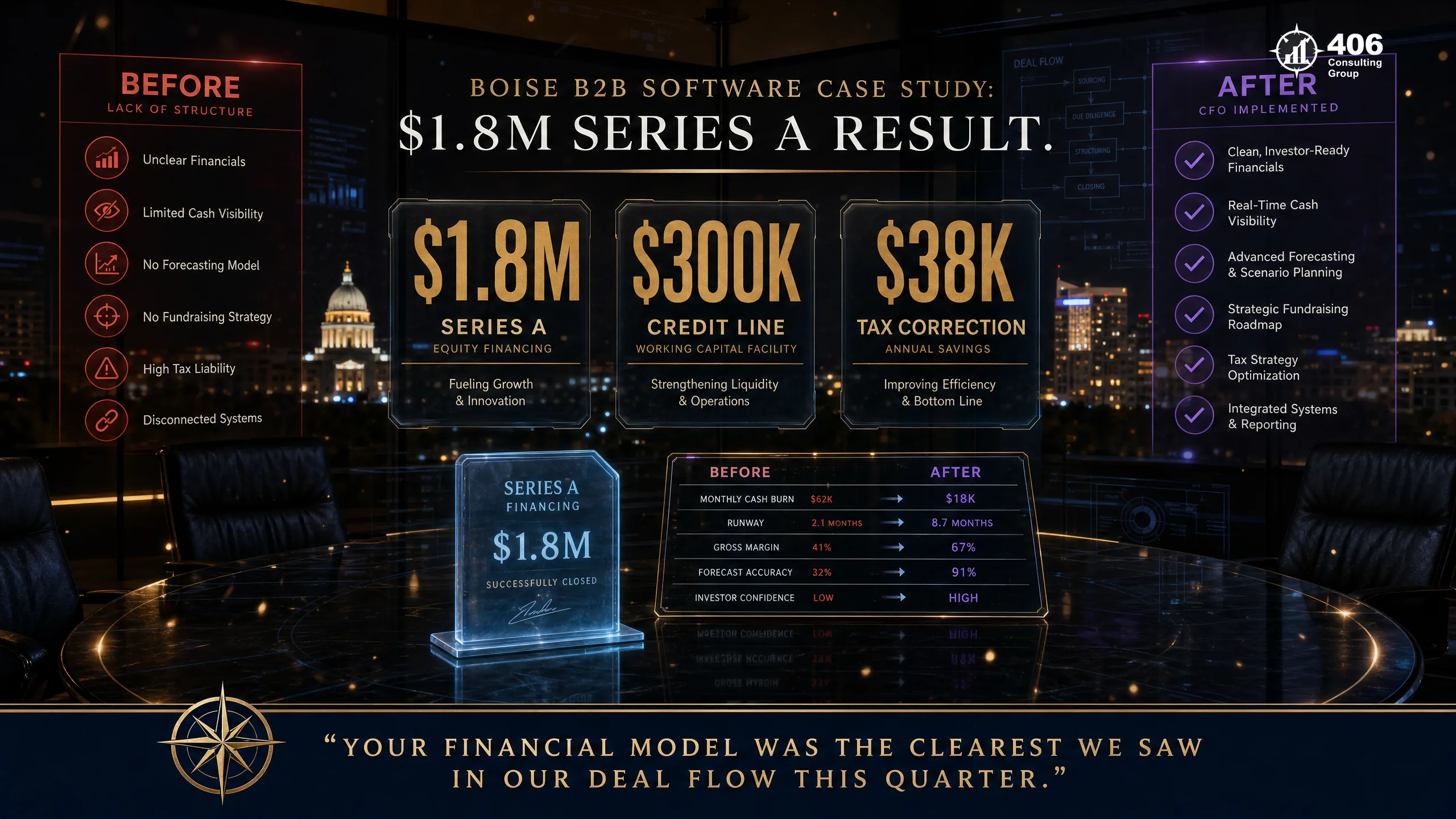

Case Study: Boise Technology Company — Series A Ready in 14 Months

Anonymized — Boise, Idaho

B2B Software Company — 12 Employees, $2.4M ARR

When We Were Engaged

- Growing fast — $2.4M ARR, 40% YoY growth — but no CFO-level financial infrastructure

- Books were cash-basis; revenue recognition not aligned with GAAP — a problem for any investor diligence

- No financial model, no investor deck projections, no 3-year forecast

- Burn rate tracked informally — founders did not know runway within 2 months of accuracy

- R&D costs expensed immediately despite Section 174 requiring amortization for domestic software development

- No banking relationship — payroll and operations run through a consumer bank account

14 Months Later

- Books restated to accrual / GAAP-basis; revenue recognition policy documented and consistently applied

- 3-year financial model built with MRR, churn, expansion revenue, and headcount plan

- Investor deck financial section: full model with base/bull/bear scenarios and use-of-funds waterfall

- Banking relationship established with a Boise commercial bank — $300K line of credit approved

- Section 174 amortization properly applied — $38K tax correction avoided future audit exposure

- $1.8M Series A round closed — lead investor cited financial model quality as a key diligence factor

$1.8M

Series A round closed — 14 months after CFO engagement began

$300K

Commercial line of credit approved — first institutional banking relationship

$38K

Tax correction avoiding Section 174 audit exposure

The lead investor's comment at close:"Your financial model was the clearest we saw in our deal flow this quarter. We knew exactly what we were investing in." That clarity is the product of 14 months of CFO-level financial infrastructure — books that are right, metrics that are tracked, a model that is built from the ground up, and a management team that can defend every number in the room.

FAQ: Virtual CFO Services for Boise Businesses

What is a virtual CFO?

A virtual CFO (also called a fractional CFO) is a Chief Financial Officer who works with your business on a part-time, fractional basis — delivering CFO-level strategic financial leadership without the cost of a full-time hire. A virtual CFO provides cash flow forecasting, financial modeling, lender relationship management, KPI tracking, tax strategy coordination, and strategic financial planning. For businesses between $1M and $15M in revenue, a virtual CFO typically delivers 80–90% of the value of a full-time CFO at 20–30% of the cost.

How is a virtual CFO different from a bookkeeper or CPA?

A bookkeeper records what happened — transactions, reconciliations, the historical record. A CPA handles tax compliance — returns, filings, and IRS representation. A virtual CFO looks forward — cash flow forecasting, financial modeling, strategic planning, lender relationships, and KPI management. In a well-run business, all three roles work together: the bookkeeper produces the data, the CFO uses it to make decisions and prepare for growth, and the CPA files the taxes. Most businesses between $1M and $5M have a bookkeeper and a CPA but no CFO — which means the forward-looking, strategic financial work is not being done.

When does a Boise business need a virtual CFO?

The clearest trigger events: revenue has crossed $1M and you do not know where the money goes; a bank loan was declined or came back at unfavorable terms; you cannot forecast your cash position 90 days out; you are making major financial decisions (hires, equipment, expansion) without a financial model; tax surprises are recurring; or you are planning to sell, raise capital, or take on a business partner in the next 3–5 years. The short answer: if your financial team cannot answer forward-looking questions — what will our cash position be in 60 days, what is the margin impact of this hire, what is the business worth today — you need CFO-level coverage.

What does a virtual CFO cost in Boise, ID?

Virtual CFO engagements for Boise businesses typically range from $2,500–$8,000 per month depending on scope, business complexity, and the deliverables included. A foundational engagement (cash flow forecasting, monthly financial review, quarterly planning) runs $2,500–$4,000/month. A full-scope engagement (all of the above plus lender relationship management, investor reporting, or transaction support) runs $5,000–$8,000/month. Compared to the all-in cost of a full-time Boise CFO ($180,000–$280,000/year), a virtual CFO delivering comparable strategic value typically costs 20–40% as much.

What financial deliverables does a virtual CFO provide monthly?

Standard monthly deliverables from a virtual CFO engagement: a complete financial package (P&L, balance sheet, cash flow statement) closed by the 10th of the month; a management commentary on the prior month results — what drove the numbers and what to watch; a KPI dashboard updated with prior month actuals; a rolling 13-week cash flow forecast updated for the current cash position; a budget vs. actual variance analysis with explanations; and any tax estimated payment reminders or updates. Quarterly, the CFO facilitates a 90-minute review call and updates the full-year reforecast.

Can a virtual CFO help my Boise business get a bank loan?

Yes — and this is one of the highest-ROI applications of CFO-level work for Boise businesses. A CFO prepares the financial package that lenders actually need: 3 years of clean, accrual-basis financial statements; a normalized EBITDA presentation; DSCR and working capital calculations; a business narrative; and cash flow projections. A business that shows up to a lender meeting with CFO-prepared materials borrows on materially better terms — and gets approved more often — than one presenting QuickBooks reports. Carrie Anderson's commercial banking background means she knows exactly what the underwriter needs to see before they see it.

Does 406 Consulting Group provide virtual CFO services in Boise?

Yes. 406 Consulting Group provides virtual CFO services for businesses in Boise, the Treasure Valley, and across Idaho and the Intermountain West. Our engagements include the full CFO scope: cash flow forecasting, financial modeling, lender relationship management, KPI dashboard, tax strategy coordination, and strategic planning. Carrie Anderson leads our CFO practice with a background in commercial banking — which means our CFO work is grounded in what lenders and investors actually need to see, not just what looks good on paper. Contact us to discuss what a virtual CFO engagement looks like for your specific business.

External Resources

Boise, ID & Treasure Valley

Virtual CFO Services for Boise Business Owners

406 Consulting Group provides CFO-level financial leadership for Boise businesses ready to scale — cash flow forecasting, lender relationships, financial modeling, and strategic planning delivered virtually, year-round.

Financial Command Framework

Which phase is your business in?

Visibility

Clear picture of financial reality

Control

Reliable monthly reporting and KPIs

Strategy

Budget, model, and forward planning

Scale

Capital, acquisitions, and growth

Virtual CFO vs. Full-Time

Related Reading

Ready for CFO-level clarity?

Virtual CFO services for Boise businesses — cash flow forecasting, lender relationships, financial modeling, and strategic planning.

Schedule a Consultation